Distributed Ledger

Auto Added by WPeMatico

Auto Added by WPeMatico

In the 1990s when the web was young, companies like Yahoo, created directories of web pages to help make them more discoverable. Hacera wants to bring that same idea to blockchain, and today it announced the launch of the Hacera Network Registry.

CEO Jonathan Levi says that blockchains being established today risk being isolated because people simply can’t find them. If you have a project like the IBM -Maersk supply chain blockchain announced last month, how does an interested party like a supplier or customs authority find it and ask to participate? Up until the creation of this registry, there was no easy way to search for projects.

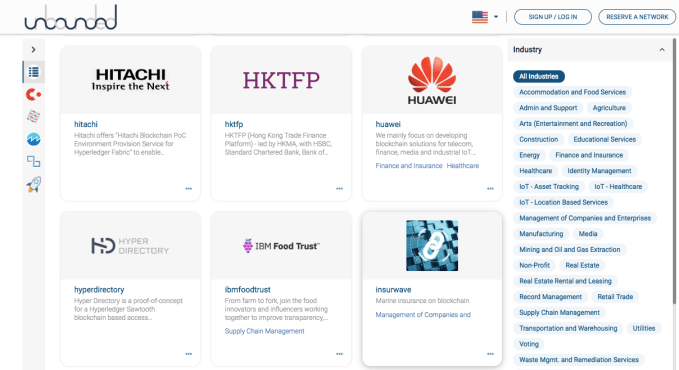

Early participants include heavy hitters like Microsoft, Hitachi, Huawei, IBM, SAP and Oracle, who are linking to projects being created on their platforms. The registry supports projects based on major digital ledger communities including Hyperledger, Quorum, Cosmos, Ethereum and Corda. The Hacera Network Registry is built on Hyperledger Fabric, and the code is open source. (Levi was Risk Manager for Hyperledger Fabric 1.0.)

Hacera Network Registry page

While early sponsors of the project include IBM and Hyperledger Fabric, Levi stressed the network is open to all. Blockchain projects can create information pages, not unlike a personal LinkedIn page, and Hacera verifies the data before adding it to the registry. There are currently more than 70 networks in the registry, and Hacera is hoping this is just the beginning.

Jerry Cuomo, VP of blockchain technologies at IBM, says for blockchain to grow it will require a way to register, lookup, join and transact across a variety of blockchain solutions. “As the number of blockchain consortiums, networks and applications continues to grow we need a means to list them and make them known to the world, in order to unleash the power of blockchain,” Cuomo told TechCrunch. Hacera is solving that problem.

This is exactly the kind of underlying infrastructure that the blockchain requires to expand as a technology. Cuomo certainly recognizes this.”We realized from the start that you cannot do blockchain on your own; you need a vibrant community and ecosystem of like-minded innovators who share the vision of helping to transform the way companies conduct business in the global economy,” he said.

Hacera understands that every cloud vendor wants people using their blockchain service. Yet they also see that to move the technology forward, there need to be some standard ways of conducting business, and they want to provide that layer. Levi has a broader vision for the network beyond pure discoverability. He hopes eventually to provide the means to share data through the registry.

Powered by WPeMatico

A stablecoin is a cryptocurrency pegged 1-to-1 with another “stable” currency. In most cases, these coins are pegged to the US dollar and, as such, allow for true transfers of actual fiat currencies between parties using the blockchain. If you’re nodding off right now thinking about this, I would posit that these moves, however minor right now, are an important step forward in cryptocurrency acceptance.

The latest stablecoin to hit the virtual streets is the Gemini Dollar. This coin comes on the heels of the much-ridiculed Tether, a stablecoin created in 2014 that has been the the brunt of much criticism including suggestions that the team has been artificially pumping the currency with wash trades.

The new currency by Winklevoss-run Gemini is pegged directly to the US dollar on the Ethereum blockchain. This means that for every Gemini Dollar there is one actual dollar in a bank account. The Gemini Trust Company holds the deposits and has been officially accepted by the New York Department of Financial Services, the regulatory body associated with banking and finance.

The GD, in other words, is the first stablecoin to gain a truly official imprimatur.

