digital banking

Auto Added by WPeMatico

Auto Added by WPeMatico

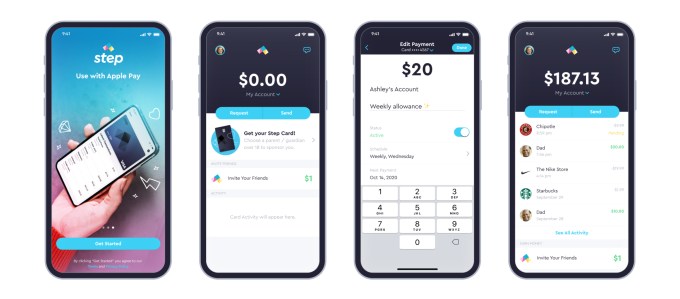

Step, the digital banking service aimed at teens and endorsed by TikTok star Charli D’Amelio, announced this morning the close of a $100 million round of Series C funding after growing to more than 1.5 million users just six months after launch. The new round, led by General Catalyst, comes shortly after Step’s $50 million Series B, announced at the end of last year after the startup hit half a million users in only two months post-launch.

The new round also includes participation from Step’s existing investors, Coatue, Stripe, Charli D’Amelio, The Chainsmokers, Will Smith and Jeffrey Katzenberg, and brings on newcomer Franklin Templeton, signaling a plan to move into investments is on the horizon. It also includes actor and musician Jared Leto. Step is also formally announcing NBA All-Star Stephen Curry as an investor, which had not previously been disclosed, as well as former Square executives Sarah Friar, Jacqueline Reses and Gokul Rajaram.

As a result of the fundraise, Kyle Doherty of General Catalyst is joining Step’s board. To date, Step has raised more than $175 million.

Image Credits: Step

According to CEO CJ MacDonald, Step hasn’t yet spent the money from its Series B, but believes the additional funds can help the startup grow more quickly.

“We’ve signed up more than a million and a half accounts in the first six months. We’re signing up 10,000 accounts-plus a day, and there’s just a lot of things that we want to do to bring this to millions and millions of households to help educate the next generation be smarter with money,” he says. At the time of the Series B, for comparison, Step said it was adding around 7,000 to 10,000 accounts per day.

“Honestly we don’t need the capital,” MacDonald added. “It’s just we think speed to market is really key and we think we can accelerate our growth and invest in infrastructure.”

The company is also planning to hire across operations, engineering, product and design, to double its now 65-person team over the next year.

Step today competes in a crowded market of mobile banking services aimed at a younger demographic, but it’s one of very few that targets teenagers ages 13 to 18. Through Step’s app, teens gain access to an FDIC-insured bank account without fees and a secured Visa card that helps them establish credit before they turn 18. The app also offers Venmo-like functionality for sending money to friends.

Image Credits: Step

Step’s growth so far has benefitted from a combination of factors, including word-of-mouth, use of social media and its popular referral program, which has paid out a few dollars per new sign-up. Step has also leveraged its partnerships with social media influencers like D’Amelio and Josh Richards, as well as celebs like Step investor Justin Timberlake.

The company believes the Curry announcement may also help to raise awareness about the banking app. As a father of three, if Curry talks about introducing Step to his own children, people will take notice.

While the additional funds are focused on driving growth, Step is also thinking about its future as its existing users begin to age up. The company plans to enter into the credit and lending market, as well as introduce investments at some point in the future. The Franklin Templeton investment could be useful here, MacDonald notes.

“Franklin [Templeton is] obviously, one of the largest financial institutions in the world. And, as we start thinking about investments and the journey of the customer, to have a great brand like Franklin Templeton that’s invested in this round — I think it’s just a testament to where they see the world going,” he says.

Step’s fundraise falls on the same day that competitor Current and Greenlight, both which focus on families, also raised new rounds.

Powered by WPeMatico

“Challenger” startups in banking and insurance have upended their industries, and picked up significant business, by building more customer-friendly tools and services — more personalized, easier to access and usually competitively priced — than those typically provided by their bigger, incumbent rivals. Now, a startup out of Romania that is building tools to help the incumbents respond with better services of their own is announcing a significant round of funding as its business grows.

FintechOS, which has built a low-code platform aimed at larger (older) banking and insurance companies to help them build new services and analytics on top of and around their existing infrastructure, has raised €51 million ($61.5 million at today’s rates, but $60 million at the time of the deal closing) in a Series B round of funding.

FintechOS’s opportunity has been to target the wave of incumbents in the insurance and banking industries that have been slowly watching as newer players like Lemonade (in insurance) and a huge plethora of challenger banks (Revolut, N26, Monzo and many others) are swooping in and picking up customers, especially among younger demographics, while they have been unable to respond mostly because their infrastructure is too old and big. Turning a huge ship around, as we have seen, is no small task — a situation that has become only more apparent in the last year of pandemic living and the big shift to digital interactions that resulted from it.

