Cryptocurrency

Auto Added by WPeMatico

Auto Added by WPeMatico

It was the Lehman Brothers of blockchain. 850,000 Bitcoin disappeared when cryptocurrency exchange Mt. Gox imploded in 2014 after a series of hacks. The incident cemented the industry’s reputation as frighteningly insecure. Now a controversial crypto celebrity named Brock Pierce is trying to get the Mt. Gox flameout’s 24,000 victims their money back and build a new company from the ashes.

Pierce spoke to TechCrunch for the first interview about Gox Rising — his plan to reboot the Mt. Gox brand and challenge Coinbase and Binance for the title of top cryptocurrency exchange. He claims there’s around $630 million and 150,000 Bitcoin waiting in the Mt. Gox bankruptcy trust, and Pierce wants to solve the legal and technical barriers to getting those assets distributed back to their rightful owners.

The consensus from several blockchain startup CEOs I spoke with was that the plot is “crazy”, but that it also has the potential to right one of the biggest wrongs marring the history of Bitcoin.

But the story starts with Magic: The Gathering. Mt. Gox launched in 2006 as a place for players of the fantasy card game to trade monsters and spells before cryptocurrency came of age. The Magic: The Gathering Online eXchange wasn’t designed to safeguard huge quantities of Bitcoin from legions of hackers, but founder Jed McCaleb pivoted the site in 2010. Seeking to focus on other projects, he gave 88 percent of the company to French software engineer Mark Karpeles, and kept 12 percent. By 2013, the Tokyo-based Mt. Gox had become the world’s leading cryptocurrency exchange, handling 70 percent of all Bitcoin trades. But security breaches, technology problems, and regulations were already plaguing the service.

Then everything fell apart. In February 2014, Mt. Gox halted withdrawls due to what it called a bug in Bitcoin, trapping assets in user accounts. Mt. Gox discovered that it had lost over 700,000 Bitcoins due to theft over the past few years. By the end of the month, it had suspended all trading and filed for bankruptcy protection, which would contribute to a 36 percent decline in Bitcoin’s price. It admitted that 100,000 of its own Bitcoin atop 750,000 owned by customers had been stolen.

Mt. Gox is now undergoing bankruptcy rehabilitation in Japan overseen by court-appointed trustee and veteran bankruptcy lawyer Nobuaki Kobayashi to establish a process for compensating the 24,000 victims who filed claims. There’s now 137,892 Bitcoin, 162,106 Bitcoin Cash, and some other forked coins in Mt. Gox’s holdings, along with $630 million from the sale of 25 percent of the Bitcoin Kobayashi handled at a precient price point above where it is today. But five years later, creditors still haven’t been paid back.

Brock Pierce, the eccentric crypto celebrity

Pierce had actually tried to acquire Mt. Gox in 2013. The child actor known from The Mighty Ducks had gone on to work with a talent management company called Digital Entertainment Network. But accusations of sex crime led Pierce and some team members to flee the US to Spain until they were extradited back. Pierce wasn’t charged and paid roughly $21,000 to settle civil suits, but his cohorts were convicted of child molestation and child pornography.

The situation still haunts Pierce’s reputation and makes some in the industry apprehensive to be associated with him. But he managed to break into the virtual currency business, setting up World Of Warcraft gold mining farms in China. He claims to have eventually run the world’s largest exchanges for WOW Gold and Second Life Linden Dollars.

Soon Pierce was becoming a central figure in the blockchain scene. He co-founded Blockchain Capital, and eventually the EOS Alliance as well as a “crypto utopia” in Puerto Rico called Sol. His eccentric, Burning Man-influenced fashion made him easy to spot at the industry’s many conferences.

As Bitcoin and Mt. Gox rose in late 2012, Pierce tried to buy it, but “my biggest investor was Goldman Sachs. Goldman was not a fan of me buying the biggest Bitcoin exchange” due to the regulatory issues, Pierce tells me. But he also suspected the exchange was built on a shaky technical foundation that led him to stop pursuing the deal. “I thought there was a big risk factor in the Mt. Gox back-end. That was may intuition and I’m glad I was because my intuition was dead right.”

After Mt. Gox imploded, Pierce claims his investment group Sunlot Holdings successfully bought founder McCaleb’s 12 percent stake for 1 Bitcoin, though McCaleb says he didn’t receive the Bitcoin and it’s not clear if the deal went through. Pierce also claims he had a binding deal with Karpeles to buy the other 88 percent of Mt. Gox, but that Karpeles tried to pull out of the deal that remains in legal limbo.

The Sunlot has since been trying to handle the bankruptcy proceedings, but that arrangement was derailed by a lawsuit from CoinLab. That company had partnered with Mt. Gox to run its North American operations but claimed it never received the necessary assets, and sued Mt. Gox for $75 million, though Mt. Gox countersued saying CoinLab wasn’t legally certified to run the exchange in the US and that it hadn’t returned $5.3 million in customer deposits. For a detailed account the tangle of lawsuits, check out Reuters’ deep-dive into the Mt. Gox fiasco.

