DoorDash

Auto Added by WPeMatico

Auto Added by WPeMatico

DoorDash, Affirm, Roblox, Airbnb, C3.ai and Wish all filed to go public in recent days, which means some venture capitalists are having the best week of their lives.

Tech companies that go public capture our imagination because they are literal happy endings. An Initial Public Offering is the promised land for startup pilgrims who may wander the desert for years seeking product-market fit. After all, the “I” in “ISO” stands for “incentive.”

A flurry of new S-1s in a single week forced me to rearrange our editorial calendar, but I didn’t mind; our 360-degree coverage let some of the air out of various hype balloons and uncovered several unique angles.

For example: I was familiar with Affirm, the service that lets consumers finance purchases, but I had no idea Peloton accounted for 30% of its total revenue in the last quarter.

“What happens if Peloton puts on the brakes?” I asked Alex Wilhelm as I edited his breakdown of Affirm’s S-1. We decided to use that as the subhead for his analysis.

The stories that follow are an overview of Extra Crunch from the last five days. Full articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thank you very much for reading Extra Crunch this week; I hope you have a relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

Gaming company Roblox filed to go public yesterday afternoon, so Alex Wilhelm brought out a scalpel and dissected its S-1. Using his patented mathmagic, he analyzed Roblox’s fundraising history and reported revenue to estimate where its valuation might land.

Noting that “the public markets appear to be even more risk-on than the private world in 2020,” Alex pegged the number at “just a hair under $10 billion.”

HANGZHOU, CHINA – JULY 31: An employee uses face recognition system on a self-service check-out machine to pay for her meals in a canteen at the headquarters of Alibaba Group on July 31, 2018 in Hangzhou, Zhejiang Province of China. The self-service check-out machine can calculate the price of meals quickly to save employees’ queuing time. (Photo by Visual China Group via Getty Images)

For all the hype about new forms of payment, the way I transact hasn’t been radically transformed in recent years — even in tech-centric San Francisco.

Sure, I use NFC card readers to tap and pay and tipped a street musician using Venmo last weekend. But my landlord still demands paper checks and there’s a tattered “CASH ONLY” taped to the register at my closest coffee shop.

In China, it’s a different story: Alibaba’s employee cafeteria uses facial recognition and AI to determine which foods a worker has selected and who to charge. Many consumers there use the same app to pay for utility bills, movie tickets and hamburgers.

“Today, nobody except Chinese people outside of China uses Alipay or WeChat Pay to pay for anything,” says finance researcher Martin Chorzempa. “So that’s a big unexplored side that I think is going to come into a lot of geopolitical risks.”

Image Credits: Nigel Sussman (opens in a new window)

Consumer lending service Affirm filed to go public on Wednesday evening, so Alex used Thursday’s column to unpack the company’s financials.

After reviewing Affirm’s profitability, revenue and the impact of COVID-19 on its bottom line, he asked (and answered) three questions:

Image Credits: XiXinXing (opens in a new window) / Getty Images

“The only thing more rare than a unicorn is an exited unicorn,” observes Managing Editor Danny Crichton, who looked back at Exitpalooza 2020 to answer “a simple question — who made the money?”

Covering each exit from the perspective of founders and investors, Danny makes it clear who’ll take home the largest slice of each pie. TL;DR? “Some really colossal winners among founders, and several venture firms walking home with billions of dollars in capital.

Image Credits: Nigel Sussman (opens in a new window)

The S-1 Airbnb released at the start of the week provided insight into the home-rental platform’s core financials, but it also raised several questions about the company’s health and long-term viability, according to Alex Wilhelm:

Andrew Anagnost, president and CEO, Autodesk.

Earlier this week, Autodesk announced its purchase of Spacemaker, a Norwegian firm that develops AI-supported software for urban development.

TechCrunch reporter Steve O’Hear interviewed Autodesk CEO Andrew Anagnost to learn more about the acquisition and asked why Autodesk paid $240 million for Spacemaker’s 115-person team and IP — especially when there were other startups closer to its Bay Area HQ.

“They’ve built a real, practical, usable application that helps a segment of our population use machine learning to really create better outcomes in a critical area, which is urban redevelopment and development,” said Anagnost.

“So it’s totally aligned with what we’re trying to do.”

Image Credits: Nigel Sussman (opens in a new window)

On Monday, Alex dove into the IPO filing for enterprise artificial intelligence company C3.ai.

After poring over its ownership structure, service offerings and its last two years of revenue, he asks and answers the question: “is the business itself any damn good?”

Image Credits: jayk7 / Getty Images

In his new book, “Subprime Attention Crisis,” writer/researcher Tim Hwang attempts to answer a question I’ve wondered about for years: does advertising actually work?

Managing Editor Danny Crichton interviewed Hwang to learn more about his thesis that there are parallels between today’s ad industry and the subprime mortgage crisis that helped spur the Great Recession.

So, are online ads effective?

“I think the companies are very reticent to give up the data that would allow you to find a really definitive answer to that question,” says Hwang.

Image Credits: Zoom

Even after much of the population has been vaccinated against COVID-19, we will still be using Zoom’s video-conferencing platform in great numbers.

That’s because Zoom isn’t just an app: it’s also a platform play for startups that add functionality using APIs, an SDK or chatbots that behave like smart assistants.

Enterprise reporter Ron Miller spoke to entrepreneurs and investors who are leveraging Zoom’s platform to build new applications with an eye on the future.

“By offering a platform to build applications that take advantage of the meeting software, it’s possible it could be a valuable new ecosystem for startups,” says Ron.

Image Credits: Bryce Durbin

Without an on-campus experience, many students (and their parents) are wondering how much value there is in attending classes via a laptop in a dormitory.

