DocuSign

Auto Added by WPeMatico

Auto Added by WPeMatico

Postman, a five-year-old startup that is attempting to simplify development, tests and management of APIs through its platform, has raised $50 million in a new round to scale its business.

The Series B for the startup, which began its journey in India, was led by CRV and included participation from existing investor Nexus Venture Partners . The startup, with offices in India and San Francisco, closed its Series A financing round four years ago and has raised $58 million to date.

Postman offers a development environment which a developer or a firm could use to build, publish, document, design, monitor, test and debug their APIs. Postman, like some other startups such as RapidAPI, also maintains a marketplace to offer APIs for quick integration with other popular services.

The startup was co-founded by Abhinav Asthana, a former intern at Yahoo . Asthana was frustrated with how APIs were an afterthought for many developers, as they usually got around to building them in the eleventh hour. Additionally, developers were relying on their own workflows and there was no organized platform that could be used by many, he explained in an interview with TechCrunch.

Even big software firms have not looked into this space yet, and many have instead become a customer of Postman. “We are solving a fundamental problem for the technology landscape. Big companies tend to be slower as they have many other things on their plate,” said Asthana.

Five years later, Postman has grown significantly. More than 7 million users and 300,000 companies, including Microsoft, Twitter, Best Buy, AMC Theaters, PayPal, Shopify, BigCommerce and DocuSign today use Postman’s platform.

The modern software development relies heavily on APIs as more businesses begin to talk with one another. According to research firm Gartner, more than 65% of global infrastructure service providers’ revenue will be generated through services enabled by APIs by 2023, up from 15% in 2018.

Asthana said Postman intends to use the fresh capital to scale its startup, products and grow its team. “We are scaling rapidly across all dimensions. There are many use cases that we still want to address over the coming months. We will also experiment with sales and invest in improving user experience,” he added.

Postman offers some of its services in limited capacity for free to users. For the rest, it charges between $8 to $18 per user to its customers. That’s how the company generates revenue. Asthana declined to share the financial performance of the startup, but said its customer base was “growing phenomenally.”

Postman said CRV general partner Devdutt Yellurkar has joined its board of directors.

Powered by WPeMatico

Google today announced a few new workflow integrations for its Drive file storage service that’ll bring to the service support for some features from DocuSign and process automation platforms K2 and Nintex.

None of these new integrations are all that unusual, but if you use a combination of Drive and the newly supported tools, they will undoubtedly make your daily work a little bit easier.

For DocuSign, the new integration lets you prepare, sign and store your documents right in Google Drive, as well as trigger actions like billing, account activation and payments after an agreement has been signed.

The K2 integration is a bit different and focuses on that company’s machine learning tools. It’ll allow users to train models on a workflow (using Google machine learning tools) and then, for example, determine whether a loan should be automatically approved or denied, with all of the information about those requests and the approval process stored in a Google Sheet. The integration also supports more pedestrian use cases, though, including the ability to make lots of documents in Drive more easily discoverable.

“K2 is committed to simplifying the way in which our customers connect and manage their information, whether it resides on-premise or in the cloud,” said Eyal Inbar, vice president of Global Technology Alliances at K2. “By integrating with Google Drive, we are able to put the next-generation of content management services in the hands of our customers so they can build and implement powerful workflows into their applications.”

Nintex’s solution seems to be a bit more specialized, with a focus on contract management lifecycles for HR, legal and sales use cases. There’s nothing exciting about managing contracts, but that’s probably a good thing, and ideally, adding more automation will help to keep it that way.

Powered by WPeMatico

Workato, a startup that offers an integration and automation platform for businesses that competes with the likes of MuleSoft, SnapLogic and Microsoft’s Logic Apps, today announced that it has raised a $25 million Series B funding round from Battery Ventures, Storm Ventures, ServiceNow and Workday Ventures. Combined with its previous rounds, the company has now received investments from some of the largest SaaS players, including Salesforce, which participated in an earlier round.

