dollar shave club

Auto Added by WPeMatico

Auto Added by WPeMatico

Last week, Procter & Gamble (P&G) announced that it was terminating plans to acquire razor startup Billie following a U.S. Federal Trade Commission lawsuit to stop the deal.

Last year, Edgewell Personal Care ditched its debt-heavy $1.37 billion deal for Harry’s, Inc, formerly valued at $1 billion after the FTC sought to block the acquisition.

In addition to these FTC challenges, it is also now becoming clear that relying on VC-subsidized products and celebrating outrageous valuations can be problematic for D2C brands. With a few wonderful and rare exceptions such as Rothy’s (which raised $42 million but was profitable from the beginning and generated $140 million in revenue within two years of launching), D2C unicorns are addicted to the cycle of venture funding to feed growth in order to maintain a high valuation multiple.

The path to profitability has become a more important part of the startup story versus growth at all costs.

This works for a while; however, when the path to profitability appears murky and exit options either don’t appear or only appear from nontech companies with very conservative multiples, the walls start crumbling.

In a WWD article, Odile Roujol, the former CEO of Lancôme who launched venture fund FAB Ventures, said, “Generally speaking, the era of $1 billion valuations for beauty companies is over. The people that struggle have been the companies that spend so much money in just a few years.” She went on to say, “The big corporations now … are not ready to spend $1.2 billion, $1.5 billion on such a brand like Glossier.”

This change in sentiment from acquirers is further fueled by recent research on the challenges of turning hypergrowth companies profitable. In his Harvard Business School case study “Direct to Consumer Brands,” Professor Sunil Gupta wrote, “Acquiring DTC brands is easy for incumbent conglomerates, but making them profitable is challenging. More than three years after Unilever acquired Dollar Shave Club, it was still unprofitable.”

Unilever executives learned that the average cost of acquiring a new customer online was about the same as in stores. David Taylor, CEO of P&G, said his company was still figuring out how to turn recently acquired direct-to-consumer brands into profitable businesses.

Taylor summarized this dilemma, saying, “There are many, many launches that grow fast … a business model that makes money is a higher challenge.” Since making these realizations, incumbent conglomerates will be more cautious when considering the acquisition of hyped D2C brands that raised lots of venture capital.

What’s cooler than beauty companies that are (or were) valued at $1 billion? Beauty tech SaaS companies that are worth $5.2 billion at IPO. We don’t hear much about the leading global beauty tech companies such as Meitu and Perfect Corp. because their founders are not celebrity influencers, they don’t have massive Instagram followings here in the U.S. and they are not celebrated in our media. Although their companies are based in Asia and they raised money mostly from Chinese investors, their companies are global successes.

Powered by WPeMatico

Of the various channels available to growth marketers, podcast is among the most misunderstood.

Brands like Dollar Shave Club, Squarespace, and ZipRecruiter have deployed podcast advertising for user acquisition for years, but it’s still a channel that flies under the radar. We have managed tens of millions of dollars in podcast ad spend for challenger brands and market leaders alike, and are eager to share some tricks of the trade.

If you want to test in a channel where early adopters are being rewarded with both attractive CAC and scale, here’s what you need to know:

Dive deeper on podcast ads and other growth marketing tips with Extra Crunch’s ongoing coverage of growth marketing, where Right Side Up was recently featured as a Verified Expert Growth Marketer.

Podcast listeners are a sought after group – the audience trends towards educated, early adopters with a high household income. You can find this profile elsewhere, but what makes podcasts unique is that they are choosing to consume that particular content time and time again. The host becomes a trusted voice to deliver them not only interesting stories and banter, but information on companies as well.

Often podcast advertisers are newcomers or start-ups, and the podcast ad might be the first time the listener has heard about that company. Having the first touch with consumers be from a thorough, personal, and often funny host-read interaction is incredibly valuable and helps brands jump over the credibility hurdle. Compare that to an impersonal banner ad, and I’d choose a podcast ad every time.

Even though the term ‘podcast’ was coined in 2004, advertising in the medium has exploded in the last ~5 years. The IAB has been tracking podcast ad revenue since 2015, when the entire medium generated #105.7 million in ad sales. It recently released its third study of podcast ad revenue, which estimated the US market at $479 million in 2018, with growth accelerating to a projected $1 billion+ by 2021.

Andreesen Horowitz did a great investor profile on the space earlier this year, with a helpful rundown of the holistic ecosystem, from hosting mechanisms and platforms to the pace of podcast monetization.

Historically, the medium has been dominated by a mix of comedians doing their own thing, radio entities simulcasting sports shows, and otherwise popular shows that had a devoted niche following relative to other mediums. Most advertisers bought podcast ads as an extension of their other audio acquisition campaigns.

Then Serial came along, in 2014, exploding into popularity and pop culture. They ran a MailChimp ad that had someone mispronouncing the name of the company as “MailKimp”, which was a funny inside joke for those in the know. Nina Cwik and David Raphael, co-founders of Public Media Marketing, explain the initial conversation around this now iconic spot.

