decentralization

Auto Added by WPeMatico

Auto Added by WPeMatico

I learned about Yat in April, when a friend sent our group chat a link to a story about how the key emoji sold as an “internet identity” for $425,000. “I hate the universe,” she texted.

Sure, the universe would be better if people with a spare $425,000 spent it on mutual aid or something, but minutes later, we were trying to figure out what this whole Yat thing was all about. And few more minutes later, I spent $5 (in U.S. dollars, not crypto) to buy

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

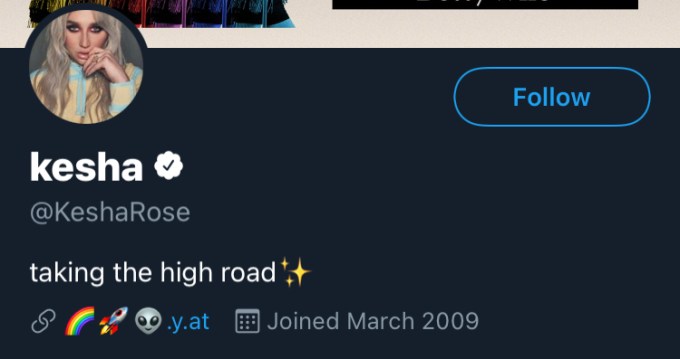

Kesha’s Yat URL on Twitter

On the surface, Yat is a platform that lets you buy a URL with emojis in it — even Kesha (y.at/

), Lil Wayne (y.at/

), Lil Wayne (y.at/ ), and Disclosure (y.at/

), and Disclosure (y.at/ ) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

This convenience, however, comes at a premium. Yat uses an algorithm to determine your Yat’s “rhythm score,” its metric for determining how to price your emoji combo based on its rarity. Yats with one or two emojis are so expensive that you have to contact the company directly to buy them, but you can easily find a four- or five-emoji identity that’ll only put you out $4.

Beyond that, CEO Naveen Jain — a Y Combinator alumnus, founder of digital marketing company Sparkart and angel investor — thinks that Yat is ultimately an internet privacy product. Jain wants people to be able to use their Yats in any way they’re able to use an online identity now, whether that’s to make payments, send messages, host a website or log in to a platform.

“Objectively, it’s a strange norm. You go on the internet, you register accounts with ad-supported platforms, and your username isn’t universal. You have many accounts, many usernames,” Jain said. “And you don’t control them. If an account wants to shut you down, they shut you down. How many stories are there of people trying to email some social network, and they don’t respond because they don’t have to?”

Image Credits: Yat (opens in a new window)

Yat doesn’t plan to fuel itself with ad money, since users pay for the product when they purchase their Yat, whether they get it for $4 or $400,000.

In the long run, Yat’s CEO says the company plans to use blockchain technology as a way to become self-sovereign. Yats would become assets issued on decentralized, distributed databases. Today, there are several projects working to create a decentralized alternative to the current domain name system (DNS), which is managed by internet regulatory authority ICANN. DNS is how you find things on the internet, but uses a centralized, hierarchical system. A blockchain domain name system would have no central authority, and some believe this could be the foundation of a next-gen web, or “Web 3.0.”

Today, words like “blockchain” and “cryptocurrency” don’t appear on the Yat website. Jain doesn’t think that’s compelling to average consumers — he believes in progressive decentralization, which explains why Yats are currently purchased with dollars, not ethereum.

“Something we think is really funny about the cryptocurrency world is that anyone who’s a part of it spends a lot of time talking about databases,” Jain said. “People don’t care about databases. When’s the last time you went to a website and it said ‘powered by MySQL’?”

Y.at, however, was registered at a traditional internet registrar, not on the blockchain.

“This is laying the foundation — there are certain elements of the vision that are certainly more of a social contract than actual implementation at this point in time,” says Jain. “But this is the vision that we’ve set forth, and we’re working continuously towards that goal.”

Still, until Yat becomes more decentralized, it can’t yet give users the complete control it aspires to. At present, the Terms & Conditions give Yat the authority to terminate or suspend users at its discretion, but the company claims it hasn’t yet booted anyone from the system.