CoinLab co-founder Peter Vessenes

This week, CoinLab co-founder Peter Vessenes increased the claim and is now seeking $16 billion. Pierce alleges “this is a frivolous lawsuit. He’s claiming if [the partnership with Mt. Gox] hadn’t been cancelled, CoinLab would have been Coinbase and is suing for all the value. He believes Coinbase is worth $16 billion so he should be paid $16 billion. He embezzled money from Mt. Gox, he committed a crime, and he’s trying to extort the creditors. He’s holding up the entire process hoping he’ll get a payday.” Later, Pierce reiterated that “Coinlab is the villain trying to take all the money and see creditors get nothing.” Industry sources I spoke to agreed with that characterization

Mt. Gox customers worried that they might only receive the cash equivalent of their Bitcoin according to the currency’s $486 value when Gox closed in 2014. That’s despite the rise in Bitcoin’s value rising to around 7X that today, and as high as 40X at the currency’s peak. Luckily, in June 2018 a Japanese District Court halted bankruptcy proceedings and sent Mt. Gox into civil rehabilitation which means the company’s assets would be distributed to its creditors (the users) instead of liquidated. It also declared that users would be paid back their lost Bitcoin rather than the old cash value.

Now Pierce and Sunlot are attempting another rescue of Mt. Gox’s $1.2 billion assets. He wants to track down the remaining cryptocurrency that’s missing, have it all fairly valued, and then distribute the maximum amount to the robbed users with Mt. Gox equity shareholders including himself receiving nothing. That’s a much better deal for creditors than if Mt. Gox paid out the undervalued sum, and then shareholders like Pierce got to keep the Bitcoins or proceeds of their sale at today’s true value. “I‘ve been very blessed in my life I did commit to giving my first billion away” Pierce notes, joking that this plan could account for the first $700 million he plans to ‘donate’.

“Like Game Of Thrones, the last season of Mt. Gox hasn’t been written” Pierce tells me, speaking in terms HBO’s Silicon Valley would be quick to parody. “What kind of ending do we want to make for it? I’m a Joseph Campbell fan so I’m obviously going to go with a hero’s journey, with a rise and a fall, and then a rise from the ashes like a phoenix.”

But to make this happen, Sunlot needs at least half of those Mt. Gox users seeking compensation, or roughly 12,000 that represent the majority of assets, to sign up to join a creditors committee. That’s where GoxRising.com comes in. The plan is to have users join the committee there so they can present a united voice to Kobayashi about how they want Mt. Gox’s assets distributed. “I think that would allow the process to move faster than it would otherise. Things are on track to be resolved in the next three to five years. If [a majority of creditors sign on] this could be resolved in maybe 1 year.

Beyond providing whatever the Mt. Gox estate pays out, Pierce wants to create a Gox Coin that gives original Mt Gox creditors a stake in the new company. He plans to have all of Mt. Gox’s equity wiped out, including his own. Then he’ll arrange to finance and tokenize an independent foundation governed by the creditors that will seek to recover additional lost Mt. Gox assets and then distribute them pro rata to the Gox Coin holders. There are plenty of unanswered questions about the regulatory status of a Gox Coin and what holders would be entitled to, Pierce admits.

Meanwhile, Pierce is bidding to buy the intangibles of Mt. Gox, aka the brand and domain. He wants to then relaunch it as a Gox or Mt. Gox exchange that doesn’t provide custody itself for higher security.

“We want to offer [creditors] more than the bankruptcy trustee can do on its own” Pierce tells me. He concedes that the venture isn’t purely altruistic. “If the exchange is very successful I stand to benefit sometime down the road.” Still, he stands by his plan, even if the revived Mt. Gox never rises to legitimately challenge Binance, Coinbase, and other leading exchanges. Pierce concludes, “Whether we’re successful or not, I want to see the creditors made whole.” Those creditors will have to decide for themselves who to trust.

Powered by WPeMatico

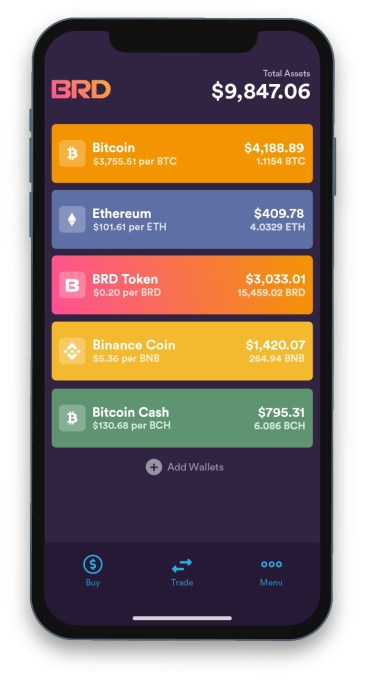

Mobile cryptocurrency wallet BRD is announcing that it has raised $15 million in Series B funding.

The funding comes from SBI Crypto Investment, a subsidiary of Japanese financial services company SBI Holdings (formerly a subsidiary of SoftBank). BRD said the funding will allow it to grow its product and engineering teams, and to expand in Japan and across Asia.