“While discussing a launch sponsorship with sponsors there wasn’t a huge amount of interest in taking a risk on a new show even with the amazing This American Life provenance. MailChimp was committed to supporting Serial. The talented production team at Serial and This American Life created MailKimp and the sponsor was rewarded for believing in the show.”

Not only were they rewarded by being a launch sponsor of one of the most successful podcasts in history, but once Serial and the medium itself expanded, a loving impersonation of Serial host Sarah Koenig and the MailKimp joke eventually made its way into a Saturday Night Live skit. Serial also appealed to a female audience, helping to bring new listeners into the channel, and podcasters and advertisers followed.

Over the past 5 years, the space has diversified. We now see so many different shows with all flavors of true crime, news and politics takes that you don’t hear in the broader media picture, women talking to other women about literally everything, comedy and pop culture pods as diverse as Bodega Boys, Who? Weekly, and RuPaul: What’s the Tee with Michelle Visage, and a podcast to go with every reality and television show you can think of. There are too many shows to talk about; there are over 750,000 shows indexed by iTunes.

So how do companies start testing in podcasts? And how do they do so successfully?

We advise companies to start with a test spend that you consider meaningful in the context of your other customer acquisition efforts. Initial tests in the channel that are properly diversified typically vary from $50,000 to $150,000 in media cost. If the idea of a testing budget in the high five figures makes you gasp, don’t rush it. If you under-invest, you run the risk of a false negative, i.e. you didn’t spend enough to validate performance, or a false positive; when you buy tiny shows, one or two sales may pay back. If you make media decisions at scale based on that data, you may find yourself in deep water. If the risk of testing a new channel and having a dip in your CAC is too great, we recommend you exhaust other channels, like Facebook, before jumping into the podcast space.

Podcast offers advertisers a low barrier to entry. Creative production is limited to producing copy points for hosts to use as they record their ad reads. However, it is quite manual relative to digital channels, and can take weeks to put into place. Most purchasing is done through a show’s sales representation or network, via calls and emails, and set in advance (sometimes way in advance depending on inventory levels). It entails RFPing multiple network partners, doing research and outreach to independent shows, gathering rates and evaluating content, and finally making decisions based on budget and inventory availability. We often describe this as the media puzzle – making sure that the ideal shows, with favorable pricing are available when you want them to be. This can take time and some back and forth with your network rep to set in stone, so give yourself room to plan ahead.

Image via Getty Images / venimo

We buy with a lot of direct shows, sales representation firms, and ad networks. We’re starting to see the beginnings of programmatic and exchange-based inventory become available, but it’s largely impression-based media, which isn’t yet a proven tactic that direct response-oriented advertisers can consistently use for customer acquisition. There are some managed service-like buying partners in the space, that work to varying degrees of efficiency for customer acquisition.

When it comes to choosing what types of shows to partner with, beyond budget and availability, it’s important to remember the obvious choice may not be the best one.

One of the most consistent, and pleasant, surprises in podcast advertising is how well shows that are seemingly unrelated to a product work well for customer acquisition. We’ve worked on products that had a primary target demographic of suburban moms, but guess what? Gamers want to stay at home and order snacks and food delivery, too; they have disposable income and are harder to reach via traditional channels.

If you’re advertising a product targeted to parents, you shouldn’t just test into parenting shows, you should also consider testing into shows with hosts who are parents, but have content not at all or tangentially related to parenting, like Your Mom’s House, with Tom Segura and Christina Pazsitzky. Sure, it’s a comedy podcast, and it’s NSFW (and hilarious). They’re also human parents who they do amazing reads, and their fans are legion.

Ryan Iyengar, CMO of HealthIQ, notes that “hosts with wildly different backgrounds were able to find a through-line to connect ad reads with their audiences, regardless of product line.” Of course, contextual advertising is worth consideration, and there are sometimes unique opportunities, but most successful shows aren’t a bullseye for content.

We’ve also seen the inverse, on contextual fit; food products can either do amazing or not well at all on food-related podcasts. If you have a food product with mass appeal, but one that (for example) many home cooks may already be familiar with, you may be better off doing just about any other popular genre of shows besides food.

Plus, these hosts are pros; they’ve been doing ad reads for everything from mattresses to meal kits for years. They know how to talk about your product in an engaging way.

Doug Hoggatt, the VP of Marketing at Betabrand, agrees, mentioning he would also coach new advertisers to “take the time to test across genres and hosts, you’ll be surprised at the results.” Iyengar is also the former VP of Marketing at ZipRecruiter; if you’ve ever heard a podcast, you may have heard the company advertised once or twice. He also notes, “[regardless of] content of the show, audiences can be interested in all sorts of topics, and are still potential customers. Yes, even hiring managers listen to comedy podcasts!”

Many business-to-business (B2B) advertisers do well in the channel, in part due to higher allowable CAC and high lifetime value (LTV). And the same point about show selection holds true for those audiences, as well. Visnick noted, “[HoneyBook] originally focused on testing industry-specific podcasts as those seemed to be the most natural way to target our prospective customers. We discovered that by diversifying our podcast mix into non-industry content we could still reach our target audience while also growing our reach and overall program performance.”