“As Yat becomes more decentralized, our terms and conditions won’t be important,” Jain said. “This is the nature of pursuing a progressive decentralization strategy.”

In its “generation zero” phase (an open beta), Yat claims to have sold almost $20 million worth of emoji identities. Now, as the waitlist to get a Yat ends, Yat is posting some rare emoji identities on OpenSea, the NFT marketplace that recently reached a valuation of $1.5 billion.

A still image of a Yat visualizer creation

“For the first time ever, we’re going to be auctioning some Yats on OpenSea, and we’re going to be launching minting of Yats on Ethereum,” Jain said. Before minting Yats as NFTs, users can create a digital art landscape for their Yats through a Visualizer. These features, as well as new emojis in the Yat emoji set, will launch this evening at a virtual event called Yat Horizon.

“Yat Creators will now have more rights,” Jain said about the new ability to mint Yats as NFTs. “We are going to continue to pursue progressive decentralization until we achieve our ultimate goal: making Yat the best self-directed, self-sovereign identity system for all.”

Consumers have a demonstrated interest in retaining greater privacy on the internet — data shows that in iOS 14.5, 96% of users opted out of ad tracking. But the decentralization movement hasn’t yet been able to market its privacy advantages to the mainstream. Yat helps solve this problem because even if you don’t understand what blockchain means, you understand that having a personal string of emojis is pretty fun. But, before you spend $425,000 on a single-emoji username, keep in mind that Yat’s vision will only completely materialize with the advent of Web 3.0, and we don’t yet know when or if that will happen.

Powered by WPeMatico

While retail investors grew more comfortable buying cryptocurrencies like Bitcoin and Ethereum in 2021, the decentralized application world still has a lot of work to do when it comes to onboarding a mainstream user base.

