e-commerce

Auto Added by WPeMatico

Auto Added by WPeMatico

On the heels of Heroes announcing a $200 million raise earlier today, to double down on buying and scaling third-party Amazon Marketplace sellers, another startup out of London aiming to do the same is announcing some significant funding of its own. Olsam, a roll-up play that is buying up both consumer and B2B merchants selling on Amazon by way of Amazon’s FBA fulfillment program, has closed $165 million — a combination of equity and debt that it will be using to fuel its M&A strategy, as well as continue building out its tech platform and to hire more talent.

Apeiron Investment Group — an investment firm started by German entrepreneur Christian Angermayer — led the Series A equity round, with Elevat3 Capital (another Angermayer firm that has a strategic partnership with Founders Fund and Peter Thiel) also participating. North Wall Capital was behind the debt portion of the deal. We have asked and Olsam is only disclosing the full amount raised, not the amount that was raised in equity versus debt. Valuation is also not being disclosed.

Being an Amazon roll-up startup from London that happens to be announcing a fundraise today is not the only thing that Olsam has in common with Heroes. Like Heroes, Olsam is also founded by brothers.

Sam Horbye previously spent years working at Amazon, including building and managing the company’s business marketplace (the B2B version of the consumer marketplace); while co-founder Ollie Horbye had years of experience in strategic consulting and financial services.

Between them, they also built and sold previous marketplace businesses, and they believe that this collective experience gives Olsam — a portmanteau of their names, “Ollie” and “Sam” — a leg up when it comes to building relationships with merchants; identifying quality products (versus the vast seas of search results that often feel like they are selling the same inexpensive junk as each other); and understanding merchants’ challenges and opportunities, and building relationships with Amazon and understanding how the merchant ecosystem fits into the e-commerce giant’s wider strategy.

Olsam is also taking a slightly different approach when it comes to target companies, by focusing not just on the usual consumer play, but also on merchants selling to businesses. B2B selling is currently one of the fastest-growing segments in Amazon’s Marketplace, and it is also one of the more overlooked by consumers. “It’s flying under the radar,” Ollie said.

“The B2B opportunity is very exciting,” Sam added. “A growing number of merchants are selling office supplies or more random products to the B2B customer.”

Estimates vary when it comes to how many merchants there are selling on Amazon’s Marketplace globally, ranging anywhere from 6 million to nearly 10 million. Altogether those merchants generated $300 million in sales (gross merchandise value), and it’s growing by 50% each year at the moment.

And consolidating sellers — in order to achieve better economies of scale around supply chains, marketing tools and analytics, and more — is also big business. Olsam estimates that some $7 billion has been spent cumulatively on acquiring these businesses, and there are more out there: Olsam estimates there are some 3,000 businesses in the U.K. alone making more than $1 million each in sales on Amazon’s platform.

(And to be clear, there are a number of other roll-up startups beyond Heroes also eyeing up that opportunity. Raising hundreds of millions of dollars in aggregate, others that have made moves this year include Suma Brands [$150 million], Elevate Brands [$250 million], Perch [$775 million], factory14 [$200 million], Thrasio [currently probably the biggest of them all in terms of reach and money raised and ambitions], Heyday, The Razor Group, Branded, SellerX, Berlin Brands Group [X2], Benitago, Latin America’s Valoreo and Rainforest and Una Brands out of Asia.)

“The senior team behind Olsam is what makes this business truly unique,” said Angermayer in a statement. “Having all been successful in building and selling their own brands within the market and having worked for Amazon in their marketplace team – their understanding of this space is exceptional.”

Powered by WPeMatico

Can reading glasses actually be cool? A new eyewear company called Cheeterz Club thinks so. The startup is working to change the perception of reading glasses from being just cheap, disposable items you pick up from a rotating display rack at your local drug store to being something you’d actually be proud to wear. To do so, the company is designing its glasses with quality lenses and frames in a range of styles, while still keeping the pricing affordable.

The startup — whose name is a reference to the slang term for glasses, “cheaters” — was founded by Jennifer Farrelly, whose background includes work in advertising and sales at companies like Uber and Virool.

She said the idea to make a better set of readers came to her because she found herself frustrated by the current options on the market.

“It all started a few years ago. My friends were posting on social media these really depressing comments and posts like: ‘I’m old and turning into my parents, this is awful.’ And I [thought to myself] why does it have to be like that? I feel just as young today as I did 10 years ago,” Farrelly explains. “Why are my friends and I feeling forced to feel old because of something that happens overnight?,” she says, of what felt like the sudden onset of middle age and the hardships it brings.

