Current

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

First and foremost, Equity was nominated for a Webby for “Best Technology Podcast”! Drop everything and go Vote for Equity! We’d appreciate it. A lot. And even if we lose, well, we’ll keep doing our thing and making each other laugh. (Note: We are in last place, which is, well, something.)

Regardless, the Equity team got together once again this week to not only go over the news of the week, but also to do a little soul searching. You see, some news broke yesterday, so we figured that we had to talk about it in our usual style. So, here’s the rundown:

We are back Monday morning with our weekly kick-off show. Have a great weekend!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

U.S.-based challenger bank Current, which has now grown to nearly 3 million users, announced this morning it has raised a $220 million round of Series D funding, led by new investor Andreessen Horowitz (a16z). The funding swiftly follows Current’s $131 million Series C at the end of last year, at which point the company had doubled its user base over just six months to more than 2 million users.

As a result of the new round, the fintech company has roughly tripled its valuation in five months, to $2.2 billion.

Other participants in the round include returning investors Tiger Global Management, TQ Ventures (the fund managed by media executive Scooter Braun), Avenir, Sapphire Ventures, Foundation Capital, Wellington Management and EXPA. David George, who led the round with a16z, will become a Current board member.

Current began its life as a teen debit card controlled by parents, but later expanded to offer personal checking accounts powered by the same underlying banking technology. Like a range of modern-day “neobanks,” or digital banks, the Current app offers a baseline of standard features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, free ATMs, check deposits using your phone’s camera and more. It also last year launched a points rewards program in an effort to better differentiate its service from the growing number of competitors and became one of the first banks to transfer the early round of stimulus payments during the pandemic.

These days, Current is partnering with creators, like the recently announced MrBeast (aka Jimmy Donaldson), who said last week on his YouTube channel that he will personally send $1 to the first 100,000 people who sign up using his Creator code. MrBeast is also an investor.

Like other fintechs in its same space, Current has benefitted from the younger generation’s adoption of mobile banking apps instead of larger, traditional banks, which they feel don’t serve their interests. Its average customer age is 27, for example. Digital banks can keep costs down by not having to pay for the overhead of brick-and-mortar locations, allowing them to roll out benefits like reduced or zero account fees and other consumer-friendly protections.

Current today continues to offer teen banking, in a challenge to mobile banking app Step, which has also leveraged social media influencers to get the word out with a younger demographic. But Step today is appealing to the 13 to 18-year-old crowd directly, offering banking services and a secured card. Current, meanwhile, targets its service to the parents.

Its teen account costs $36 per year, while personal checking is available both as a free and premium ($4.99/mo) service. The company in the past has said its primary focus is the more than 130 million Americans who live paycheck to paycheck. This continues to be its main drive today, though the mission may attract a broader slice of the American population over time.

“We are still focused on onboarding people to the financial system, making sure that everyone has access to everything, and then democratizing — or going out and getting that value — in this new world that’s being rewritten and bringing it back to as many people as possible,” says Current CEO and founder Stuart Sopp. “Now, in that increase of scope and time. I think we’re going to pick up more and more people.”

Current says the new funds will be used to grow the company and its member base as it expands it range of banking products. One key area of new investment will be cryptocurrency, it says, which will involve a partnership and an educational component to help Current’s users better understand the crypto market.

As it turns out, Sopp’s background includes crypto, in addition to Wall Street trading. In fact, an early version of Current designed by Sopp and CTO Trevor Marshall involved crypto.

“A little-known fact is that Current started with Bitcoin wallet addresses and Ripple gateways,” he says. But the team realized the technology was a little too nascent at the time, and moved to mobile banking. “We have this background, and this knowledge of how it all works. Now do we need to build it ourselves? No, I don’t think we need to build it all ourselves. There’s lots of good companies out there,” he says.

Crypto fits into Current’s vision of democratizing access to financial systems to those in the U.S. who are today underserved by traditional banking and investing products and services.

“There’s a ton of value being created [in crypto] and we want to make sure we have this nexus of providing safe, and trustworthy financial services in that world, as well as what we already exist in,” notes Sopp. “And then, lending, credit cards,” he adds, noting how important these moves are “done safely, in a respectful way for our demographic — because traditionally most of our members have a FICO score of 650.”

In addition, Current will use the new funds for hiring across all roles, including marketing, product, engineering, finance, customer success, fraud and risk, and, of course, crypto. The company today has 100 employees, and plans to grow to around 200 or 300 in the next 18 months.

Current’s fundraise remarkably falls on the same day that competitor Step and Greenlight, both which focus on families, also raised new rounds.

“This new generation of customers doesn’t want to bank in physical branches,” said a16z’s David George, in a statement. “We believe there will be a shift in the next 10 years to mobile and consumer-focused banking services powered by innovation in technology, and with Current’s exceptional growth over the past year, they’ve clearly demonstrated they’re at the forefront of this trend. Their product is among the best in the market, and they have proven an ability to reach customers who previously were unserved or underserved by traditional banks,” he said.

