debit card

Auto Added by WPeMatico

Auto Added by WPeMatico

When Anik Khan graduated from college, his first job was working on credit cards and business expenses at Accenture. There, he found that someone could bring in a couple of thousand dollars just by having the right credit cards and following the rewards and promotions.

It was back in 2017 when he and David Gao got the idea for his company MaxRewards, a digital wallet app that manages credit cards and automatically activates benefits like rewards, cashback offers and monthly credits. It also makes recommendations at the point of purchase on which card would yield the best reward for that purchase.

Going after the some 83% of Americans that have a credit card, the app version was officially launched in 2019, and now the Atlanta-based company is announcing a $3 million seed round co-led by Dundee Venture Capital and Calano Ventures. Also backing the company are Techstars, Fintech Ventures Fund, Service Provider Capital and Fleetcor president Nick Izquierdo.

Tracking his own credit cards manually prior to MaxRewards, Khan recalled in one year, getting $16,000 in rewards. However, utilizing those benefits was time-consuming and difficult, because the rewards and savings aren’t always made evident by the credit card companies.

“Other companies have tried to do something similar, but the issue is you don’t have the reward information or the offers,” Khan told TechCrunch. “If you were to aggregate this information, you still would have to activate all of these things and use them before they expired.”

Users connect their accounts and when they make a purchase, their location is cross-referenced with the merchant and an algorithm is applied to tell the user which card to use. The average app user has six credit cards.

MaxRewards is free to download and use, and the majority of the app’s functionalities are free. Users who want additional features, like the auto activation or rewards, can join MaxRewards Gold and are given the opportunity to choose their own monthly price — the average is over $25 per month — based on the value they expect to gain, Khan said.

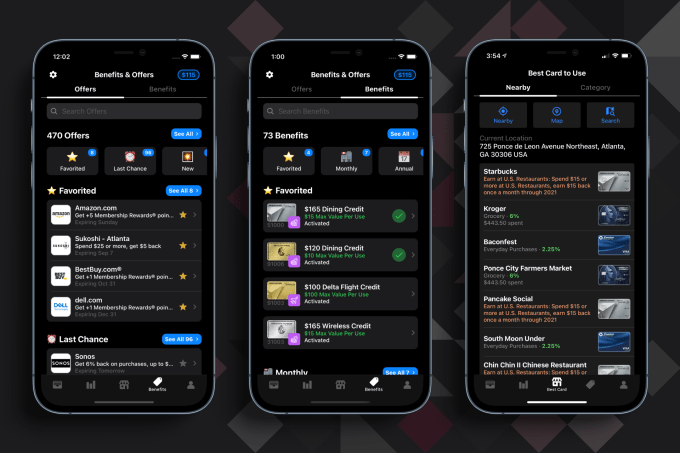

MaxRewards offers and benefits. Image Credits: MaxRewards

Ron Watson, partner at Dundee, said his firm invests in seed-stage companies between the coasts and is interested in consumer and e-commerce companies. Watson said he was impressed with what MaxRewards has been able to do with a team of three. He also relates to the company’s mission, having grown up in a lower, middle-class family that did not frequently go on vacations.

When he got his first job and was suddenly flying everywhere, he recalls building up so many rewards to the point where he was able to go on a vacation to Hawaii and only spend maybe $100, he said.

“I used to put my points into a spreadsheet, but as I got older and had kids, I realized how hard it was for the average person to do that and how important it is to have automation,” Watson said. “I downloaded the app, and on the first day, saved $20.”

The company is often compared to NerdWallet or Mint, but in terms of functionality, Khan said he feels MaxRewards is unique due to its credit card system connectors. Rather than rely on third-party aggregators to discover the rewards, MaxRewards leverages its own proprietary connectors to card systems.

There are hundreds of thousands of offers to be discovered, and consumers are asking for even more features, so Khan decided it was time to go after seed funding. He had raised a small seed, about $200,000, from his time at Techstars, but the new funding will enable him to add to his team of three people. He expects to be at 20 by the end of the year. Khan also wants to accelerate its user acquisition, product improvement and compliance.

Next up, the company is going to automate rewards and savings across additional platforms like debit cards, payment apps and cashback apps, as well as create browser extensions and a web app. Khan also wants to do more on the education side with regard to using credit cards in a smart manner.

Arron Solano, managing partner at Calano, met Khan through Techstars and said he is an advocate for using credit cards in the right way. His firm was looking for a company like MaxRewards.

“During our first call, I remember telling my partner that Anik was a bulldog who knew what he was talking about, especially at that stage,” Solano added. “He had strong team members, his vision lined up well and that checked off a massive box for us. He energized us and showed he could find a market with insanely high ‘super users.’ ”