What’s worse, Farrelly says, is that when you finally make your way to the drugstore to pick out some reading glasses, all you’ll find are bad, plastic pairs that both look and feel cheap.

“That’s even more demoralizing,” she adds.

Image Credits: Cheeterz Club

So Farrelly teamed up with a former Warby Parker and Pair Eyewear head of Product, Lee Zaro, to design a new line of more fashion-forward eyewear.

Zaro, who is based in the LA area, immediately saw the opportunity.

“Drugstore reading glasses are typically poor in quality, and can feel like they are designed with our parents in mind, leaving a huge unmet need for sophisticated eyewear options,” he said. “When Jennifer approached me to help design her first line of eyewear, I knew it was a brilliant idea.”

To differentiate itself from lower-end readers, Cheeterz Club glasses are made with 100% acetate and feature spring hinges and stainless steel. The lenses, meanwhile, offer more clarity than is often found in reading glasses.

Image Credits: Cheeterz Club

Typically, ophthalmic plastic lens materials have an Abbe value — a measure of the degree at which light is dispersed or separated — between 30 and 58. The higher number offers better optical performance. Crown glass can have an Abbe value as high as 59, but polycarbonate readers (like those from Warby Parker, Farrelly notes) would have an Abbe value of 30. Cheeterz Club lenses, which are CR-39 lenses, are at at 58. This is a difference you can tell when trying the glasses on alongside your drugstore readers.

Cheeterz’ lenses also offer 100% UVA/UVB protection, and are oil and water repellent. They can optionally be bought in one of eight fashion tints, from pink to blue, or in two sun shades. Consumers can also opt to add Blue Light coating to help with screen-induced eye fatigue or they can choose Progressive lenses, which combine distance vision with a reading lens.

Tints are an extra $10, Blue Light protection is $25 and Progressive lenses are $40.99 — lower than market rates.

At launch, Cheeterz Club offers 42 different styles ranging from traditional to the more modern, starting at $28.99.

Farrelly says finding the right price was key, because unlike regular glasses, consumers often buy multiple pairs of readers to leave around the house or car, pack in purses and bags, and so on.

“If I break something that costs me a couple hundred dollars, I’d be really upset about it,” she says. “But at a drugstore price of under $30, I can have them in all sorts of colors and different tints.”

For Farrelly, making the startup a success goes beyond bringing higher-quality reading glasses to market. It’s also about serving a demographic that often gets overlooked.

“Founders in their forties do not get representation, and it’s unfortunate. And there are also people in their forties and fifties that have disposable income and are looking for cute things. They’re spending so much money on facial creams and Botox,” she says, “but then you’re forced to put this really ugly pair of glasses on your face that make you feel bad about yourself.”

While Cheeterz Club today is selling direct to the consumer, the company is talking to eye doctors, boutiques and others who may eventually resell for them, as more of a B2B model. It’s also testing selling on Amazon with one pair of Blue Light glasses.

Cheeterz Club plans to start discussing fundraising with seed investors later this fall.

Update, 8/31/21, 5:30 PM ET: Cheeterz Club incorrectly shared the number of frames available at launch. An earlier version of this article said it was 14, it’s actually 42, they said. We’ve updated with the new information.

Powered by WPeMatico

Heroes, one of the new wave of startups aiming to build big e-commerce businesses by buying up smaller third-party merchants on Amazon’s Marketplace, has raised another big round of funding to double down on that strategy. The London startup has picked up $200 million, money that it will mainly be using to snap up more merchants. Existing brands in its portfolio cover categories like babies, pets, sports, personal health and home and garden categories — some of them, like PremiumCare dog chews, the Onco baby car mirror, gardening tool brand Davaon and wooden foot massager roller Theraflow, category best-sellers — and the plan is to continue building up all of these verticals.

Crayhill Capital Management, a fund based out of New York, is providing the funding, and Riccardo Bruni — who co-founded the company with twin brother Alessio and third brother Giancarlo — said that the bulk of it will be going toward making acquisitions, and is therefore coming in the form of debt.

Raising debt rather than equity at this point is pretty standard for companies like Heroes. Heroes itself is pretty young: it launched less than a year ago, in November 2020, with $65 million in funding, a round comprised of both equity and debt. Other investors in the startup include 360 Capital, Fuel Ventures and Upper 90.

Heroes is playing in what is rapidly becoming a very crowded field. Not only are there tens of thousands of businesses leveraging Amazon’s extensive fulfillment network to sell goods on the e-commerce giant’s marketplace, but some days it seems we are also rapidly approaching a state of nearly as many startups launching to consolidate these third-party sellers.

