Doughbies

Auto Added by WPeMatico

Auto Added by WPeMatico

There are few things in this world more difficult than launching a successful startup. It takes talent, know-how, money and a hell of a lot of good timing and luck. And even with all of those magical components in place, the odds may still be against you.

At TechCrunch, we take pride in covering the best and brightest of the startup world. But while covering the startup world is one of the most exciting and fulfilling parts of our job, death is a part of any life cycle. Sadly, not all startups that burn bright ultimately make it. In fact, most don’t.

As we wrap up this year and look forward to the next, let’s take a moment to remember some of those startups we lost in 2018.

Total Raised: $118 million

Airware created a cloud software system to help construction companies, mining operations and other enterprise customers use drones to inspect equipment for damage. It also tried to build its own drones, but found that it couldn’t compete with giants like China’s DJI.

The shutdown appears to have been very sudden, coming just four days after Airware opened a Tokyo office, with an investment and partnership from Mitsubishi. In a statement, the company said, “Unfortunately, the market took longer to mature than we expected. As we worked through the various required pivots to position ourselves for long-term success, we ran out of financial runway.”

Total Raised: $131.7 million

Blippar was one of the early pioneers in augmented reality, but unfortunately the AR market has yet to live up to the hopes for mainstream adoption. And despite raising a funding round earlier this year, the startup was apparently losing money quickly as it sought new customers.

Not helping matters was some shareholder drama, where an emergency influx of $5 million was blocked by Khazanah, a strategic investment fund from the Malaysian government. In a blog post, the company said this was “an incredibly sad, disappointing, and unfortunate outcome.”

Total Raised: $25.6 million

One of the major casualties of the FAA’s ban on smart luggage, this New York-based startup was forced to close its doors in May. CEO Tomi Pierucci was extremely outspoken when airlines started to enforce the new rules early this year, calling the news “an absolute travesty.”

From the standpoint of Bluesmart, he was right. The startup went all-in on connected luggage, and ultimately found it impossible to adapt when battery packs were no longer allowed on flights. The startup ended all sales and manufacturing, selling what was left of its tech, designs and IP to luggage giant TravelPro.

Total Raised: $760,000

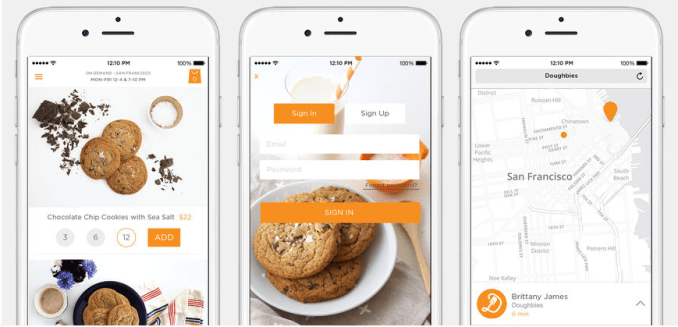

Things came crumbling down for San Francisco-based Doughbies in July, when the 500 Startups-backed, same-day cookie delivery service announced it was shutting down immediately. But it wasn’t because the startup ran out of money. Doughbies was actually profitable. Rather, its founders, Daniel Conway and Mariam Khan, just wanted to move onto something new.

TechCrunch’s Josh Constine argued at the time that Doughbies really didn’t need venture backing and that pressure to deliver adequate returns may have weighed more heavily on Doughbies than it was willing to admit. RIP Doughbies.

Total Raised: $21.5 million

Like many failed startups before it, San Francisco-based Lantern was forced to shutter operations after an acquisition deal fell through. The mental health startup, founded by Nicholas Bui LeTourneau and Alejandro Foung, had raised millions in venture capital funding from the University of Pittsburgh Medical Center’s venture arm, Mayfield and SoftTechVC, but failed to follow through on its promise.

What was that promise? To offer personalized tools to deal with stress, anxiety and body image based on cognitive behavioral therapy techniques via a mobile application. Despite being an early mover in a now overly crowded field of mental wellness apps, Lantern wasn’t able to find enough customers to survive.