At its core, Workato’s service isn’t that different from other integration services (you can think of them as IFTTT for the enterprise), in that it helps you to connect disparate systems and services, set up triggers to kick off certain actions (if somebody signs a contract on DocuSign, send a message to Slack and create an invoice). Like its competitors, it connects to virtually any SaaS tool that a company would use, no matter whether that’s Marketo and Salesforce, or Slack and Twitter. And like some of its competitors, all of this can be done with a drag-and-drop interface.

What’s different, Workato founder and CEO Vijay Tella tells me, is that the service was built for business users, not IT admins. “Other enterprise integration platforms require people who are technical to build and manage them,” he said. “With the explosion in SaaS with lines of business buying them — the IT team gets backlogged with the various integration needs. Further, they are not able to handle all the workflow automation needs that businesses require to streamline and innovate on the operations.”

Battery Ventures’ general partner Neeraj Agrawal also echoed this. “As we’ve all seen, the number of SaaS applications run by companies is growing at a very rapid clip,” he said. “This has created a huge need to engage team members with less technical skill-sets in integrating all these applications. These types of users are closer to the actual business workflows that are ripe for automation, and we found Workato’s ability to empower everyday business users super compelling.”

Tella also stressed that Workato makes extensive use of AI/ML to make building integrations and automations easier. The company calls this Recipe Q. “Leveraging the tens of billions of events processed, hundreds of millions of metadata elements inspected and hundreds of thousands of automations that people have built on our platform — we leverage ML to guide users to build the most effective integration/automation by recommending next steps as they build these automations,” he explained. “It recommends the next set of actions to take, fields to map, auto-validates mappings, etc. The great thing with this is that as people build more automations — it learns from them and continues to make the automation smarter.”

The AI/ML system also handles errors and offers features like sentiment analysis to analyze emails and detect their intent, with the ability to route them depending on the results of that analysis.

As part of today’s announcement, the company is also launching a new AI-enabled feature: Automation Editions for sales, marketing and HR (with editions for finance and support coming in the future). The idea here is to give those departments a kit with pre-built workflows that helps them to get started with the service without having to bring in IT.

Powered by WPeMatico

HeadSpin has closed a $20 million Series B, valuing the provider of mobile application performance software at $500 million. New investors ICONIQ Capital, Battery Ventures and EQT Ventures participated in the funding round. Existing backers GV, Telstra Ventures, Danhua Capital, Nexus Ventures Partners and NextWorld Capital did not participate.

The company emerged from stealth last year with Manish Lachwani at the helm. Lachwani was the former principal architect of the Amazon Kindle, chief technology officer of mobile gaming company Zynga and co-founder and chief technology officer of Google-acquired Appurify, which helped developers automate testing and optimization of their mobile apps and websites.

He’s been in the application performance management business for a long time; under his leadership, Palo Alto-based HeadSpin has quickly grown into one of the fastest growing, though relatively unknown, startups in Silicon Valley.

“What HeadSpin has been able to achieve in its first three years is remarkable, and it has already attracted dozens of major clients across the mobile ecosystem,” ICONIQ partner Will Griffith said in a statement. “The company is quickly becoming the new standard of record for all mobile ecosystem players going forward. It’s one of the fastest-scaling software companies we’ve seen.”

HeadSpin works with Tinder, DocuSign and some 200 other app providers, allowing the companies to test and monitor their apps in real-time and on real devices before, during and after an app is released. The AI-enabled platform gives developers the ability to experience their app just as any regular user would and highlights high priority issues so companies can quickly resolve customer’s problems at scale.

Founded in 2015, HeadSpin says it expects to double revenue in 2018 but did not disclose any financial metrics.

Chief technology officer Brien Colwell is the other half of the company’s founding team. Colwell is the founder and former CEO of Nextop.io, a Y Combinator graduate and app optimization startup. Colwell and Lachwani are joined by HeadSpin’s head of product Sriram Krishnan, Tinder’s former head of international growth. Krishnan joined HeadSpin in October 2017 after working with HeadSpin’s toolset in his role at the app-based dating company.

“When I signed up for HeadSpin, I found out how phenomenal the product was,” Krishnan told TechCrunch .

“A lot of what we built was predicated on the fact that the mobile ecosystem is still very new,” he added. “If you think about the apps world, it’s only been around 10 years … It’s the Wild West out there when it comes to understanding performance.”