“As the financial technology marketplace continues to evolve, New York is committed to fostering innovation while ensuring responsible growth. These approvals demonstrate that companies can create change and strong standards of compliance within a strong state regulatory framework that safeguards regulated entities and protects consumers,” said Department of Financial Services Superintendent Maria T. Vullo.

From the release:

DFS issued a limited purpose trust company charter to Gemini in October 2015 to operate a virtual currency exchange through which it offers customers services for buying, selling, sending, receiving, and storing virtual currency. DFS issued a limited purpose trust company charter in May 2015 to itBit, now Paxos Trust Company, which operates the itBit exchange, to offer services for buying, selling, sending, receiving, and storing virtual currency.

The NYDFS requires that the Gemini dollars “are fully exchangeable for a U.S. dollar” and that Gemini will maintain records of their movement. The requirements also include controls including AML and OFAC controls to present money laundering or terrorist financing. An independent accountant will examine the fiat-holding bank account to ensure that all of the stable coins are accounted for. You can convert and withdraw Gemini Dollars directly onto the Ethereum blockchain.

What all this means is that there is now a stable, regulated coin that should offset some of the traditional volatility of crypto. It’s an interesting – if limited – move by a big player in the crypto space.

Powered by WPeMatico

As cryptocurrencies emerge from the speculative bloodletting of the past months, believers in the promise of distributed ledger technologies for business and consumer applications are casting about for what comes next.

On our stage at Disrupt San Francisco we’ll be welcoming some of the leading thinkers in how distributed ledgers can create an entirely new architecture for computing and new processes for almost every conceivable transaction framework.

For Brian Behlendorf, the executive director of Hyperledger, distributed ledger technologies represent a powerful path for the future of networked computing — no matter the underlying technology. That’s why Behlendorf –through the Linux Foundation — is investing resources in ensuring that viable open source distributed ledger projects are supported and coming to market for any number of applications for businesses and consumers.

One of the leading lights of the internet revolution, Behlendorf’s career shaping the future of the networked world began in 1993 when he co-founded Organic Inc. — the first business dedicated to building commercial websites. Going on to become one of the foundational architects of the Apache http protocol, Behlendorf has served as the chief technology officer of the World Economic Forum and as an executive director for the technology investment fund, Mithril Capital.

Meanwhile, Parity Technologies is attempting to ensure that businesses don’t need to worry about the underlying technologies at all. Selling a suite of services that are all enabled by distributed ledger technologies and cryptographic computing, Jutta Steiner is giving businesses a way through the maze of competing protocols with a service that can enable the creation and adoption of distributed apps for businesses.

“We see it as a way for people to build blockchains that fulfill their particular needs,” Steiner told our own Samantha Stein at our Blockchain event earlier this year in Zug. “One of the challenges we’re addressing in this is to come up with a scalable framework.”

Before Parity, Steiner was responsible for security and partner integration within the Ethereum Foundation when the public blockchain first launched in 2015. Steiner also co-founded Project Provenance — a London based start-up that employs blockchain technology to make supply chains more transparent.

Supply chains are at the heart of Tradeshift’s offerings — and the company is hoping that distributed ledgers will be too. That’s why the company created Tradeshift Frontiers, an innovation lab and incubator that will focus on transforming supply chains through emerging technologies, such as distributed ledgers, artificial intelligence and the Internet of Things.

“The use cases we’re working through Frontiers cover a very wide variety of themes, including supply chain financing, asset liquidity, and supply chain transparency,” said Gert Sylvest, co-founder and GM of Tradeshift Frontiers, at the time. “There is so much more potential than just cryptocurrencies.”

That potential will be one of the things that Sylvest, Steiner, and Behlendorf discuss. We’ll hope you’ll be in the audience to listen.

Disrupt SF will take place in San Francisco’s Moscone Center West from September 5 to 7. The full agenda is here, and you can still buy tickets right here.

Powered by WPeMatico

The blockchain is in the middle of a major hype cycle at the moment, and that makes it hard for many people to take it seriously, but if you look at the core digital ledger technology, there is tremendous potential to change the way we think about trust in business. Yet these are still extremely early days and there are a number of missing pieces that need to be in place for the blockchain to really take off in the enterprise.

Suffice it to say that it has caught the fancy of major enterprise vendors with the likes of SAP, IBM, Oracle, Microsoft and Amazon all looking at providing some level of Blockchain as a service for customers.