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

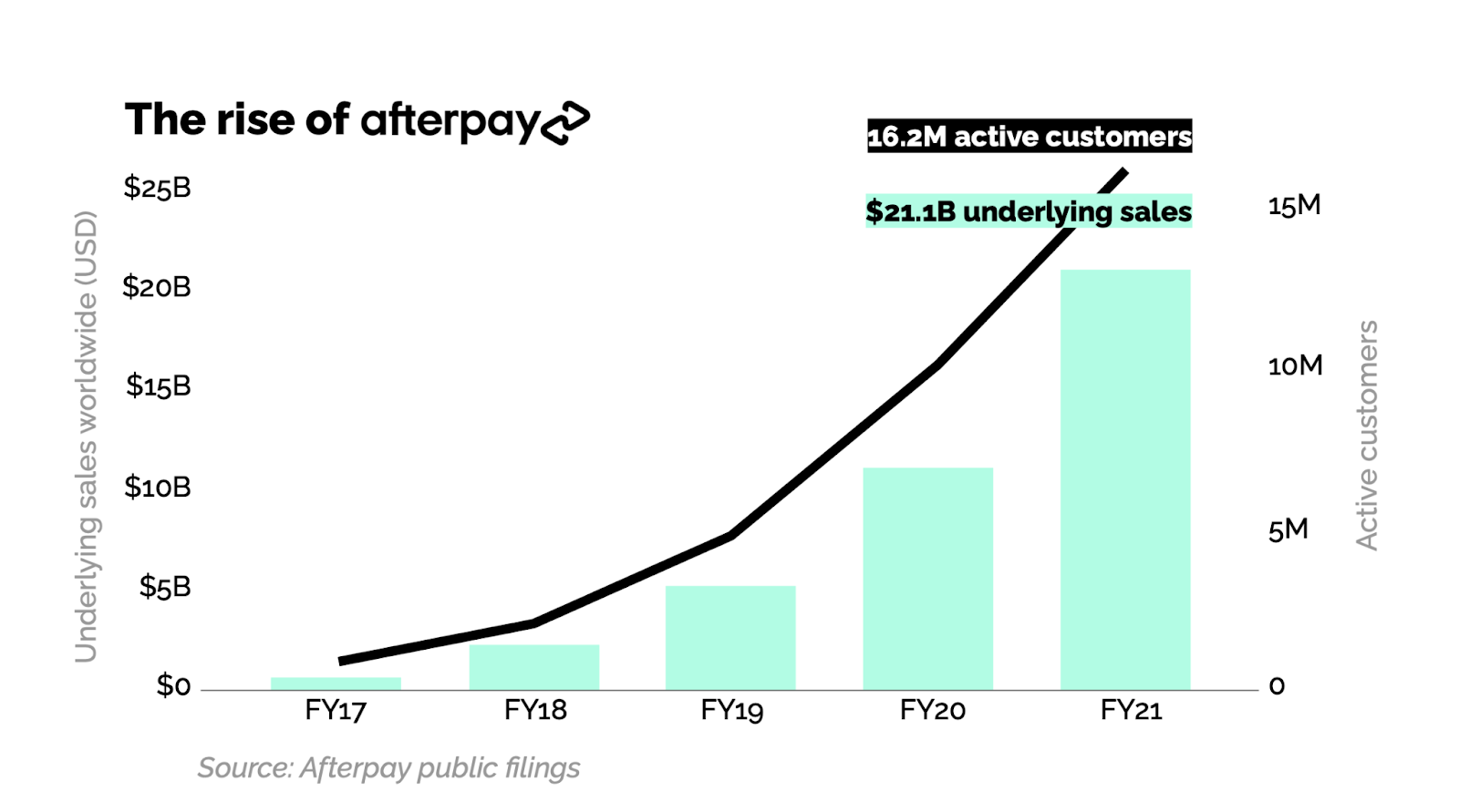

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

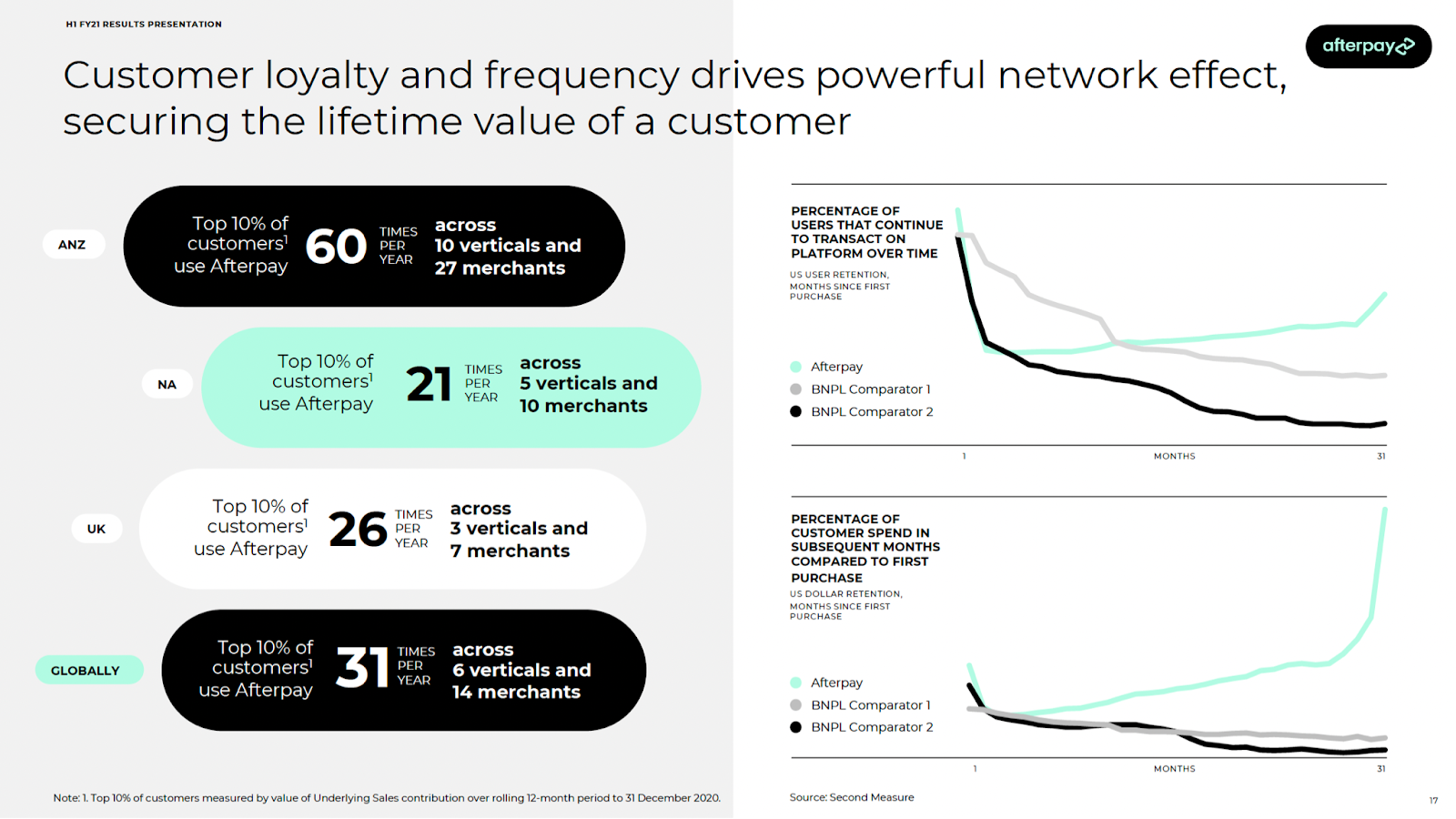

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

It looks like everyone and their mother is trying to reinvent the Brazilian banking system. Earlier this year we wrote about Nubank’s $400 million Series G, last month there was the PicPay IPO filing and today, alt.bank, a Brazilian neobank, announced a $5.5 million Series A led by Union Square Ventures (USV).

It’s no secret that the Brazilian banking system has been poised for disruption, considering the sector’s little attention to customer service and exorbitant fee structure that’s left most Brazilians unbanked, and alt.bank is just the latest company trying to take home a piece of the pie.

Following Nubank’s strategy of launching a bank with colors that are very un-bank-like, signaling that they do things differently, alt.bank similarly launched its first financial product in 2019 — a fluorescent-yellow debit card which the locals have endearingly dubbed, “o amarelinho,” meaning, “the little yellow card.”

The company, founded by serial entrepreneur Brad Liebmann, follows the founder’s $480 million exit of Simply Business, which was acquired by U.S. insurance giant Travelers in 2017.

Unlike many fintechs, alt.bank has a strong social mission and pays commissions for referrals that last for the customer’s lifetime.

“Most fintechs just help wealthy people get wealthier, so I thought let’s do something with a social mission,” Liebmann told TechCrunch in an interview.

To drive home the mission, and really target the unbanked, Liebman and his team of 80 employees have designed an app that can be used by the illiterate. Instead of words, users can follow color-coded prompts to complete a transaction. The company also plans to launch credit products soon.

According to the company, close to a million people have downloaded the android app since launch, but Liebman declined to disclose how many active users the company actually has.

Today, the company’s core offerings include the debit card, a prepaid credit card, Pix (similar to Zelle), a savings account and even telemedicine visits via a partnership with Dr. Consulta, a network of healthcare clinics throughout the country. The prepaid credit card is key because online stores in Brazil don’t accept debit card purchases.

In addition to the perk of ongoing commissions, alt.bank has also partnered with three major drugstores, allowing their users to get 5-30% off any item at the stores, including medication.