Powered by WPeMatico

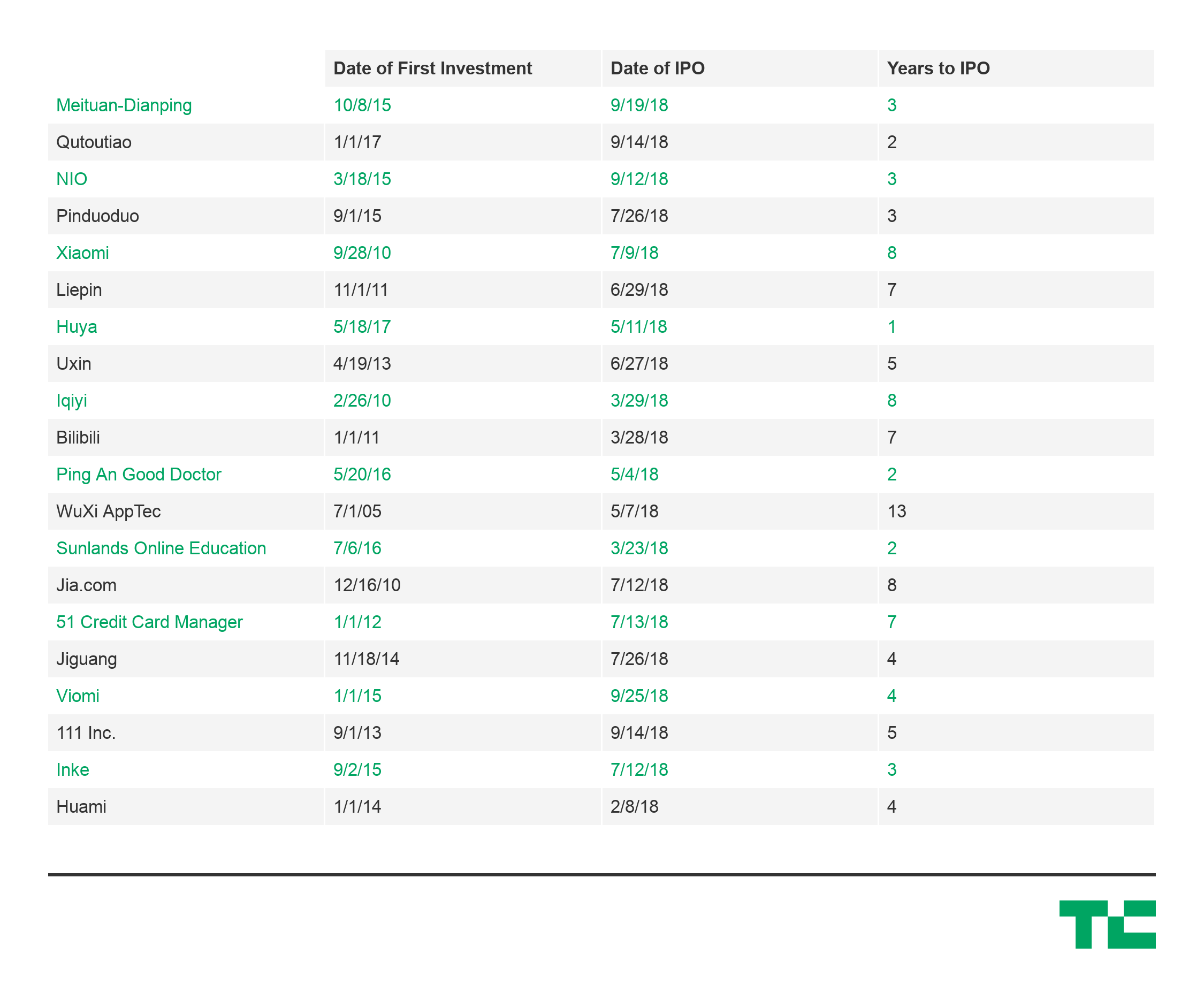

This year’s rush of IPOs from Chinese tech companies has dominated headlines, but what’s more interesting is how quickly they got there.