Powered by WPeMatico

U.S. challenger bank Current, which has doubled its member base in less than six months, announced this morning it raised $131 million in Series C funding, led by Tiger Global Management. The additional financing brings Current to over $180 million in total funding to date, and gives the company a valuation of $750 million.

The round also brought in new investors Sapphire Ventures and Avenir. Existing investors returned for the Series C, as well, including Foundation Capital, Wellington Management Company and QED.

Current began as a teen debit card controlled by parents, but expanded to offer personal checking accounts last year, using the same underlying banking technology. The service today competes with a range of mobile banking apps, offering features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, check deposits using your phone’s camera and other now-standard baseline features for challenger banks.

In August 2020, Current debuted a points rewards program in an effort to better differentiate its service from the competition, which as of this month now includes Google Pay.

When Current raised its Series B last fall, it had over 500,000 accounts on its service. Today, it touts over 2 million members. Revenue has also grown, increasing by 500% year-over-year, the company noted today.

“We have seen a demonstrated need for access to affordable banking with a best-in-class mobile solution that Current is uniquely suited to provide,” said Current founder and CEO Stuart Sopp, in a statement about the fundraise. “We are committed to building products specifically to improve the financial outcomes of the millions of hard-working Americans who live paycheck to paycheck, and whose needs are not being properly served by traditional banks. With this new round of funding we will continue to expand on our mission, growth and innovation to find more ways to get members their money faster, help them spend it smarter and help close the financial inequality gap,” he added.

The additional funds will be used to further develop and expand Current’s mobile banking offerings, the company says.