While the level of interest in blockchain remains fluid, a July 2017 survey of 400 large companies by UK firm Juniper Research found 6 in 10 respondents were “either actively considering, or are in the process of, deploying blockchain technology.”

In spite of the growing interest we have seen over the last 12-18 months, blockchain lacks some basic underlying system plumbing, the kind any platform needs to thrive in an enterprise setting. Granted, some companies and the open source community are recognizing this as an opportunity and trying to build it, but many challenges remain.

Even though the blockchain clearly has many possible use cases, some people still have trouble separating it from its digital currency roots, and Joshua McKenty, who helped develop Open Stack while working at NASA and now is head of Cloud Foundry at Pivotal, sees this as a real problem, one that could hold back the progress of blockchain as an enterprise technology.

He believes that right now bitcoin and blockchain are akin to Napster and peer to peer (P2P) technology in the late 90s. When Napster made it easy to share MP3 files illegally on a P2P network, McKenty believes, it set back business usage of P2P for a decade because of the bad connotations associated with the popular use case.

“You couldn’t talk about Napster [and P2P] and have it be a positive conversation. Bitcoin has done that to blockchain. It will take us time to recover what bitcoin has done to get to something that is really useful [with blockchain],” he said.

Photo by Spencer Platt/Newsmakers – Getty Images

A recent survey by Deloitte of over 1000 participants in 7 countries found that outside the US in particular this perception held true. “When asked if they believed that blockchain was just “a database for money” with little application outside of financial services, just 18 percent of US respondents agreed with that statement versus 61 percent of respondents in France and the United Kingdom,” the report stated.

Richie Etwaru, founder and CEO at Hu-manity and author of the book, Blockchain Trust Companies sees it as a matter of trust. Companies aren’t used to dealing from a position of trust. In fact, his book argues that the entire contract system exists because of a total lack of it.

“The hurdle [to widespread blockchain adoption in the enterprise] is that those who have traditionally designed or transformed business models in large enterprise settings have systematically and habitually treated trust and transparency as second, sometimes third level characteristics of a business model. The raw material needed are the willingness and executive level alignment and harmonization around the notion that trust and transparency are the next differentiators,” Etwaru explained.

Blockchain was originally created as a system to track bitcoin (digital currency) ownership, and it’s still used extensively for that purpose, but a trusted and immutable record has great utility to track virtually anything of value and enforce a set of rules. We have seen companies like po.et trying to use it to enforce content ownership, Hu-manity, which wants to enforce data ownership, and the IBM TrustChain consortium to track the provenance of diamonds from mine to store.

Photo: LeoWolfert/Getty Images

Rob May, who is CEO at Talla and whose company helped launch a blockchain called BotChain to track the authenticity of bots, says finding good use cases could help ultimately determine the technology’s success or failure. “Blockchain has a bunch of different use cases, and they are usually either all lumped together or poorly understood separately,” May said.

He believes that in many instances today, companies don’t understand the advantages of blockchain, which he identifies as immutability, trust and tokenization, the latter of which can help finance blockchain initiatives (but which can also contribute to confusion with digital currency use cases).

“Right now, businesses are missing real blockchain opportunities and instead throwing blockchain in places where it doesn’t belong. For example, they are trying to use it for smart contracts, and that stuff isn’t ready. They also try to use it for cases that require a lot of speed, and again blockchains aren’t ready,” he said.

Finally, he says, if you don’t require immutability, trust and tokenization, you might want to consider a different approach other than blockchain.

Like any network, identity will be at the core of any blockchain network because it is imperative that you understand whom you are communicating with. Charles Francis, a senior analyst at Accenture says for now blockchains will remain private for the most part, but authentication will become increasingly important as we eventually have blockchain-to-blockchain communications.

Photo: NicoElNino/Getty Images

“Initially blockchain-to-blockchain connections will be manually set up and you will manage your network in a private model and bad actors will be immediately obvious,” he explained. But he believes that we will require a system in place to ensure we are authentically who we say we are as we move beyond private networks.