Many a roll-up play follows a similar playbook, which goes like this: Amazon provides the marketplace to sell goods to consumers, and the infrastructure to fulfill those orders, by way of Fulfillment By Amazon and its Prime service. Meanwhile, the roll-up business — in this case Heroes — buys up a number of the stronger companies leveraging FBA and the marketplace. Then, by consolidating them into a single tech platform that they have built, Heroes creates better economies of scale around better and more efficient supply chains, sharper machine learning and marketing and data analytics technology, and new growth strategies.

What is notable about Heroes, though — apart from the fact that it’s the first roll-up player to come out of the U.K., and continues to be one of the bigger players in Europe — is that it doesn’t believe that the technology plays as important a role as having a solid relationship with the companies it’s targeting, key given that now the top marketplace sellers are likely being feted by a number of companies as acquisition targets.

“The tech is very important,” said Alessio in an interview. “It helps us build robust processes that tie all the systems together across multiple brands and marketplaces. But what we have is very different from a SaaS business. We are not building an app, and tech is not the core of what we do. From the acquisitions side, we believe that human interactions ultimately win. We don’t think tech can replace a strong acquisition process.”

Image Credits: Heroes

Heroes’ three founder-brothers (two of them, Riccardo and Alessio, pictured above) have worked across a number of investment, finance and operational roles (the CVs include Merrill Lynch, EQT Ventures, Perella Weinberg Partners, Lazada, Nomura and Liberty Global) and they say there have been strong signs so far of its strategy working: of the brands that it has acquired since launching in November, they claim business (sales) has grown five-fold.

Collectively, the roll-up startups are raising hundreds of millions of dollars to fuel these efforts. Other recent hopefuls that have announced funding this year include Suma Brands ($150 million); Elevate Brands ($250 million); Perch ($775 million); factory14 ($200 million); Thrasio (currently probably the biggest of them all in terms of reach and money raised and ambitions), Heyday, The Razor Group, Branded, SellerX, Berlin Brands Group (X2), Benitago, Latin America’s Valoreo and Rainforest and Una Brands out of Asia.

The picture that is emerging across many of these operations is that many of these companies, Heroes included, do not try to make their particular approaches particularly more distinctive than those of their competitors, simply because — with nearly 10 million third-party sellers today on Amazon globally — the opportunity is likely big enough for all of them, and more, not least because of current market dynamics.

“It’s no secret that we were inspired by Thrasio and others,” Riccardo said. “Combined with COVID-19, there has been a massive acceleration of e-commerce across the continent.” It was that, plus the realization that the three brothers had the right e-commerce, fundraising and investment skills between them, that made them see what was a ‘perfect storm’ to tackle the opportunity, he continued. “So that is why we jumped into it.”

In the case of Heroes, while the majority of the funding will be used for acquisitions, it’s also planning to double headcount from its current 70 employees before the end of this year with a focus on operational experts to help run their acquired businesses.

Powered by WPeMatico

As artificial intelligence continues to weave its way into more enterprise applications, a startup that has built a platform to help businesses, especially non-tech organizations, build more customized AI decision-making tools for themselves has picked up some significant growth funding. Peak AI, a startup out of Manchester, England, that has built a “decision intelligence” platform, has raised $75 million, money that it will be using to continue building out its platform, expand into new markets and hire some 200 new people in the coming quarters.

The Series C is bringing a very big name investor on board. It is being led by SoftBank Vision Fund 2, with previous backers Oxx, MMC Ventures, Praetura Ventures and Arete also participating. That group participated in Peak’s Series B of $21 million, which only closed in February of this year. The company has now raised $119 million; it is not disclosing its valuation.

(This latest funding round was rumored last week, although it was not confirmed at the time and the total amount was not accurate.)

Richard Potter, Peak’s CEO, said the rapid follow-on in funding was based on inbound interest, in part because of how the company has been doing.

Peak’s so-called Decision Intelligence platform is used by retailers, brands, manufacturers and others to help monitor stock levels and build personalized customer experiences, as well as other processes that can stand to have some degree of automation to work more efficiently, but also require sophistication to be able to measure different factors against each other to provide more intelligent insights. Its current customer list includes the likes of Nike, Pepsico, KFC, Molson Coors, Marshalls, Asos and Speedy, and in the last 12 months revenues have more than doubled.

The opportunity that Peak is addressing goes a little like this: AI has become a cornerstone of many of the most advanced IT applications and business processes of our time, but if you are an organization — and specifically one not built around technology — your access to AI and how you might use it will come by way of applications built by others, not necessarily tailored to you, and the costs of building more tailored solutions can often be prohibitively high. Peak claims that those using its tools have seen revenues on average rise 5%, return on ad spend double, supply chain costs reduce by 5% and inventory holdings (a big cost for companies) reduce by 12%.