Even worse: Declining enrollment is leading many institutions to eliminate majors and find other ways to cut costs, like furloughing staff and cutting athletic programs.

Edtech solutions could fill the gap, but there’s no real consensus in higher education over which tools work best. Many colleges and universities are using a number of “third-party solutions to keep operations afloat,” reports Natasha Mascarenhas.

“It’s a stress test that could lead to a reckoning among edtech startups.”

3D rendering of TNT dynamite sticks in carton box on blue background. Explosive supplies. Dangerous cargo. Plotting terrorist attack. Image Credits: Gearstd / Getty Images.

I look for guest-written Extra Crunch stories that will help other entrepreneurs be more successful, which is why I routinely turn down submissions that seem overly promotional.

However, Henrik Torstensson (CEO and co-founder of Lifesum) submitted a post about the techniques he’s used to scale his nutrition app over the last three years. “It’s a strategy any startup can use, regardless of size or budget,” he writes.

According to Sensor Tower, Lifesum is growing almost twice as fast as Noon and Weight Watchers, so putting his company at the center of the story made sense.

Image via Getty Images / Alexander Spatari

Every year, we ask TechCrunch reporters, VCs and our Extra Crunch readers to recommend their favorite books.

Have you read a book this year that you want to recommend? Send an email with the title and a brief explanation of why you enjoyed it to bookclub@techcrunch.com.

We’ll compile the suggestions and publish the list as we get closer to the holidays. These books don’t have to be published this calendar year — any book you read this year qualifies.

Please share your submissions by November 30.

Image Credits: Sophie Alcorn

Dear Sophie:

My VC partner and I are working with 50/50 co-founders on their startup — let’s call it “NewCo.” We’re exploring pre-seed terms.

One founder is on a green card and already works there. The other founder is from India and is working on an H-1B at a large tech company.

Can the H-1B co-founder lead this company? What’s the timing to get everything squared away? If we make the investment we want them to hit the ground running.

— Diligent in Daly City

Powered by WPeMatico

The only thing more rare than a unicorn is an exited unicorn.

At TechCrunch, we cover a lot of startup financings, but we rarely get the opportunity to cover exits. This week was an exception though, as it was exitpalooza as Affirm, Roblox, Airbnb and Wish all filed to go public. With DoorDash’s IPO filing last week, this is upwards of $100 billion in potential float heading to the public markets as we make our way to the end of a tumultuous 2020.

All those exits raise a simple question — who made the money? Which VCs got in early on some of the biggest startups of the decade? Who is going to be buying a new yacht for the family for the holidays (or, like, a fancy yurt for when Burning Man restarts)? The good news is that the wealth is being spread around at least a couple of VC firms, although there are definitely a handful of partners who are looking at a very, very nice check in the mail compared to others.

So let’s dive in.

I’ve covered DoorDash’s and Airbnb’s investor returns in-depth, so if you want to know more about those individual returns, feel free to check out those analyses. But let’s take a more panoramic perspective of the returns of these five companies as a whole.

First, let’s take a look at the founders. These are among the very best startups ever built, and therefore, unsurprisingly, the founders all did pretty well for themselves. But there are pretty wide variations that are interesting to note.

First, Airbnb — by far — has the best return profile for its founders. Brian Chesky, Nathan Blecharczyk and Joe Gebbia together own nearly 42% of their company at IPO, and that’s after raising billions in venture capital. The reason for their success is simple: Airbnb may have had some tough early innings when it was just getting started, but once it did, its valuation just skyrocketed. That helped to limit dilution in its earlier growth rounds, and ultimately protected their ownership in the company.

David Baszucki of Roblox and Peter Szulczewski of Wish both did well: they own 12% and about 19% of their companies, respectively. Szulczewski’s co-founder Sheng “Danny” Zhang, who is Wish’s CTO, owns 4.9%. Eric Cassel, the co-founder of Roblox, did not disclose ownership in the company’s S-1 filing, indicating that he doesn’t own greater than 5% (the SEC’s reporting threshold).

DoorDash’s founders own a bit less of their company, mostly owing to the money-gobbling nature of that business and the sheer number of co-founders of the company. CEO Tony Xu owns 5.2% while his two co-founders Andy Fang and Stanley Tang each have 4.7%. A fourth co-founder, Evan Moore, didn’t disclose his share totals in the company’s filing.

Finally, we have Affirm . Affirm didn’t provide total share counts for the company, so it’s hard right now to get a full ownership picture. It’s also particularly hard because Max Levchin, who founded Affirm, was a well-known, multi-time entrepreneur who had a unique shareholder structure from the beginning (many of the venture firms on the cap table actually have equal proportions of common and preferred shares). Levchin has more shares all together than any of his individual VC investors — 27.5 million shares, compared to the second largest investor, Jasmine Ventures (a unit of Singapore’s GIC) at 22 million shares.

Powered by WPeMatico

Airbnb filed to go public today, bringing the well-known unicorn one step closer to being a public company.

The financial results show a company on the rebound, but smaller than it was. Its more granular financial results also make clear how hard the pandemic was on the travel-reliant unicorn. Regarding Airbnb’s worth, investors will have to balance how they value recovery and recent profits over the company’s disrupted historical growth arc.

The home-sharing startup had a tumultuous year, with the COVID-19 pandemic harming its business in the first and second quarters of the year, and Airbnb later recovering on the strength of more local bookings.

Its filing comes mere days after fellow unicorns DoorDash and C3.ai themselves filed to go public in what could be a rush to the public markets by richly valued startups.

Airbnb’s S-1 filing was expected to come last week, but was delayed due to purported election concerns, a concept that TechCrunch staff did not find entirely convincing.