If we hear something that we think can help us at work, we’re amenable to that message, especially when it comes from our favorite host. Having an open mind to testing has helped so many advertisers unlock additional shows, and possible customers. You can take those insights back to other channels, too, and begin to integrate your campaigns and establish cross-channel frequency.

Pricing in the channel is unstable, and demand-based because inventory is finite; effective CPMs for host read, embedded mid-roll advertisements — by far, the most consistently performing ad unit for customer acquisition in the space — vary from $10 to $100. Yes, really.

Worrying too much about CPMs could mean that you’re leaving behind some of the best inventory in the space. So while it could make sense to cut higher CPM placements from a media plan, you want to be cautious. You could inadvertently cut out potential volume drivers or otherwise highly effective placements.

Image via Getty Images / TwilightShow

The listener is there for the hosts. They relate to them, laugh with them, or laugh at them. They come to expect a performance from them, and often that performance bleeds into the ad reads. Whether it’s a semi-NSFW jingle about MeUndies from Bill Burr, or Joe Rogan recommending his mind-blowing NatureBox snack combination, or Levar Burton delivering an oh-so soothing Calm read.

Alan Abdine, Senior Vice President of Business Development for Rooster Teeth, a network with geeky, gamer shows with a hint of irreverence, said “the best ads are the ads that are organic, natural, and originate from the voice of the show talent. When brands allow our hosts to be themselves, there are more opportunities for entertaining side stories and commentary related to the brand.”

He continues to say his “belief is that if an advertiser is willing to spend money to reach out audience, then let us be the experts on that audience and let us use our own voice to share their message and talking points! They will always get better results in that scenario.”

There is a certain special trust that goes into podcast ads. And to allow hosts to be themselves while also being a positive brand advocate often mean striking a balance between scripting and giving space. The most commonly purchased ad unit for customer acquisition advertisers is a host-read, embedded, mid-roll advertisement, typically :60 in length, but many hosts go over.

Overly scripting the copy can lead to an ad sounding inauthentic and infringe on their creativity. Kate Spencer, the co-host of Forever 35, notes that “often there are a lot of required talking points to hit in a short amount of time. We’re always happy to oblige, but I think it takes away from the organic and conversational nature of the ad, which is what makes podcast advertising especially unique. ”

On the flip side, not scripting enough could lead to a disjointed read where the host is trying to piece value props together on the fly. Nick Freeman, Chief Revenue Officer at Cadence13, explains that “some hosts do like the perfectly written out :60 script, while others like bullets they can riff off of.” Because podcast campaign test across multiple shows and personalities, it’s best to find a starting point in your copy where hosts can be guided, but not stifled. Freeman says “that doesn’t necessarily mean trying to make jokes for comedy hosts, for example, so much as it’s giving the hosts who do well with it the freedom to ad-lib.”

And for those that want to get a little more creative, the space is primed for custom integrations. Recently DoorDash partnered with Rooster Teeth for an ad on a livestream in celebration of a new game their studios were releasing. Since there was a visual element, DoorDash and Rooster Teeth partnered on a creative spin to the ad.

Instead of the typical copy, food would be delivered to the group of hosts while recording. Grant Durando, Senior Marketing Consultant at Right Side Up, works with DoorDash on their podcast campaign and stewarded this unique partnership. “[Rooster Teeth] approached us with the opportunity to engage with the live stream in a deeper way than just a regular podcast ad. It was definitely an unorthodox integration, but exciting to be in front of the right audience for DoorDash, at scale, and in a meaningful, memorable way. Many conversations about chicken nuggets later (which I never thought would be part of my job), Rooster Teeth and Vicious Circle delivered a superb ad experience, [integrating] multiple brand mentions and actually making DoorDash a part of the content itself.”

Zack Boone, Senior Director of Sales at Rooster Teeth, added there is, “nothing better than having clients that understand how impactful utterly stupid things like this can be for a brand.” DoorDash “[offers] industry-leading selection to our customers,” said Micah Moreau, VP of Growth Marketing at DoorDash. “It was incredibly effective to bring the DoorDash experience to life with Rooster Teeth in a highly differentiated, yet relevant way.”

Ads almost always end in some sort of call to action, like use the show’s promo code to save money, or visit a URL to get a free trial of a product for listeners of the show. It’s a way for shows to get credit for their listeners taking some sort of action, usually a purchase, related to hearing the ad.

And it’s how advertisers can figure out if their ad investments are paying back, too. Along those lines, Hoggatt was happy to see “how direct response the channel could be. I was surprised at the lift in site visits and follow-on orders that correlate so closely to when our podcasts drop.” Consumers have been conditioned to listen for that call to action at the end of an advertisement so we can measure a direct response in the channel.

That isn’t to say podcast advertising should displace a highly effective channel like paid social or paid search in your paid marketing testing priorities. We often ask advertisers information about their overall CAC or CPA from other paid marketing efforts like Facebook or Google advertising, and use that data to benchmark target CAC for podcast.