Peak’s platform, I should point out, is not exactly a “no-code” approach to solving that problem — not yet at least: It’s aimed at data scientists and engineers at those organizations so that they can easily identify different processes in their operations where they might benefit from AI tools, and to build those out with relatively little heavy lifting.

There have also been different market factors that have played a role. COVID-19, for example, and the boost that we have seen both in increasing “digital transformation” in businesses and making e-commerce processes more efficient to cater to rising consumer demand and more strained supply chains have all led to businesses being more open and keen to invest in more tools to improve their automation intelligently.

This, combined with Peak AI’s growing revenues, is part of what interested SoftBank. The investor has been long on AI for a while; but it also has been building out a section of its investment portfolio to provide strategic services to the kinds of businesses in which it invests.

Those include e-commerce and other consumer-facing businesses, which make up one of the main segments of Peak’s customer base.

Notably, one of its recent investments specifically in that space was made earlier this year, also in Manchester, when it took a $730 million stake (with potentially $1.6 billion more down the line) in The Hut Group, which builds software for and runs D2C businesses.

“In Peak we have a partner with a shared vision that the future enterprise will run on a centralized AI software platform capable of optimizing entire value chains,” Max Ohrstrand, senior investor for SoftBank Investment Advisers, said in a statement. “To realize this a new breed of platform is needed and we’re hugely impressed with what Richard and the excellent team have built at Peak. We’re delighted to be supporting them on their way to becoming the category-defining, global leader in Decision Intelligence.”

It’s not clear that SoftBank’s two Manchester interests will be working together, but it’s an interesting synergy if they do, and most of all highlights one of the firm’s areas of interest.

Longer term, it will be interesting to see how and if Peak evolves to extend its platform to a wider set of users at the organizations that are already its customers.

Potter said he believes that “those with technical predispositions” will be the most likely users of its products in the near and medium term. You might assume that would cut out, for example, marketing managers, although the general trend in a lot of software tools has precisely been to build versions of the same tools used by data scientists for these less technical people to engage in the process of building what it is that they want to use.

“I do think it’s important to democratize the ability to stream data pipelines, and to be able to optimize those to work in applications,” Potter added.

Powered by WPeMatico

I’m a native French data scientist who cut his teeth as a research engineer in computer vision in Japan and later in my home country. Yet I’m writing from an unlikely computer vision hub: Stuttgart, Germany.

But I’m not working on German car technology, as one would expect. Instead, I found an incredible opportunity mid-pandemic in one of the most unexpected places: An ecommerce-focused, AI-driven, image-editing startup in Stuttgart focused on automating the digital imaging process across all retail products.

My experience in Japan taught me the difficulty of moving to a foreign country for work. In Japan, having a point of entry with a professional network can often be necessary. However, Europe has an advantage here thanks to its many accessible cities. Cities like Paris, London, and Berlin often offer diverse job opportunities while being known as hubs for some specialties.

While there has been an uptick in fully remote jobs thanks to the pandemic, extending the scope of your job search will provide more opportunities that match your interest.

I’m working at the technology spin-off of a luxury retailer, applying my expertise to product images. Approaching it from a data scientist’s point of view, I immediately recognized the value of a novel application for a very large and established industry like retail.

Europe has some of the most storied retail brands in the world — especially for apparel and footwear. That rich experience provides an opportunity to work with billions of products and trillions of dollars in revenue that imaging technology can be applied to. The advantage of retail companies is a constant flow of images to process that provides a playing ground to generate revenue and possibly make an AI company profitable.

Another potential avenue to explore are independent divisions typically within an R&D department. I found a significant number of AI startups working on a segment that isn’t profitable, simply due to the cost of research and the resulting revenue from very niche clients.

I was particularly attracted to this startup because of the potential access to data. Data by itself is quite expensive and a number of companies end up working with a finite set. Look for companies that directly engage at the B2B or B2C level, especially retail or digital platforms that affect front-end user interface.

Leveraging such customer engagement data benefits everyone. You can apply it towards further research and development on other solutions within the category, and your company can then work with other verticals on solving their pain points.

It also means there’s massive potential for revenue gains the more cross-segments of an audience the brand affects. My advice is to look for companies with data already stored in a manageable system for easy access. Such a system will be beneficial for research and development.

The challenge is that many companies haven’t yet introduced such a system, or they don’t have someone with the skills to properly utilize it. If you finding a company isn’t willing to share deep insights during the courtship process or they haven’t implemented it, look at the opportunity to introduce such data-focused offerings.