We’ve scraped together quite a lot about Airbnb’s recent financial performance, but its S-1 is the real treasure trove. What follows is a dive into the company’s high-level numbers. From there, TechCrunch will dig into the company’s financial nuances and ownership stakes.

What we want to know is how the pandemic impacted Airbnb’s business; its year-to-date results, and what we can suss out from its quarterly trends.

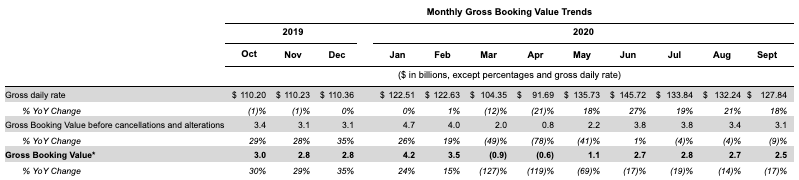

Up top in Airbnb’s S-1 is a chart that shows monthly bookings on its platform. The implication is somewhat simple; namely that Airbnb knows what we want to know and wanted to share. Here are those numbers:

Image Credits: Airbnb S-1

As expected, Airbnb took a huge hit in March. But by May things were back to year-over-year growth, where they stayed.

Now, the company has seen precious little bookings growth since June — indeed it has seen bookings fall in the months since. And, worse, the company’s gross bookings after removing cancellations are down on a year-over-year basis. (Update: We misread this table at first, and have updated our notes on it.)

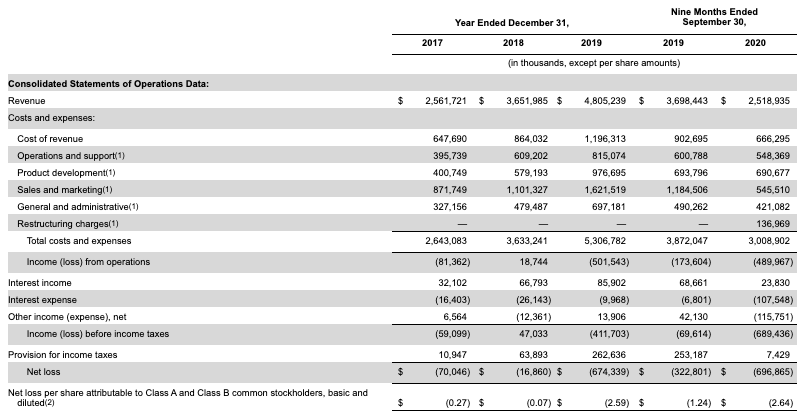

So, what does all of that look like in more traditional accounting figures? Here’s Airbnb’s reported income statement:

Image Credits: Airbnb S-1

As expected, Airbnb’s year has not been tremendous. Indeed, the company is on track to match its 2018 size, if we have our math correct.

What changed from the first three quarters of 2019 to the first three quarters of 2020? The biggest thing, apart from expected lower revenue costs — less revenue costs less — is the huge decline in sales and marketing spend at the company. Airbnb slashed S&M outlays from $1.18 billion in the first three quarters of 2019 to just $545.5 million in the same period of 2020.

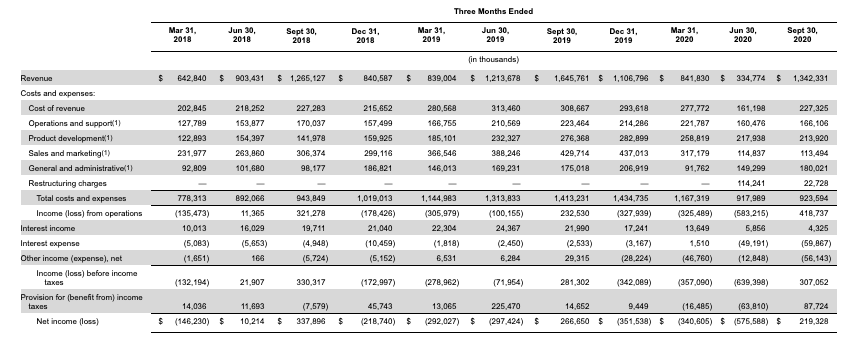

So, where will Airbnb wind up in 2020 once it’s all done? We’ll need to peek at its quarterly results for that. Here they are:

Image Credits: Airbnb S-1

Airbnb’s growth continues in year-over-year terms right until the March 31, 2020 quarter, when it was effectively flat compared to Q1 2019. Or, the company would have grown sans COVID-19. In the June 30, 2020 quarter we see the real damage, with Airbnb’s revenue falling from $1.2 billion in the year-ago quarter to just $334.8 million. That’s a shocking decline.

But, looking ahead to Q3 2020 we see a large return to form. Yes, Airbnb’s third quarter was smaller than its Q3 2019, with $1.34 billion in top line instead of $1.65 billion in 2019, but the company effectively quadrupled from its preceding quarter. If the company manages another Q3 worth of revenue in Q4, it would be larger than it was in 2018 by a few hundred million.

Critically, Airbnb managed to swing from a number of unprofitable quarters to a profit in Q3, akin to its 2019 Q3 when it was also in the black. Of course, Airbnb’s $219.3 million in GAAP net income during the third quarter pales compared to its losses tallied earlier in the year. The company will not break even in 2020.

Airbnb also reported adjusted profit metrics. Its adjusted EBITDA results are based on the following definition:

Adjusted EBITDA is defined as net income or loss adjusted for (i) provision for income taxes; (ii) interest income, interest expense, and other income (expense), net; (iii) depreciation and amortization; (iv) stock-based compensation expense; (v) net changes to the reserves for lodging taxes for which we may be held jointly liable with hosts for collecting and remitting such taxes; and (vi) restructuring charges.