Traditionally, “going public” represented the gratifying culmination of sleepless nights and missed birthdays that went into building a company. The peak of a lengthy climb, where founders and VCs would finally see the fruits of their labor.

However, Chinese companies appear to be reaching that peak much quicker than their American peers, heading to the public markets only a few years after initial venture investments, and often with little operating history.

Analyzing twenty of the most high profile Chinese tech IPOs this year, the average time from first venture investment to IPO was only around three to five years. Take e-commerce platform Pinduoduo, which pulled in $1.6 billion less than three years after its Series A. Or the recent IPO of EV-manufacturer NIO, which raised a billion dollars just three-and-a-half years after its Series A and having just delivered its first car in June.

China IPO data for 2018 compiled from NASDAQ, Pitchbook, and Crunchbase

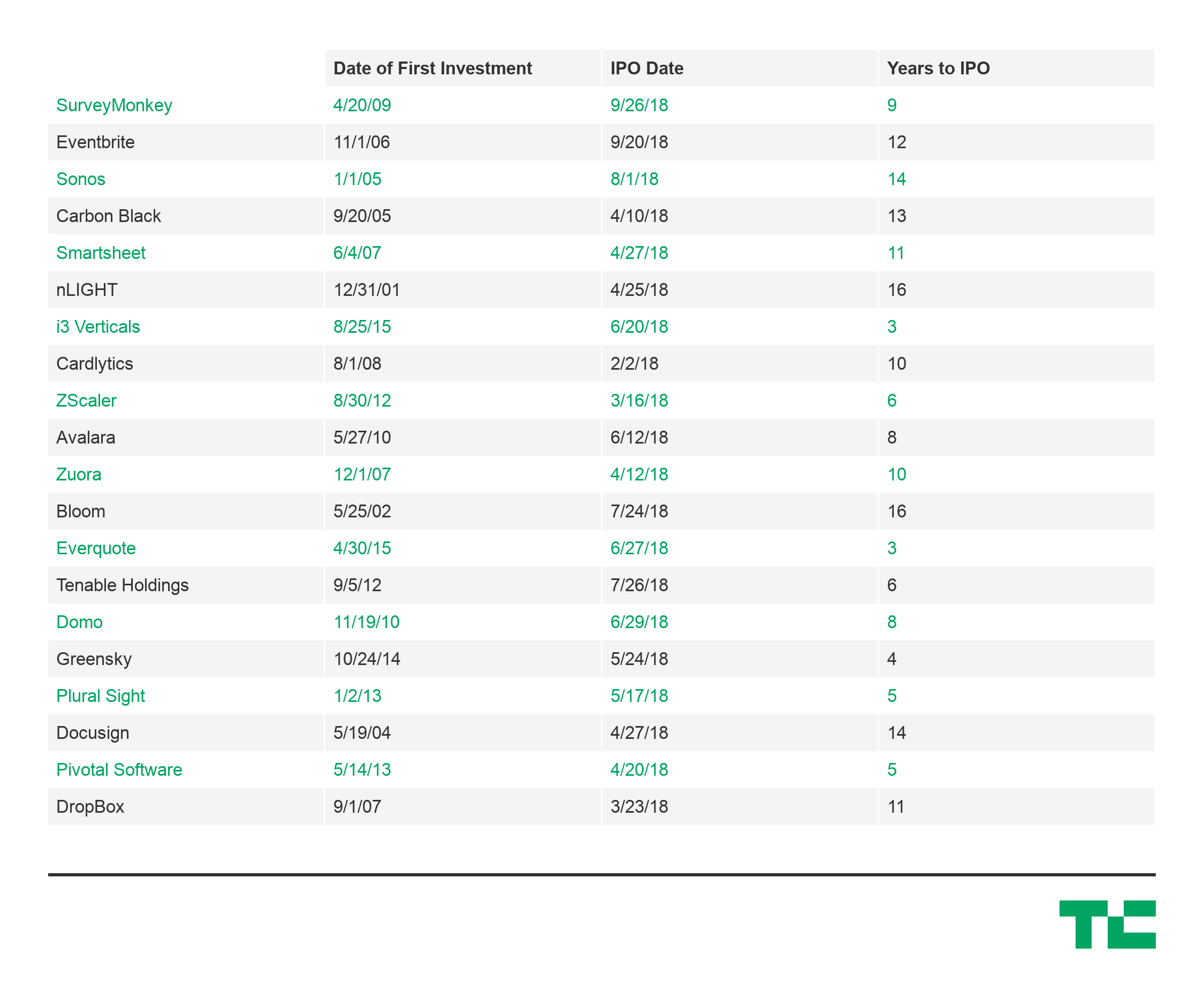

That’s less than half the average 10-year timeline for venture-backed US tech companies that went public in 2018, including Dropbox, Eventbrite, and DocuSign, which all IPO’d more than a decade after their initial investments.

Differences in market maturity, government involvement, and support from large tech incumbents all undoubtedly play a factor, but the speed to liquidity for the Chinese companies is still astounding.