Jerry Cuomo, IBM Fellow and VP of Blockchain says that there will come a time when there are multiple networks and we will need to set up systems for them to communicate. “There won’t be one blockchain network to rule them all. It’s a very safe bet. Once you make that statement, these systems need to work together,” he said. “All [the different pieces of networks] need identity and the identity better play across networks. My identity on one network better be the same on another network,” he explained.

For Etwaru it comes back to trust, and a trusted identity would be a natural extension of that. “Transformational blockchain use cases require a network of trading partners to start to operate in a more trusted and transparent way, not just one individual,” he said.

All this said, there is still a steady march toward adoption in the enterprise. As Talla’s May says, there may be open questions, but that just represents a big opportunity for smart companies. “If you are interacting with a network instead of a single company, whose throat do you choke when something goes wrong? I think you will see many companies in the blockchain space do what Red Hat did for Linux. Enterprises need consulting help and better frameworks to think about how [blockchain] networks will work, since Ethereum isn’t a product per se in the traditional sense,” he said.

Gil Perez, SVP for products and innovation, as well as head of digital customer initiatives at SAP says he’s seeing companies with real projects in production. “It is beyond just wanting to do something. We’re doing large scale implementations and pilots. For example, we did one in the pharmaceutical industry with over a billion transactions,” he said.

In fact, SAP has a total of 65 companies working on various projects at different stages of progress at the moment. Perez says the next level of adoption will require a way to involve multiple parties, not just a single company, as with a supply chain example, which involves moving goods and paperwork across multiple countries involving many individuals.

Photo: allanswart

He also points out the importance of making sure there is good data because ultimately, if you have bad data in an immutable record, that is going to be a serious problem. That requires the companies involved to come together and agree to a common system to enter and agree upon each piece of information that moves through the system and that is a work in progress.

May sees blockchain technology transforming the way we do business in the future and providing a more standard way of interacting than today’s hodgepodge of vendor approaches.

“Now that blockchain is here, what if we could launch a standard and have shared marketplace by all apps in a space? So as a developer, you write your [application] add-on one time and it works with any [similar application] that supports that standard, and they share one giant marketplace. But how do you get them to share a marketplace? Blockchain and tokens provide decentralization and incentives such that, if you set the right rules, maybe you could do it. That could be transformational,” he said.

As with any new technology, the more it scales the more the tools and adjacent technologies are required. We are still in the early stages of discovering what those are, and before the technology can take off in a big way, we will need more underlying infrastructure in place. If that happens, blockchain could be just as transformational as May suggests.

Powered by WPeMatico

What a day. Yesterday, hundreds of people gathered in Zug, Switzerland for TechCrunch Sessions: Blockchain. In addition to some of the key people of the Ethereum Foundation, the team interviewed the entrepreneurs behind Binance, Coinbase, ConsenSys, CryptoKitties and many other organizations.

The event was packed with interesting content. But if you couldn’t be there in person, don’t worry as you can watch everything that happened in Zug:

Disclosure: I own small amounts of various cryptocurrencies.

Powered by WPeMatico

SAP announced today at its Sapphire customer conference it was making the SAP Leonardo Blockchain service generally available. The latter is a cloud service to help companies build applications based on digital ledger-style technology.

Gil Perez, senior vice president for product and innovation and head of digital customer initiatives at SAP, says most of the customers he talks to are still very early in the proof of concept stage, but not so early that SAP doesn’t want to provide a service to help move them along the maturity curve.

“We are announcing the general availability of the SAP Cloud Platform Blockchain Services.” This is a generalized service on top of which customers can begin building their blockchain projects. He says SAP is taking an agnostic approach to the underlying ledger technology whether it’s the open source Hyperledger project, where SAP is a platinum sponsor, MultiChain or any additional blockchain or decentralized distributed ledger technologies.

Perez said part of the reason for this flexibility is that blockchain technology is really still being defined and SAP doesn’t want to commit to any underlying ledger approach until the market decides which way to go. He says this should allow them to minimize the impact on customers as the technology evolves.

They join other enterprise companies like Oracle, IBM, Microsoft and Amazon who have previously released blockchains services for their customers. For SAP, which many companies use for the back-office management of everything from finance to logistics, the blockchain could present some interesting use cases for its customers such as supply chain management.

In this case, the blockchain could help reduce paperwork, bring products to market more quickly and provide an easy audit trail. Instead of requesting a scanned copy of a signed document, you could simply click on a node on the blockchain and see the approval (or denial) and follow the products through the shipping process to the marketplace.