The decision to remove restructuring costs raised eyebrows, with Amy Cheetham, an investor at Costanoa Ventures, saying that “it feels like leaving out restructuring costs is a little aggressive?” We agree, as it gives the company too much flexibility to count the good in its results, like lower operating costs, while discounting what it took to get those results, like restructuring its business operations.

That’s having your cake and eating it as well and not counting the calories.

Still, who are we to withhold numbers from you? Here is the very adjusted EBITDA that Airbnb claims:

Image Credits: Airbnb S-1

The numbers are still not good even after ripping out so very any costs. Worse, perhaps is the company’s cash burn in the year. That deficit helps explain why Airbnb took on more capital when it did earlier this year.

It’s hard to put a firm grade on this S-1. It contains what we expected, but how investors weigh the company’s year-over-year revenue declines in Q3 2020 against its rapid comeback from Q2 2020 should help decide its eventual value. On the whole Airbnb has managed something incredibly impressive — bouncing back from so low a low.

But, now that it’s going public we can’t merely say “good job”; it wants to price itself well and trade strongly. So, all eyes on its first IPO range as that should tell us what investors just might be willing to pay for the famous company’s equity.

Powered by WPeMatico

One of my favorite series of Monty Python sketches is built around the concept of surprise:

Chapman: I didn’t expect a kind of Spanish Inquisition.

[JARRING CHORD]

[Three cardinals burst in]

Cardinal Ximénez: NOBODY expects the Spanish Inquisition!

I was reminded of this today when I needed to reschedule a few stories so we could cover DoorDash’s S-1 filing from multiple angles. First, Managing Editor Danny Crichton looked at how well the company’s co-founders and many investors stand to make out. Alex Wilhelm covered the IPO announcement in depth on TechCrunch before writing an Extra Crunch column that studied the role the COVID-19 pandemic played in the home-delivery platform’s recent growth.

Our all-hands-on-deck coverage of DoorDash’s S-1 is a good illustration of Extra Crunch’s mission: timely analysis of current and future technology trends that serves founders and investors. We have a talented team, and as today’s coverage shows, they’re just as good as they are fast.

The stories that follow are an overview of Extra Crunch from the last five days. The full articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thanks very much for reading Extra Crunch this week. I hope you have a great weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Klaus Vedfelt / Getty Images

We frequently run posts by guest contributors, but two stories we published this week were written in the first person, which is a bit of a departure.

In Why I left edtech and got into gaming, Darshan Somashekar brought us inside his decision to pivot away from a sector that’s been growing hotter in 2020.

His post is a unique take on two oft-discussed categories, but it also examines one founder/investor’s thought process when it comes to evaluating new opportunities.

Andy Areitio, a partner at early-stage fund TheVentureCity, wrote What I wish I’d known about venture capital when I was a founder, a reflection on the “classic mistakes” founders tend to make when it’s time to fundraise.

“Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time,” he says. “They can also put all their eggs in one basket too early. I made that mistake.”

You can find business writing that explores best practices anywhere, which is why we hunt down stories that are firmly rooted in data or personal experience (which includes success and failure).

Image Credits: DoorDash

The coronavirus pandemic looms large in DoorDash’s S-1 filing.

According to the food-delivery platform, “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” and “the COVID-19 pandemic has further accelerated these trends.”

As in other sectors, the pandemic didn’t wave a magic wand — instead, it hastened trends that were already in play: consumers love convenience, which means DoorDash’s gross order volume and revenue were tracking well before the virus started to shape our lives.

“It’s your call on how to balance the factors and decide whether or not to buy into the IPO, but this one is going to be big,” writes Alex Wilhelm in a supplemental edition of today’s The Exchange.

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

None of us knew DoorDash would release its S-1 filing today, but Danny Crichton jumped on the story “so we can see who is raking in the returns on the country’s delivery startup champion.”

After estimating the value of the respective ownership stakes held by DoorDash’s four co-founders, he turned to the investors who participated in rounds seed through Series H.

Some growth funds are about to look very good after this IPO, and each founder is looking at hundreds of millions, he found.

But even so, their diminished haul of about $1.3 billion is “a sign of just how much dilution the co-founders took given the sheer amount of capital the company fundraised over its life.”

Image Credits: Nigel Sussman (opens in a new window)

Investors sent stacks of cash to late-stage fintech companies in Q3 2020, but these sizable rounds may also point to shrinking opportunities for early-stage firms, reports Alex Wilhelm in this morning’s edition of The Exchange.

2020 could be a record year for fintech VC in Europe and North America, but are these “huge late-stage dollars” actually “a dampener for new fintech startups trying to get off the ground?”

Devin Coldewey interviewed the leaders of three startup accelerators to learn more about the adaptations they’ve made in recent months:

Due to travel bans, shelter-in-place orders and other unknowns, they’ve all shifted to virtual. But accelerators are intensive programs designed to indoctrinate founders and elicit brutally honest feedback in real time.

Despite the sudden shift, that boot-camp mindset is still in effect, Devin reports.

“Cutting out the commute time in a busy city leaves founders with more time for workshops, mentor matchmaking, pitch practice and other important sessions,” said Fernandez. “Everybody just has more flexibility and tranquility.”

Said Ebersweiler: “People are for some reason more participative and have more feedback than physically — it’s pretty strange.”

Image Credits: Greylock

In a recent interview with Greylock partner Asheem Chandna, Managing Editor Danny Crichton asked him about the buzz around no-code platforms and what’s happening in early-stage enterprise startups before segueing into a discussion about “shift left” security:

“Every organization today wants to bring software to market faster, but they also want to make software more secure,” said Chandna.

“There is a genuine interest today in making the software more secure, so there’s this concept of shift left — bake security into the software.”