“SBI Group’s investment in BRD allows us to firmly cement ourselves in the Asian market,” said BRD co-founder and CEO Adam Traidman in a statement. “It shows incredible support for the foundation that we have built in North America and reinforces our proven ability to scale the success we have achieved in the past 4 years. The new investment will ensure our long-term global growth, and we are incredibly excited about collaborating with SBI as a strategic investor and business partner to make that happen.”

It’s surprising to see a crypto startup raising money now, given the broader crypto downturn. After all, BRD bills itself as the simplest way to start buying and storing cryptocurrencies — but does that mean anything if consumers are being scared away from investing?

When I asked Spencer Chen, the company’s vice president of global marketing (and an occasional friend of mine), about the industry’s recent challenges, he argued, “The need for a single, global currency still exists.”

“That’s what all got lost in 2018 as the fast-money, traders, and speculators came piling into the crypto space,” Chen told me via email. “It really convoluted the core mission of a natively digital currency. Money that worked just like the open internet. As a company that’s built-to-last and committed to the core mission of crypto currency, there was nothing more frustrating than to witness the many steps backwards the industry at large took in 2018.”

In fact, BRD says it doubled its total install base in 2018, ending the year with 1.8 million users globally. It also says it’s currently being used to store the equivalent of $6 billion mostly in Bitcoin and Ethereum — with a 24 percent increase in monthly active users between November and December, after it started accepting stablecoins (which are pegged to the value of a fiat currency).

BRD has now raised a total of $55 million. It’s also announcing a partnership with Coinify, allowing users to make cryptocurrency purchases using bank accounts in the European market.

Powered by WPeMatico

I’m not allowed to tell you exactly how Anchorage keeps rich institutions from being robbed of their cryptocurrency, but the off-the-record demo was damn impressive. Judging by the $17 million Series A this security startup raised last year led by Andreessen Horowitz and joined by Khosla Ventures, #Angels, Max Levchin, Elad Gil, Mark McCombe of Blackrock and AngelList’s Naval Ravikant, I’m not the only one who thinks so. In fact, crypto funds like Andreessen’s a16z crypto, Paradigm and Electric Capital are already using it.

They’re trusting in the guys who engineered Square’s first encrypted card reader and Docker’s security protocols. “It’s less about us choosing this space and more about this space choosing us. If you look at our backgrounds and you look at the problem, it’s like the universe handed us on a silver platter the Venn diagram of our skill set,” co-founder Diogo Monica tells me.

![]()

Today, Anchorage is coming out of stealth and launching its cryptocurrency custody service to the public. Anchorage holds and safeguards crypto assets for institutions like hedge funds and venture firms, and only allows transactions verified by an array of biometrics, behavioral analysis and human reviewers. And because it doesn’t use “buried in the backyard” cold storage, asset holders can actually earn rewards and advantages for participating in coin-holder votes without fear of getting their Bitcoin, Ethereum or other coins stolen.

The result is a crypto custody service that could finally lure big-time commercial banks, endowments, pensions, mutual funds and hedgies into the blockchain world. Whether they seek short-term gains off of crypto volatility or want to HODL long-term while participating in coin governance, Anchorage promises to protect them.

Anchorage’s story starts eight years ago when Monica and his co-founder Nathan McCauley met after joining Square the same week. Monica had been getting a PhD in distributed systems while McCauley designed anti-reverse engineering tech to keep U.S. military data from being extracted from abandoned tanks or jets. After four years of building systems that would eventually move more than $80 billion per year in credit card transactions, they packaged themselves as a “pre-product acqui-hire” Monica tells me, and they were snapped up by Docker.

As their reputation grew from work and conference keynotes, cryptocurrency funds started reaching out for help with custody of their private keys. One had lost a passphrase and the $1 million in currency it was protecting in a display of jaw-dropping ignorance. The pair realized there were no true standards in crypto custody, so they got to work on Anchorage.

“You look at the status quo and it was and still is cold storage. It’s the same technology used by pirates in the 1700s,” Monica explains. “You bury your crypto in a treasure chest and then you make a treasure map of where those gold coins are,” except with USB keys, security deposit boxes and checklists. “We started calling it Pirate Custody.” Anchorage set out to develop something better — a replacement for usernames and passwords or even phone numbers and two-factor authentication that could be misplaced or hijacked.

This led them to Andreessen Horowitz partner and a16z crypto leader Chris Dixon, who’s now on their board. “We’ve been buying crypto assets running back to Bitcoin for years now here at a16z crypto. [Once you’re holding crypto,] it’s hard to do it in a way that’s secure, regulatory compliant, and lets you access it. We felt this pain point directly.”

Andreessen Horowitz partner and Anchorage board member Chris Dixon

It’s at this point in the conversation when Monica and McCauley give me their off-the-record demo. While there are no screenshots to share, the enterprise security suite they’ve built has the polish of a consumer app like Robinhood. What I can say is that Anchorage works with clients to whitelist employees’ devices. It then uses multiple types of biometric signals and behavioral analytics about the person and device trying to log in to verify their identity.