Speed to liquidity is a critical metric for the health of a startup ecosystem. It creates a positive cycle where faster liquidity can drive faster fundraising, faster reinvestment, faster startup building, and faster public liquidity again. An accelerated cycle could be especially appealing for funds with LPs that require faster returns due to cash commitments or otherwise.

It’s important to note that venture returns are a function of capital and time, so quicker exits will also drive higher returns for the same amount invested. For example, a $1 million investment with a $5 million exit after ten years would generate an Internal Rate of Return (a commonly used metric to evaluate VC performance) of 20%. If the same exit occurred after five years, the IRR would be 50%.

Liquidity is a key consideration as China’s influence on the flow of global venture capital intensifies. As China’s tech ecosystem sees more of its darlings mature and more consistently deliver smashing exits, investments in China will have to be a more serious consideration for VCs, even if only to minimize the sheer amount of time, resources, and painstaking energy needed to build a company in the U.S.

Powered by WPeMatico

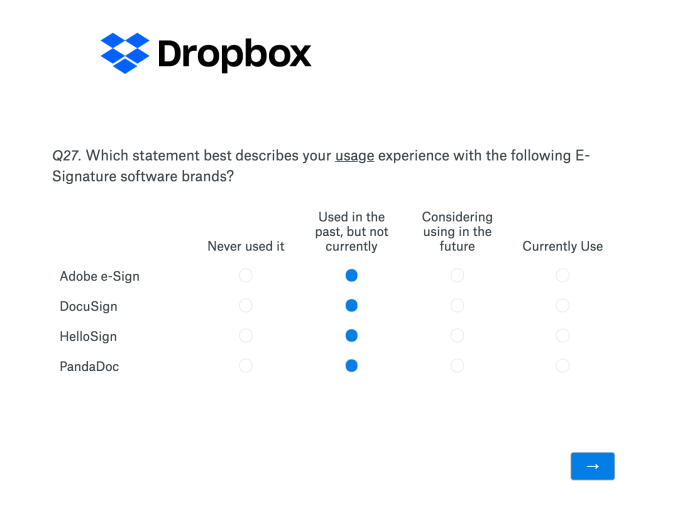

A recent user survey sent out by Dropbox confirms the company is considering the addition of an electronic signature feature to its Dropbox Professional product, which it refers to simply as “E-Signature from Dropbox.” The point of the survey is to solicit feedback about how likely users are to use such a product, how often, and if they believe it would add value to the Dropbox experience, among other things.

While a survey alone doesn’t confirm the feature is in the works, it does indicate how Dropbox is thinking about its professional product.