As a general rule of thumb, if you can’t make Facebook or Google work for customer acquisition at meaningful scale, think twice before you engage in testing podcasts at a scale meaningful to your business. But if you’re looking for demand generating channels, podcast is an excellent contender.

“The success we’ve seen from podcast advertising has proven that we can drive sales through paid media outside of “traditional” direct digital response campaigns,” said Visnick. “We’ve significantly grown our podcast budget every quarter since we started testing the channel and it’s now a core part of our overall acquisition strategy and an important part of our media mix.

Image via Getty Images / Olivier Le Moal

Another challenge for advertisers that aren’t used to offline channels is managing indirect activity, also sometimes called breakage. It’s imperative to look at indirect activity to help triangulate response, as another way to get a false negative is to only look at direct response, i.e. direct redemptions of a promo code or sales from only users who visited the vanity URL.

A decent analog is like view-through conversions, but without the technology enablement. You can tell, via tracking, what actions site visitors have taken after exposure to ads on Facebook and Google, etc.

However, there isn’t a way for a consumer to tap or click on your podcast ad, so you don’t have a direct action correlated to ad download or exposure, nor can you track indirect activity (view-through) via pixels or other technology enablement. The aforementioned promo code/vanity URL combo is what generates that direct response.

To get around this breakage and triangulate a full response, advertisers commonly use a post-conversion attribution survey, colloquially referred to as a How Did You Hear About Us? or HDYHAU survey. This allows for a crude, but effective, translation of the impact that podcasts had on that user’s activity.

It helps you determine how much of the activity you’re capturing in paid search, for example, may have actually been driven by podcasts, streaming audio, or television. It’s self-reported data from users, sure, and it can feel a little shaky when you’re used to more precise digital measurement, but it’s how virtually every scaled advertiser in the channel has discovered a path to scale.

It also helps you determine benchmarks before you get into other channels, and can provide a solid look at multi-touch attribution if the survey is designed with best practices, and served to enough of the population to achieve stability.

We already talked about why, even though podcasts are digital audio, we can’t track conversions digitally (we know, it’s a little crazy). Unlike television, where you can use spot-based attribution, or radio, where you can achieve consistent ad exposure and but according to average quarter-hour (AQH) ratings, there’s a delay in both download of an episode and media consumption.

For advertisers, that means performance comes in over time, and it takes a minute to build reach and frequency (R/F). You may see very little activity for the first week or two of a campaign, and then as R/F builds and crescendos, you’ll see conversion activity catch up. That’s when you can start to get a solid picture of return on ad spend (ROAS); you should have structured your tests so you have a good sense of performance by the third or fourth drop with a show.

Looking at results sooner is possible but largely inadvisable. “Give it time,” says Dan Visnick, CMO at HoneyBook, “It can take a few weeks to see the impact from a single podcast, and months to build a strong portfolio.”

One of the biggest mistakes new advertisers in the channel make is getting a false positive, by testing into tiny shows that back out because 2 people bought their product, and then quickly scaling in the same genre only to find out that the content doesn’t scale.

False negatives are also common, when advertisers get cold feet in the first few weeks of an integration, and cancel shows after one ad insertion in a single episode. The channel requires diligence in testing, and if you have other business challenges to navigate, using digital growth channels can help iron out your messaging, landing pages, etc. before you launch offline channels.

Although you may have honed your messaging in other channels, you should expect to be flexible when it comes to podcast creative.

Image via Getty Images / Anastasiia_New

Positive signals in podcast campaigns can also indicate that other audio channels may be ripe for testing, which can help diversify your marketing mix and minimize the pressure on individuals channels. Hoggatt says his “success in podcast advertising proved that it is possible to invest in offline channels and find measurable success.”

SiriusXM and streaming platforms, whether pureplay like Pandora or Spotify, or aggregators like Westwood One and ESPN, are great next steps for advertisers who see the right signals in podcast. For SiriusXM, it’s a high household income audience that are used to paying for a subscription (any subscription model companies out there?), and streaming audiences are choosing to listen to their content, similarly to how podcast listeners choose their content. The podcast landscape is the perfect arena to play in to learn more about how your brand works in offline media and allows there to be a stepping stone into other mediums.

We know that podcast advertising can have a powerful impact on the marketing mix for companies of all sizes. As more and more players get involved in the space, it benefits all involved, from advertisers, to networks, to marketers.

It’s rare to have an opportunity to participate in a nascent medium, and be good stewards of one of the last remaining mediums on earth with finite inventory and listeners who actually respond to ads. And along the way, we hope to change the way people think about traditional offline media channels, like how they can be held to high growth performance standards, and where they intersect with popular digital growth tactics like paid social.

You’ll have to get creative, but with some trust and patience, and adherence to best practices, advertisers can reap significant benefits and customer acquisition, at scale, from podcast advertising campaigns.

