delaware

Auto Added by WPeMatico

Auto Added by WPeMatico

As an entrepreneur, you started your business to create value, both in what you deliver to your customers and what you build for yourself. You have a lot going on, but if building personal wealth matters to you, the assets you’re creating deserve your attention.

You can implement numerous advanced planning strategies to minimize capital gains tax, reduce future estate tax and increase asset protection from creditors and lawsuits. Capital gains tax can reduce your gains by up to 35%, and estate taxes can cost up to 50% on assets you leave to your heirs. Careful planning can minimize your exposure and actually save you millions.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle. Different strategies should be used at different times and for different reasons. The following are a few key considerations when determining what, if any, advanced strategies you might consider:

Some additional items to consider include issues related to qualified small business stock (QSBS), gift and estate taxes, state and local income taxes, liquidity, asset protection, and whether you and your family will retain control and manage the assets over time.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle.

Here are some advanced equity planning strategies that you can implement at different stages of your company life cycle to reduce tax and optimize wealth for you and your family.

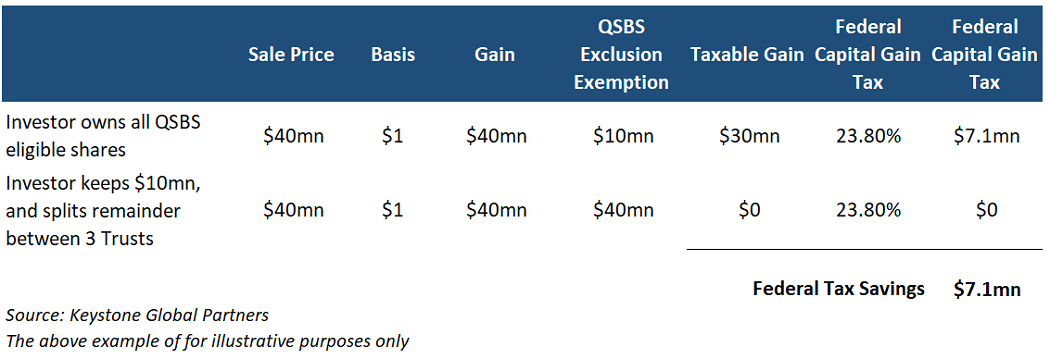

QSBS allows you to exclude tax on $10 million of capital gains (tax of up to 35%) upon an exit/sale. This is a benefit every individual and some trusts have. There is significant opportunity to multiply the QSBS tax exclusion well beyond $10 million.

The founder can gift QSBS eligible stock to an irrevocable nongrantor trust, let’s say for the benefit of a child, so that the trust will qualify for its own $10 million exclusion. The founder owning the shares would be the grantor in this case. Typically, these trusts are set up for children or unborn children. It is important to note that the founder/grantor will have to gift the shares to accomplish this, because gifted shares will retain the QSBS eligibility. If the shares are sold into the trust, the shares lose QSBS status.

Image Credits: Peyton Carr

In addition to the savings on federal taxes, founders may also save on state taxes. State tax can be avoided if the trust is structured properly and set up in a tax-exempt state like Delaware or Nevada. Otherwise, even if the trust is subject to state tax, some states, like New York, conform and follow the federal tax treatment of the QSBS rules, while others, like California, do not. For example, if you are a New York state resident, you will also avoid the 8.82% state tax, which amounts to another $2.6 million in tax savings if applied to the example above.

This brings the total tax savings to almost $10 million, which is material in the context of a $40 million gain. Notably, California does not conform, but California residents can still capture the state tax savings if their trust is structured properly and in a state like Delaware or Nevada.

Currently, each person has a limited lifetime gift tax exemption, and any gifted amount beyond this will generate up to a 40% gift tax that has to be paid. Because of this, there is a trade-off between gifting the shares early while the company valuation is low and using less of your gift tax exemption versus gifting the shares later and using more of the lifetime gift exemption.

The reason to wait is that it takes time, energy and money to set up these trusts, so ideally, you are using your lifetime gift exemption and trust creation costs to capture a benefit that will be realized. However, not every company has a successful exit, so it is sometimes better to wait until there is a certain degree of confidence that the benefit will be realized.