While the company is based in São Paulo and São Carlos, Liebmann and his family are currently based in London due to regulations around the pandemic.

The investment in alt.bank marks USV’s first investment in South America, solidifying a trend by other major U.S. investors such as Sequoia who only in the last several years have started looking to LatAm for deals.

“The bar was high for our first investment in South America,” said Union Square Ventures partner John Buttrick. “The combination of the alt.bank business model and world-class management team enticed us to expand our geographic focus to help build the leading digital bank targeting the 100 million Brazilians who are currently being neglected by traditional lenders,” he added in a statement.

Powered by WPeMatico

Diem, a London, U.K.-based fintech startup, has raised a seed round of $5.5 million led by Fasanara Capital, and angel investor Chris Adelsbach, founder of Outrun Ventures. Additional investors include Andrea Molteni (early investor in Farfetch), Ben Demiri (co-chairman at fashion tech PlatformE) and Nicholas Kirkwood (founder of the eponymous brand).

Diem is a debit card with an app affording instant cash access, traditional banking service benefits (debit card, domestic and international bank transfers), but also allowing consumers to dispose of goods for eventual resale. The idea here is that this feeds into the so-called circular economy, making Diem attractive from an environmental point of view. Some estimates put the amount of worth of goods disposed of in the last 15 years at $6.9 trillion.

Here’s how it works: You have an old item of clothing, phone, book or bag, for instance. You load the item it into the app. The app makes you an offer for what the item is worth. If you accept, cash is loaded into your account immediately. You send the item to Diem, which is then resold. The incentive, therefore, is not to throw away the object and add to landfill, because you have now turned it into cash. Think “neo bank meets people who sell your stuff on eBay.”

Geri Cupi said in a statement: “Diem’s mission is to empower consumers to value, unlock, and enjoy wealth they never knew they had. All of this while fuelling the circular economy and supporting the commitment to sustainability as our key value proposition. DIEM makes it possible for capitalism and sustainability to co-exist.”

Lead Investor and CEO at Fasanara Capital, Francesco Filia, said: “Fasanara is excited to announce our partnership with DIEM and Geri Cupi… [it’s] a new generation fintech powered by principles of circular economy and look forward to support its growth.”