Powered by WPeMatico

Neighborhood Goods, the direct to consumer department store hawking brands like Rothy’s, Dollar Shave Club, Buck Mason, Draper James and Stadium Goods, has new cash to expand its storefront for e-commerce juggernauts.

The company has raised $11 million in a new round of financing led by Global Founders Capital, with participation from previous investors Forerunner Ventures, Serena Ventures, NextGen Venture Partners, Allen Exploration, Capital Factory and others.

The Dallas-based startup has raised $25.5 million to date and is expanding into a new location in Austin to complement its stores in Plano, Texas and a location in New York, opening soon, according to the company’s chief executive and co-founder Matt Alexander.

The Neighborhood Goods concept, providing a brick and mortar outlet for online brands, is one that dovetails nicely with backers like Global Founders Capital and Forerunner Ventures, which are both longtime investors in direct to consumer startups.

“As we expand our network of brands, we’re so thrilled to have Neighborhood Goods as a core element of our portfolio for them to test, assess, explore and learn about the impact of physical retail as they grow,” said Global Founders Capital investor Don Stalter.

As the company expands its geographic footprint, it’s also experimenting with different online features, like online browsing of in-store collections and the option for physical, in-store pickup of digital orders. Neighborhood Goods also said it will begin offering an analytics back-end for brand partners to provide data on activations and branded events at the company’s stores.

Powered by WPeMatico

Entrepreneurship in consumer packaged goods (CPG) is being democratized. Every step of the value channel has been compressed and made more affordable (and thereby accessible).

At VMG Ignite, we have worked with dozens of direct-to-consumer startups trying to both find product-market fit and achieve scale through Amazon and online advertising.

This article focuses on customer acquisition, particularly Amazon and online advertising, for the direct-to-consumer (D2C) CPG venture. Selling on Amazon, specifically third-party (3P), has become an increasingly important component of the D2C playbook. About 46% of product searches start on Amazon, which makes it a compelling source of sales even for early-stage ventures.

People say that ideas are a dime a dozen. They aren’t valuable. But finding product-market fit? Now, that’s hard. The gap between an unexecuted idea and proven product-market fit can seem vast. Yet it’s a critical first step because, ultimately, marketing amplifies your product and value proposition.

If they aren’t compelling, marketing will fail. If they’re compelling, even mediocre marketing can often be successful. So start with a great product that people love.

How do you create a great product, you ask? A/B test your product configuration like you A/B test your landing page, copy, and design. Your product is a variable, not a constant. Build, ship, get feedback. Build, ship, get feedback. Turn detractors into your customer panel for testing.

Early-stage D2C companies typically get their first customers through three channels:

The companies that succeed are often the ones that iterate the fastest. In his book Creative Confidence, IDEO founder David Kelley and his co-author (and brother) Tom relay a story of a pottery class that was split into two groups.

The first group was told they would each be graded on the single best piece of pottery they each produced. The second group was told they would each be graded based on the sheer volume of pottery they produced.

Naturally, the first group labored to craft the perfect piece while the second group churned through pottery with reckless abandon. Perhaps not so intuitive, at the end of the class, all the best pottery came from the second group! Iteration was a more effective driver of quality than intentionality.

Don’t know how to manage Amazon or Facebook? Here are some best practices:

Powered by WPeMatico

One of the most-discussed plot twists in recent advertising has been the pivot of Direct-to-Consumer (DTC) brands to linear TV. These data-driven, digital-first players are expanding well beyond Facebook and Instagram—and becoming serious players on the largest traditional medium in advertising.

A January 2019 Video Advertising Bureau study found that in 2018, 120 DTC brands collectively spent over $2 billion in TV ads—up from $1.1 B in 2016. 70 of those 2018 advertisers ran TV ads for the first time.

But while we know that they’re advertising on TV, what may be less discussed is whether they’re succeeding on television—and what strategies they use to achieve their success.

At EDO, we have a unique and differentiated ability to measure how DTC advertisers perform on TV by tracking incremental online searches above baseline in the minutes immediately following individual TV ad airings as viewers translate their interest in advertised brands and products directly into online engagement with them.

By measuring incremental search activity across 60 million national TV ad airings since 2015, we are able to effectively isolate the effects of TV ad placement and creative decisions that are most likely to cause online engagement.

We ran the numbers on DTCs as well as advertisers in various other categories to better understand how DTCs specifically are succeeding in TV ads—and what DTCs who are considering TV advertising can do to achieve success on TV.

The DTC revolution is a quintessential David and Goliath story. In vertical after vertical, small, digital-native upstarts are changing the game and overtaking major brands. Does that story play out on TV as well—or is TV advertising one area where DTC marketers have finally met their match?

To answer that question, EDO looked at how effectively TV ads elicited viewer activity since September 2018 across eight major industry categories including DTC. Guided by historical ad performance across billions of ads, we rated ad performance based on how closely the DTC ads came to meeting the benchmark volume of brand-related online activity in the minutes following each TV ad airing.