Total Raised: $17 million

Smart security camera maker Lighthouse AI had a promising product with a natural language processing system that allowed users to navigate their footage. But it also faced a crowded market, and it seems consumers didn’t embrace the product. The company announced this month that it’s winding down.

“I am incredibly proud of the groundbreaking work the Lighthouse team accomplished – delivering useful and accessible intelligence for our homes via advanced AI and 3D sensing,” wrote CEO Alex Teichman. “Unfortunately, we did not achieve the commercial success we were looking for and will be shutting down operations in the near future.”

Total Raised: N/A

Mayfield, which was originally part of Bosch, created the adorable home robot Kuri. However, it announced in July that it would stop manufacturing Kuri, and followed with an announcement that it would cease operations altogether.

“Our team is beyond disappointed,” the company said in a blog post. “Together we’ve spent the past four years designing and building not just Kuri, but also an equally incredible company culture and spirit.”

Total Raised: $149.5 million

A major player in industrial robotics, Rethink was founded by iRobot co-founder Rod Brooks and former MIT CSAIL staff researcher Ann Whittaker. The Boston area startup grew into one of the most important players in both the collaborative and educational robotics space, courtesy of creations like Baxter and Sawyer.

Ultimately, however, the company served as yet another testament to just how difficult it is to launch a robotics startup. Even with brilliant minds and nearly $150 million in funding, the company couldn’t turn enough profit to stay afloat. A last-minute planned acquisition fell through, and Rethink was forced to close up shop in October.

Total Raised: $1.4 billion

Startup stories don’t come more film-ready than this. Even before it officially closed its doors, Theranos was set to be the subject of a book, documentary and an Adam McKay-directed feature film starring Jennifer Lawrence as founder Elizabeth Holmes. Holmes founded the company in 2003, promising a breakthrough in blood testing. By age 31, she became the world’s youngest self-made billionaire.

Theranos would go on to raise $1.4 billion, with a $10 billion valuation at its peak. In 2015, medical professionals began to mount criticism against the company’s methods. The following year, the SEC began investigating Theranos, ultimately charging it with “massive fraud.” In September, the company finally called it quits, with Holmes agreeing to pay a $500,000 penalty, while being barred from serving as an officer or director of a public company for 10 years.

Total Raised: $62 million

NEW YORK, NY – MAY 06: Co-founder and CEO of Shyp, Kevin Gibbons speaks onstage during TechCrunch Disrupt NY 2015 – Day 3 at The Manhattan Center on May 6, 2015 in New York City. (Photo by Noam Galai/Getty Images for TechCrunch)

A $250 million valuation and capital from some of the best investors (Kleiner Perkins, Slow Ventures) failed to keep on-demand shipping startup Shyp from dissolving. The San Francisco-based startup raised multiple rounds of venture capital amid a major hype cycle for on-demand shipping companies, but wasn’t able to scale successfully beyond the Bay Area.

“To this day, I’m in awe of the vigor the team possessed in tackling a 200-year-old industry,” CEO Kevin Gibbon wrote at the time. “But, growth at all costs is a dangerous trap that many startups fall into, mine included.”

Total Raised: $54.4 million

Over the past few years, Telltale Games seemed to reinvent adventure gaming, adapting big franchises like The Walking Dead, Game of Thrones and Batman into episodic stories where players’ choices seemed to have real weight. It even partnered with Netflix to bring a version of “Minecraft: Story Mode” to the streaming service.

But it seems the company has had longstanding business issues, with 90 employees laid off in November 2017, then another 250 let go in September of this year. Although a skeleton crew remained employed to finish the work for Netflix, it looks like Telltale is dead. And the fact that those employees were let go without severance seems to reinforce an earlier report of toxic management.

Powered by WPeMatico

Doughbies should have been a bakery, not a venture-backed startup. Founded in the frothy days of 2013 and funded with $670,000 by investors, including 500 Startups, Doughbies built a same-day cookie delivery service. But it was never destined to be capable of delivering the returns required by the VC model that depends on massive successes to cover the majority of bets that fail. The startup became the butt of jokes about how anything could get funding.