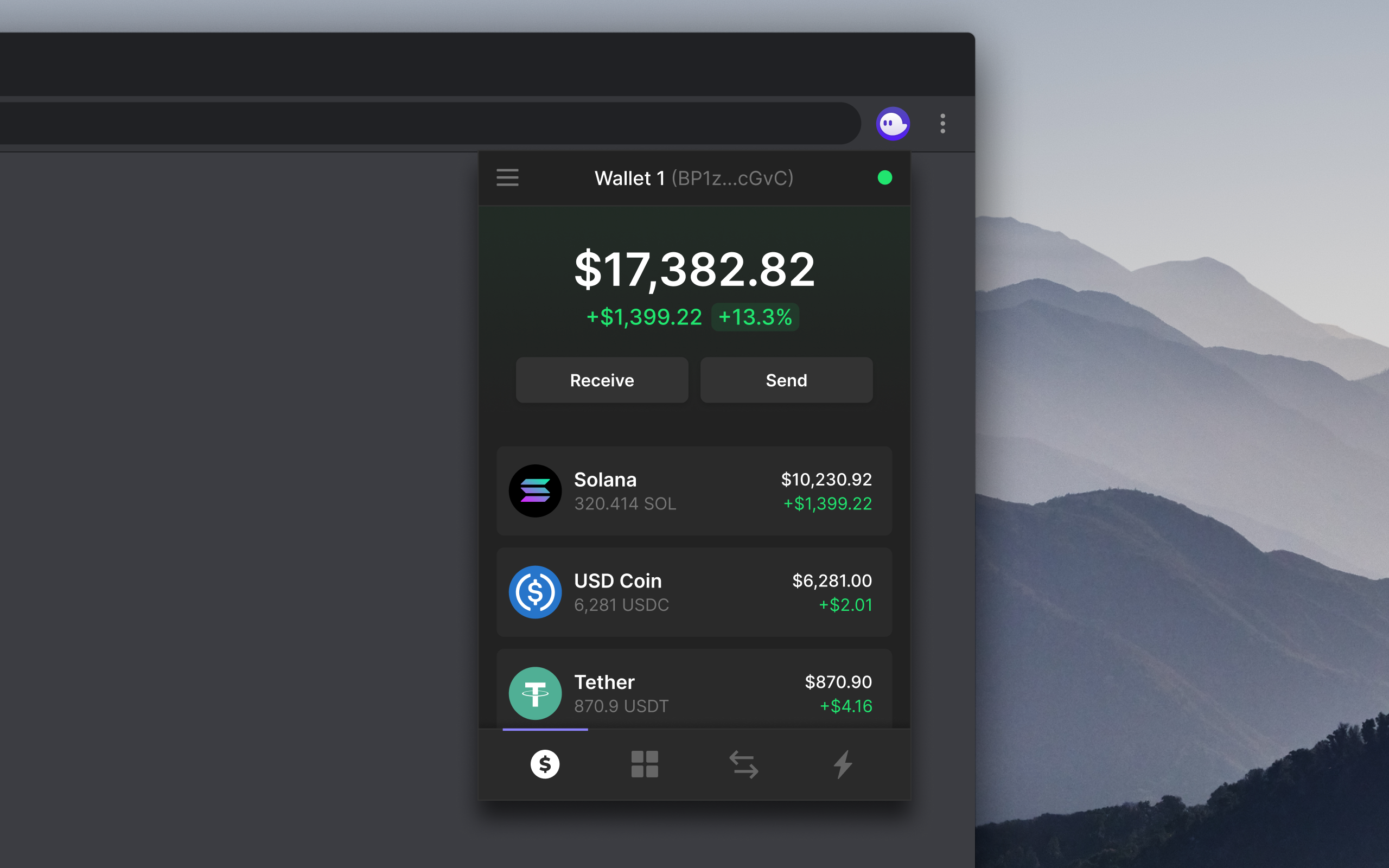

Phantom is part of a new class of crypto startups looking to build infrastructure that streamlines blockchain-based applications and provides a more user-friendly UX for navigating the crypto world, something that can make the entire space more approachable to a non-developer audience. Users can download the Phantom wallet to their browsers to interact with applications, swap tokens and collect NFTs.

The crypto wallet startup has banked a $9 million Series A round led by Andreessen Horowitz (a16z), with Variant Fund, Jump Capital, DeFi Alliance, Solana Foundation and Garry Tan also participating. The round, which closed earlier this summer, comes as some venture capital firms embrace a crypto future even as volatility continues to envelop the broader market. Last month, a16z announced a whopping 2.2 billion crypto fund, the firm’s largest vertical-specific investment vehicle ever.

Image via Phantom

The co-founding team of CEO Brandon Millman, CPO Chris Kalani and CTO Francesco Agosti all come aboard from crypto infrastructure startup 0x.

At the moment, Phantom is best-known among the Solana community, where it has become the go-to wallet for applications on that blockchain. The startup’s ambition is to interface with more and more networks, currently building out compatibility with Ethereum and looking to embrace other blockchains, aiming to be a product built for a “multichain world,” Millman tells TechCrunch.

Alongside building out support for other networks, Phantom wants to build more sophisticated DeFi mechanisms right into their wallet, allowing users to stake cryptocurrencies and swap more tokens inside the wallet.

The startup says they have some 40,000 users of their existing wallet product.

Building out a presence on the popular Ethereum blockchain, which already has a handful of popular wallet providers, will be a challenge, but Phantom’s broadest challenge is helping a new breed of crypto-curious users interface with a network of apps that still have a long way to go when it comes to being mainstream-friendly.

“The entire space is kind of stuck in this ‘built by developers for other developers mode,’ ” Millman says. “This bar has been kind of stuck there, and no one is really stepping up to push the bar up higher.”

Powered by WPeMatico

Mercuryo, a startup that has built a cross-border payments network, has raised $7.5 million in a Series A round of funding.

The London-based company describes itself as “a crypto infrastructure company” that aims to make blockchain useful for businesses via its “digital asset payment gateway.” Specifically, it aggregates various payment solutions and provides fiat and crypto payments and payouts for businesses.

Put more simply, Mercuryo aims to use cryptocurrencies as a tool for putting in motion next-gen, cross-border transfers or, as it puts it, “to allow any business to become a fintech company without the need to keep up with its complications.”