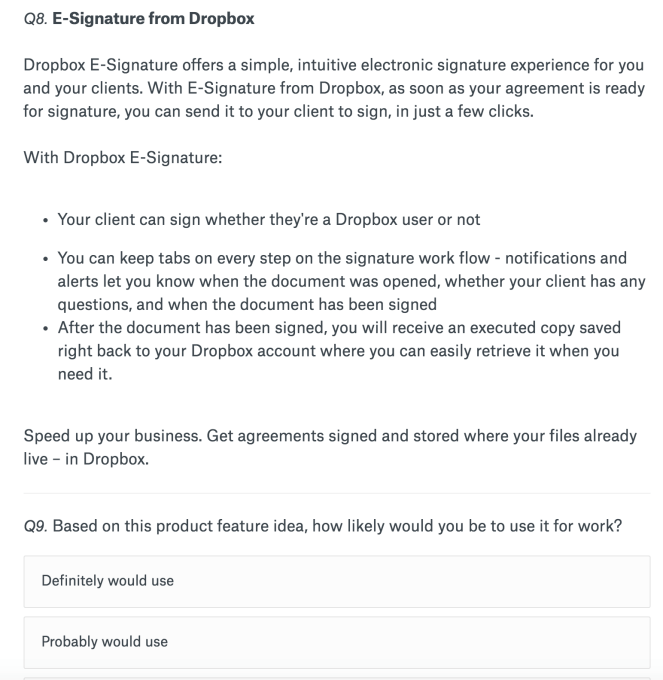

According to the company’s description of E-Signature, the feature would offer “a simple, intuitive electronic signature experience for you and your clients” where documents could be sent to others to sign in “just a few clicks.”

The clients also wouldn’t have to be Dropbox users to sign, the survey notes. And the product would offer updates on every step of the signature workflow, including notifications and alerts about the document being opened, whether the client had questions, and when the document was signed. After the signed document is returned, the user would receive the executed copy saved right in their Dropbox account for easy access, the company says.

In addition to soliciting general feedback about the product, Dropbox also asked survey respondents about their usage of other e-signature brands, like Adobe e-Sign, DocuSign, HelloSign, and PandaDoc, as well as their usage other more traditional methods, like in-person signing and documents sent over mail.

Given the numerous choices on the market today, it’s unclear if Dropbox will choose to move forward and launch such a product. However, if it did, the benefit of having its own E-Signature service would be its ability to be more tightly integrated into Dropbox’s overall product experience. It could also push more business users to upgrade from a basic consumer account to the Professional tier.

This kind of direct integration would make sense in the context of Dropbox’s business workflows. If, for instance, a company is working on a contract workflow, being able to move to the signature phase without changing context (or to share with a user who doesn’t use Dropbox) could add tremendous value over and above simply storing the document.

Companies like Dropbox have been looking for ways to move beyond pure storage to give customers the ability to collaborate and share that content, particularly without forcing them to leave the application to complete a job. This ability to do work without task switching is something that Dropbox has been working on with Dropbox Paper.

While it remains to be seen how they would implement such a solution, it might be a case where it would make more sense to partner with existing vendors or buy a smaller player than it would be build such functionality from scratch — although it’s not clear from a simple survey what their ultimate goal would be at this point.

Dropbox has not yet responded to requests for comment.

Powered by WPeMatico

Elastic, the provider of subscription-based data search software used by Dell, Netflix, The New York Times and others, has unveiled its IPO filing after confidentially submitting paperwork to the SEC in June. The company will be the latest in a line of enterprise SaaS businesses to hit the public markets in 2018.

Headquartered in Mountain View, Elastic plans to raise $100 million in its NYSE listing, though that’s likely a placeholder amount. The timing of the filing suggests the company will transition to the public markets this fall; we’ve reached out to the company for more details.

Elastic will trade under the symbol ESTC.

The business is known for its core product, an open-source search tool called ElasticSearch. It also offers a range of analytics and visualization tools meant to help businesses organize large data sets, competing directly with companies like Splunk and even Amazon — a name it mentions 14 times in the filing.

“Amazon offers some of our open source features as part of its Amazon Web Services offering. As such, Amazon competes with us for potential customers, and while Amazon cannot provide our proprietary software, the pricing of Amazon’s offerings may limit our ability to adjust,” the company wrote in the filing, which also lists Endeca, FAST, Autonomy and several others as key competitors.

This is our first look at Elastic’s financials. The company brought in $159.9 million in revenue in the 12 months ended July 30, 2018, up roughly 100 percent from $88.1 million the year prior. Losses are growing at about the same rate. Elastic reported a net loss of $18.5 million in the second quarter of 2018. That’s an increase from $9.9 million in the same period in 2017.