One way for the founder to plan for future generations while minimizing estate taxes and high state taxes is through a parent-seeded trust. This trust is created by the founder’s parents, with the founder as the beneficiary. Then the founder can sell the shares to this trust — it doesn’t involve the use of any lifetime gift exemption and eliminates any gift tax, but it also disqualifies the ability to claim QSBS.

The benefit is that all the future appreciation of the asset is transferred out of the founder’s and the parent’s estate and is not subject to potential estate taxes in the future. The trust can be located in a tax-exempt state such as Delaware or Nevada to also eliminate home state-level taxes. This can translate up to 10% in state-level tax savings. The trustee, an individual selected by the founder, can make distributions to the founder as a beneficiary if desired.

Further, this trust can be used for the benefit of multiple generations. Distributions can be made at the discretion of the trustee, and this skips the estate tax liability as assets are passed from generation to generation.

This strategy enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, specifically without using any lifetime gift exemption or being subject to gift tax. It’s particularly helpful when an individual has used up all their lifetime gift tax exemption. This is a powerful strategy for very large “unicorn” positions to reduce a founder’s future gift/estate tax exposure.

For the GRAT, the founder (grantor) transfers assets into the GRAT and gets back a stream of annuity payments. The IRS 7520 rate, currently very low, is a factor in calculating these annuity payments. If the assets transferred into the trust grow faster than the IRS 7520 rate, there will be an excess remainder amount in GRAT after all the annuity payments are paid back to the founder (grantor).

This remainder amount will be excluded from the founder’s estate and can transfer to beneficiaries or remain in the trust estate tax-free. Over time, this remainder amount can be multiples of the initial contributed value. If you have company stock that you expect will pop in value, it can be very beneficial to transfer those shares into a GRAT and have the pop occur inside the trust.

This way, you can transfer all the upside gift and estate tax-free out of your estate and to your beneficiaries. Additionally, because this trust is structured as a grantor trust, the founder can pay the taxes incurred by the trust, making the strategy even more powerful.

One thing to note is that the grantor must survive the GRAT’s term for the strategy to work. If the grantor dies before the end of the term, the strategy unravels and some or all the assets remain in his estate as if the strategy never existed.

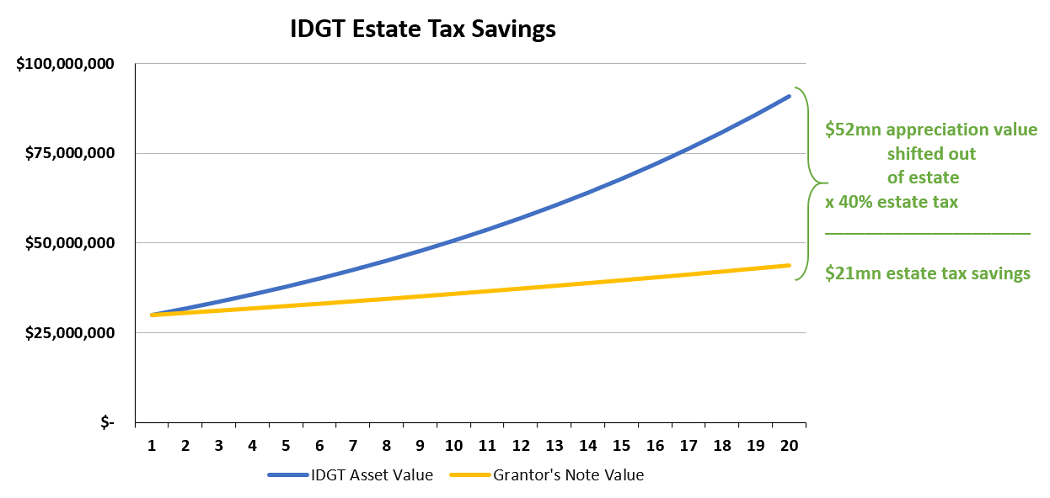

This is similar to the GRAT in that it also enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, but has some key differences. The grantor must “seed” the trust by gifting 10% of the asset value intended to be transferred, so this approach requires the use of some lifetime gift exemption or gift tax.

The remaining 90% of the value to be transferred is sold to the trust in exchange for a promissory note. This sale is not taxable for income tax or QSBS purposes. The main benefits are that instead of receiving annuity payments back, which requires larger payments, the grantor transfers assets into the trust and can receive an interest-only note. The payments received are far lower because it is interest-only (rather than an annuity).