“The need for fast and efficient international payments, especially for businesses, is as relevant as ever,” said Petr Kozyakov, Mercuryo’s co-founder and CEO. While there is no shortage of companies enabling cross-border payments, the startup’s emphasis on crypto is a differentiator.

“Our team has a clear plan on making crypto universally available by enabling cheap and straightforward transactions,” Kozyakov said. “Cryptocurrency assets can then be used to process global money transfers, mass payouts and facilitate acquiring services, among other things.”

Image Credits: Left to right: Alexander Vasiliev, Greg Waisman, Petr Kozyakov / MercuryO

Mercuryo began onboarding customers at the beginning of 2019, and has seen impressive growth since with annual recurring revenue (ARR) in April surpassing over $50 million. Its customer base is approaching 1 million, and the company has partnerships with a number of large crypto players including Binance, Bitfinex, Trezor, Trust Wallet, Bithumb and Bybit. In 2020, the company said its turnover spiked by 50 times while run-rate turnover crossed $2.5 billion in April 2021.

To build on that momentum, Mercuryo has begun expanding to new markets, including the United States, where it launched its crypto payments offering for B2B customers in all states earlier this year. It also plans to “gradually” expand to Africa, South America and Southeast Asia.

Target Global led Mercuryo’s Series A, which also included participation from a group of angel investors and brings the startup’s total raised since its 2018 inception to over $10 million.

The company plans to use its new capital to launch a cryptocurrency debit card (spending globally directly from the crypto balance in the wallet) and continuing to expand to new markets, such as Latin America and Asia-Pacific.

Mercuryo’s various products include a multicurrency wallet with a built-in crypto exchange and digital asset purchasing functionality, a widget and high-volume cryptocurrency acquiring and OTC services.

Kozyakov says the company doesn’t charge for currency conversion and has no other “hidden fees.”

“We enable instant and easy cross-border transactions for our partners and their customers,” he said. “Also, the money transfer services lack intermediaries and require no additional steps to finalize transactions. Instead, the process narrows down to only two operations: a fiat-to-crypto exchange when sending a transfer and a crypto-to-fiat conversion when receiving funds.”

Mercuryo also offers crypto SaaS products, giving customers a way to buy crypto via their fiat accounts while delegating digital asset management to the company.

“Whether it be virtual accounts or third-party customer wallets, the company handles most cryptocurrency-related processes for banks, so they can focus more on their core operations,” Kozyakov said.

Mike Lobanov, Target Global’s co-founder, said that as an experiment, his firm tested numerous solutions to buy Bitcoin.

“Doing our diligence, we measured ‘time to crypto’ – how long it takes from going to the App Store and downloading the app until the digital assets arrive in the wallet,” he said.

Mercuryo came first with 6 minutes, including everything from KYC and funding to getting the cryptocurrency, according to Lobanov.

“The second-best result was 20 minutes, while some apps took forever to process our transaction,” he added. “This company is a game-changer in the field, and we are delighted to have been their supporters since the early days.”

Looking ahead, the startup plans to release a product that will give businesses a way to send instant mass payments to multiple customers and gig workers simultaneously, no matter where the receiver is located.

Powered by WPeMatico

Even as NFT sales dip below their most speculative highs, startups aiming to tap into their potential are still scoring big funding rounds from investors who believe there’s much more to crypto collectibles than the past few months of hype.

Mythical Games, an NFT games startup based out of Los Angeles, has banked a $75 million raise from new and existing investors betting on the startup’s aim to expand the ambitions of their first title and locate a substantial platform opportunity amid helping developers build blockchain-based gaming experiences.

The round was led by WestCap. Existing investors were joined by 01 Advisors and Gary Vaynerchuk’s VaynerFund in the Series B funding. The startup has raised a whopping $120 million to date.

The company has been building a title called Blankos Block Party that seems to be Fall Guys meets Roblox meets Funko Pop. The PC game capitalizes on a number of big social gaming trends around user-created content, while adding in a marketplace where users can buy avatar figures and accessories crafted by a variety of artists and designers that Mythical has partnered with. Users can buy or sell the limited run or open edition items through their marketplace. Unlike some other NFT platforms, the goods live on a private blockchain so they can’t be re-sold on public marketplace platforms like OpenSea.