Powered by WPeMatico

It’s only been a few months since Lili announced its $10 million seed round, and it’s already raised more funding — namely, a $15 million Series A.

The startup, founded by CEO Lilac Bar David and CTO Liran Zelkha, is creating a bank account and associated products designed for freelancers, with features like early access to direct deposit payments and the ability to set aside a percentage of income for taxes.

The account (and associated Visa debit card) is free of overdraft fees or minimum balance requirements; Bar David said the company only makes money from card processing fees.

She also said that the platform has seen rapid growth this year, with transactions up 700% since the beginning of the pandemic and nearly 100,000 accounts opened since the launch in 2019.

Bar David suggested that the economic turmoil caused by COVID-19 has prompted (or forced) more skilled workers — such as programmers and digital marketers — to turn to freelancing. Meanwhile, she’s also seen “a big shift from part-time freelance to full-time freelance.”

Lili CEO Lilac Bar David

Bar David predicted that the recent growth of the freelance economy won’t simply disappear once the pandemic is over, because workers are discovering the benefits of freelancing.

“If you have a 9-to-5 job, you’re dependent on one employer,” she said. “If something happens you’re out of a job … If you’ve got a diversified customer base, you’re not dependent on just one source of income.”

In recent months, Lili has added new features like automatically generated quarterly income and expense reports, a digital debit card (which customers can use before the physical card arrives in the mail) and the ability to send and receive money via Google Pay (Lili already supported Cash App and Venmo) .

Bar David said the startup decided to raise more funding to expand its engineering team and further accelerate its growth. Apparently she was preparing for a traditional Series A fundraising process (albeit one that was conducted in the middle of a pandemic), but “our current investors were so tremendously impressed by the product-market fit and the growth” that they were willing to fund almost all of the new round.

So the Series A was led by previous investor Group 11, with participation from Foundation Capital, AltaIR Capital, Primary Venture Partners and Torch Capital — along with new backer Zeev Ventures.

“As the global workforce evolves at a rapid pace, we are excited to lead another round of funding to help Lili capitalize on unprecedented demand and offer an entirely new solution to help freelancers seamlessly save time and money,” said Group 11’s Dovi Frances in a statement.