Image Credits: Nigel Sussman (opens in a new window)

If you missed Wednesday’s The Exchange, Alex scoured earnings reports from PayPal and Square to see what the near future might hold for several fintech startups currently waiting in the wings.

Using Square and PayPal’s recent numbers for stock purchases, card usage and consumer payment activity as a proxy, he attempts to “see what we can learn, and to which unicorns it might apply.”

Image Credits: jayk7 (opens in a new window)/ Getty Images

In California, non-competition agreements can’t be enforced and a court has ruled that customer contact lists aren’t trade secrets.

That doesn’t mean salespeople who switch jobs can start soliciting their former customers on their first day at the new gig, however.

Before you jump ship — or hire a salesperson who already has — read this overview of California’s trade secret laws.

“Even without litigation, a former employer can significantly hamper a departing salesperson’s career,” says Nick Saenz, a partner at Lewis & Llewellyn LLP, who focuses on employment and trade secret issues.

Image: Bryce Durbin / TechCrunch

News of a highly effective COVID-19 vaccine appeared to drive down prices of the three best-known publicly traded edtech companies: 2U, Chegg and Kahoot saw declines of about 20%, 10% and 9%, respectively after the report.

Are COVID-19 tailwinds dissipating, or did the market make a correction because “edtech has been categorically overhyped in recent months?”

Image Credits: Sophie Alcorn

What does President-elect Biden’s victory mean for U.S. immigration and immigration reform?

I’m in tech in SF and have a lot of friends who are immigrant founders, along with many international teammates at my tech company. What can we look forward to?

— Anticipation in Albany

Powered by WPeMatico

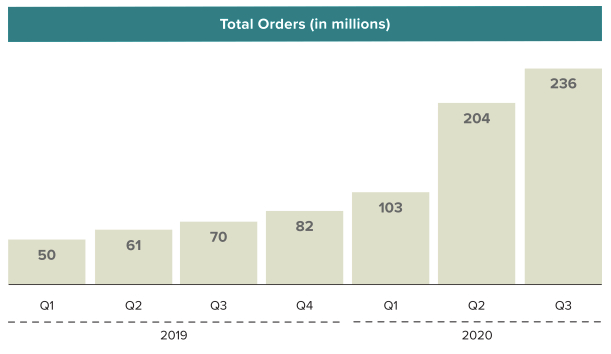

DoorDash filed to go public today, publishing numbers that showed rapid growth, enhanced profitability and an improving cash flow record which helped explain how the company had grown to a $16 billion valuation while private. The unicorn’s impending liquidity event will enrich a host of venture capital firms that bet on its eventual maturity.

Instead of posting this entry of The Exchange on Monday, we’ve put it out today for your Friday and weekend reading. Enjoy! — Alex and Walter.

But notable in DoorDash’s impressive results is the impact of COVID-19, accelerating secular trends already in place, and boosting the unicorn’s growth. Before we get into pricing this IPO and guessing what the company might be worth, let’s strive to understand what portion of its 2020 business gains could stem from the pandemic — and might not persist into the future.

We’re not being pessimistic; we merely want to better understand the company. And DoorDash agrees with our general thrust, writing in its S-1 filing that “58% of all adults and 70% of millennials say that they are more likely to have restaurant food delivered than they were two years ago,” adding that it believes “the COVID-19 pandemic has further accelerated these trends.”

Even more, elsewhere in its filings DoorDash states plainly that COVD-19 led it to experience “a significant increase in revenue, Total Orders, and Marketplace [gross order volume] due to increased consumer demand for delivery, more merchants using our platform to facilitate both delivery and take-out, and improved efficiency of our local logistics platform.” The company then went on to warn investors that the “circumstances that have accelerated the growth of our business stemming from the effects of the COVID-19 pandemic may not continue in the future, and we expect the growth rates in revenue, Total Orders, and Marketplace [gross order volume] to decline in future periods.”

We’re not idly speculating.

Let’s observe how DoorDash’s growth accelerated from 2019 through 2020 and then peek at how the company’s economics improved during the same period, giving the company a shot at adjusted profitability for the full year, a nearly unheard of result in the on-demand market.

DoorDash generates revenue when a customer orders food via its service, splitting the total bill of food costs, taxes, fees and tips, distributing them to itself, the merchant creating the goods and the delivery person.

In an “illustrative” example that DoorDash notes its 2019 “approximate average per-order information,” the split works out as follows:

Given that the company is giving us old data and DoorDash’s performance has been stellar this year in terms of generating more gross profit, I wonder what has happened amidst 2020’s upheaval. But, the old numbers do for what we need, which is to understand the link between gross order volume (GOV) and DoorDash revenue. When the former goes up, the latter goes up.

So, as orders rise:

Powered by WPeMatico

During yesterday’s tense voting and this morning, shares of American-listed technology companies are shooting higher.

The tech-heavy Nasdaq composite is up around 3.35% this morning, more than double what the broad S&P 500 index is currently managing. SaaS and cloud stocks kicked off the day up a staggering 4.98%, a sharp rally in the value of smaller, more growth-oriented technology companies.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

For technology companies on the wings of the IPO market, it’s great news.

In 2020 it can be easy to forget, but tech stocks do not have to rise. They merely have in recent months, perhaps warming the waters for more technology debuts as the fourth quarter races toward its midpoint. The Exchange has heard whispers from several folks that the late-November/early-December period could be active for new filings, bringing rising stocks and pent-up demand together for a possible IPO run.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

We’ll see. Today’s rally — and ballot measure results in California — could be the push companies like Airbnb and DoorDash needed to stop faffing around with private filings.

In pedestrian terms, the getting is good right now for public tech companies, so if you are going to go public, go get got while the getting stays good.