“When we launched FintechOS in 2017, we could already see existing solutions to digital transformation would struggle to deliver tangible results. By contrast, our unique approach has quickly inspired a sea-change in how financial institutions address digitization and engage with their customers,” said Teodor Blidarus, co-founder and CEO at FintechOS, in a statement. “Events over the last year have only increased pressure on our industry to evolve and as a result we’re seeing growing demand for our powerful platforms. Our latest round of funding will help us grow at the pace needed to improve outcomes for financial institutions and their customers globally.”

(It is not the only one. Others out of Europe in the space of bringing new tools to incumbent banks to help them make more modern and competitive products include 10x, Thought Machine, Temenos, Mambu and many more.)

The Series B round of funding is being led by Draper Esprit, with Earlybird, Gapminder Ventures, Launchub and OTB Ventures (which all participated in its Series A in December 2019) also participating. There are other backers in the round that are not being disclosed at this time, the startup added. FintechOS is also not disclosing its valuation. The company, based out of Bucharest, has raised just under $80 million to date.

FintechOS is active today in the U.K. and Europe — where it has been growing at a CAGR of 200% and says its services touch “millions” of people, with some of its key customers including the likes of banking giants Societe Generale and IdeaBank and international insurance brokers Howden. The plan will be to continue investing in those markets, as well as expanding internationally.

And it will be adding more services. Today, the banking platform is designed to help banks launch more retail services for consumers and small and medium business customers, and for insurance companies to build new health, life and general insurance products (there are a lot of synergies in how insurance and financial services companies have been built over the years, and so it’s a natural couplet when it comes to building tools for those industries).

In the financial sector, FintechOS lets banks build in new digital onboarding flows, credit cards and loan products, savings and mortgage products. Insurance products include new approaches to generating and handling quotes, customer onboarding and management and claims automation — which may well bring FintechOS into closer contact and collaboration with the most successful startup to come out of its home country to date, the RPA juggernaut UiPath. In all cases, it helps stitch together data from a bank’s own systems with more modern tooling, and to link that up with yet more modern tools to help process that data more easily.

This is “low code,” but it typically means that the company needs to work with third parties to enable all of this. Partners include the likes of integrators and other global services technicians, such as Microsoft, Deloitte, CapGemini, KPMG and so on. (And the founders of the startup themselves come from consulting backgrounds so they well understand the role these companies play in the process of bringing technology into big businesses.)

FintechOS is tapping into a couple of very big trends that have arguably been the biggest in the financial and related insurance industries.

The first of these is the fact that core services around things like credit/loans, current deposits and savings are not just very complex to build but actually have largely become commoditized — similar to digital payments — and so packaging them up and turning them into services that can be integrated by way of an API makes them more easily accessed without the heavy lifting needed to build them from scratch. This lets companies focus instead on customer service or building more interesting tools around those basic services to customise them (for example AI-based personalization). Disintermediating basic functions from the services built around them is arguably a bigger trend, but it has been especially prevalent in enterprise, which has long been a slow-moving space when it comes to innovation in the back-end, and the front-end.

The second of these is the big swing toward using no-code and low-code tools to empower more people within organizations to get stuck in when they can see something not working as efficiently as it could, and building the workflows themselves to improve that. This also applies to trying out and testing new products — again something that typically has not been done in financial and insurance services but can now be possible with low-code and no-code tools.

“Not only is our technology helping financial institutions become customer centric, but it’s also helping them provide products and services to more people and businesses,” said Sergiu Negut, the other co-founder who is FintechOS’s CFO and COO, in a separate statement. “With so many markets still underserved, the ability to tailor offerings to a segment of one offers the opportunity to increase financial inclusion and adheres to our ideal that easy access to financial services is essential. We’re delighted to be working with investors who share our views on how fintech should be transforming the financial services industry.”

Notably, Draper Esprit also has backed Thought Machine, another big player in the world of fintech that is taking some of the learnings and models that have helped new entrants disrupt incumbents, and is packaging them up as services for incumbents, too. It takes a different approach to doing this, not using low-code but smart contracts, which could be one reason why the VC doesn’t see the investments as conflict of interest. They are also tackling an enormous market, and so at least for now there is room for them, and many others in the space, such as 10x, Temenos, Mambu, Rapyd and many others.

“When we met Teo and Sergiu, we were immediately convinced of their vision: a data led, end-to-end platform, facilitated with a low-code/no-code infrastructure,” Vinoth Jayakumar, partner at Draper Esprit, said in a statement. “Incumbent financial services firms have cost-to-income ratios up to 90%, so we see a huge and increasing need for infrastructure software that allows digitisation at speed, ease and lower cost. Draper Esprit builds enduring partnerships; with the team at FintechOS we hope to build an enduring fintech company that will dramatically change financial services experiences for people all over the world.”

Powered by WPeMatico

Cora, a São Paulo-based technology-enabled lender to small and-medium-sized businesses, has raised $26.7 million in a Series A round led by Silicon Valley VC firm Ribbit Capital.

Kaszek Ventures, QED Investors and Greenoaks Capital also participated in the financing, which brings the startup’s total raised to $36.7 million since its 2019 inception. Kaszek led Cora’s $10 million seed round (believed at that time to be one of the largest seed investments in LatAm) in December 2019, with Ribbit then following.

