Cryptocurrency

Auto Added by WPeMatico

Auto Added by WPeMatico

Cryptocurrency exchange company Bitfinex is launching Bitfinex Pay, a cryptocurrency payment gateway. With this new product, online merchants can accept payments in various cryptocurrencies. It should make cross-border transactions easier in particular.

While there are a few crypto payment gateways already, Bitfinex Pay has the advantage of working seamlessly with the company’s exchange. Merchants can create a widget and start accepting payments in Ethereum and bitcoin. Payments are deposited on your exchange wallet.

Bitfinex’s widget works a bit like the “Buy Now with PayPal” button. When you click on the Bitfinex Pay button, you’re redirected to the cryptocurrency company’s website. Once your payment is approved, you’re redirected back to the original merchant website. Payments are capped at the equivalent of $1,000 in cryptocurrencies.

You don’t pay any fee with Bitfinex Pay transactions. Of course, there are some network fees involved with sending crypto tokens. Merchants will also end up paying fees if they want to convert their cryptocurrency holdings on the exchange and transfer fiat money out of their account.

Bitfinex Pay also lets you accept Tether payments. Tether is a stablecoin, which means that one unit of Tether is supposed to be worth one USD — it doesn’t fluctuate over time.

That statement has been challenged, as the attorney general in New York has concluded that Tethers weren’t fully backed by USD sitting in bank accounts at all times. At some point, Bitfinex couldn’t access $850 million held in a Panamanian bank.

As a result, Tether and Bitfinex are currently banned in the state of New York. So you’ll have to determine whether you trust Bitfinex enough to use it as part of your checkout process on your website.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Non-fungible tokens have been around for two years, but these NFTs, one-of-one digital items on the Ethereum and other blockchains, are suddenly becoming a more popular way to collect visual art, primarily, whether it’s an animated cat or an NBA clip or virtual furniture.

“Suddenly” is hardly an overstatement. According to the outlet Cointelegraph, during the second half of last year, $9 million worth of NFT goods sold to buyers; during one 24-hour window earlier this week, $60 million worth of digital goods were sold.

What’s going on? A thorough New York Times piece on the trend earlier this week likely fueled new interest, along with a separate piece in Esquire about the artist Beeple, a Wisconsin dad whose digital drawings, which he has created every single day for the last 13 years, began selling like hotcakes in December. If you evidence of a tipping point (and it’s amply available), the work of Beeple, whose real name is Mike Winkelmann, was just made available through Christie’s. It’s the venerable auction house’s first sale of exclusively digital work.

To better understand the market and why it’s blowing up in real time, we talked this week with David Pakman, a former internet entrepreneur who joined the venture firm Venrock a dozen years ago and began tracking Bitcoin soon after, even mining the cryptocurrency at his Bay Area home beginning in 2015. (“People would come over and see racks of computers, and it was like, ‘It’s sort of hard to explain.’”)

Perhaps it’s no surprise that he also became convinced early on of the promise of NFTs, persuading Venrock to lead the $15 million Series A round for a young startup, Dapper Labs, when its primary offering was CryptoKitties, limited-edition digital cats that can be bought and bred with cryptocurrency.

While the concept baffled some at the time, Pakman has long seen the day when Dapper’s offerings will be far more extensive, and indeed, a recent Dapper deal with the NBA to sell collectible highlight clips has already attracted so much interest in Dapper that it is reportedly right now raising $250 million in new funding at a post-money valuation of $2 billion. While Pakman declined to confirm or correct that figure, but he did answer our other questions in a chat that’s been edited here for length and clarity.

TC: David, dumb things down for us. Why is the world so gung-ho about NFTs right now?

DP: One of the biggest problems with crypto — the reason it scares so many people — is it uses all these really esoteric terms to explain very basic concepts, so let’s just keep it really simple. About 40% of humans collect things — baseball cards, shoes, artwork, wine. And there’s a whole bunch of psychological reasons why. Some people have a need to complete a set. Some people do it for investment reasons. Some people want an heirloom to pass down. But we could only collect things in the real world because digital collectibles were too easy to copy.

Then the blockchain came around and [it allowed us to] make digital collectibles immutable, with a record of who owns what that you can’t really copy. You can screenshot it, but you don’t really own the digital collectible, and you won’t be able to do anything with that screenshot. You won’t be able to to sell it or trade it. The proof is in the blockchain. So I was a believer that crypto-based collectibles could be really big and actually could be the thing that takes crypto mainstream and gets the normals into participating in crypto — and that’s exactly what’s happening now.

TC: You mentioned a lot of reasons that people collect items, but one you didn’t mention is status. Assuming that’s your motivation, how do you show off what you’ve amassed online?

DP: You’re right that one of the other reasons why we collect is to show it off status, but I would actually argue it’s much easier to show off our collections in the digital world. If I’m a car collector, the only way you’re going to see my cars is to come over to the garage. Only a certain number of people can do that. But online, we can display our digital collections. NBA Top Shop, for example, makes it very easy for you to show off your moments. Everyone has a page and there’s an app that’s coming and you can just show it off to anyone in your app, and you can post it to your social networks. And it’s actually really easy to show off how big or exciting your collection is.