But Perez stresses that just because it’s early doesn’t mean they aren’t working on some pretty substantial projects. He cited one with a pharmaceutical company to ensure the provenance of drugs that involved over a billion transactions already.

SAP is simply trying to keep up with what customers want. Prior to the GA announced today, the company conducted a survey of 250 customers and found, that although it was early days, there is enterprise interest in exploring blockchain technology. Whether this initiative can expand into a broader business is hard to say, but SAP sees blockchain as logical adjacent technology to their core offerings.

Powered by WPeMatico

")

Excited to announce that this year’s The Europas Unconference & Awards is shaping up! Our half day Unconference kicks off on 3 July, 2018 at The Brewery in the heart of London’s “Tech City” area, followed by our startup awards dinner and fantastic party and celebration of European startups!

The event is run in partnership with TechCrunch, the official media partner. Attendees, nominees and winners will get deep discounts to TechCrunch Disrupt in Berlin, later this year.

The Europas Awards are based on voting by expert judges and the industry itself. But key to the daytime is all the speakers and invited guests. There’s no “off-limits speaker room” at The Europas, so attendees can mingle easily with VIPs and speakers.

What exactly is an Unconference? We’re dispensing with the lectures and going straight to the deep-dives, where you’ll get a front row seat with Europe’s leading investors, founders and thought leaders to discuss and debate the most urgent issues, challenges and opportunities. Up close and personal! And, crucially, a few feet away from handing over a business card. The Unconference is focused into zones including AI, Fintech, Mobility, Startups, Society, and Enterprise and Crypto / Blockchain.

We’ve confirmed 10 new speakers including:

Eileen Burbidge, Passion Capital

Carlos Eduardo Espinal, Seedcamp

Richard Muirhead, Fabric Ventures

Sitar Teli, Connect Ventures

Nancy Fechnay, Blockchain Technologist + Angel

George McDonaugh, KR1

Candice Lo, Blossom Capital

Scott Sage, Crane Venture Partners

Andrei Brasoveanu, Accel

Tina Baker, Jag Shaw Baker

We’d love for you to ask your friends to join us at The Europas – and we’ve got a special way to thank you for sharing.

Your friend will enjoy a 15% discount off the price of their ticket with your code, and you’ll get 15% off the price of YOUR ticket.

That’s right, we will refund you 15% off the cost of your ticket automatically when your friend purchases a Europas ticket.

So you can grab tickets here.

Public Voting is still humming along. Please remember to vote for your favourite startups!

Awards by category:

Hottest Media/Entertainment Startup

Hottest E-commerce/Retail Startup

Hottest Marketing/AdTech Startup

Hottest Enterprise, SaaS or B2B Startup

Hottest Platform Economy / Marketplace

Hottest Cyber Security Startup

Hottest Internet of Things Startup

Fastest Rising Startup Of The Year

Hottest GreenTech Startup of The Year

Best Angel/Seed Investor of the Year

Hottest VC Investor of the Year

Hottest Blockchain/Crypto Startup Founder(s)

Hottest Blockchain Protocol Project

Hottest Corporate Blockchain Project

Hottest Blockchain ICO (Europe)

Hottest Financial Crypto Project

Hottest Blockchain for Good Project

Hottest Blockchain Identity Project

Hall Of Fame Award – Awarded to a long-term player in Europe

The Europas Grand Prix Award (to be decided from winners)

The Awards celebrates the most forward thinking and innovative tech & blockchain startups across over some 30+ categories.

Startups can apply for an award or be nominated by anyone, including our judges. It is free to enter or be nominated.

Instead of thousands and thousands of people, think of a great summer event with 1,000 of the most interesting and useful people in the industry, including key investors and leading entrepreneurs.

• No secret VIP rooms, which means you get to interact with the Speakers

• Key Founders and investors speaking; featured attendees invited to just network

• Expert speeches, discussions, and Q&A directly from the main stage

• Intimate “breakout” sessions with key players on vertical topics

• The opportunity to meet almost everyone in those small groups, super-charging your networking

• Journalists from major tech titles, newspapers and business broadcasters

• A parallel Founders-only track geared towards fund-raising and hyper-networking

• A stunning awards dinner and party which honors both the hottest startups and the leading lights in the European startup scene

• All on one day to maximise your time in London. And it’s PROBABLY sunny!