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

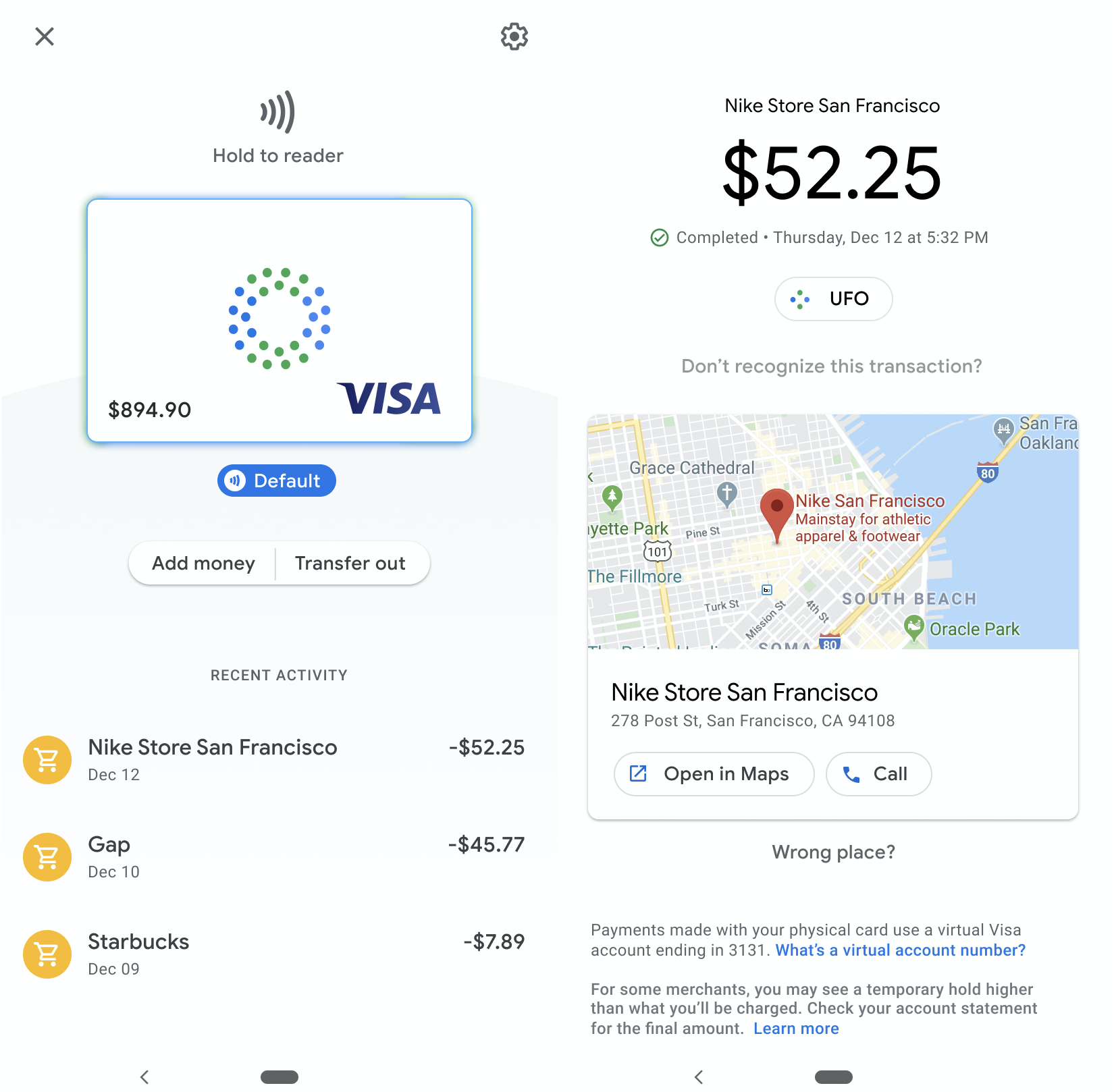

Would you pay with a “Google Card?” TechCrunch has obtained imagery that shows Google is developing its own physical and virtual debit cards. The Google card and associated checking account will allow users to buy things with a card, mobile phone or online. It connects to a Google app with new features that let users easily monitor purchases, check their balance or lock their account. The card will be co-branded with different bank partners, including CITI and Stanford Federal Credit Union.

A source provided TechCrunch with the images seen here, as well as proof that they came from Google. Another source confirmed that Google has recently worked on a payments card that its team hopes will become the foundation of its Google Pay app — and help it rival Apple Pay and the Apple Card. Currently, Google Pay only allows online and peer-to-peer payments by connecting a traditionally issued payment card. A “Google Pay Card” would vastly expand the app’s use cases, and Google’s potential as a fintech giant.

By building a smart debit card, Google has the opportunity to unlock new streams of revenue and data. It could potentially charge interchange fees on purchases made with the card or other checking account fees, and then split them with its banking partners. Depending on its privacy decisions, Google could use transaction data on what people buy to improve ad campaign measurement or even targeting. Brands might be willing to buy more Google ads if the tech giant can prove they drive a sales lift.

The long-term implications are even greater. While once the industry joke was that every app eventually becomes a messaging app, more recently it’s been that every tech company eventually becomes a financial services company. A smart debit card and checking accounts could pave the way for Google offering banking, stock brokerage, financial advice or robo-advising, accounting, insurance or lending.

Image Credits: jossnatu / Getty Images

Google’s vast access to data could allow it to more accurately manage risk than traditional financial institutions. Its deep connection to consumers via apps, ads, search and the Android operating system gives it ample ways to promote and integrate financial services. With the COVID-19 downturn taking shape, high-margin finance products could help Google develop efficient revenue opportunities and build its share price back up.

When TechCrunch asked Google for confirmation, it did not dispute our findings or assertions. The company offered us a statement it provided reporters following a November story, wherein Google told The Wall Street Journal’s Peter Rudegeair and Liz Hoffman it was experimenting in the checking account space. TechCrunch is the first to report Google’s debit card plans:

We’re exploring how we can partner with banks and credit unions in the US to offer smart checking accounts through Google Pay, helping their customers benefit from useful insights and budgeting tools, while keeping their money in an FDIC or NCUA-insured account. Our lead partners today are Citi and Stanford Federal Credit Union, and we look forward to sharing more details in the coming months.

For now, Google’s strategy is to let partnered banks and credit unions provide the underlying financial infrastructure and navigate regulation while it builds smarter interfaces and user experiences. It’s forseeable that one day Google might cut out the banks and take all the spoils for itself. Google launched a Wallet debit card in 2013 as an extension of its old payment app Google Wallet, but shut the card down in 2016. Given Google’s penchant for renaming or shutting down then reviving products, building a new debit card feels on-brand.

With people around the world suddenly more concerned about their finances amidst the coronavirus economic disaster, a debit card with more transparency and controls could be appealing.

Traditional banking products can be clunky, often requiring phone communication with customer service or sifting through cluttered websites to address security issues. Google hopes to make financial management as intuitive as its email and mapping apps. The card and app designs shown here are not final, and it’s unclear when Google’s debit card may launch. But let’s take a look at what these internal Google materials reveal about its ambitions for its payment instrument.

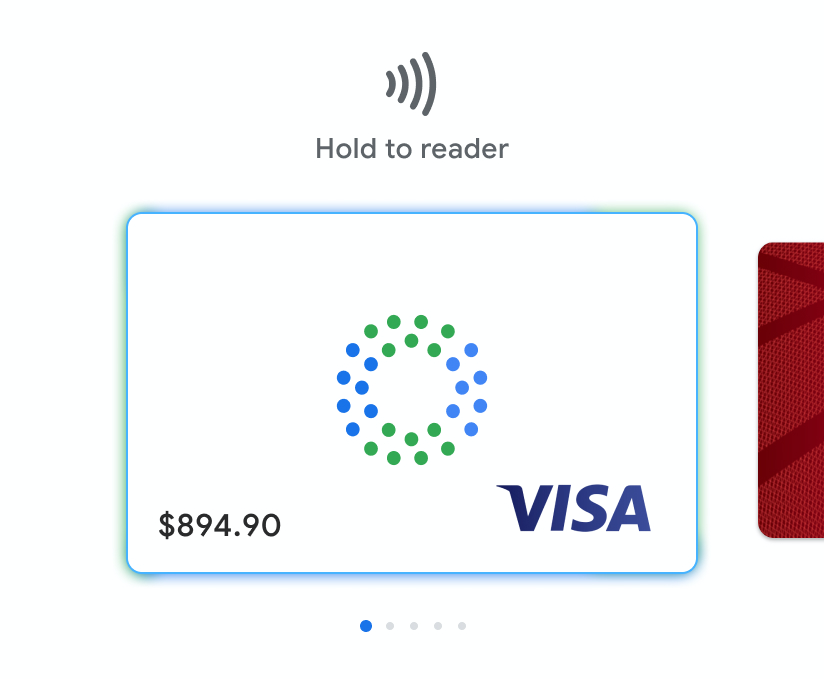

The Google debit card will come co-branded with the Google name and its partnered bank, though the exact name of the product is still unknown. In the designs, it’s a chip card on the Visa network, though Google could potentially support other networks like Mastercard. Users are able to add money or transfer funds out of their account from the connected Google app, which is likely to be Google Pay, and use a fingerprint and PIN for account security.