Founded in 2012, the company has raised about $100 million in venture capital funding, garnering a $700 million valuation the last time it raised VC, which was all the way back in 2014. Its investors include Benchmark, NEA and Future Fund, which each retain a 17.8 percent, 10.2 percent and 8.2 percent pre-IPO stake, respectively.

A flurry of business software companies have opted to go public this year. Domo, a business analytics company based in Utah, went public in June raising $193 million in the process. On top of that, subscription biller Zuora had a positive debut in April in what was a “clear sign post on the road to SaaS maturation,” according to TechCrunch’s Ron Miller. DocuSign and Smartsheet are also recent examples of both high-profile and successful SaaS IPOs.

Powered by WPeMatico

Mixmax, a service that aims to make email and other outbound communications more usable and effective, today announced the official launch of its new IFTTT-like rules for automating many of the most repetitive aspects of your daily email workflow.

On the one hand, this new feature is a bit like your standard email filter on steroids (and with connections to third-party tools like Slack, Salesforce, DocuSign, Greenhouse and Pipedrive). Thanks to this, you can now receive an SMS when a customer who spends more than $5,000 a month emails you, for example.

But rules also can be triggered by any of the third-party services the company currently supports. Maybe you want to send out a meeting reminder based on your calendar entries, for example. You can then set up a rule that always emails a reminder a day before the meeting, together with all the standard info you’d want to send in that email.

“One way we think about Mixmax is that we want to do for externally facing teams and people who talk a lot of customers what GitHub did for engineering and what Slack did for internal team communication,” Mixmax co-founder and CEO Olof Mathé told me. “That’s what we do for external communication.”

While the service started out as a basic Chrome extension for Gmail, it’s now a full-blown email automation system that offers everything from easy calendar sharing to tracking when recipients open an email and, now, building rules around that. Mathé likened it to an executive assistant, but he stressed that he doesn’t think Mixmax is taking anybody’s jobs away. “We’re not here to replace other people,” he said. “We amplify what you are able to do as an individual and give you superpowers so you can become your own personal chief of staff so you get more time.”

The new rules feature takes this to the next level and Mathé and his team plan to build this out more over time. He teased a new feature called “beast mode” that’s coming in the near future and that will see Mixmax propose actions you can take across different applications, for example.

Many of the new rules and connectors will be available to all paying users, though some features, like access to your Salesforce account, will only be available to those on higher-tier plans.

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

DocuSign CEO Dan Springer was all smiles at the Nasdaq on Friday, following the company’s public debut.

And he had a lot to be happy about. After pricing the IPO at a better-than-expected $29, the company raised $629 million. Then DocuSign finished its first day of trading at $39.73, up 37% in its debut.

Springer, who took over DocuSign just last year, spoke with TechCrunch in a video interview about the direction of the company. “We’ve figured out a way to help businesses really transform the way they operate,” he said about document-signing business. The goal is to “make their life more simple.”

But when asked about the competitive landscape which includes Adobe Sign and HelloSign, Springer was confident that DocuSign is well-positioned to remain the market leader. “We’re becoming a verb,” he said. Springer believes that DocuSign has convinced large enterprises that it is the most secure platform.

Yet the IPO was a long-time coming. The company was formed in 2003 and raised over $500 million over the years from Sigma Partners, Ignition Partners, Frazier Technology Partners, Bain Capital Ventures and Kleiner Perkins, amongst others. It is not uncommon for a venture-backed company to take a decade to go public, but 15 years is atypical, for those that ever reach this coveted milestone.

Dell Technologies Capital president Scott Darling, who sits on the board of DocuSign, said that now was the time to go public because he believes the company “is well positioned to continue aggressively pursuing the $25 billion e-signature market and further revolutionizing how business agreements are handled in the digital age.”

Sales are growing, but it is not yet profitable. DocuSign brought in $518.5 million in revenue for its fiscal year ending in 2018. This is an increase from $381.5 million last year and $250.5 million the year before. Losses for this year were $52.3 million, reduced from $115.4 million last year and, $122.6 million for 2016.

Springer says DocuSign won’t be in the red for much longer. The company is “on that fantastic path to GAAP profitability.” He believes that international expansion is a big opportunity for growth.

Powered by WPeMatico