Powered by WPeMatico

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

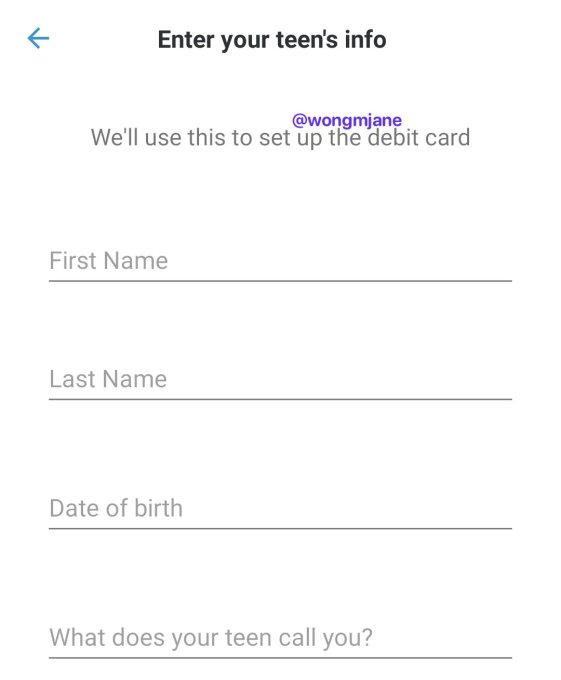

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

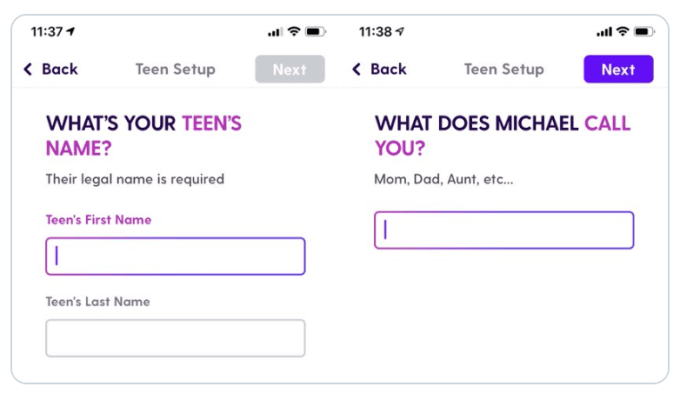

Current’s teen debit card

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

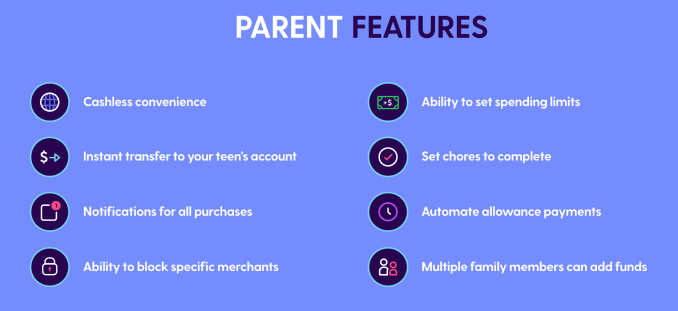

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

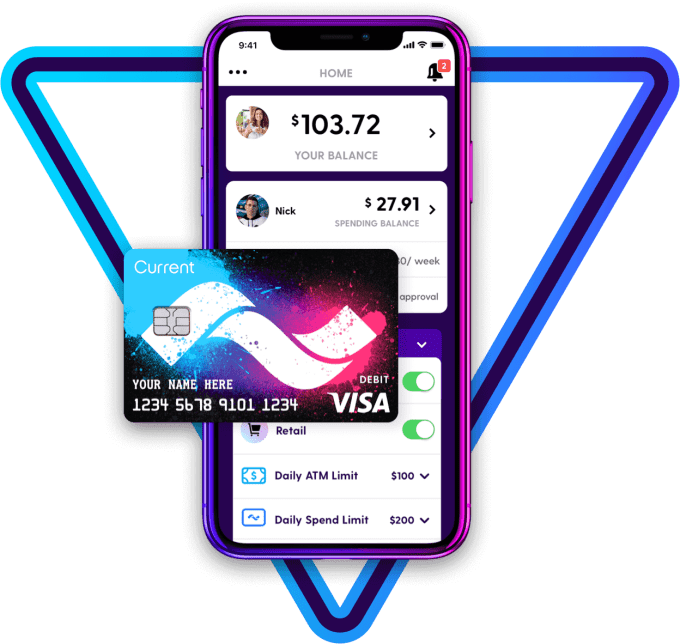

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

Mobile banking app Current, which began as a teen debit card controlled by parents, expanded to offer personal checking accounts earlier this year. Now the company says it has grown to host more than 500,000 accounts on its service and has closed on $20 million in Series B funding to further its growth.

The round included new investors Wellington Management Company, Galaxy Digital EOS VC Fund and CMFG Ventures — the venture capital arm of the CUNA Mutual Group, a mutual insurance company serving credit unions and their 120 million members. Returning investors included QED Investors, Expa and Elizabeth Street Ventures.

The first version of Current, which debuted in 2017, was focused on giving parents a more modern way to dole out allowances and reward their kids for chores. But over time, the product became more like a real bank account for teens, culminating with the addition of routing and account numbers late last year. This allowed working teens to direct their paycheck to Current, as they could with a traditional bank.

The first version of Current, which debuted in 2017, was focused on giving parents a more modern way to dole out allowances and reward their kids for chores. But over time, the product became more like a real bank account for teens, culminating with the addition of routing and account numbers late last year. This allowed working teens to direct their paycheck to Current, as they could with a traditional bank.

This year, Current launched personal checking using the same core technology powering its teen banking product. The product includes features like faster direct deposits, gas hold crediting and merchant blocking without charging overdraft fees, hidden fees or requiring minimum balances.

While the teen checking account users have an average age of 15, the average age for the new personal checking account users is 27.

Although personal checking was only launched in late January, it already accounts for about half of Current’s accounts. It also benefits from conversions from Current’s teen users who turn 18 and want to graduate to their own banking app. (Around 98% of teens on Current move to the personal checking app when they come of age, the company noted.)

This puts Current in a more competitive market, where a number of banking apps are now targeting a younger, more mobile generation that has begun to favor modern, feature-rich apps over brick-and-mortar banks. Among its rivals are apps like Step, Cleo, N26, Chime, Simple, Stash and others.

Like many in this space, Current isn’t actually a bank — its banking services are provided by Choice Financial Group and Metropolitan Commercial Bank, which allows it to offer FDIC insurance up to $250,000. Instead, many of the banking apps focus instead on the feature set and user experience they can offer.

Both of Current’s products include a Visa co-branded debit card tied to the Current account. Along with the funding, Current and Visa are also announcing an expanded joint marketing partnership, which will help Current reach new customers.

“We believe everyone should have access to affordable financial services that improve the chances for a better life,” said Stuart Sopp, Current founder and CEO. “We have made this a reality through rebuilding financial infrastructure with the Current Core. It allows us to build more products that offer new ways to interact with money. Our rapid growth to half a million accounts serves as a testament to the ways our products and cost savings are bringing better financial outcomes and we anticipate bringing those benefits to over 1,000,000 customers by mid-2020.”

The company is planning to launch more features starting next year, including a cash-back system with brands and merchants in Q1, and further down the road, it’s considering things like a credit product and maybe Bitcoin investing. But this will require further education and careful attention to do well.

“It’s expensive to be poor — it really is,” he says. “If you don’t have much money, you’re paying 30% or 35% for your credit, whereas if you’re rich you’re paying 5%. So it’s like the world is inverted for you and it holds you down,” Sopp says. “So if we were to do [credit], we are going to do it right.”

In the near-term, the focus is on offering better budgeting tools and more ways for users to save money. This, Sopp argues, is what Current’s young users need most.

To date, Current has raised $45 million in funding.

Powered by WPeMatico

A startup called Current is today launching a new way for parents to dole out allowances to their kids: with an app. The company offers a Visa debit card that would allow teenagers to shop in stores or online using funds from their own bank account, which is funded through allowance money that mom or dad transfers from their own bank account. Parents can use the accompanying mobile app to… Read More

A startup called Current is today launching a new way for parents to dole out allowances to their kids: with an app. The company offers a Visa debit card that would allow teenagers to shop in stores or online using funds from their own bank account, which is funded through allowance money that mom or dad transfers from their own bank account. Parents can use the accompanying mobile app to… Read More

Powered by WPeMatico