I have a sweet spot for early-stage companies that give you the opportunity to create processes and core systems. The company I work for was still in its early days when I started, and it was working towards creating scalable technology for a specific industry. The questions that the team was tasked with solving were already being solved, but there were numerous processes that still had to be put into place to solve a myriad of other issues.

Our year-long efforts to automate bulk image editing taught me that as long as the AI you’re building learns to run independently across multiple variables simultaneously (multiple images and workflows), you’re developing a technology that does what established brands haven’t been able to do. In Europe, there are very few companies doing this and they are hungry for talent who can.

So don’t be afraid of a little culture shock and take the leap.

Powered by WPeMatico

With more than 270,000 stickers, Stipop’s library of colorful, character-driven expressions has a little something for everyone.

The company offers keyboard and social app stickers through ad-supported mobile apps on iOS and Android, but it’s recently focused more on providing stickers to developers, creators and other online businesses.

“We were able to gather so many artists because we actually began as our own app that provided stickers,” Stipop co-founder Tony Park told TechCrunch. The team took what they learned from running their own consumer-facing app — namely that collecting and licensing hundreds of thousands of stickers from artists around the world is hard work — and adapted their business to help solve that problem for others.

Stipop was the first Korean company to go through Yellow, Snapchat’s exclusive accelerator. The company is also part of Y Combinator’s Summer 2021 cohort.

Stipop’s sticker library is accessible through an SDK and an API, letting developers slot the searchable sticker library into their existing software. The company already has more than 200 companies that tap into its huge sticker trove, which offers a “single-day solution” for a process that would otherwise necessitate a lot more legwork. Stipop launched a website recently that helps developers integrate its SDK and API through quick installs.

“They can just add a single line of code inside their product and will have a fully customized sticker feature [so] users will be able to spice up their chats,” Park said.

Park points out that stickers encourage engagement — and for social software, engagement means growth. Stickers are a playful way to send characters back and forth in chat, but they also pop up in a number of other less obvious spots, from dating apps to e-commerce and ridesharing apps. Stipop even drives the sticker search in work collaboration software Microsoft Teams.

The company has already partnered with Google, which uses Stipop’s sticker library in Gboard, Android Messages and Tenor, a GIF keyboard platform that Google bought in 2018. That partnership drove 600 million sticker views within the first month. A new partnership between Stipop and Coca-Cola on the near horizon will add Coke-branded stickers to its sticker library and the company is opening its doors to more brands that understand the unique appeal of stickers in messaging apps.

Park says that people tend to compare stickers and gifs, two ways of wordlessly expressing emotion and social nuance, but stickers are a world unto themselves. Stickers exist in their own creative universe, with star artists, regional themes and original casts of characters that take on a life of their own among fans. “Sticker creators have their own profession,” Park said.

Visual artists can also find a lot of traction releasing stickers, even without sophisticated illustrations. And since they’re all about meaning rather than refinement, non-designers and less skilled artists can craft hit stickers too.

“Stickers are great for them because it [is] so easy to go viral,” Park said. The company has partnered with 8,000 sticker creators across 25 languages, helping those artists monetize their creations and generate income based on how many times a sticker is shared.

Stickers command their own visual language around the world, and Park has observed interesting cultural differences in how people use them to communicate. In the West, stickers are often used in place of text, but in Asia, where they’re used much more frequently, people usually send stickers to enhance rather than replace the meaning of text.

In East Asia, users tend to prefer simple black and white stickers, but in India and Saudi Arabia, bright, golden stickers top the trends. In South America, popular stickers take on a more pixelated, unique quality that resonates culturally there.

“With stickers, you fall in love with [the] characters you send… that becomes you,” Park said.

Powered by WPeMatico

Earlier today, spend management startup Ramp said it has raised a $300 million Series C that valued it at $3.9 billion. It also said it was acquiring Buyer, a “negotiation-as-a-service” platform that it believes will help customers save money on purchases and SaaS products.

The round and deal were announced just a week after competitor Brex shared news of its own acquisition — the $50 million purchase of Israeli fintech startup Weav. That deal was made after Brex’s founders invested in Weav, which offers a “universal API for commerce platforms.”

From a high level, all of the recent deal-making in corporate cards and spend management shows that it’s not enough to just help companies track what employees are expensing these days. As the market matures and feature sets begin to converge, the players are seeking to differentiate themselves from the competition.

But the point of interest here is these deals can tell us where both companies think they can provide and extract the most value from the market.

These differences come atop another layer of divergence between the two companies: While Brex has instituted a paid software tier of its service, Ramp has not.