Image Credits: Peyton Carr

Another key distinction is that the IDGT strategy has more flexibility than the GRAT and can be generation-skipping.

If the goal is to avoid generation-skipping transfer tax (GSTT), the IDGT is superior to the GRAT, because assets are measured for GSTT purposes when they are contributed to the trust prior to appreciation rather than being measured at the end of the term for a GRAT after the assets have appreciated.

Depending on a founder’s situation and goals, we may use some combination of the above strategies or others altogether. Many of these strategies are most effective when planning in advance; waiting until after the fact will limit the benefits you can extract.

When considering strategies for protecting wealth and minimizing taxes as it relates to your company stock, there’s a lot to take into account — the above is only a summary. We recommend you seek proper counsel and choose wealth transfer and tax savings strategies based on your unique situation and individual appetite for complexity.

Powered by WPeMatico

Facebook will soon be the latest tech giant to enter the world of cloud gaming. Their approach is different than what Microsoft or Google has built, but Facebook highlights a shared central challenge: dealing with Apple.

Facebook is not building a console gaming competitor to compete with Stadia or xCloud; instead, the focus is wholly on mobile games. Why cloud stream mobile games that your device is already capable of running locally? Facebook is aiming to get users into games more quickly and put less friction between a user seeing an advertisement for a game and actually playing it themselves. Users can quickly tap into the title without downloading anything, and if they eventually opt to download the title from a mobile app store, they’ll be able to pick up where they left off.

Facebook’s service will launch on the desktop web and Android, but not iOS due to what Facebook frames as usability restrictions outlined in Apple’s App Store terms and conditions.

With the new platform, users will be able to start playing mobile games directly from Facebook ads. Image via Facebook.

While Apple has suffered an onslaught of criticism in 2020 from developers of major apps like Spotify, Tinder and Fortnite for how much money they take as a cut from revenues of apps downloaded from the App Store, the plights of companies aiming to build cloud gaming platforms have been more nuanced and are tied to how those platforms are fundamentally allowed to operate on Apple devices.

Apple was initially slow to provide a path forward for cloud gaming apps from Google and Microsoft, which had previously been outlawed on the App Store. The iPhone maker recently updated its policies to allow these apps to exist, but in a more convoluted capacity than the platform makers had hoped, forcing them to first send users to the App Store before being able to cloud stream a gaming title on their platform.

For a user downloading a lengthy single-player console epic, the short pitstop is an inconvenience, but long-time Facebook gaming exec Jason Rubin says that the stipulations are a non-starter for what Facebook’s platform envisions, a way to start playing mobile games immediately without downloading anything.

“It’s a sequence of hurdles that altogether make a bad consumer experience,” Rubin tells TechCrunch.

Apple tells TechCrunch that they have continued to engage with Facebook on bringing its gaming efforts under its guidelines and that platforms can reach iOS by either submitting each individual game to the App Store for review or operating their service on Safari.

In terms of building the new platform onto the mobile web, Rubin says that without being able to point users of their iOS app to browser-based experiences, as current rules forbid, Facebook doesn’t see pushing its billions of users to accessing the service primarily from a browser as a reasonable alternative. In a Zoom call, Rubin demonstrates how this could operate on iOS, with users tapping an advertisement inside the app and being redirected to a game experience in mobile Safari.

“But if I click on that, I can’t go to the web. Apple says, ‘No, no, no, no, no, you can’t do that,’ ” Rubin tells us. “Apple may say that it’s a free and open web, but what you can actually build on that web is dictated by what they decide to put in their core functionality.”

Facebook VP of Play Jason Rubin. Image via Facebook.

Rubin, who co-founded the game development studio Naughty Dog in 1994 before it was acquired by Sony in 2001, has been at Facebook since he joined Oculus months after its 2014 acquisition was announced. Rubin had previously been tasked with managing the games ecosystem for its virtual reality headsets; this year he was put in charge of the company’s gaming initiatives across their core family of apps as the company’s VP of Play.

Rubin, well familiar with game developer/platform skirmishes, was quick to distinguish the bone Facebook had to pick with Apple and complaints from those like Epic Games, which sued Apple this summer.

“I do want to put a pin in the fact that we’re giving Google 30% [on Android]. The Apple issue is not about money,” Rubin tells TechCrunch. “We can talk about whether or not it’s fair that Google takes that 30%. But we would be willing to give Apple the 30% right now, if they would just let consumers have the opportunity to do what we’re offering here.”