Mythical Games is part of a growing movement to bring blockchain-based game mechanics mainstream while leaving behind elements of crypto platforms that are seen as less ready for primetime. Users can purchase avatars on the platform with cryptocurrency through BitPay but they can also pay with a credit card. Users don’t need to walk through the mechanics of setting up a wallet or writing down a seed phrase either.

While the company has big hopes for Blankos as it onboards more users, the bigger investor opportunity is likely in the game engine that the team is building. The startup’s “Mythical Economic Engine” is being designed to help budding game builders create NFT-based marketplaces that won’t get them in any regulatory trouble, marrying compliance across geographies and tools that help creators comply with anti-money laundering laws and know-your-customer frameworks.

“With any new market like [NFTs], it goes through all these different cycles,” Mythical Games CEO John Linden tells TechCrunch. “We think this will actually change gaming for the long haul. The more we talk to game studios, we’re finding more and more potential use cases.”

Powered by WPeMatico

From the early success of Crypto Kitties to the explosive growth of NBA Top Shot, Dapper Labs has been at the forefront of the cryptocurrency collectible craze known as NFTs.

Now the company is reaping the benefits of its trailblazing status with a new $305 million financing led by some of the biggest names in Hollywood, sports and investing.

The new round values the company at a whopping $2.6 billion, according to multiple media reports, and comes at a time when NFTs have captured the popular imagination.

Leading the company’s financing was Coatue, the financial services firm that’s behind many of the biggest later-stage tech deals. But heavy hitters from the entertainment world also took their cut — these are folks like NBA legend Michael Jordan as well as current players and funds including Kevin Durant, Andre Iguodala, Kyle Lowry, Spencer Dinwiddie, Andre Drummond, Alex Caruso, Michael Carter-Williams, Josh Hart, Udonis Haslem, JaVale McGee, Khris Middleton, Domantas Sabonis, Klay Thompson, Nikola Vucevic and Thad Young and Richard Seymour’s 93 Ventures.

Entertainment and music heavyweights including Ashton Kutcher and Guy Oseary’s Sound Ventures, Will Smith and Keisuke Honda’s Dreamers VC, Shawn Mendes and Andrew Gertler’s AG Ventures, Shay Mitchell and 2 Chainz also bought in on the action.

And from the venture world comes other strategic investors like Andreessen Horowitz, The Chernin Group, USV, Version One and Venrock.

The company said it would use the funds to continue building out NBA Top Shot and expanding the updated digital trading card platform to other sports and a broader creator community.

Top Shot has already notched over $500 million in sales for its animated trading cards featuring things like LeBron James dunking, and the sky (at least for now) is seemingly the limit for the collectible applications of blockchain.

It’s like the one thing that cryptocurrency can do really well and it’s been embraced far beyond the world of sports collectibles. The recent $69 million sale of a digital piece of art at Christies also marks a watershed moment for the art world.

“NBA Top Shot is successful because it taps into basketball fandom — it’s a new and more exciting way for people to connect with their favorite teams and players,” said Roham Gharegozlou, CEO of Dapper Labs. “We want to bring the same magic to other sports leagues as well as help other entertainment studios and independent creators find their own approaches in exploring open platforms. NFTs unlock a new model for monetization that benefits the fans much more than advertising or sponsorships.”

Powering the Top Shot system and Dapper Labs’ other offerings is a new blockchain protocol called Flow, which purports to handle mainstream consumer applications at scale, and can support mass adoption.

Flow also allows for transactions using fiat currency and credit cards, and provides a much needed ease of cryptocurrency, and can keep customers safe from the fraud or theft common in cryptocurrency systems, according to a statement from Dapper Labs.

Flow enables NFT marketplaces and other decentralized applications that need to scale to handle mainstream demand without extremely high transaction costs (“gas fees”) or environmental concerns, the company said.