Today, let’s examine recent market gains for tech stocks and remind ourselves who is expected to go public next. Then, of course, chat about all the unicorns on the unofficial IPO list who could find a greased path ahead of them toward a flotation.

Big tech stocks are gaining, small stocks are up and software companies are hot. The NASDAQ is now less than 5% away from its all-time highs, and the Bessemer Cloud Index is now just 9% down from its own, a rebound from its prior status in correction territory. (A correction occurs when an index falls 10% or more from highs.)

So, who does the rally help? Let’s rock through a list:

Powered by WPeMatico

Delivery service DoorDash is giving employers a way to feed their remote employees through a new suite of products called DoorDash for Work.

There are four main products, starting with DashPass for Work, where employers can fund employee memberships to DashPass, a program that eliminates delivery fees on orders from thousands of restaurants. In fact, DoorDash says it already worked with Mt. Sinai to offer free DashPass subscriptions to 42,000 healthcare employees, and that other DashPass for Work customers include Charles Schwab, Hulu and Stanford Research Park.

DoorDash for Work also includes the ability for employers to provide credits for meal orders — there are options for day and time restrictions, so employers can be sure they’re paying for food while someone is working. For teams that are working in-person, there’s the ability to combine individual meal orders into a larger group order. And the service also includes employee gift cards (Zoom, for example, is providing these on employee birthdays).

In a blog post, Broderick McClinton, the head of DoorDash for Work, noted that COVID-19 has had “a profound impact on our daily routines, including the way we eat.”

“Instead of meeting our favorite barista on the way into the office or socializing with our colleagues in the lunch room, we’re spending a lot more time in the kitchen and eating solo at home, missing out on those moments to engage with peers and support our favorite restaurants,” McClinton wrote. “In this new normal, companies are adapting and looking for ways to support their employees’ wellbeing and productivity through new work-from-home corporate wellness benefits, including food perks.”

While free food might seem relatively low on the list of priorities during the pandemic (at least for those of us who have been fortunate enough to keep our jobs), DoorDash says it conducted a survey of 1,000 working Americans last month and found that 90% of them said they miss at least one food-related benefit from the office.

So DoorDash for Work is designed to help employers continue offering benefits in this area, and also it opens up a new source of revenue for DoorDash.

Powered by WPeMatico

Companies that have leveraged technology to make the procurement and delivery of food more accessible to more people have been seeing a big surge of business this year, as millions of consumers are encouraged (or outright mandated, due to COVID-19) to socially distance or want to avoid the crowds of physical shopping and eating excursions.

Today, one of the companies that is supplying produce and other items both to consumers and other services that are in turn selling food and groceries to them, is announcing a new round of funding as it gears up to take its next step, an IPO.

GrubMarket, which provides a B2C platform for consumers to order produce and other food and home items for delivery, and a B2B service where it supplies grocery stores, meal-kit companies and other food tech startups with products that they resell, is today announcing that it has raised $60 million in a Series D round of funding.

Sources close to the company confirmed to TechCrunch that GrubMarket — which is profitable, and originally hadn’t planned to raise more than $20 million — has now doubled its valuation compared to its last round — sources tell us it is now between $400 million and $500 million.

The funding is coming from funds and accounts managed by BlackRock, Reimagined Ventures, Trinity Capital Investment, Celtic House Venture Partners, Marubeni Ventures, Sixty Degree Capital and Mojo Partners, alongside previous investors GGV Capital, WI Harper Group, Digital Garage, CentreGold Capital, Scrum Ventures and other unnamed participants. Past investors also included Y Combinator, where GrubMarket was part of the Winter 2015 cohort. For some context, GrubMarket last raised money in April 2019 — $28 million at a $228 million valuation, a source says.

Mike Xu, the founder and CEO, said that the plan remains for the company to go public (he’s talked about it before), but given that it’s not having trouble raising from private markets and is currently growing at 100% over last year, and the IPO market is less certain at the moment, he declined to put an exact timeline on when this might actually happen, although he was clear that this is where his focus is in the near future.

“The only success criteria of my startup career is whether GrubMarket can eventually make $100 billion of annual sales,” he said to me over both email and in a phone conversation. “To achieve this goal, I am willing to stay heads-down and hardworking every day until it is done, and it does not matter whether it will take me 15 years or 50 years.”

I don’t doubt that he means it. I’ll note that we had this call in the middle of the night his time in California, even after I asked multiple times if there wasn’t a more reasonable hour in the daytime for him to talk. (He insisted that he got his best work done at 4:30 a.m., a result of how a lot of the grocery business works.) Xu on the one hand is very gentle with a calm demeanor, but don’t let his quiet manner fool you. He also is focused and relentless in his work ethic.

When people talk today about buying food, alongside traditional grocery stores and other physical food markets, they increasingly talk about grocery delivery companies, restaurant delivery platforms, meal kit services and more that make or provide food to people by way of apps. GrubMarket has built itself as a profitable but quiet giant that underpins the fuel that helps companies in all of these categories by becoming one of the critical companies building bridges between food producers and those that interact with customers.

Its opportunity comes in the form of disruption and a gap in the market. Food production is not unlike shipping and other older, non-tech industries, with a lot of transactions couched in legacy processes: GrubMarket has built software that connects the different segments of the food supply chain in a faster and more efficient way, and then provides the logistics to help it run.

To be sure, it’s an area that would have evolved regardless of the world health situation, but the rise and growth of the coronavirus has definitely “helped” GrubMarket not just by creating more demand for delivered food, but by providing a way for those in the food supply chain to interact with less contact and more tech-fueled efficiency.

Sales of WholesaleWare, as the platform is called, Xu said, have seen more than 800% growth over the last year, now managing “several hundreds of millions of dollars of food wholesale activities” annually.