But even once they have access, Anchorage is built around quorum-based approvals. Withdrawals, other transactions and even changing employee permissions requires approval from multiple users inside the client company. They could set up Anchorage so it requires five of seven executives’ approval to pull out assets. And finally, outlier detection algorithms and a human review the transaction to make sure it looks legit. A hacker or rogue employee can’t steal the funds even if they’re logged in because they need consensus of approval.

That kind of assurance means institutional investors can confidently start to invest in crypto assets. That swell of capital could help replace the retreating consumer investors who’ve fled the market this year, leading to massive price drops. The liquidity provided by these asset managers could keep the whole blockchain industry moving. “Institutional investing has had centuries to build up a set of market infrastructure. Custody was something that for other asset classes was solved hundreds of years ago, so it’s just now catching up [for crypto],” says McCauley. “We’re creating a bigger market in and of itself,” Monica adds.

With Anchorage steadfastly handling custody, the risk these co-founders admit worries them lies in the smart contracts that govern the cryptocurrencies themselves. “We need to be extremely wide in our level of support and extremely deep because each blockchain has details of implementation. This is inherently a very difficult problem,” McCauley explains. It doesn’t matter if the coins are safe in Anchorage’s custody if a janky smart contract can botch their transfer.

There are plenty of startups vying to offer crypto custody, ranging from Bitgo and Ledger to well-known names like Coinbase and Gemini. Yet Anchorage offers a rare combination of institutional-since-day-one security rigor with the ability to participate in votes and governance of crypto assets that’s impossible if they’re in cold storage. Down the line, Anchorage hints that it might serve clients recommendations for how to vote to maximize their yield and preserve the sanctity of their coin.

They’ll have crypto investment legend Chris Dixon on their board to guide them. “What you’ll see is in the same way that institutional investors want to buy stock in Facebook and Google and Netflix, they’ll want to buy the equivalent in the world 10 years from now and do that safely,” Dixon tells me. “Anchorage will be that layer for them.”

But why do the Anchorage founders care so much about the problem? McCauley concludes that, “When we look at what’s potentially possible with crypto, there a fundamentally more accessible economy. We view ourselves as a key component of bringing that future forward.”

Powered by WPeMatico

The Intercontinental Exchange’s (ICE) cryptocurrency project Bakkt celebrated New Year’s Eve with the announcement of a $182.5 million equity round from a slew of notable institutional investors. ICE, the operator of several global exchanges, including the New York Stock Exchange, established Bakkt to build a trading platform that enables consumers and institutions to buy, sell, store and spend digital assets.

This is Bakkt’s first institutional funding round; it was not a token sale. Participating in the round are Horizons Ventures, Microsoft’s venture capital arm (M12), Pantera Capital, Naspers’ fintech arm (PayU), Protocol Ventures, Boston Consulting Group, CMT Digital, Eagle Seven, Galaxy Digital, Goldfinch Partners and more.

Bakkt is currently seeking regulatory approval to launch a one-day physically delivered Bitcoin futures contract along with physical warehousing. The startup initially planned for a November 2018 launch, but confirmed this morning an earlier CoinDesk report that it was delaying the launch to “early 2019” as it awaits permission from the Commodity Futures Trading Commission. Along with the funding, crypto news blog The Block Crypto also reports Bakkt has hired Balaji Devarasetty, a former vice president at Vantiv, as its head technology.

ICE’s crypto project was first announced in August and is led by chief executive officer Kelly Loeffler, ICE’s long-time chief communications and marketing officer. Bakkt quickly inked partnerships with Microsoft, which provides cloud infrastructure to the service, and Starbucks, to develop “practical, trusted and regulated applications for consumers to convert their digital assets into U.S. dollars for use at Starbucks,” Starbucks vice president of payments Maria Smith said in a statement at the time.

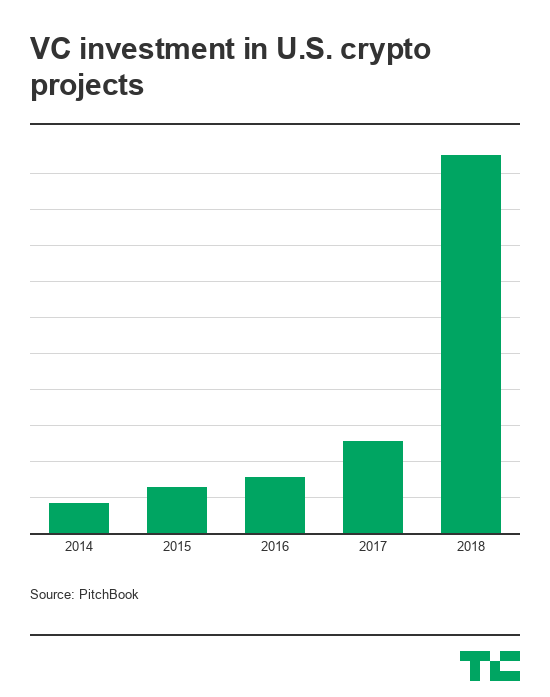

Many Bitcoin startups floundered in 2018, despite record amounts of venture capital invested in the industry. This was as a result of failed initial coin offerings, an inability to scale following periods of rapid growth and the falling price of Bitcoin. Still, VCs remained bullish on Bitcoin and blockchain technology in 2018, funneling a total of $2.2 billion in U.S.-based crypto projects — a nearly 4x increase year-over-year. Around the globe, investment hit a high of $4.6 billion — a more than 4x increase from last year, according to PitchBook.