Once connected to their bank or credit union account, users could pay for purchases in retail stores with a physical Google debit card, including with contactless payments, by just holding it up to a card reader. A virtual version of the card that lives on a user’s phone can also be used for Bluetooth mobile payments. Meanwhile, a virtual card number can be used for online or in-app payments.

Users are shown a list of recent transactions, with each including the merchant name, date and price. They can dig into each transaction to see the location on a map, get directions or call the store. If users don’t recognize a transaction, it’s easy to protect themselves with the card’s vast security options.

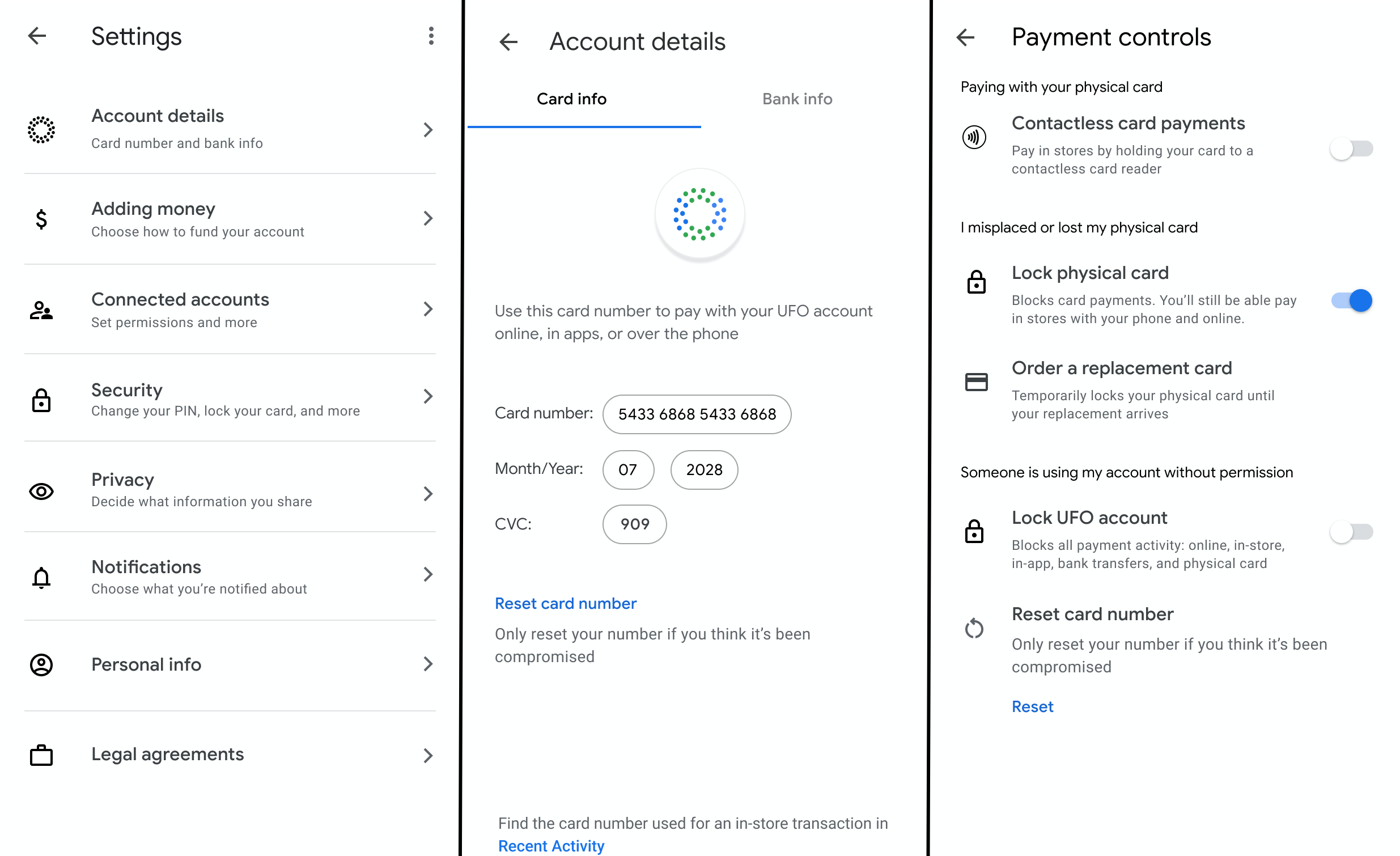

If a customer suspects foul play because they lost their card, they can lock it and optionally order a replacement while still being able to pay with their phone or online, thanks to Google’s virtual card number system that’s different than the one on their physical card. If instead they suspect their virtual card number was stolen by a hacker, they can quickly reset it. And if they believe someone has gained unauthorized access to their account, they can lock it entirely to block all types of payments and transfers.

The settings reveal options for notifications and privacy controls to “decide what information you share,” though we don’t have imagery of what’s contained in those menus. It’s unclear how much power Google will give customers to limit the company or merchant’s data access. Google’s decisions there could impact how transaction data might fuel its other businesses.