Let’s start with Ramp. Launched in 2019, the company is a relative newcomer in the spend management category. But by all accounts, it’s producing some impressive growth numbers. As our colleague Mary Ann Azevedo wrote:

Since the beginning of 2021, the company says it has seen its number of cardholders on its platform increase by 5x, with more than 2,000 businesses currently using Ramp as their “primary spend management solution.” The transaction volume on its corporate cards has tripled since April, when its last raise was announced. And, impressively, Ramp has seen its transaction volume increase year over year by 1,000%, according to CEO and co-founder Eric Glyman.

Ramp’s focus has always been on helping its customers save money: It touts a 1.5% cash back reward for all purchases made through its cards, and says its dashboard helps businesses identify duplicitous subscriptions and license redundancies. Ramp also alerts customers when they can save money on annual versus monthly subscriptions, which it says has led many customers to do away with established T&E platforms like Concur or Expensify.

All told, the company claims that the average customer saves 3.3% per year on expenses after switching to its platform — and all that is before it brings Buyer into the fold.

Powered by WPeMatico

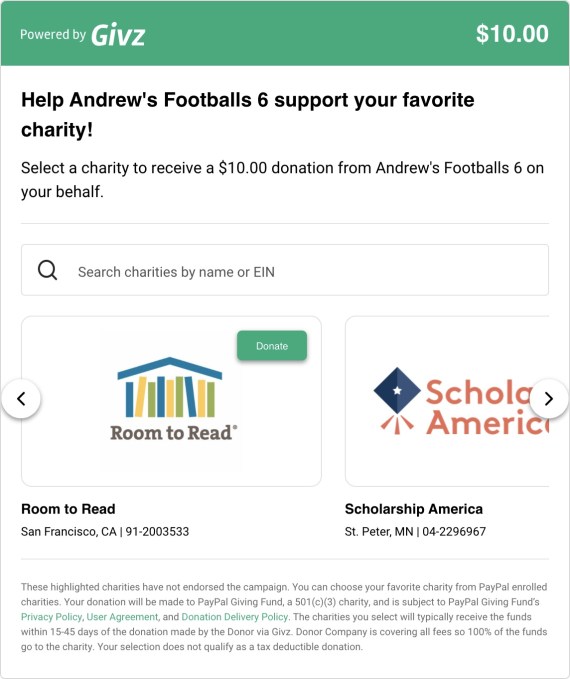

Givz, which has developed an API-powered platform that gives brands a way to convert discounts into donations, has raised $3 million in seed funding.

Eniac and Accomplice co-led the financing for the New York-based startup. Additional investors include Supernode Ventures, Claude Wasserstein of Fine Day, Phoenix Club and Dylan Whitman.

Givz was founded in 2017 to make charitable giving more accessible and convenient for the masses. In March 2020, right before the COVID-19 pandemic hit, the company pivoted from B2C to B2B and used the technology rails it had built to create the e-commerce marketing platform that Givz is today.

The company aims to drive “full-price purchasing behavior” by giving consumers the ability to convert the money they would be saving if getting a discount, and donating it to their favorite charities.

Prior to the funding, Givz had been working with more than 80 enterprise, mid-market and SMB retail and e-commerce clients such as H&M, Tom Brady’s TB12, Seedlip and Terez, and accumulated more than 40,000 individual users. Since the shift last year, the company has helped drive more than $1 million to 1,100 charities, according to CEO and founder Andrew Forman.

It just launched on Shopify, which Forman says will give the startup access to the 1.7 million retailers that use Shopify as their e-commerce platform.

Givz operates under the premise that “donation-driven marketing” consistently outperforms discounts and costs less, “making it an attractive addition” to corporate marketing.

“We are creating a new marketing category and generating the largest sustainable charitable giving platform in the process,” he told TechCrunch.

An example of a company using Givz can be found in Tervis, which offered customers “For every $50 you spend, you’ll receive $15 to give to the charity of your choice.”

“They used Givz technology to allow consumers to choose the charity of their choice and make a turnkey disbursement to hundreds of charities,” Forman explained. “They saw a 20% lift in website conversion and a 17% increase in average order value as a result of this offer.”

Image Credits: Givz

Currently, Givz has eight employees with plans to more than double that number over the next year.

The company plans to use the new capital toward that hiring, and to do some marketing of its own.

“We also want to explore the full potential around the consumer behavior data we collect,” Forman said.

In the short term, Givz is focused on “Shopify growth” with direct to consumer brands.