“NBA Top Shot is one of the best demonstrations we’ve seen of how quickly new technology can change the landscape for media and sports fans,” said Kevin Durant, co-founder of Thirty Five Ventures. “We’re excited to follow the progress with everything happening on Flow blockchain and use our platform with the Boardroom to connect with fans in a new way.”

Already companies like Warner Music Group, Ubisoft, Warner Media and the UFC, as well as thousands of third-party developers, artists and other creators, are using the Flow mainnet to sell collectible cards and develop custodial wallets.

Additional investors in the round include: MLB players like Tim Beckham and Nolan Arenado; NFL players Ken Crawley, Thomas Davis, Stefon Diggs, Dee Ford, Malcom Jenkins, Rodney McLeod, Jordan Matthew, Devin McCourty, Jason McCourty, DK Metcalf, Tyrod Taylor and Trent Williams; team ownership, including Vivek Ranadivé (Kings); and notable sports investors Bolt Ventures.

Powered by WPeMatico

Data protection and data privacy have gone from niche concerns to mainstream issues in the last several years, thanks to new regulations and a cascade of costly breaches that have laid bare the problems that arise when information and data security are treated haphazardly.

Yet that swing has also thrown up a whole series of issues for organisations and business functions that depend on sharing and exchanging data in order to work. Today, a startup that has built a new way of exchanging data while still keeping privacy in mind — starting first by applying the concept to the “marketing industrial complex” — is announcing a round of funding as it continues to pick up momentum.

InfoSum, a London startup that has built a way for organizations to share their data with each other without passing it on to each other — by way of a federated, decentralized architecture that uses mathematical representations to organise, “read” and query the data — is today announcing that it has raised $15.1 million.

Data may be the new oil, but according to founder and CEO Nick Halstead, that just means “it’s sticky and gets all over the place.” That is to say, InfoSum is looking for a new way to use data that is less messy, and less prone to leakage, and ultimately devaluation.

The Series A is being co-led by Upfront Ventures and IA Ventures. A number of strategics using InfoSum — Ascential, Akamai, Experian, British broadcaster ITV and AT&T’s Xandr — are also participating in the round. The startup has raised $23 million to date.

Nicholas Halstead, the founder and CEO who previously had founded and led another big data company, DataSift (the startup that gained early fame as a middleman for Twitter’s firehose of data, until Twitter called time on that relationship to push its own business strategy), said in an interview that the plan is to use the funding to continue fueling its growth, with a specific focus on the U.S. market.

To that end, Brian Lesser — the founder and former CEO of Xandr (AT&T’s adtech business that is now a part of AT&T’s WarnerMedia), and previous to that the North American CEO of GroupM — is joining the company as executive chairman. Lesser had originally led Xandr’s investment into InfoSum and had previously been on the board of the startup.

InfoSum got its start several years ago as CognitiveLogic, founded at a time when Halstead was first starting to get his head around the problems that were becoming increasingly urgent in how data was being used by companies, and how newer information architecture models using data warehousing and cloud computing could help solve that.

“I saw the opportunity for data collaboration in a more private way, helping enable companies to work together when it came to customer data,” he said. This eventually led to the company releasing its first product two years ago.

In the interim, and since then, that trend, he noted, has only gained momentum, spurred by the rise of companies like Snowflake that have disrupted the world of data warehousing, cookies have started to increasingly go out of style (and some believe will disappear altogether over time) and the concept of federated architecture has become much more ubiquitous, applied to identity management and other areas.

All of this means that InfoSum’s solution today may be aimed at martech, but it is something that affects a number of industries. Indeed, the decision to focus on marketing technology, he said, was partly because that is the industry that Halstead worked most closely with at DataSift, although the plan is to expand to other verticals as well.

“We’ve done a lot of work to change the marketing industrial complex,” said Lesser, “but its bigger use cases are in areas like finance and healthcare.”

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

The Intercontinental Exchange’s (ICE) cryptocurrency project Bakkt celebrated New Year’s Eve with the announcement of a $182.5 million equity round from a slew of notable institutional investors. ICE, the operator of several global exchanges, including the New York Stock Exchange, established Bakkt to build a trading platform that enables consumers and institutions to buy, sell, store and spend digital assets.