That’s just the beginning. There’s more to come…

Interested in sponsoring the Europas or hosting a table at the awards? Or purchasing a table for 10 or 12 guest or a half table for 5 guests? Get in touch with:

Petra Johansson

Petra@theeuropas.com

Phone: +44 (0) 20 3239 9325

Powered by WPeMatico

Veridium Labs has been trying to solve a hard problem about how to trade carbon offset credits in an open market. The trouble is that more complex credits don’t have a simple value like a stock, and there hasn’t been a formula to determine their individual value. That has made accounting for them and selling them on open exchanges difficult or impossible. It’s a problem Veridium believes they can finally solve with tokens and the blockchain.

This week the company announced a partnership with IBM to sell carbon offset tokens on the Stellar blockchain. Each company has a role here with Veridium setting up the structure and determining the value formula. Stellar acts as the digital ledger for the transactions and IBM will handle the nuts and bolts of the trade activity of buying, selling and managing the tokens.

Todd Lemons, chairman at Veridium Labs, which is part of a larger environmental company called EnVision Corporation, says that even companies with the best of intentions have struggled with how to account for the complex carbon credits. There are simpler offset credits that are sold on exchanges, but ones that seek to measure the impact of a product through the entire supply chain are much more difficult to determine. As one example, how does a company making a candy bar source its cocoa and sugar. It’s not always easy to determine through a web of suppliers and sellers.

To partly solve this problem, another Envision company, InfiniteEARTH developed a way to account for them called the Redd+ forest carbon accounting methodology. It is widely accepted to the point that it has been incorporated in the Paris Climate Agreement, but it doesn’t provide a way to turn the credits into what are called fungible assets, that is an easily tradable one. The problem is the value of a given credit shifts according to the overall environmental impact of producing a good and getting it to market. That value can change according to the product.

Jared Klee, blockchain manager for token initiatives at IBM, says that buying and accounting for Redd+ credits on the company balance sheet has been a huge challenge for organizations. “It’s a major pain point. Today Redd+ credits are over the counter assets and there is no central exchange,” he said. That means they are essentially one-off transactions and the company is forced to hold these assets on the books with no easy way to account for their actual value. That often results in a big loss, he says, and companies are looking for ways to comply in a more cost-efficient way.

The three companies — Veridium, IBM and Stellar — have come together to solve this problem by creating a digital token that acts as a layer on top of the carbon credit to give it a value and make it easier to account for. In addition, the tokens can be bought and sold on the blockchain.

The blockchain provides all the usual advantages of a decentralized record keeping system, immutable records and encrypted transactions.

Veridium is working on the underlying formula for token valuation that measures “carbon density per dollar times product group,” Lemons explained. “That can be coded into a token and carried out automatically,” he added. They are working with various world bodies like the United Nations and The World Resource Institute to help figure out the values for each product group.

All of the details are still being worked out as the idea works its way through the various regulatory bodies, but the companies hope to be making the tokens available for sale some time later this year.

Ultimately this is about finding ways to help businesses comply with environmental initiatives and remove some of the complexity inherent in that process today. “We hope the tokens will provide less friction and a much higher adoption rate,” Lemons said.

Powered by WPeMatico

As old-school industries like oil and gas increasingly network entities like oil platforms, they become more vulnerable to hacking attacks that were impossible when they were stand-alone. That requires a new approach to security and Xage (pronounced Zage), a security startup that launched last year thinks it has the answer with a concept called ‘fingerprinting’ combined with the blockchain.

“Each individual fingerprint tries to reflect as much information as possible about a device or controller,” Duncan Greatwood, Xage’s CEO explained. They do this by storing configuration data from each device and controller on the network. That includes the hardware type, the software that’s installed on it, the CPU ID, the storage ID and so forth.

If someone were to try to inject malware into one of these controllers, the fingerprint identification would notice a change and shut it down until human technicians could figure out if it’s a legitimate change or not.

You may be wondering where the blockchain comes into this, but imagine a honey pot of these fingerprints were stored in a conventional database. If that database were compromised, it would mean hackers could have access to a company’s entire store of fingerprints, completely neutering that idea. That’s where the blockchain comes in.