“Notably, 2018 was the most active year for crypto in its brief ten-year history,” Loeffler wrote. “This was evidenced by rising investment in distributed ledger technology and digital assets, as well as by blockchain network metrics such as daily bitcoin transaction value and active addresses. Yet, these milestones tend to be overshadowed by the more narrow focus on bitcoin’s price, which has been seen by some, as a proxy for the potential of the technology.”

Today, the price of Bitcoin is hovering around $3,700 one year after a historic run valued the cryptocurrency at roughly $20,000. The crash caused many to dismiss Bitcoin and its underlying technology, while others remained committed to the tech and its potential for complete financial disruption. A project like Bakkt, created in-house at a respected financial institution with support from noteworthy businesses, is a logical bet for crypto and traditional private investors alike.

“The path to developing new markets is rarely linear: progress tends to modulate between innovation, dismissal, reinvention, and, finally, acceptance,” Loeffler added. “Each step, whether part of discovery or adversity, ultimately strengthens the product. Twenty years ago, it was controversial to suggest that commodities or bonds could trade electronically on a screen, and many steps were required for that evolution to play out.”

Powered by WPeMatico

A year ago, crypto was reaching ever new highs, and I was talking about whether ICOs would supplant the VC funding round and warning about Kim Jong Un’s crypto trading operations.

And then the world turned upside down.

Crypto prices are near rock-bottom prices, with Bitcoin hanging around $4,000 and Ethereum around $113, down from their highs earlier this year of around $16,600 and $1,400, respectively.

While that has put a dampener on the enthusiasm of a lot of cryptocurrency retail investors, the bigger question is how do institutional players work through this market? What’s the strategy for finding value in this technology sector long-term?

I chatted with Alexander Liegl, who may just have at least part of the answer. He’s the founder of Layer1, which announced a $2.1 million fundraise this week from Peter Thiel, Digital Currency Group and Jeffrey Tarrant.

Liegl saw a huge challenge in the blockchain and cryptocurrency spaces: too many good ideas and not enough developers working on product development work. So he decided to create an “activist fund for cryptocurrencies” that would “take concentrated bets on protocols that we think have a need in this world.” Layer1 then supplies developers and other experts to provide “infrastructure and support,” he explained. “An operating entity like us can have a lot of influence in moving the needle.” He describes Layer1 as “a combination of Polychain and Blockstreet” and “the Rocket Internet of crypto.”

That might sound vaguely similar to ConsenSys, the loosely coupled group of startups and infrastructure engineers trying to build out Ethereum, which has run into very hard times recently. Unlike ConsenSys, which was founded by Ethereum co-founder Joe Lubin and is directly focused on that ecosystem, Layer1 isn’t wedded to one blockchain or ecosystem, and instead selects a single project at a time through a mix of financial analysis and thesis development.

With capital in the bank, Layer1 has backed Grin as its first cryptocurrency. Grin is designed to be a completely private and censorship-resistant transaction medium, and Liegl says that “conceptually it really reconciles with our view in the space.” He particularly liked that Grin has an anonymous founder like Bitcoin, as no founder controls the governance of the project. Grin is intending to publicly launch in mid-January.

I asked Liegl how he was responding to the crypto crunch this year in the markets, and he considered it far more of an opportunity than a detriment to his work. “I’m really pumped about all of this,” he explained. “A lot of the bad actors have to be flushed out.” He noted that the low of the bear market may not be reached yet, but that Layer1 was in a good position to take advantage of the timing. “We raised the newest dollars, so we are not suffering from any of these ICO-induced problems,” he said.

Liegl, who graduated from Stanford in 2015 and briefly worked at Stanford’s endowment, has certainly seen the vagaries of the cryptocurrency markets. He learned about Bitcoin during its first popular run-up in 2013, even convincing his parents to invest in the budding project.

Now, he has his eyes set on Grin, and then additional projects. He thinks Layer1 will invest in a new project roughly every six to nine months, which will accelerate over time with additional capital.

While these “platform” models have struggled a bit in the venture world, I think it’s reasonable that blockchain projects, which often suffer from a lack of attention from developers and end uses, could use a strong engineering and popularization boost. Layer1 isn’t the first in the blockchain world to take this approach nor I am sure will it be the last, but it might be just the ticket forward for a world that has struggled to pay its employees and bills in a crash.

Powered by WPeMatico

Meet Spot, a beautifully designed mobile app to control your cryptocurrencies. Spot looks like a portfolio-tracking app. But the company has built a strong foundation to add more features in the coming months. Spot wants to be your unique gateway to the world of cryptocurrencies.