Google is a relative late-comer to offering its own card. Apple launched its Apple Card in August, offering a slickly designed titanium Mastercard credit card backed by Goldman Sachs. It charges minimal customer fees, comes with a virtual card for use through Apple Pay and generates interest.

Apple Card

Apple does collect interchange fees from merchants, though, which Google could similarly gather to earn revenue. Last month, Apple changed the Card’s privacy settings to share more data with Goldman Sachs that might also help the two provide additional financial services. Apple Pay now accounts for 5% of global card transactions, and is forecast to hit 10% by 2024, according to Bernstein research. The underlines the gigantic market Google is gunning for here.

The stock brokerage and robo-advisor apps have also joined the payments race. Wealthfront launched cash accounts and debit cards last February, bringing in $1 billion in assets in two months and doubling the company’s total holdings to $20 billion by September. Betterment launched its checking product in October 2019 with a Visa debit card, but it doesn’t generate interest.

Robinhood botched the December 2018 launch of its checking accounts due to ineligible insurance, but relaunched in October 2019 with debit card withdrawls from 75,000 ATMs and a solid interest rate. It’s unclear how Google’s card will work with ATMs or how its checking accounts will generate interest.

Robinhood’s debit cards

The appeal for Google and the rest is clear. It seems whenever companies help move people’s money around, some of it inevitably “falls off the truck” and lands in their pockets. Financial services are typically low-overhead ways to generate revenue. That could be especially enticing, as Google has found many of its side hustle “other bets” to be unsustainable. It’s moved to prune some of these tertiary projects, such as its Makani wind energy kites.

Google may never find businesses as lucrative as its core in search and advertising, but it has the advantages to become a serious player in fintech. Its vast sums of cash, deep bench of engineering talent, experience building complex utilities, numerous consumer touch points and near-bottomless well of data could give it an edge over stodgier old banks and scrappier startups. And while Facebook slams into regulatory scrutiny and is forced to scale back its Libra cryptocurrency, Google’s more familiar approach via debit cards could pay off.

Powered by WPeMatico

This time it actually has insurance. Zero-fee stock-trading app Robinhood is launching Cash Management, a new feature that earns users 2.05% APY interest on uninvested money in their account with the ability to spend it through a special Mastercard debit card. The waitlist opens today in the U.S. with the first users to be admitted soon. “If you have $5,000 in your account while you’re thinking about what to invest in, you’d have an extra $105 at the end of the year” thanks to Robinhood Cash Management’s interest, co-CEO Baiju Bhatt tells me.

The $7.6 billion-valuation startup first attempted something similar in December with Robinhood Checking, promising a stunningly tall 3% interest rate. But the product turned into a PR disaster when the Securities Investor Protection Corporation that was supposed to insure users’ funds declared Robinhood ineligible, with its CEO noting it had never agreed to cover checking accounts. That led Robinhood to shelve the feature, scrub its site of any mention of Checking and apologize.

Robinhood Cash Management’s debit cards, featuring the same design from the scrapped Checking launch

Now despite Bhatt claiming “Cash Management is a brand new program built from the ground up,” it will offer the same debit card design and network of 75,000 ATMs. It’s even using an identical promo image for its half-translucent green, black, white and American flag debit card designs. But each user’s funds will be covered by the Federal Deposit Insurance Corporation up to $1.25 million. To get around the $250,000 FDIC limit per bank, Robinhood is partnering with six banks that it will spread a user’s cash across as necessary to bundle up to that sum. Robinhood earns money by taking a chunk of the interchange fees from transactions on its debit card run in partnership with Sutton Bank, and from a fee paid by the six banks cash gets swept into.

To help it avoid further regulatory missteps, Robinhood yesterday added former SEC commissioner Dan Gallagher as its first independent board member. He joins the startup’s recently hired COO, CFO, chief compliance officer, VP of Risk & Compliance and VP of Legal & Regulatory to bring more supervision to Robinhood.

Robinhood co-founders and co-CEOs (from left): Baiju Bhatt and Vlad Tenev

The opt-in feature prevents users from missing out on earning interest if they keep money in their Robinhood account, and makes funds from stock sales quickly accessible via the debit card for spending or withdrawal. That convenience could give Robinhood an edge as its loses one if its key differentiators. Last week, its top incumbent competitors Charles Schwab, E*Trade and AmeriTrade all dropped their $4.95 to $6.95 fees on stock trades to match Robinhood’s free offering. That makes Cash Management and Robinhood Crypto even more critical to its continued growth. That’s necessary to justify the $7.6 billion valuation from its recent $323 million Series E raise led by DST Global that brings it to $860 million in total funding.

“We decided the best thing to do is giving people the peace of mind that their money is held at these banks, while trying to pay back the very best interest rates,” Bhatt tells me. [Disclosure: I know Robinhood’s co-founders from college.]

With Cash Management, once users deposit cash into the Robinhood accounts and opt into the program, they’re eligible to earn interest. Any balance on their account, including returns from sales of securities or cryptocurrencies, is swept into the FDIC-insured partner banks via Promontory’s debit suite system. Those banks include Wells Fargo, HSBC, Goldman Sachs, Citibank, U.S. Bank and Bank of Baroda. If one of those banks folds, the FDIC will make customers whole for up to $250,000, equaling $1.25 million across all six working with Robinhood. Users are able to opt out of specific banks.