Facebook is notably also taking a 30% cut of transaction within these games, even as Facebook’s executive team has taken its own shots at Apple’s steep revenue fee in the past, most recently criticizing how Apple’s App Store model was hurting small businesses during the pandemic. This saga eventually led to Apple announcing that it would withhold its cut through the end of the year for ticket sales of small businesses hosting online events.

Apple’s reticence to allow major gaming platforms a path toward independently serving up games to consumers underscores the significant portion of App Store revenues that could be eliminated by a consumer shift toward these cloud platforms. Apple earned around $50 billion from the App Store last year, CNBC estimates, and gaming has long been their most profitable vertical.

Though Facebook is framing this as an uphill battle against a major platform for the good of the gamer, this is hardly a battle between two underdogs. Facebook pulled in nearly $70 billion in ad revenues last year, and improving their offerings for mobile game studios could be a meaningful step toward increasing that number, something Apple’s App Store rules threaten.

For the time being, Facebook is keeping this launch pretty conservative. There are just 5-10 titles that are going to be available at launch, Rubin says. Facebook is rolling out access to the new service, which is free, this week across a handful of states in America, including California, Texas, Massachusetts, New York, New Jersey, Connecticut, Rhode Island, Delaware, Pennsylvania, Maryland, Washington, D.C., Virginia and West Virginia. The hodge-podge nature of the geographic rollout is owed to the technical limitations of cloud-gaming — people have to be close to data centers where the service has rolled out in order to have a usable experience. Facebook is aiming to scale to the rest of the U.S. in the coming months, they say.

Powered by WPeMatico

There comes a time for many startup companies where they either realize they need to do a nationwide rollout, or they need to actively target buyers in the middle of the country. If you are a startup on either the East or the West Coasts, it’s worth thinking about how this market might present its own set of unique challenges, and how you plan to overcome them.

There are a lot of misconceptions about what some people call “flyover country,” and as a San Francisco native who spent two decades in New York, Washington DC, and Boston before moving to Pittsburgh, I can assure you they are almost all wrong. Without getting into specifics, the reality of “middle America” is that it’s the same as anywhere else.

Income, education, world view, and waistlines are all varied. It’s pretty accurate that San Francisco possesses a culture obsessed with fitness and entrepreneurship, but California isn’t necessarily all like that, and if you think it is, I encourage you to go to Bakersfield, the Central Valley, or Eureka sometime.

In addition, just because the stereotypes are wrong doesn’t mean there’s nothing different about doing business here. As you think about how to conduct your rollout, here are some things you should consider:

As with any market, research is key since it informs every other aspect of the rollout. Start by looking into who your competition is.

Since there are fewer VC-backed startups in middle America, and smaller companies tend to get less press, the research may be harder. However, there are some major universities that are actively putting money into their own Entrepreneurship programs and those spinoffs often do very well.

Powered by WPeMatico

Today, Peloton is a bonafide success. The company, which sells $2,245 internet-connected exercise bikes, boasts a $4 billion valuation and a cult following.

That hasn’t always been the case. For years, Peloton battled for venture capital investment and struggled to attract buyers. Now that it’s proven the market for tech-enabled home exercise equipment and affiliated subscription products, a whole bunch of startups are chasing down the same customer segment.

Mirror, a New York-based company that sells $1,495 full-length mirrors that double as interactive home gyms, is closing in a round of funding expected to reach $36 million, sources and Delaware stock filings confirm, at a valuation just under $300 million. It’s unclear who has signed on to lead the round; we’ve heard a number of high-profile firms looked at Mirror’s books and passed. The company has previously raised a total of $38 million from Spark Capital, First Round Capital, Lerer Hippeau, BoxGroup and more.

Mirror declined to comment for this story.

Like Peloton, Mirror is sold for a hefty fee with a subscription to the service’s unlimited live and on-demand workouts that comes at an additional cost. The company hasn’t disclosed subscriber numbers, though The New York Times reported in February the business was selling $1 million worth of Mirrors — or some 650 units — per month.

The company has not only benefited from the Peloton effect, but also from a near-immediate interest from celebrities and influencers in its product. Kate Hudson, Alicia Keys, Reese Witherspoon, Jennifer Aniston and Gwyneth Paltrow are among the many celebrities to have publicly boasted about Mirror, undoubtedly boosting sales for the up-and-coming startup.