“Spot’s vision isn’t to build a portfolio tracker — we went a bit overboard with this feature,” co-founder and CEO Edouard Steegmann told me. “Eventually, we want to become the app to manage all your cryptos, a sort of Revolut but with a crypto DNA.”

When you first install the app, you can connect it to your existing wallets by adding public addresses. Even if you store your tokens on a hardware wallet, Spot can read the public details of your wallet to show them in the app.

“We have our own nodes on Ethereum, Bitcoin, Litecoin, Stellar and others to recover the amount on your wallet,” Steegmann said. Data is also cross-checked with third-party services to make sure that everything is fine.

Spot also lets you connect to an exchange account using API keys. Right now, the app supports Binance, Kraken, Bitfinex and Poloniex, but the company already plans to add more exchanges.

The app then gives you a detailed overview of your holdings across all services and wallets. You can see detailed charts, and discover which token is performing better than the rest. It’s also one of the most well-designed mobile apps I’ve seen this year — the animations and interactions are gorgeous.

But Spot doesn’t rely on an API to get pricing information for each token. “We’ve rebuilt CoinMarketCap from the ground up, and we’re one of the few companies that have done it,” Steegmann said. The company stores pricing information for dozens of tokens across 150 exchanges. That’s a lot of pairings.

If you tap on the Spot logo at the top of the app, you can see the maximum value of your portfolio if you cash out on exchanges with the highest prices for your tokens. The company makes sure that there’s enough volume to show you coherent prices.

Spot thinks that controlling your own data is too important to rely on API calls. When you have your own data, you don’t have any API rate limits, you don’t have a major dependency and you can scale more calmly.

Up next, you’ll be able to trade directly in the app. The company isn’t going to build its own exchange, but you can expect to buy and sell tokens on a third-party exchange without having to visit the website.

“We think that many things will be tokenized and that there’s no user-friendly interface to transfer, receive, buy and sell,” Steegmann said.

The company raised a $1.2 million round (€1.056 million to be exact) from Kima Ventures and business angels, including Eric Larchevêque and Thomas France from Ledger, Jean-Daniel Guyot, Thibaud Elzière, Eduardo Ronzano, Nicolas Steegmann, Sébastien Lucas and Nicolas Debock.

Disclosure: I own small amounts of various cryptocurrencies.

Powered by WPeMatico

Coinbase acquired Earn.com for at least $120 million back in April. And the company now plans to transform Earn.com into Coinbase Earn, a website with educational content to learn more about cryptocurrencies. Users who complete those classes will earn tokens.

Coinbase bought Earn.com partly so that it could appoint Earn.com co-founder and CEO Balaji Srinivasan as Coinbase’s CTO. The previous iteration of Earn.com wasn’t a priority for Coinbase.

Earn.com started as a service where you can contact busy people for a small fee. Busy people would get paid in cryptocurrencies to accept those requests. The platform quickly became a way to massively contact Earn.com’s user base for initial coin offerings and airdrops.

Coinbase Earn is launching today in private beta. But at the time of this article, the new Coinbase Earn service is not live (Update: Coinbase Earn is now live and is a separate website from Earn.com). Some Coinbase users will receive an invitation to the service. The company says that educational content will go beyond Bitcoin and Ethereum. Developing education pages for obscure cryptocurrencies makes sense as Coinbase plans to add dozens of cryptocurrencies over the coming months.

At first, there is just one track. Users can learn more about 0x (ZRX), a protocol that lets you create decentralized exchanges. Cryptocurrency trades can be executed without a centralized exchange thanks to 0x .

0x content includes video lessons and quizzes — and yes, writing this makes me feel like it’s 2005 and webinars are cool again. Even if you’re not invited to Coinbase Earn, you can view the content. But those who are part of Coinbase Earn will receive a small amount of ZRX at the end of the track.

Coinbase had previously launched a learning hub to understand the basics of cryptocurrencies.

Disclosure: I own small amounts of various cryptocurrencies.

Powered by WPeMatico

It’s hard to believe that you still had to convert your BTC into USD in order to buy ETH on Coinbase. The company is finally adding direct cryptocurrency-to-cryptocurrency conversions.

The feature works with Bitcoin (BTC), Ethereum (ETH), Ethereum Classic (ETC), Litecoin (LTC), 0x (ZRX) and Bitcoin Cash (BCH). It is only available to U.S. customers for now, but the company plans to roll out the feature to other countries too.

Let’s look at the fees more closely. If you live in Europe or the U.S., every time you buy or sell cryptocurrencies using USD or EUR, you pay at least 1.49 percent in fees on top of the spread (the difference between the highest selling price and the lowest purchasing price). Fees are even higher if you’re using a credit or debit card.

Coinbase says that the spread between a fiat currency and a cryptocurrency should be around 0.5 percent but may vary depending on the trading pair and the order queue.

If you buy or sell less than 200 USD or equivalent, fees get much more expensive. For instance, a $10 order will generate $0.99 in fees, or 9.9 percent. Customers pay 3 percent in fees for a $100 order.