We index each industry accordingly—giving an index value of 100 to an ad that meets benchmark standards, and below-par ads getting a score under 100 while higher-scoring ads receive a score over 100. We chose to set our index baseline of 100 to the average Consumer Packaged Good (CPG) ad since it is such a large and broad ad category. Our results are as follows:

Powered by WPeMatico

Aditya and Aarti Kochhar Kaji didn’t set out to start the snack food business Taali Foods when they were studying for their business degrees at Harvard.

The couple both hail from Mumbai and met at the University of Pennsylvania . They were married before starting at Harvard’s Business School and initially were interested in other areas — Aarti was exploring a career in venture capital and Aditya was looking at the food and beverage industry broadly in his classes at Harvard.

Addicted to snack foods like chips and popcorn to fuel her Harvard study sessions, Aarti started making popped water lily seeds as a snack — a food both she and her husband had grown up eating in India, she said.

The seeds, which are high in anti-oxidants and low in fat, have been a staple of Ayurvedic medicine — thanks to their purported anti-inflammatory properties, and are a staple of Indian snacking traditions. Now, with American consumers on the hunt for healthier snacks, they’re becoming a big business in the U.S. as well.

Y Combinator is very on-trend, with its decision to invest and accelerate Taali as part of its most recent cohort of startups. But in this instance you may call the accelerator a fast follower rather than a progenitor of this trend.

No less auspicious a food tastemaker than Whole Foods named water lily seeds as one of the top 10 new food trends of 2019. With that attention, competitors to Taali abound.

Bohana and AshaPops are just two new snack food companies floating on the popped water lily seed movement. Bohana even managed to nab the attention of PepsiCo’s Nutrition Greenhouse competitive accelerator.

It’s no secret that technology investors are investing more heavily in consumer businesses — everything from snack foods to period products and baby formula — and startups need only point to the success of Amazon as the everything store to show that there’s always money to be made in the category.

Indeed, at $1.47 trillion, the consumer packaged goods industry dwarfs technology as a share of the nation’s economy.

As Ryan Caldbeck, the head of the consumer-focused investment firm CircleUp noted last year:

The uptick in tech VC dollars going to the CPG market is partly because tech investing is brutally competitive and saturated, and largely because these VCs are awakening to the strong historical returns in CPG, especially with the trend leaning towards small brands stealing market share.

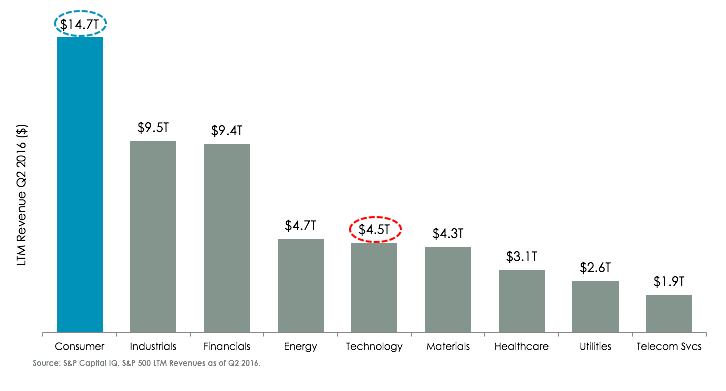

Consumer is a massive market – about 3x the size of tech, as seen below.

Despite the size of the market, the early-stage has historically been underserved by investors due to market inefficiencies like the geographic dispersion of brands and a lack of structured information sources (i.e. there is no Silicon Valley for consumer, and certainly no Crunchbase equivalents – yet).

Strong exits are already possible for consumer brands — and not necessarily from the big-ticket, headline grabbing acquisitions like Dollar Shave Club. Last week This is L. — the condom and period product retailer — sold for roughly $100 million after raising seed funding from investors, including 500 Startups and Y Combinator.

Taali was similarly bootstrapped before it was accepted into Y Combinator. The company is already selling its snacks through Amazon and in retail locations like Fairway in New York and Central Market in Texas. The founders expect to be in stores in California in the next few months.

Powered by WPeMatico

The lines between streetwear and luxury fashion have blurred in recent years, especially as excitement around sneaker brands like Yeezy and Off-White has soared.

A marriage between a luxury fashion marketplace and a sneaker and streetwear reseller seems like a natural way to wrap up M&A in 2018. With that said, Farfetch has acquired New York-based Stadium Goods, opting to pay $250 million for the sneaker startup in a combination of cash and Farfetch stock. Headquartered in London, Farfetch went public on the New York Stock Exchange in September, pricing its shares at $20 apiece and raising $885 million in the process.

What’s more impressive is Stadium Goods’ journey to exit. The company, which sells new and deadstock products online and in a brick-and-mortar store in New York’s Soho neighborhood, was founded in 2015 by John McPheters and Jed Stiller and had only raised $4.6 million in venture capital funding from Forerunner Ventures, The Chernin Group and Mark Cuban, who is an advisor to the startup.

“There was a time not that long ago when you couldn’t wear sneakers and streetwear to nightclubs and restaurants,” McPheters, Stadium Goods’ chief executive officer, told TechCrunch. “But adoption of the stuff we are selling has continued to grow at a very large clip.”