Venture capitalists were quick to show support for Mirror, too; in fact, the business attracted money at a $200 million valuation prior to launching its first product. Mirror began selling its sleek equipment, dubbed by The New York Times as “The Most Narcissistic Exercise Equipment Ever,” in September.

SAN FRANCISCO, CA – SEPTEMBER 06: Mirror Founder and CEO Brynn Putnam (L) and moderator Lucas Matney speak onstage during Day 2 of TechCrunch Disrupt SF 2018 at Moscone Center on September 6, 2018, in San Francisco, California. (Photo by Steve Jennings/Getty Images for TechCrunch)

The round comes amid a distinct boom in funding for fitness-related startups evidenced not only by Peloton’s mammoth valuation and hyped-over initial public offering expected soon but by the rapid uptick in small upstarts looking to capitalize on rising interest in fitness apps and equipment. In total, VCs bet some $2 billion on U.S. fitness startups in 2018, a record amount of funding for the space. So far this year, nearly $500 million has been allocated to the growing sector, per PitchBook, as entrepreneurs strive to bring the gym into the home.

Tonal, which sells personal exercise equipment that combines on-demand training with smart features, is among a small class of venture-backed fitness companies to have accumulated a large following. The company has raised $91.7 million in equity funding at a valuation of $185 million, according to PitchBook, from investors including L Catterton, Shasta Ventures, Mayfield and Sapphire Sport.

When it comes to early-stage efforts, there’s no shortage of recent fundraises. Last week, Livekick, which gives customers access to one-on-one personal training and yoga from their home, closed a $3 million seed round led by Firstime VC. Two weeks ago, fitness startup Future secured an $8.5 million round led by Kleiner Perkins’ Mamoon Hamid. For a $150 monthly fee, Future assigns personalized workout plans and a coach who tracks customers’ fitness activity through an Apple Watch. To keep users committed to their workout regimens, Future sends daily text messages with motivational feedback.

The AI-based personal training company Aaptiv, Plankk, which sells live fitness lessons led by Instagram stars, and audio coaching app Eastnine, have also recently launched.

Mirror was founded in late 2016 by Brynn Putnam, an entrepreneur behind Refine Method, a chain of boutique fitness studios located in New York. The former professional dancer spoke to TechCrunch’s Lucas Matney at Disrupt San Francisco in September about the future of the business.

“[We want] to enhance the human touch rather than to replace it,” Putnam said. “Our goal is not to be the next treadmill in your life, our goal is to be the next screen in your home,” Putnam said.

Ultimately, Putnam added, Mirror plans to scale beyond fitness content with potential extensions including physical therapy, fashion, beauty and education.

“We have the ability to create personalized premium content across a wide range of verticals, with fitness being our first vertical,” Putnam said.

Powered by WPeMatico

On January 12, 2016, Grindr announced it had sold a 60% controlling stake in the company to Beijing Kunlun Tech, a Chinese gaming firm, valuing the company at $155 million. Champagne bottles were surely popped at the small-ish firm.

Though not at a unicorn-level valuation, the 9-figure exit was still respectable and signaled a bright future for the gay hookup app. Indeed, two years later, Kunlun bought the rest of the firm at more than double the valuation and was planning a public offering for Grindr.

On March 27, 2019, it all fell apart. Kunlun was putting Grindr up for sale instead.

What went wrong? It wasn’t that Grindr’s business ground to a halt. By all accounts, its business seems to actually be growing. The problem was that Kunlun owning Grindr was viewed as a threat to national security. Consequently, CFIUS, or the Committee for Foreign Investment in the United States, stepped in to block the transaction.

So what changed? CFIUS was expanded by FIRRMA, or the Foreign Risk Review Modernization Act, in late 2018, which gave it massive new power and scale. Unlike before, FIRRMA gave CFIUS a technology focus. So now CFIUS isn’t just an American problem—it’s an American tech problem. And in the coming years, it will transform venture capital, Chinese involvement in US tech, and maybe even startups as we know it.

Here’s a closer look at how it all fits together.

Image via Getty Images / Busà Photography

CFIUS is the most important agency you’ve never heard of, and until recently it wasn’t even more than a committee. In essence, CFIUS has the ability to stop foreign entities, called “covered entities,” from acquiring companies when it could adversely affect national security—a “covered transaction.”