“But we have successful use cases and huge potential with enterprise retailers and financial institutions,” Forman told TechCrunch. “In the future, we have our sights set on restaurants, the gaming industry and global expansion. I believe that using personalized donations to incentivize consumer behavior has endless application across industries, verticals and continents.”

Eniac partner Vic Singh said that there’s been a trend of brands experimenting with different ways to target the socially conscious consumer.

“We believe Givz’s donation-driven marketing platform offers brands the best way to attract the socially conscious consumer while elevating their brand, moving more inventory and driving increased order value rather than simplistic traditional discounting,” he added.

Accomplice’s TJ Mahony said that both he and Singh believed SMS would emerge as a new marketing category, which led to early investments in Attentive and Postscript, respectively.

“We both saw a similar opportunity with Givz,” he wrote via e-mail. “Discounting is a well worn marketing muscle, but it’s detrimental to the brand, margins and customer expectations. We believe continuous impact marketing becomes the alternative to discounting and marketers will begin to build teams and budget around thoughtful and persistent giving strategies.”

Powered by WPeMatico

Cart.com, a Houston-based company providing end-to-end e-commerce services, brought in its third funding round this year, this time a $98 million Series B round to bring its total funding to $143 million.

Oak HC/FT led the new round of funding and was joined by PayPal Ventures, Clearco, G9 Ventures, Mercury Fund, Valedor Partners and Arsenal Growth. Strategic investors in the Series B include Heyday CEO Sebastian Rymarz and Casper CEO Philip Krim. This new round follows a $25 million Series A round, led by Mercury and Arsenal in July, and a $20 million seed round from Bearing Ventures.

Cart.com CEO Omair Tariq, who was previously an executive at Home Depot and COO of Blinds.com, co-founded the company in September 2020 with Jim Jacobson, former CEO of RTIC Outdoors.

Tariq told TechCrunch that the company provides software, services and infrastructure to businesses so they can scale online. Cart.com is taking the best parts of selling direct-to-consumer on marketplaces like Amazon and Shopify to create value for brands. Tariq said he is pioneering the term “e-commerce-as-a-service” to bring together under one platform a suite of business tools like storefront software, marketing, fulfillment, payments and customer service.

“We see the power of having an interconnected platform,” Tariq said. “There also needs to be a hybrid between selling direct-to-consumer and on Amazon and Shopify for companies that don’t have the money to pay for a percentage of their sales and receive no access to customers or data, and needing 20 different plug-ins that are not connected.”

Cart.com went after the new funding after seeing validation of its idea: brands coming to them wanting more products and services, which led to acquisitions. The company has acquired seven companies so far, including — AmeriCommerce, Spacecraft Brands and, more recently, DuMont Project and Sauceda Industries. Tariq is planning for another three or four by the end of the year.

In addition, it received inbound interest from strategic investors, like Oak and PayPal, which Tariq said was going to enable the company “to be more successful faster.”

Allen Miller, principal at Oak HC/FT, said after spending time with Tariq to understand his vision about Cart.com’s software, payments and services, he felt that the company was doing something that didn’t exist in today’s commerce infrastructure.

He said that Cart.com is well positioned to help companies, like those with $1 million in sales, stay focused on growing the business while Cart.com stitches together all of the tools for them to operate in the background.

“It’s a unique offering to merchants that has a high value proposition,” Miller said. “The vision and drive that Omair and Jim have, along with an inspiring mission they want to achieve — to be brand-centric and help the next generation of merchants. These guys also have a good playbook on finding companies and teams to acquire, as well as handling the post M&A to have everyone on one platform.”

The new financing will enable Cart.com to further invest in technology development and to increase headcount by at least 15 times, with plans to go from fewer than two dozen employees to more than 300 team members by the end of the year. The company has nearly 70 jobs posted on its website for positions in engineering, technology, digital marketing and e-commerce. Tariq also expects half of the funds to go toward more acquisitions.

Cart.com currently serves over 2,000 e-commerce brands, including GNC, Haymaker Coffee and KeHE, and processes more than $700 million in gross merchandise value per year. The company saw revenue increase 400% since the platform’s launch in November.

In addition, the company has nine fulfillment centers across the country, and is increasing its access to reach 80% of the U.S. population with two-day shipping, Tariq added.

“We are giving the power back to brands by giving them what they need to operate e-commerce,” he said. “There are still a few pieces to fill in so brands have a unified experience, but with us, they can add fulfilment, marketing or customer conversion tools with the click of a couple of buttons.”