The sale to Farfetch not only provides a major boost to the sneaker tech ecosystem, which is surprisingly much larger than those who aren’t familiar with it might have guessed, but it’s yet another successful e-commerce exit for Kirsten Green, the founding partner of Forerunner Ventures, who’s also backed Dollar Shave Club and Bonobos — direct-to-consumer retailers that sold for $1 billion and $310 million, respectively.

Stadium Goods founders John McPheters (left) and Jed Stiller

Farfetch boarded the sneaker and streetwear hype train a while ago when it incorporated brands like Nike’s Jordan, pairs of which sell for more than $1,000 on the site. The company doubled down on sneakers earlier this year when it began integrating Stadium Goods products. After noticing high-demand, Farfetch founder and CEO José Neves tells TechCrunch, they began acquisition talks with the startup. Stadium Goods will remain independent as part of the deal, with McPheters and Stiller staying on to lead the brand forward. The company’s portfolio of shoes and apparel will be fully available on Farfetch’s e-commerce platform in the coming months.

“Luxury streetwear is a significant part of our business,” Neves said. “For many years now, we have had the largest collection of Off-White, for example, on the internet … What we did not have was the resale, secondary market. It was clear this was an interesting opportunity.”

Together, Farfetch and Stadium Goods will focus on international growth. McPheters tells TechCrunch Stadium Goods already had a significant international base of customers, but a partnership with Farfetch gives them the tools to go places they’ve never been.

“In my mind, we are only just beginning,” McPheters said. “As more and more customers get comfortable with purchasing aftermarket items, we are going to continue to grow.”

The global athletic footwear industry is expected to be worth $95 billion by 2025. Meanwhile, sneaker resale is a $1 billion market and growing, fueled by a cohort of startups making it easier than ever for sneakerheads to locate rare shoes online and have them delivered to their doorsteps. That includes Stadium Goods, Flight Club, GOAT and StockX.

All four of these resellers, which ensure authentication of their products, are backed by VCs. Flight Club merged with GOAT earlier this year and together the pair raised a $60 million Series C. Before that, GOAT had brought in $30 million for its secondary market for collectible shoes from Accel, Upfront Ventures, Matrix Partners and more. StockX, for its part, has raised just over $50 million from Mark Wahlberg, Scooter Braun, Wale, Eminem, SV Angel and others.

According to Crunchbase data, VCs have funneled more than $200 million into sneaker startups in the past two years. Now, given the size of Stadium Goods’ exit, investment in the space will likely pick up significantly as other VCs hope to land an exit multiple that substantial.

Whether the reselling market will continue to expand is in question. Some have called it a bubble poised to burst, claiming it’s at its “height in popularity.” Why? Because corporate shoe brands like Nike and Adidas are keenly aware of the secondary market for their products and how they, too, can profit from it. If they decide to increase the supply of particular shoe models hot on the secondary market, they can radically disrupt the reseller economy. McPheters, however, says this doesn’t concern him.

“Brands need to strangle the demand to keep driving excitement in the space,” McPheters said. “They count on that hype to really move the needle.”

Powered by WPeMatico

Many entrepreneurs assume that an invention carries intrinsic value, but that assumption is a fallacy.

Here, the examples of the 19th and 20th century inventors Thomas Edison and Nikola Tesla are instructive. Even as aspiring entrepreneurs and inventors lionize Edison for his myriad inventions and business acumen, they conveniently fail to recognize Tesla, despite having far greater contributions to how we generate, move and harness power. Edison is the exception, with the legendary penniless Tesla as the norm.

Universities are the epicenter of pure innovation research. But the reality is that academic research is supported by tax dollars. The zero-sum game of attracting government funding is mastered by selling two concepts: Technical merit, and broader impact toward benefiting society as a whole. These concepts are usually at odds with building a company, which succeeds only by generating and maintaining competitive advantage through barriers to entry.

In rare cases, the transition from intellectual merit to barrier to entry is successful. In most cases, the technology, though cool, doesn’t give a fledgling company the competitive advantage it needs to exist among incumbents and inevitable copycats. Academics, having emphasized technical merit and broader impact to attract support for their research, often fail to solve for competitive advantage, thereby creating great technology in search of a business application.

Of course there are exceptions: Time and time again, whether it’s driven by hype or perceived existential threat, big incumbents will be quick to buy companies purely for technology. Cruise/GM (autonomous cars), DeepMind/Google (AI) and Nervana/Intel (AI chips). But as we move from 0-1 to 1-N in a given field, success is determined by winning talent over winning technology. Technology becomes less interesting; the onus is on the startup to build a real business.

If a startup chooses to take venture capital, it not only needs to build a real business, but one that will be valued in the billions. The question becomes how a startup can create a durable, attractive business, with a transient, short-lived technological advantage.

Most investors understand this stark reality. Unfortunately, while dabbling in technologies which appeared like magic to them during the cleantech boom, many investors were lured back into the innovation fallacy, believing that pure technological advancement would equal value creation. Many of them re-learned this lesson the hard way. As frontier technologies are attracting broader attention, I believe many are falling back into the innovation trap.