Greatwood says it serves multiple purposes to prevent such a scenario from happening. For starters, it takes away that centralized honey pot. It also provides a means of authentication making it impossible to insert a fake fingerprint without explicit permission to do so.

But he says that Xage takes one more precaution unrelated to the blockchain to allow for legitimate updates to the controller. “We have a digital replica (twin) of the system we keep in the cloud, so if someone is changing the software or plans to change it on a device or controller, we will pre-calculate what the new fingerprint will be before we update the controller,” he said. That will allow them to understand when there is a sanctioned update happening and not an external threat agent trying to mimic one.

In this way they check the validity of every fingerprint and have checks and balances every step of the way. If the updated fingerprint matches the cloud replica, they can be reasonably assured that it’s authentic. If it doesn’t, he says they assume the fingerprint might have been hacked and shut it down for further investigation by the customer.

While this sounds like a complex way of protecting this infrastructure, Greatwood points out that these devices and controllers tend to be fairly simple in terms of their configuration, not like the complexities involved in managing security on a network of workstations with many possible access points for hackers.

The irony here is that these companies are networking their devices to simplify maintenance, but in doing so they have created a new set of issues. “It’s a very interesting problem. They are adopting IoT, so they don’t have to do [so many] truck rolls. They want that network capability, but then the risk of hacking is greater because it only takes one hack to get access to thousands of controllers,” he explained.

In case you are thinking they may be overstating the actual problem of oil rigs and other industrial targets getting hacked, a Department of Homeland Security report released in March suggests that the energy sector has been an area of interest for nation-state hackers in recent years.

Powered by WPeMatico

Increasingly we are going to be having bots conducting business on a company’s behalf. As that happens, it is going to require a trust mechanism to ensure that bot-to-bot communication is legitimate. BotChain, a new startup out of Boston wants to be the blockchain for registering bots.

The new blockchain, which is built on Ethereum, is designed to register and identify bots and provide a way for companies to collaborate between bots with auditing capabilities built in. BotChain has the potential to become a standard way of sharing data between bots in a trusted way.

The idea is to have an official and sanctioned place for companies to register their bots securely. As the organization describes it, “BotChain offers bot developers, enterprises, software companies, and system integrators the critical systems, standards, and means to validate, certify, and manage the millions of bots and billions of transactions powered by AI.

Photo: allanswart

The company was created by the team at Talla, a bot startup in Cambridge, but the goal is to open this up to much larger community of partners and expand. In fact, early partners include Gupshup, a platform for developers and Howdy.ai, B2B enterprise bot developers along with Polly, CareerLark, Disco (formerly Growbot), Zoom.ai, and Botkeeper.

BotChain is the brainchild of Rob May, who is CEO at Talla. He was formerly co-founder and CEO at Backupify, which was sold to Datto in 2014. He recognized that as bot usage increases, there needed to be a system in place to help companies using bots to exchange information, and eventually even digital currencies to complete transactions in a fully digital context.

May believes that blockchain is the best solution to build this trust mechanism because of the ledger’s nature as an immutable and irrefutable record. If the entities on the blockchain agree to work with one another, and the other members allow it, there should be an element of confidence inherent in that.

He points to other advantages such as being decentralized so that no single company can control the data on the blockchain, and of course nobody can erase a record once it’s been written to the chain. It also provides a way for bots to identify one another in an official way and for participating companies to track transactions between bots.

Talla opened this up to a community of users because it wants BotChain to be a standard way for bots to exchange information. Whether that happens or not remains to be seen, but these types of projects could be important building blocks as companies look for ways to conduct business confidently, even when there are no humans involved.

BotChain has raised $5 million USD in a private token sale to institutional investors such as Galaxy Digital, Pillar, Glasswing and Avalon, according to the company.

In addition, they will be conducting another token pre-sale starting this Friday to raise additional funds from community stakeholders. “This token sale is a way to give [our community] access. Purchasing these tokens allows users to start registering their assets and create chains of immutable records of what their machines have done,” May explained. He said the company expects to sell about $20 million worth of tokens this year.

You can learn more about Botchain from this video:

Powered by WPeMatico