But the good news is that it’s a completely different story with token-to-token transactions. Coinbase doesn’t charge you any markup fee — but there’s some inevitable spread. And with some obscure trading pairs (exchanging ZRX for BCH for instance), you might end up paying around 1 percent in spread. Still, it’s a much better user experience for those who just want to trade on Coinbase.

Without even mentioning other exchanges, Coinbase Pro users have been able to trade between multiple cryptocurrencies for a long time. But Coinbase is still the entry gate for many new cryptocurrency users.

Powered by WPeMatico

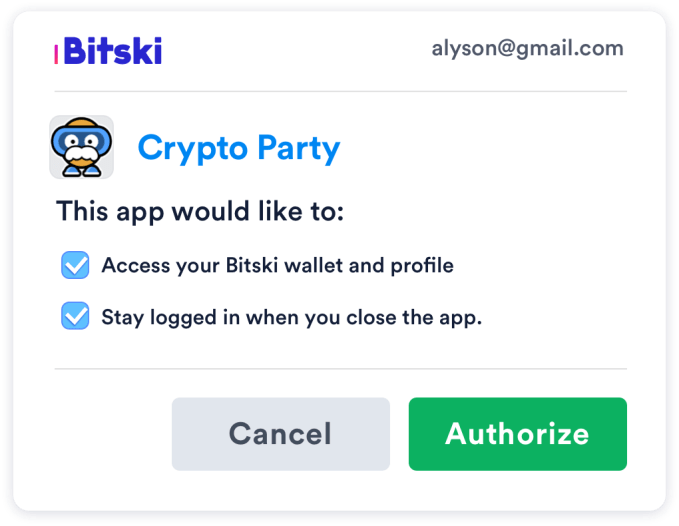

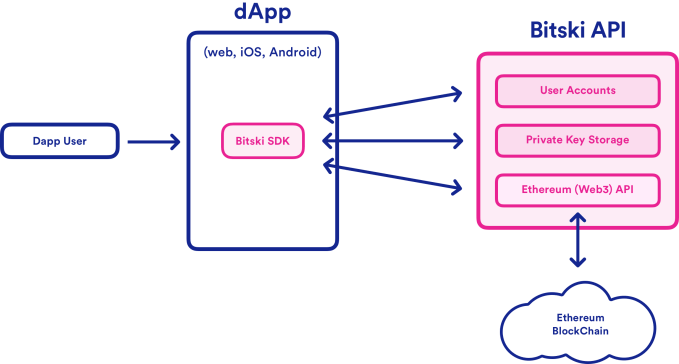

The mainstream will never adopt blockchain-powered decentralized apps (dApps) if it’s a struggle to log in. They’re either forced to manage complex security keys themselves, or rely on a clunky wallet-equipped browser like MetaMask. What users need is for signing in to blockchain apps to be as easy as Login with Facebook. So that’s what Bitski built. The startup emerges from stealth today with an exclusive on TechCrunch about the release of the developer beta of its single sign-on cryptocurrency wallet platform.

Ten projects, including 7 game developers, are lined up to pay a fee to integrate Bitski’s SDK. Then, whenever they need a user’s identity or to transact a payment, their app pops open a Bitski authorization screen, where users can grant permissions to access their ID, send money or receive items. Users sign up just once with Bitski, and then there’s no more punching in long private keys or other friction. Using blockchain apps becomes simple enough for novices. Given the recent price plunge, the mainstream has been spooked about speculating on cryptocurrencies. But Bitski could unlock the utility of dApps that blockchain developers have been promising but haven’t delivered.

“One of the great challenges for protocol teams and product companies in crypto today is the poor UX in dApps, specifically onboarding, transactions, and sign-in/password recovery,” says co-founder and CEO Donnie Dinch. “We interviewed a ton of dApp developers. The minute they used a wallet, there was a huge drop-off of folks. Bitski’s vision is to solve user onboarding and wallet usability for developers, so that they can in-turn focus on creating unique and useful dapps.”

The scrappy Bitski team raised $1.5 million in pre-seed capital from Steve Jang’s Kindred Ventures, Signia, Founders Fund, Village Global and Social Capital. They were betting on Dinch, a designer-as-CEO who’d built concert discovery app WillCall that he sold to Ticketfly, which was eventually bought by Pandora. After 18 months of rebranding Ticketfly and overhauling its consumer experience, Dinch left and eventually recruited engineer Julian Tescher to come with him to found Bitski.

Bitski co-founder and CEO Donnie Dinch

After Riff failed to hit scale, the team hung up its social ambitions in late 2017 and “started kicking around ideas for dApps. We mocked up a Venmo one, a remittance app…but found the hurdle to get someone to use one of these products is enormous,” Dinch recalls. “Onboarding was a dealbreaker for anyone building dApps. Even if we made the best crypto Venmo, to get normal people on it would be extremely difficult. It’s already hard enough to get people to install apps from the App Store.” They came up with Bitski to let any developer ski jump over that hurdle.

Looking across the crypto industry, the companies like Coinbase and Binance with their own hosted wallets that permitted smooth UX were the ones winning. Bitski would bring that same experience to any app. “Our hosted wallet SDK lets developers drop the Bitski wallet into their apps and onboard users with standards web 2.0 users have grown to know and love,” Dinch explains.