There the cash earns a variable annual percentage yield (APY) that may fluctuate based on market factors like the Fed fund’s rate. Currently Robinhood offers a 2.05% APY, but refused to compare it to competitors. However, it ranks relatively high amongst popular banking options like these, according to Bankrate, especially given it has no minimum balance:

Robinhood Cash Management will also compete directly with Wealthfront Cash that launched in February and now offers 2.07% APY interest, but lacks a debit card or ATMs. Betterment Checking & Savings does provide a Visa debit card, but its current APY is 1.79%.

Cash Management users can select from the four debit card styles that are accepted anywhere that takes Mastercard, plus 75,000 ATMs. It also works with Apple Pay, Google Pay and Samsung Pay. There are no foreign transaction fees, maintenance fees or account minimum.

A variety of new Cash Management features are being added to the Robinhood app. You can get notifications and emails for all your transactions, and lock the card from your phone if you suspect fraud. You also can opt for location protection, which alerts you if your card is used too far away from your phone. An in-app ATM finder shows users where they can get cash without a fee.

“Partially we want this to be a good business but we also want this to be a big part of customer’s lives,” says Robinhood VP of product Josh Elman. Instead of nickel and diming Cash Management users, the startup monetizes by charging its partners. But the bigger strategy is to get more users on Robinhood in hopes some will subscribe to Robinhood Gold. There users pay a variable monthly fee depending on how much they want to borrow from the startup to trade on margin.

Robinhood co-CEO Baiju Bhatt speaks with TechCrunch’s Josh Constine at Disrupt SF 2018

“I think the main takeaway over the last year has been that since last December, our company has been very committed to building an organization that has a really strong culture [of compliance]” Bhatt concludes. “We’ve grown the leadership team over the last year with experience from risk and finance backgrounds. We think that’s reflected pretty clearly in how Robinhood operates and the diligence that went into building this new program.”

No longer a scrappy startup, the budding fintech giant must now grapple with much greater regulatory scrutiny. With more than 6 million users, the SEC won’t stand for it putting people’s finances in in jeopardy.

Powered by WPeMatico

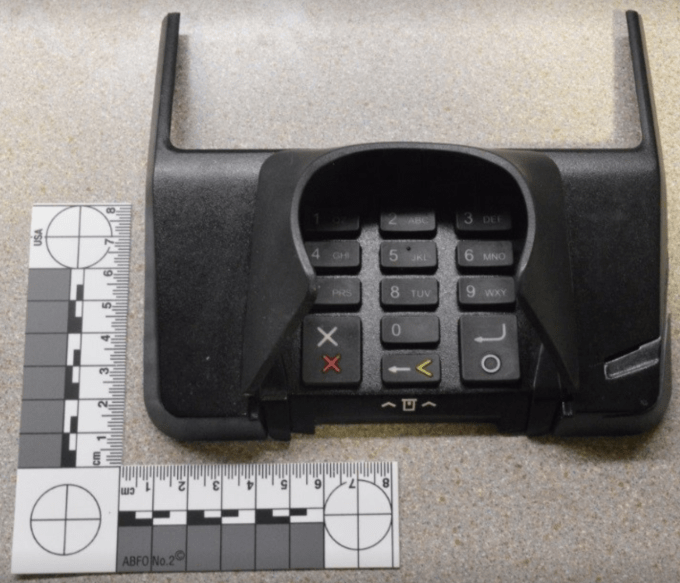

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Police in Lower Pottsgrove, Pennsylvania have spotted a group of thieves who are placing completely camouflaged skimmers on top of credit card terminals in Aldi stores. The skimmers, which the gang placed in plain sight of surveillance video cameras, look exactly like the original credit card terminals but would store debit card numbers and PINs of unsuspecting shoppers. “While Aldi… Read More

Powered by WPeMatico

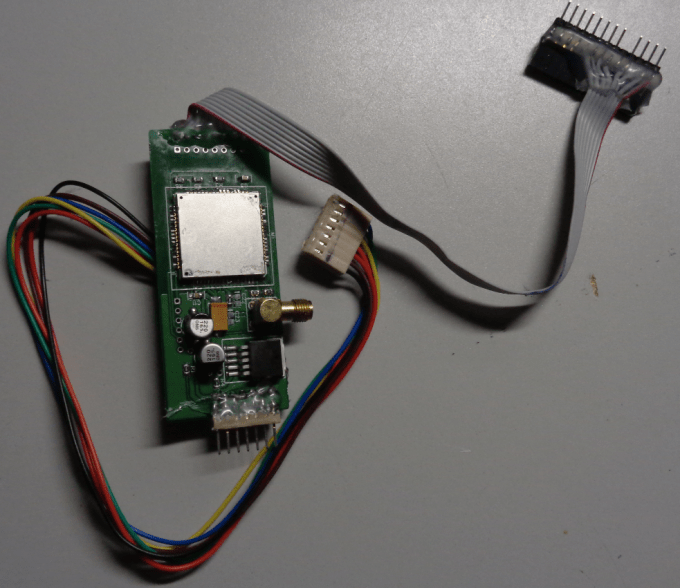

In an unsurprising move by credit card thieves, police have found a new credit card skimmer that sends stolen data via SMS. By tearing apart cheap phones, crooks are able to send credit card information to their location instantly without having to access the skimmer physically or rely on an open Bluetooth connection. Brian Krebs received images of the skimmer from an unnamed source. They… Read More

In an unsurprising move by credit card thieves, police have found a new credit card skimmer that sends stolen data via SMS. By tearing apart cheap phones, crooks are able to send credit card information to their location instantly without having to access the skimmer physically or rely on an open Bluetooth connection. Brian Krebs received images of the skimmer from an unnamed source. They… Read More

Powered by WPeMatico