Last year, Cora got its license approved from the Central Bank of Brazil, making it a 403 bank. The fintech then launched its product in October 2020 and has since grown to have about 60,000 customers and 110 employees.

Cora offers a variety of solutions, ranging from a digital checking account, Visa debit card and management tools such as an invoice manager and cashflow dashboard. With the checking account, customers have the ability to send and receive money, as well as pay bills, digitally.

This isn’t the first venture for Cora co-founders Igor Senra and Leo Mendes. The pair had worked together before — founding their first online payments company, MOIP, in 2005. That company sold to Germany’s WireCard in 2016 (with a 3 million-strong customer base), and after three years the founders were able to strike out again.

Cora co-founders Leo Mendes and Igor Senra; Image courtesy of Cora

With Cora, the pair’s long-term goal is to “provide everything that a SMB will need in a bank.”

Looking ahead, the pair has the ambitious goal of being “the fastest growing neobank focused on SMBs in the world.” It plans to use the new capital to add new features and improve existing ones; on operations; and launching a portfolio of credit products.

In particular, Cora wants to go even deeper in certain segments, such as B2B professional services such as law and accounting firms, real estate brokerages and education.

Ribbit Capital partner Nikolay Kostov believes that Cora has embarked on “an ambitious mission” to change how small businesses in Brazil are able to access and experience banking.

“While the consumer banking experience has undergone a massive transformation thanks to new digital experiences over the last decade, this is, sadly, still not the case on the small business side,” he said.

For example, Kostov points out, opening a traditional small business bank account in Brazil takes weeks, “reels of paper, and often comes with low limits, poor service and antiquated digital interfaces.”

Meanwhile, the number of new small businesses in the country continues to grow.

“The combination of these factors makes Brazil an especially attractive market for Cora to launch in and disrupt,” Kostov told TechCrunch. “The Cora founding team is uniquely qualified and deeply attuned to the challenges of small businesses in the country, having spent their entire careers building digital products to serve their needs.”

Since Ribbit’s start in 2012, he added, LatAm has been a core focus geography for the firm “given the magnitude of challenges, and opportunities in the region to reinvent financial services and serve customers better.”

Ribbit has invested in 15 companies in the region and continues to look for more to back.

“We fully expect that several fintech companies born in the region will become global champions that serve to inspire other entrepreneurs across the globe,” Kostov said.

Powered by WPeMatico

Amount, a new service that helps traditional banks compete in a digital world, has raised $81 million from none other than Goldman Sachs as it looks to help legacy fintech players compete with their more nimble digital counterparts.

The company, which spun out from the startup lending company Avant in January of this year, has already inked deals with Banco Popular, HSBC, Regions Bank and TD Bank to power their digital banking services and offer products like point-of-sale lending to compete with challenger banks like Chime and lenders like Affirm or Klarna.

“Most banks are looking for resources and infrastructure to accelerate their digital strategy and meet the demands of today’s consumer,” said Jade Mandel, a vice president in Goldman Sachs’ growth equity platform, GS Growth, who will be joining the board of directors at Amount, in a statement. “Amount enables banks to navigate digital transformation through its modular and mobile-first platform for financial products. We’re excited to partner with the team as they take on this compelling market opportunity.”

Complementing those customer-facing services is a deep expertise in fraud prevention on the back-end to help banks provide more loans with less risk than competitors, according to chief executive Adam Hughes.

It’s the combination of these three services that led Goldman to take point on a new $81 million investment in the company, with participation from previous investors August Capital, Invus Opportunities and Hanaco Ventures — giving Amount a post-money valuation of $681 million and bringing the company’s total capital raised in 2020 to a whopping $140 million.

Think of Amount as a white-labeled digital banking service provider for Luddite banks that hadn’t upgraded their services to keep pace with demands of a new generation of customers or the COVID-19 era of digital-first services for everything.

Banks pay a pretty penny for access to Amount’s services. On top of a percentage for any loans that a bank processes through Amount’s services, there’s an up-front implementation fee that typically averages at $1 million.

The hefty price tag is a sign of how concerned banks are about their digital challengers. Hughes said that they’ve seen a big uptick in adoption since the launch of their buy-now-pay-later product designed to compete with the fast growing startups like Affirm and Klarna .

Indeed, by offering banks these services, Amount gives Klarna and Affirm something to worry about. That’s because banks conceivably have a lower cost of capital than the startups and can offer better rates to borrowers. They also have the balance sheet capacity to approve more loans than either of the two upstart lenders.

“Amount has the wind at its back and the industry is taking notice,” said Nigel Morris, the co-founder of Capital One and an investor in Amount through the firm QED Investors. “The latest round brings Amount’s total capital raised in 2020 to nearly $140 million, which will provide for additional investments in platform research and development while accelerating the company’s go-to-market strategy. QED is thrilled to be a part of Amount’s story and we look forward to the company’s future success as it plays a vital role in the digitization of financial services.”

FT Partners served as advisor to Amount on this transaction.

Powered by WPeMatico