Underpinning its tech is the sheer size of the operation: economies of scale in action. The company is active in the San Francisco Bay Area, Los Angeles, San Diego, Seattle, Texas, Michigan, Boston and New York (and many places in between) and says that it currently operates some 21 warehouses nationwide. Xu describes GrubMarket as a “major food provider” in the Bay Area and the rest of California, with (as one example) more than 5 million pounds of frozen meat in its east San Francisco Bay warehouse.

Its customers include more than 500 grocery stores, 8,000 restaurants and 2,000 corporate offices, with familiar names like Whole Foods, Kroger, Albertson, Safeway, Sprouts Farmers Market, Raley’s Market, 99 Ranch Market, Blue Apron, Hello Fresh, Fresh Direct, Imperfect Foods, Misfit Market, Sun Basket and GoodEggs all on the list, with GrubMarket supplying them items that they resell directly, or use in creating their own products (like meal kits).

While much of GrubMarket’s growth has been — like a lot of its produce — organic, its profitability has helped it also grow inorganically. It has made some 15 acquisitions in the last two years, including Boston Organics and EJ Food Distributor this year.

It’s not to say that GrubMarket has not had growing pains. The company, Xu said, was like many others in the food delivery business — “overwhelmed” at the start of the pandemic in March and April of this year. “We had to limit our daily delivery volume in some regions, and put new customers on waiting lists.” Even so, the B2C business grew between 300% and 500% depending on the market. Xu said things calmed down by May and even as some B2B customers never came back after cities were locked down, as a category, B2B has largely recovered, he said.

Interestingly, the startup itself has taken a very proactive approach in order to limit its own workers’ and customers’ exposure to COVID-19, doing as much testing as it could — tests have been, as we all know, in very short supply — as well as a lot of social distancing and cleaning operations.

“There have been no mandates about masks, but we supplied them extensively,” he said.

So far it seems to have worked. Xu said the company has only found “a couple of employees” that were positive this year. In one case in April, a case was found not through a test (which it didn’t have, this happened in Michigan) but through a routine check and finding an employee showing symptoms, and its response was swift: the facilities were locked down for two weeks and sanitized, despite this happening in one of the busiest months in the history of the company (and the food supply sector overall).

That’s notable leadership at a time when it feels like a lot of leaders have failed us, which only helps to bolster the company’s strong growth.

Powered by WPeMatico

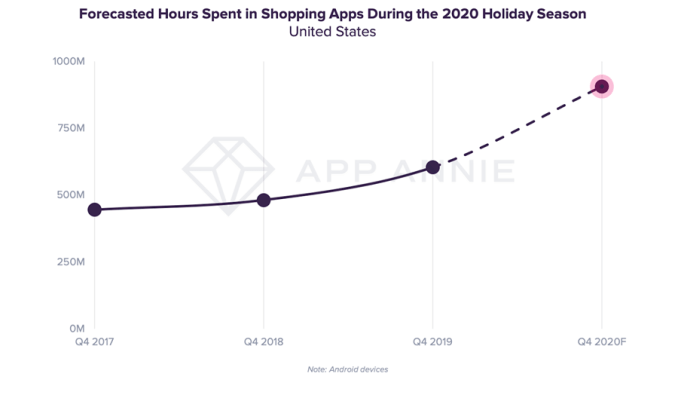

The coronavirus pandemic’s impact on the holiday shopping season is already underway. Amazon has delayed its annual sales event, Prime Day, from July to October 2020, while top e-commerce retailers, including Walmart, Target and Amazon, are becoming more powerful than ever. According to a new report from App Annie, mobile shopping apps are poised to see their biggest shopping season to date. The mobile data and analytics firm is estimating that U.S. consumers will spend more than 1 billion hours on Android devices alone during the fourth quarter, a 50% increase from the same time last year.

This forecast represents a jump ahead for mobile commerce that wasn’t expected until four to six years from now, but the pandemic has pushed that timetable forward.

Image Credits: App Annie

The firm also predicts that the pace of online shopping will look different than in years past.

While, typically, holiday shopping would be concentrated in the weeks around Black Friday and Cyber Monday, it’s expected that the shopping season this year will be longer and more drawn out. To some extent, this could be attributed to Prime Day’s delay, but the economic pressures of the pandemic are also taking their toll.

Heading into the third quarter, unemployment rates in the U.S. were still higher than during the Great Financial Crisis and more than two times higher than pre-COVID rates. App Annie says this will manifest in lower disposable incomes and greater price sensitivity, which will in turn lead consumers to seek out deals and promotions for longer periods of time throughout the lead up to the 2020 holidays.

Prime Day’s delay may also impact the shopping activity that takes place during the normally busy November shopping days, given that the sales event will take place this year much closer to Black Friday and Cyber Monday than ever before.

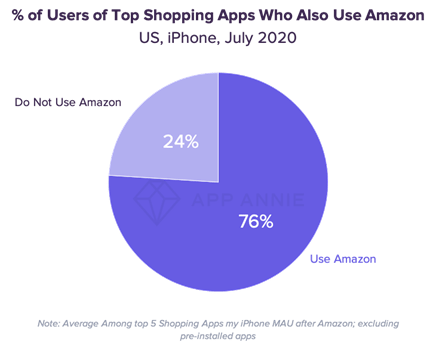

App Annie also noted that Amazon’s app continues to rank No. 1 by monthly active users among U.S. Shopping apps, and sees strong cross-app usage with other top Shopping apps.