This weekend, Doughbies announced it was shutting down immediately. Surprisingly, it didn’t run out of money. Doughbies was profitable, with 36 percent gross margins and 12 percent net profit, co-founder and CEO Daniel Conway told TechCrunch. “The reason we were able to succeed, at this level and thus far, is because we focused on unit economics and customer feedback (NPS scoring). That’s it.”

Many other startups in the on-demand space missed that memo and vaporized. Shyp mailed stuff for you and Washio dry cleaned your clothes, until they both died sudden deaths. Food delivery has become a particularly crowded cemetery, with Sprig, Maple, Juicero and more biting the dust. Asked his advice for others in the space, Conway said to “Make sure your business makes sense — that you’re making money, and make sure your customers are happy.”

Doughbies certainly did that latter. They made one of the most consistently delicious chocolate chip cookies in the Bay Area. I had them cater our engagement party. At roughly $3 per cookie plus $5 for delivery, it was pricey compared to baking at home, but not outrageous given SF restaurant rates. From its launch at 500 Startups Demo Day with an “Oprah” moment where investors looked beneath their seats to find Doughbies waiting for them, it cared a lot about the experience.

But did it make sense for a bakery to have an app and deliver on-demand? Probably not. There was just no way to maintain a healthy Doughbies habit. You were either gunning for the graveyard yourself by ordering every week, or like most people you just bought a few for special occasions. Startups like Uber succeed by getting people to routinely drop $30 per day, not twice a year. And with the push for nutritious and efficient offices, it was surely hard for enterprise customers to justify keeping cookies stocked.

Flanked by Instacart and Uber Eats, there weren’t many ripe adjacent markets for Doughbies to conquer. It was stuck delivering baked goods to customers who were deterred from growing their cart size by a sense of gluttony.

Without stellar growth or massive sales volumes, there aren’t a lot of exciting challenges to face for people like Conway and his co-founder Mariam Khan. “Ultimately we shut down because our team is ready to move on to something new,” Conway says.

The startup just emailed customers explaining that “We’re currently working on finding a new home for Doughbies, but we can’t make any promises at this time.” Perhaps a grocery store or broader food company will want its logistics technology or customer base. But delivery is a brutal market to break into, dominated by those like Uber who’ve built economies of scale through massive fleets of drivers to maximize routing efficiency.

In the end, Doughbies was a lifestyle business. That’s not a dirty word. A few co-founders with a dream can earn a respectable living doing what they care about. But they have to do it lean, without the advantage of deep-pocketed investors.

As soon as a company takes venture funding, it’s under pressure to deliver adequate returns. Not 2X or 5X, but 10X, 100X, even 1,000X what they raise. That can lead to investors breathing down their neck, encouraging big risks that could tank the business just for a shot at those outcomes. Two years ago we saw a correction hit the ecosystem, writing down the value of many startups, and we continue to see the ripple effect as companies funded before hit the end of their runway.

Desperate for cash, founders can accept dirty funding terms that screw over not just themselves, but their early employees and investors. FanDuel raised more than $416 million at a peak valuation of $1.3 billion. But when it sold for $465 million, the founders and employees received zero as the returns all flowed to the late-stage investors who’d secured non-standard liquidation preferences. After nearly 10 years of hard work, the original team got nothing.

Not every business is a startup. Not every startup is a rocket ship. It takes more than just building a great product to succeed. It can require suddenly cutting costs to become profitable before you run out of funding. Or cutting ambitions and taking less cash at a lower valuation so you can realistically hit milestones. Or accepting a low-ball acquisition offer because it’s better than nothing. Or not raising in the first place, and building up revenues the old-fashioned way so even modest growth is an accomplishment.

Investors are often rightfully blamed for inflating the bubble, pushing up raises and valuations to lure startups to take their money instead of someone else’s. But when it comes to deciding what could be a fast-growing business, sometimes its the founders who need the adjustment.

Powered by WPeMatico