Once a filing is made, CFIUS investigates the transaction and both parties, which can take over a month in its first pass. From there, the company and CFIUS enter a negotiation to see if they can resolve any issues.

Powered by WPeMatico

TechCrunch’s Connie Loizos published some interesting stats on seed and Series A financings this week, courtesy of data collected by Wing Venture Capital. In short, seed is the new Series A and Series A is the new Series B. Sure, we’ve been saying that for a while, but Wing has some clean data to back up those claims.

Years ago, a Series A round was roughly $5 million and a startup at that stage wasn’t expected to be generating revenue just yet, something typically expected upon raising a Series B. Now, those rounds have swelled to $15 million, according to deal data from the top 21 VC firms. And VCs are expecting the startups to be making money off their customers.

“Again, for the old gangsters of the industry, that’s a big shift from 2010, when just 15 percent of seed-stage companies that raised Series A rounds were already making some money,” Connie writes.

As for seed, in 2018, the average startup raised a total of $5.6 million prior to raising a Series A, up from $1.3 million in 2010.

Now on to IPO updates, then a closer look at all the companies raising big rounds. Want more TechCrunch newsletters? Sign up here. Contact me at kate.clark@techcrunch.com or @KateClarkTweets.

![]()

Slack: The workplace communication software provider dropped its S-1 on Friday ahead of a direct listing. That’s when companies sell existing shares directly to the market, allowing them to skip the roadshow and minimize the astronomical fees typically associated with an initial public offering. Here’s the TLDR on financials: Slack reported revenues of $400.6 million in the fiscal year ending January 31, 2019, on losses of $138.9 million. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before. Slack’s losses are shrinking (slowly), while its revenues expand (quickly). It’s not profitable yet, but is that surprising?

Zoom was the Slack we thought Slack was all along.

— alex (PVD) (@alex) April 26, 2019

Uber: The ride-hail giant is fast approaching its IPO, expected as soon as next week. On Friday, the company established an IPO price range of $44 to $50 per share to raise between $7.9 billion and $9 billion at a valuation of approximately $84 billion, significantly lower than the $100 billion previously reported estimations. The most likely outcome is Uber will price above range and all the latest estimates will be way off course. Best to sit back and see how Uber plays it. Oh, and PayPal said it would make a $500 million investment in the company in a private placement, as part of an extension of the partnership between the two.

There are a lot of fascinating companies raising colossal rounds, so I thought I’d dive a bit deeper than I normally do. Bear with me.

Carbon: The poster child for 3D printing has authorized the sale of $300 million in Series E shares, according to a Delaware stock filing uncovered by PitchBook. If Carbon raises the full amount, it could reach a valuation of $2.5 billion. Using its proprietary Digital Light Synthesis technology, the business has brought 3D-printing technology to manufacturing, building high-tech sports equipment, a line of custom sneakers for Adidas and more. It was valued at $1.7 billion by venture capitalists with a $200 million Series D in 2018.

Canoo: The electric vehicle startup formerly known as Evelozcity is on the hunt for $200 million in new capital. Backed by a clutch of private individuals and family offices from China, Germany and Taiwan, the company is hoping to line up the new capital from some more recognizable names as it finalizes supply deals with vendors, according to reporting from TechCrunch’s Jonathan Shieber. The company intends to make its vehicles available through a subscription-based model and currently has 400 employees. Canoo was founded in 2017 after Stefan Krause, a former executive at BMW and Deutsche Bank, and another former BMW executive, Ulrich Kranz, exited Faraday Future amid that company’s struggles.

Starry: The Boston-based wireless broadband internet startup has authorized the sale of Series D shares worth up to $125 million, according to a Delaware stock filing. If Starry closes the full authorized raise it will hold a post-money valuation of $870 million. A spokesperson for the company confirmed it had already raised new capital, but disputed the numbers. The company has already raised more than $160 million from investors, including FirstMark Capital and IAC. The company most recently closed a $100 million Series C this past July.