Image Credits: App Annie

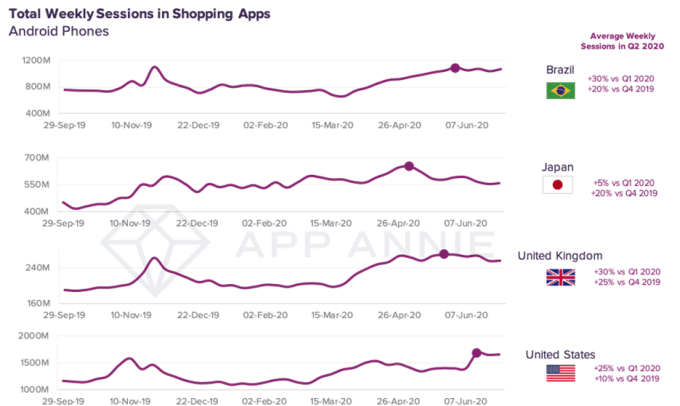

For comparison’s sake, weekly sessions in Shopping apps had grown by 25% during peak weeks during Q4 2019. They were also up 15% in the U.K.

This growth trend will continue as the changes brought on by the pandemic have been built upon existing consumer behavior, which have now been dialed up. Those changes are here to stay, App Annie claims.

Image Credits: App Annie

Related to mobile shopping’s growth, and the more than 1 billion hours spent shopping in Q4 on Android, App Annie also predicts other categories of apps will benefit. PayPal, for example, reported its best quarter ever with total payment volume increasing 29% year over year.

Online grocery services are also booming, particularly in markets with rising COVID-19 cases, like the U.S. and Brazil. Higher usage of mobile grocery shopping apps is expected to continue through Thanksgiving in the U.S., as consumers use apps for checking inventory, self-checkout, delivery and buy online/pickup in store. Similarly, meal delivery services like Uber Eats, DoorDash and Grubhub are also expected to remain valuable and widely used in Q4.

Image Credits: App Annie

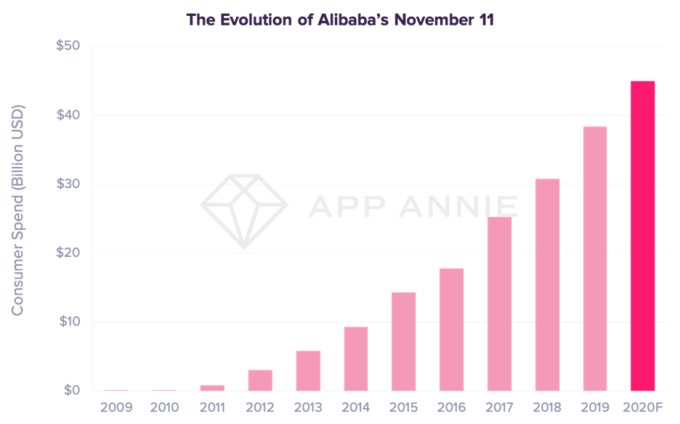

Outside the U.S., App Annie forecasts that Singles Day 2020 will bring in more than 310 billion CNY (over $45 billion in U.S. dollars) to make it the biggest shopping day ever. This will top last year’s record of $38 billion in sales, and follows Q3 2020’s 4.8% year-over-year retail sales growth in China.

Powered by WPeMatico

DoorDash is announcing that customers can now order groceries through the DoorDash app from partners including Smart & Final, Meijer and Fresh Thyme. Additional stores like Hy-Vee and Gristedes/D’Agnostino are supposed to be added in the next few weeks.

Through these partnerships, DoorDash says it has a delivery footprint covering 75 million Americans in markets like the San Francisco Bay Area, Los Angeles, Orange County, Sacramento, San Diego, Chicago, Cincinnati, Milwaukee, Detroit and Indianapolis.

DoorDash began delivering from a wide range of convenience stores earlier this year. Fuad Hannon, the company’s head of new verticals, also noted that a number of grocery stores are already part of the DoorDash Drive program, a white-label service where DoorDash handles last-mile delivery.

So Hannon said introducing grocery delivery into the DoorDash app itself is a “natural extension” of those efforts. And in contrast to many other grocery services, the company promises to deliver within an hour of your order.

“There’s no scheduling, no delivery slots, no day-long waits,” he said.

To achieve this, Hannon said DoorDash has created “deep partnerships and commercial relationships” with the grocery stores, coordinating on things like inventory management. “Embedded shoppers” hired from a staffing agency handle the shopping in each store, and the groceries are then delivered by DoorDash’s Dashers.

Image Credits: DoorDash

Hannon said these deliveries will be handled by “the same pool of Dashers” as restaurant delivery. Individual Dashers will decide for themselves when and if they want to take on groceries as well, but he argued that this provides a new opportunity for them, particularly between mealtimes when there’s not much demand for restaurant delivery.

Asked whether there’s any tension with grocery stores in the Drive program that may prefer bringing in customers through their own websites and apps, Hannon argued that customers in the DoorDash app represent “largely different users,” and he said the company is “philosophically agnostic” about whether customers are making purchases through the grocery store’s website/app or through DoorDash.

“DoorDash provides another convenient way for customers to get the value, selection and quality that Smart & Final offers, especially at a time when some are looking to limit trips outside their homes,” said Navin Cotton, Smart & Final’s director of digital commerce, in a statement. “DoorDash’s on-demand grocery service is a nice addition to our online shopping options and with delivery in under an hour, we know Smart & Final customers are going to appreciate it.”

Grocery prices are set by the merchant and should be the same as what you’d find in-store, Hannon said, though perhaps without buy-one-get-one-free offers and others in-store deals. These deliveries are also included in the company’s DashPass subscription, which offers free delivery and reduced service fees.

DoorDash is also offering prepared meals from a longer list of grocery partners, including Wegmans, Hy-Vee, Gelson’s, Kowalski’s, Big Y World Class Markets, Food City, Village Supermarkets, Save Mart, Lucky, Lucky California and Coborn’s.

Powered by WPeMatico