Imagine an iOS game wants to reward users with a digital sword or token. Users would have to set up a whole new wallet, struggle with their credentials or use another clumsy solution. They’d have to own Ethereum already to pay the Ethereum “gas” price to power the transaction, and the developer would have to manually approve sending the gift. With Bitski, users can approve receiving tokens from a developer from then on, and developers can pay the gas on users’ behalf while triggering transactions programmatically.

Magik is an AR content platform that’s one of Bitski’s first developers. Magik’s founders tell me, “We’re building towards reaching millions of mainstream consumers, and Bitski is the only wallet solution that understands what we need to reach users at that scale. They provide a dead-simple, secure and familiar interface that addresses every pain point along the user-onboarding journey.”

Bitski will offer a free tier, priced tiers based on transaction volume or a monthly fee and an enterprise version. In the future, the company is considering doubling-down on premium developer services to help them build more on top of the blockchain. “We will never, ever monetize user data. We’ve never had any intent at looking at it,” Dinch vows. The startup hopes developers will seize on the network effects of a cross-app wallet, as once someone sets up Bitski to use one product, all future sign-ins just require a few clicks.

In August, Coinbase acquired a startup called Distributed Systems that was building a similar crypto identity platform called the Clear Protocol. A “login with Coinbase” feature could be popular if launched, but the company’s focus is to spread a ton of blockchain projects. “If [login with Coinbase] launched tomorrow, they wouldn’t be able to support games or anything with a unique token. We’re a lockbox, they’re a bank,” Dinch claims.

The spectre of single sign-on’s biggest player, Facebook, looms, as well. In May it announced the formation of a blockchain team we suspect might be working on a crypto login platform or other ways to make the decentralized world more accessible for mom and pop. Dinch suspects that fears about how Facebook uses data would dissuade developers and users from adopting such a product. Still, Bitski’s haste in getting its developer platform into beta just a year after forming shows it’s eager to beat them to market.

Building a centralized wallet in a decentralized ecosystem comes with its own security risks. But Dinch assures me Bitski is using all its own hardware with air-gapped computers that have been stripped of their Wi-Fi cards, and it’s taking other secret precautions to prevent anyone from snatching its wallets. He believes cross-app wallets will also deliver a future where users actually own their virtual goods instead of just relying on the good will of developers not to pull them away or shut them down.” The idea of we’ve never been able to provably own unique digital assets is crazy to me,” Dinch notes. “Whether it’s a skin in Fortnite or a movie on iTunes that you purchase, you don’t have liquidity to resell those things. We think we’ll look back in 5 to 10 years and think it’s nuts that no one owned their digital items.”

While the crypto prices might be cratering and dApps like Cryptokitties have cooled off, Dinch is convinced the blockchain startups won’t fade away. “There is a thriving developer ecosystem hellbent on bringing the decentralized web to reality; regardless of token price. It’s a safe assumption that prices will dip a bit more, but will eventually rise whenever we see real use cases for a lot of these tokens. Most will die. The ones that succeed will be outcome-oriented, building useful products that people want.” Bitski’s a big step in that direction.

Powered by WPeMatico

Crypto news got a little boost last week after a dark month of crashes, stablecoins and birthdays. The SEC ruled that two ICO issuers, CarrierEQ Inc. and Paragon Coin Inc., were in fact selling securities instead of so-called utility tokens.

“Both companies have agreed to return funds to harmed investors, register the tokens as securities, file periodic reports with the Commission, and pay penalties,” wrote Pamela Sawhney of the SEC. “These are the Commission’s first cases imposing civil penalties solely for ICO securities offering registration violations.”

From the release:

Airfox, a Boston-based startup, raised approximately $15 million worth of digital assets to finance its development of a token-denominated “ecosystem” starting with a mobile application that would allow users in emerging markets to earn tokens and exchange them for data by interacting with advertisements. Paragon, an online entity, raised approximately $12 million worth of digital assets to develop and implement its business plan to add blockchain technology to the cannabis industry and work toward legalization of cannabis. Neither Airfox nor Paragon registered their ICOs pursuant to the federal securities laws, nor did they qualify for an exemption to the registration requirements.

This behavior — a sort of “damn the torpedoes” for the fintech set — was all the rage at the beginning of the year as no clear guidance was available for filing security tokens — essentially pieces of company equity — versus utility tokens which were, in theory, used within the company ecosystem. In fact, ICOed companies contorted themselves into all sorts of knots to appear to fit their “utility token” within the torturous confines of securities law.

“We have made it clear that companies that issue securities through ICOs are required to comply with existing statutes and rules governing the registration of securities,” said Stephanie Avakian, co-director of the SEC’s Enforcement Division. “These cases tell those who are considering taking similar actions that we continue to be on the lookout for violations of the federal securities laws with respect to digital assets.”

The SEC fined both companies $250,000 each. Future ICOs, at least in the U.S., would do well to keep this in mind.

Powered by WPeMatico