Selina & Sonder: The Airbnb competitor Sonder is in the process of closing a financing worth roughly $200 million at a $1 billion valuation, reports The Wall Street Journal. Investors including Greylock Partners, Spark Capital and Structure Capital are likely to participate. Sonder is four years old but didn’t emerge from stealth until 2018. The startup, which turns homes into hotels, quickly attracted more than $100 million in venture funding. Meanwhile, another hospitality business called Selina has raised $100 million at an $850 million valuation. The company, backed by Access Industries, Grupo Wiese and Colony Latam Partners, builds living/co-working/activity spaces across the world for digital nomads.

Fresh funds: Mary Meeker has made history with the close of her new fund, Bond Capital, the largest VC fund founded and led by a female investor to date. Bond has $1.25 billion in committed capital. If you remember, Meeker ditched Kleiner Perkins last fall and brought the firm’s entire growth team with her. Kleiner said it was a peaceful split that would allow the firm to focus more on its early-stage efforts, leaving the growth investing to Bond. Fortune, however, reported this week that a power struggle of sorts between Meeker and Mamoon Hamid, who joined recently to reenergize the early-stage side of things, was a larger cause of her exit.

Plus, SOSV, a multi-stage venture firm that was founded as the personal investment vehicle of entrepreneur Sean O’Sullivan after his company went public in 1994, has raised $218 million for its third fund. The vehicle has a $250 million target that SOSV expects to meet. Already, the fund is substantially larger than the firm’s previous vehicle, which closed with $150 million.

A grocery delivery startup crumbles: Honestbee, the online grocery delivery service in Asia, is nearly out of money and trying to offload its business. Despite looking impressive from the outside, the company is currently in crisis mode due to a cash crunch — there’s a lot happening right now. TechCrunch’s Jon Russell dives in deep here.

Extra Crunch: “When it comes to working with journalists, so many people are, frankly, idiots. I have seen reporters yank stories because founders are assholes, play unfairly, or have PR firms that use ridiculous pressure tactics when they have already committed to a story.” Sign up for Extra Crunch for a full list of PR don’ts. Here are some other EC pieces to hit the wire this week:

Equity: If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Kleiner Perkins, Chinese IPOs and Slack & Uber’s upcoming exits.

Powered by WPeMatico

The RealReal, an online retailer for authenticated luxury consignment, has authorized the sale of up to $70 million in new shares, per a Delaware stock authorization filing discovered by the Prime Unicorn Index. If the company raises the entire amount, it would reach a valuation of $1.06 billion, cementing its status as the newest e-commerce unicorn.

The filing doesn’t guarantee The RealReal will sell the full amount of authorized shares. The company declined to comment on its fundraising plans.

The RealReal is led by founder and chief executive officer Julie Wainwright (pictured), the former CEO of Pets.com, a company now synonymous with the dot-com bust. It has raised quite a bit of capital to date — a total of $288 million from venture capital and private equity backers, including Great Hill Partners, Sandbridge Capital, PWP Growth Equity, Industry Ventures, Greycroft Partners and Canaan Partners. Most recently, The RealReal closed a Series G financing of $115 million in July 2018 that valued the business at $745 million, per PitchBook.

The RealReal has recently expanded its brick-and-mortar footprint and added additional e-commerce fulfillment centers as demand increased for its supply of second-hand luxury items. Founded in 2011, the company operates eight luxury consignment offices, where customers can receive free valuations of their luxury items. The RealReal is headquartered in San Francisco.

In a conversation with TechCrunch in 2017, Wainwright confirmed the company’s intent to go public at some point. With this upcoming round, The RealReal would be well placed for a 2020 initial public offering.

“That’s the goal,” Wainwright said during the interview. “We really aren’t in the mood to sell the business, we’re in the mood to go public at some point in the future.”

The RealReal competes with fellow second-hand e-tailers ThredUp and Poshmark . The latter is gearing up for a fall IPO, according to The Wall Street Journal. The online marketplace has tapped Morgan Stanley and Goldman Sachs to lead its offering after closing in on $150 million in revenue in 2018. ThredUp, another major player in the fashion retail market, hasn’t raised capital since 2015, but did begin opening physical stores in 2017 as part of its greater effort to compete with fellow venture-backed second-hand e-tailers.

The RealReal would also be the latest in a series of high-profile female-founded companies to gain unicorn status. Glossier tripled its valuation to $1.2 billion with a $100 million round earlier this year, followed by Rent the Runway, which attracted a $125 million investment at a $1 billion valuation, to name a few.

Powered by WPeMatico