Powered by WPeMatico

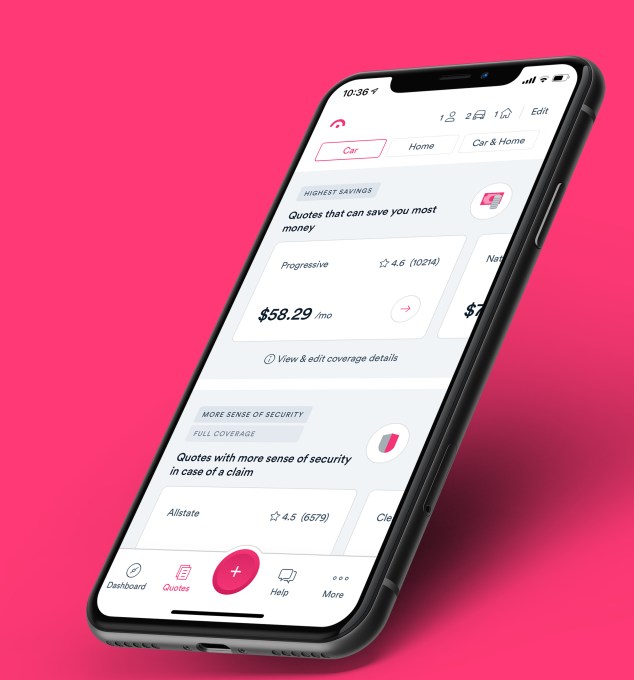

Just months after raising $28 million, Jerry announced today that it has raised $75 million in a Series C round that values the company at $450 million.

Existing backer Goodwater Capital doubled down on its investment in Jerry, leading the “oversubscribed” round. Bow Capital, Kamerra, Highland Capital Partners and Park West Asset Management also participated in the financing, which brings Jerry’s total raised to $132 million since its 2017 inception. Goodwater Capital also led the startup’s Series B earlier this year. Jerry’s new valuation is about “4x” that of the company at its Series B round, according to co-founder and CEO Art Agrawal.

“What factored into the current valuation is our annual recurring revenue, growing customer base and total addressable market,” he told TechCrunch, declining to be more specific about ARR other than to say it is growing “at a very fast rate.” He also said the company “continues to meet and exceed growth and revenue targets” with its first product, a service for comparing and buying car insurance. At the time of the company’s last raise, Agrawal said Jerry saw its revenue surge by “10x” in 2020 compared to 2019.

Jerry, which says it has evolved its model to a mobile-first car ownership “super app,” aims to save its customers time and money on car expenses. The Palo Alto-based startup launched its car insurance comparison service using artificial intelligence and machine learning in January 2019. It has quietly since amassed nearly 1 million customers across the United States as a licensed insurance broker.

“Today as a consumer, you have to go to multiple different places to deal with different things,” Agrawal said at the time of the company’s last raise. “Jerry is out to change that.”

The new funding round fuels the launch of the company’s “compare-and-buy” marketplaces in new verticals, including financing, repair, warranties, parking, maintenance and “additional money-saving services.” Although Jerry also offers a similar product for home insurance, its focus is on car ownership.

Image Credits: Jerry

“Access to reliable and affordable transportation is critical to economic empowerment,” said Rafi Syed, Jerry board member and general partner at Bow Capital, which also doubled down on its investment in the company. “Jerry is helping car owners make the most of every dollar they earn. While we see Jerry as an excellent technology investment showcasing the power of data in financial services, it’s also a high-performing investment in terms of the financial inclusion it supports.”

Goodwater Capital Partner Chi-Hua Chien said the firm’s recurring revenue model makes it stand out from lead generation-based car insurance comparison sites.

CEO Agrawal agrees, noting that Jerry’s high-performing annual recurring revenue model has made the company “attractive to investors” in addition to the fact that the startup “straddles” the auto, e-commerce, fintech and insurtech industries.

“We recognized those investment opportunities could drive our business faster and led to raising the round earlier than expected,” he told TechCrunch. “We’re eager to launch new categories to save customers time and money on auto expenses and the new investment shortens our time to market.”

Agrawal also believes Jerry is different from other auto-related marketplaces out there in that it aims to help consumers with various aspects of car ownership (from repair to maintenance to insurance to warranties), rather than just one. The company also believes it is set apart from competitors in that it doesn’t refer a consumer to an insurance carrier’s site so that they still have to do the work of signing up with them separately, for example. Rather, Jerry uses automation to give consumers customized quotes from more than 45 insurance carriers “in 45 seconds.” The consumers can then sign on to the new carrier via Jerry, which can then cancel former policies on their behalf.

Jerry makes recurring revenue from earning a percentage of the premium when a consumer purchases a policy on its site from carriers such as Progressive.

Powered by WPeMatico