This is Bakkt’s first institutional funding round; it was not a token sale. Participating in the round are Horizons Ventures, Microsoft’s venture capital arm (M12), Pantera Capital, Naspers’ fintech arm (PayU), Protocol Ventures, Boston Consulting Group, CMT Digital, Eagle Seven, Galaxy Digital, Goldfinch Partners and more.

Bakkt is currently seeking regulatory approval to launch a one-day physically delivered Bitcoin futures contract along with physical warehousing. The startup initially planned for a November 2018 launch, but confirmed this morning an earlier CoinDesk report that it was delaying the launch to “early 2019” as it awaits permission from the Commodity Futures Trading Commission. Along with the funding, crypto news blog The Block Crypto also reports Bakkt has hired Balaji Devarasetty, a former vice president at Vantiv, as its head technology.

ICE’s crypto project was first announced in August and is led by chief executive officer Kelly Loeffler, ICE’s long-time chief communications and marketing officer. Bakkt quickly inked partnerships with Microsoft, which provides cloud infrastructure to the service, and Starbucks, to develop “practical, trusted and regulated applications for consumers to convert their digital assets into U.S. dollars for use at Starbucks,” Starbucks vice president of payments Maria Smith said in a statement at the time.

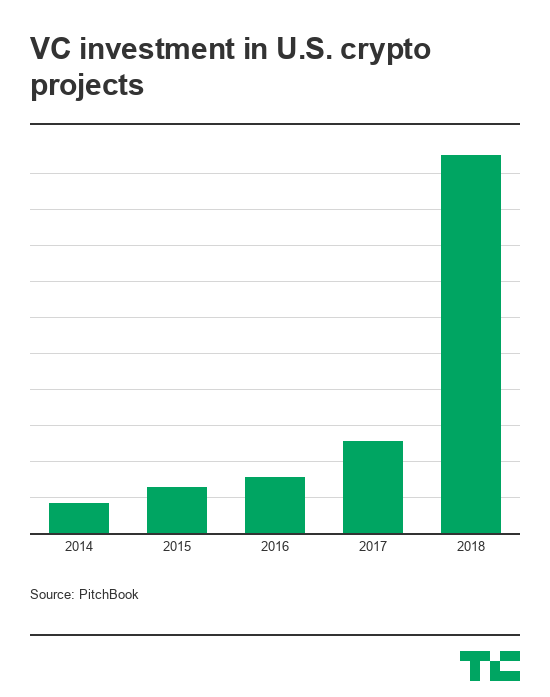

Many Bitcoin startups floundered in 2018, despite record amounts of venture capital invested in the industry. This was as a result of failed initial coin offerings, an inability to scale following periods of rapid growth and the falling price of Bitcoin. Still, VCs remained bullish on Bitcoin and blockchain technology in 2018, funneling a total of $2.2 billion in U.S.-based crypto projects — a nearly 4x increase year-over-year. Around the globe, investment hit a high of $4.6 billion — a more than 4x increase from last year, according to PitchBook.

“Notably, 2018 was the most active year for crypto in its brief ten-year history,” Loeffler wrote. “This was evidenced by rising investment in distributed ledger technology and digital assets, as well as by blockchain network metrics such as daily bitcoin transaction value and active addresses. Yet, these milestones tend to be overshadowed by the more narrow focus on bitcoin’s price, which has been seen by some, as a proxy for the potential of the technology.”

Today, the price of Bitcoin is hovering around $3,700 one year after a historic run valued the cryptocurrency at roughly $20,000. The crash caused many to dismiss Bitcoin and its underlying technology, while others remained committed to the tech and its potential for complete financial disruption. A project like Bakkt, created in-house at a respected financial institution with support from noteworthy businesses, is a logical bet for crypto and traditional private investors alike.

“The path to developing new markets is rarely linear: progress tends to modulate between innovation, dismissal, reinvention, and, finally, acceptance,” Loeffler added. “Each step, whether part of discovery or adversity, ultimately strengthens the product. Twenty years ago, it was controversial to suggest that commodities or bonds could trade electronically on a screen, and many steps were required for that evolution to play out.”