So what should aspiring frontier inventors solve for as they seek to invest capital to translate pure discovery to building billion-dollar companies? How can the technology be cast into an unfair advantage that will yield big margins and growth that underpin billion-dollar businesses?

Talent productivity: In this age of automation, human talent is scarce, and there is incredible value attributed to retaining and maximizing human creativity. Leading companies seek to gain an advantage by attracting the very best talent. If your technology can help you make more scarce talent more productive, or help your customers become more productive, then you are creating an unfair advantage internally, while establishing yourself as the de facto product for your customers.

Great companies such as Tesla and Google have built tools for their own scarce talent, and build products their customers, in their own ways, can’t do without. Microsoft mastered this with its Office products in the 1990s through innovation and acquisition, Autodesk with its creativity tools, and Amazon with its AWS Suite. Supercharging talent yields one of the most valuable sources of competitive advantage: switchover cost. When teams are empowered with tools they love, they will loathe the notion of migrating to shiny new objects, and stick to what helps them achieve their maximum potential.

Marketing and distribution efficiency: Companies are worth the markets they serve. They are valued for their audience and reach. Even if their products in of themselves don’t unlock the entire value of the market they serve, they will be valued for their potential to, at some point in the future, be able to sell to the customers that have been tee’d up with their brands. AOL leveraged cheap CD-ROMs and the postal system to get families online, and on email.

Dollar Shave Club leveraged social media and an otherwise abandoned demographic to lock down a sales channel that was ultimately valued at a billion dollars. The inventions in these examples were in how efficiently these companies built and accessed markets, which ultimately made them incredibly valuable.

Network effects: Its power has ultimately led to its abuse in startup fundraising pitches. LinkedIn, Facebook, Twitter and Instagram generate their network effects through internet and Mobile. Most marketplace companies need to undergo the arduous, expensive process of attracting vendors and customers. Uber identified macro trends (e.g. urban living) and leveraged technology (GPS in cheap smartphones) to yield massive growth in building up supply (drivers) and demand (riders).

Our portfolio company Zoox will benefit from every car benefiting from edge cases every vehicle encounters: akin to the driving population immediately learning from special situations any individual driver encounters. Startups should think about how their inventions can enable network effects where none existed, so that they are able to achieve massive scale and barriers by the time competitors inevitably get access to the same technology.

Offering an end-to-end solution: There isn’t intrinsic value in a piece of technology; it’s offering a complete solution that delivers on an unmet need deep-pocketed customers are begging for. Does your invention, when coupled to a few other products, yield a solution that’s worth far more than the sum of its parts? For example, are you selling a chip, along with design environments, sample neural network frameworks and data sets, that will empower your customers to deliver magical products? Or, in contrast, does it make more sense to offer standard chips, licensing software or tag data?

If the answer is to offer components of the solution, then prepare to enter a commodity, margin-eroding, race-to-the-bottom business. The former, “vertical” approach is characteristic of more nascent technologies, such as operating robots-taxis, quantum computing and launching small payloads into space. As the technology matures and becomes more modular, vendors can sell standard components into standard supply chains, but face the pressure of commoditization.

A simple example is personal computers, where Intel and Microsoft attracted outsized margins while other vendors of disk drives, motherboards, printers and memory faced crushing downward pricing pressure. As technology matures, the earlier vertical players must differentiate with their brands, reach to customers and differentiated product, while leveraging what’s likely going to be an endless number of vendors providing technology into their supply chains.

A magical new technology does not go far beyond the resumes of the founding team.

What gets me excited is how the team will leverage the innovation, and attract more amazing people to establish a dominant position in a market that doesn’t yet exist. Is this team and technology the kernel of a virtuous cycle that will punch above its weight to attract more money, more talent and be recognized for more than it’s product?

Powered by WPeMatico

We’re hearing from our sources Unilever has been in serious talks with the Honest Company, and may very well win the bid for the e-commerce startup, though our sources stressed that the deal is in early stages.

We’re hearing from our sources Unilever has been in serious talks with the Honest Company, and may very well win the bid for the e-commerce startup, though our sources stressed that the deal is in early stages.

As usual, the deal is fluid and the final details could change (or not happen at all), and the exact price in the conversation could not be learned, though one source said the… Read More

Powered by WPeMatico

It wasn’t so long ago that venture capital was a suburban California phenomenon. Los Angeles didn’t have much in terms of a real tech scene — and even San Francisco only had a few VCs or tech companies. Now, VC offices have sprung up in San Francisco, moving more of the investment energy up there. That great migration of companies and activity touches upon what is now… Read More

It wasn’t so long ago that venture capital was a suburban California phenomenon. Los Angeles didn’t have much in terms of a real tech scene — and even San Francisco only had a few VCs or tech companies. Now, VC offices have sprung up in San Francisco, moving more of the investment energy up there. That great migration of companies and activity touches upon what is now… Read More

Powered by WPeMatico