Powered by WPeMatico

Many doubted The Civil Media Company‘s ambitious plan to sell $8 million worth of its cryptocurrency, called CVL.

The skeptics, as it turns out, were right. Civil’s initial coin offering, meant to fund the company’s effort to create a new economy for journalism using the blockchain, failed to attract sufficient interest. The company announced today that it would provide refunds to all CVL token buyers by October 29.

Civil’s goal was to sell 34 million CVL tokens for between $8 million and $24 million. The sale began on September 18 and concluded yesterday. Ultimately, 1,012 buyers purchased $1,435,491 worth of CVL tokens. A spokesperson for Civil told TechCrunch an additional 1,738 buyers successfully registered for the sale, but never completed their transaction.

Civil isn’t giving up. The company says “a new, much simpler token sale is in the works,” details of which will be shared soon. Once those new tokens are distributed, Civil will launch three new features: a blockchain-publishing plugin for WordPress, a community governance application called The Civil Registry and a developer tool for non-blockchain developers to build apps on Civil.

ConsenSys, a blockchain venture studio that invested $5 million in Civil last fall, has agreed to purchase $3.5 million worth of those new tokens. The purchase is not an equity; all capital from the token sale is committed to the Civil Foundation, an independent nonprofit initially funded by Civil that funds grants to the newsrooms in Civil’s network.

In a blog post today, Civil chief executive officer Matthew Iles wrote that the token sale failure was a disappointment but not a shock. Days prior, he’d authored a separate post where he admitted things weren’t looking good.

“This isn’t how we saw this going,” Iles wrote. “The numbers will show clearly enough that we are not where we wanted to be at this point in the sale when we started out. But one thing we want to say at the top is that until the clock strikes midnight on Monday, we are still working nonstop on the goal of making our soft cap of $8 million.”

A recent Wall Street Journal report claimed Civil had reached out to The New York Times, The Washington Post, Dow Jones and Axios, among others, but failed to incite interest in its token.

Separate from its token sale, Civil has inked strategic partnerships with media companies like the Associated Press and Forbes, both of which confirmed to TechCrunch today that the failed token sale doesn’t impact their partnerships with Civil.

Forbes became the first major media brand to test Civil’s technology when it announced earlier this month that it would experiment with publishing content to the Civil platform. As for the AP, it granted the newsrooms in Civil’s network licenses to its content.

Civil, of course, isn’t the only blockchain startup targeting journalism. Nwzer, Userfeeds, Factmata and Po.et, which was founded by Jarrod Dicker, a former vice president at The Washington Post, are all trying their hand at bringing the new technology to the content industry.

Which, if any, will actually find success in the complicated space, is the question.

Powered by WPeMatico

SpankChain, a cryptocurrency aimed at decentralized sex cams, has announced that a hacker stole about $38,000 from their payment channel thanks to a broken smart contract. They wrote:

At 6pm PST Saturday, an unknown attacker drained 165.38 ETH (~$38,000) from our payment channel smart contract which also resulted in $4,000 worth of BOOTY on the contract becoming immobilized. Of the stolen/immobilized ETH/BOOTY, 34.99 ETH (~$8,000) and 1271.88 BOOTY belongs to users (~$9,300 total), and the rest belonged to SpankChain.

Our immediate priority has been to provide complete reimbursements to all users who lost funds. We are preparing an ETH airdrop to cover all $9,300 worth of ETH and BOOTY that belonged to users. Funds will be sent directly to users’ SpankPay accounts, and will be available as soon as we reboot Spank.Live.

The hacker used a ‘reentrancy’ bug in which the user calls the same transfer multiple times, draining a little Ethereum each time. The bug is the same one that previously affected the DAO.

The company pointed out that a security audit on their smart contract would have cost $50,000, a bit more than the amount lost. “As we move forward and grow, we will be stepping up our security practices, and making sure to get multiple internal audits for any smart contract code we publish, as well as at least one professional external audit,” they wrote.

I’ve reached out to the company for clarification but in short it seems the spanker has become the spankee.

Powered by WPeMatico