TC: It was back in October that Dapper rolled out these video moments, which you buy almost like a Pokemon set in that you’re buying a pack and know you’ll get something “good” but don’t know what. But while almost half it sales have come in through the last week. Why?

DP: There’s only about maybe 30,000 or 40,000 people playing right now. It’s growing 50% or 100% a day. But the growth has been completely organic. The game is actually still in beta, so we haven’t been doing any marketing other than posting some stuff on Twitter. There hasn’t been attempt to market this and get a lot of players [talking about it] because we’re still working the bugs out, and there are a lot of bugs still to be worked out.

But a couple NBA players have seen this and gotten excited about their own moments [on social media]. And there’s maybe a little bit of machismo going on where, ‘Hey, I want my moment to trade for a higher price.’ But I also think it’s the normals who are playing this. All you need to play is a credit card, and something like 65% of the people playing have never owned or traded in crypto before. So I think the thesis that crypto collectibles could be the thing that brings mainstream users into crypto is playing out before our eyes.

TC: How does Dapper get paid?

DP: We get 5% of secondary sales and 100% minus the cost of the transaction on primary sales. Of course, we have a relationship with the NBA, which collects some of that, too. But that’s the basic economics of how the system works.

TC: Does the NBA have a minimum that it has to be paid every year, and then above and beyond that it receives a cut of the action?

DP: I don’t think the company has gone public with the exact economic terms of their relationships with the NBA and the Players Association. But obviously the NBA is the IP owner, and the teams and the players have economic participation in this, which is good, because they’re the ones that are creating the intellectual property here.

But a lot of the appreciation of these moments — if you get one in a pack and you sell it for a higher price — 95% of that appreciation goes to the owner. So it’s very similar to baseball cards, but now IP owners can participate through the life of the product in the downstream economic activity of their intellectual property, which I think is super appealing whether you’re the NBA or someone like Disney, who’s been in the IP licensing business for decades.

And it’s not just major IP where this NFT space is happening. It’s individual creators, musicians, digital artists who could create a piece of digital art, make only five copies of it, and auction it off. They too can collect a little bit each time their works sell in the future.

TC: Regarding NBA Top Shot specifically, prices range massively in terms of what people are paying for the same limited-edition clip. Why?

DP: There are two reasons. One is that like scarce items, lower numbers are worth more than higher numbers, so if there’s a very particular LeBron moment, and they made 500 [copies] of them, and I own number one, and you own number 399, the marketplace is ascribing a higher value to the lower numbers, which is very typical of limited-edition collector pieces. It’s sort of a funny concept. But it is a very human concept.

The other thing is that over time there has been more and more demand to get into this game, so people are willing to pay higher and higher prices. That’s why there’s been a lot of price appreciation for these moments over time.

TC: You mentioned that some of the esoteric language around crypto scares people, but so does the fact that 20% of the world’s bitcoin is permanently inaccessible to its owners, including because of forgotten passwords. Is that a risk with these digital items, which you are essentially storing in a digital locker or wallet?

DP: It’s a complex topic, but I will say that Dapper has tried to build this in a way where that won’t happen, where there’s effectively some type of password recovery process for people who are storing their moments in Dapper’s wallet.

You will be able to take your moments away from Dapper’s account and put it into other accounts, where you may be on your own in terms of password recovery.

TC: Why is it a complex topic?

DP: There are people who believe that even though centralized account storage is convenient for users, it’s somehow can be distrustful — that the company could de-platform you or turn your account off. And in the crypto world, there’s almost a religious ferocity about making sure that no one can de-platform you, that the things that you buy — your cryptocurrencies or your NFTs. Long term, Dapper supports that. You’ll be able to take your moments anywhere you want. But today, our customers don’t have to worry about that I-lost-my-password-and-I’ll-never-get-my-moments-again problem.

Powered by WPeMatico

The hodl-crew are having quite the moment as bitcoin passed the $50,000 mark earlier today for the first time. Data pegs the peak at just over $50,500.

The price of bitcoin, the world’s best-known cryptocurrency, has historically proven a reasonable proxy for consumer interest in the cryptocurrency space, and for trading activity amongst blockchain-based assets. Bitcoin’s price has retreated since the milestone, and is now worth just over $49,000.

Bitcoin has been on a tear this year, rising from around the $30,000 mark at the start of 2021 to its recent $50,000 milestone, a gain of around 66%. Looking back a year and the gains are even more impressive, with the price of bitcoin rising from around $10,000 a year ago to its current price, a gain of 400%.

Luckily for investors and believers in other decentralized tokens, it’s not just bitcoin that is enjoying a valuation updraft. Cardano, one of the most highly valued blockchain assets, is up around 27% in the last week, according to CoinMarketCap. Its total value is nearing the $27 billion mark.

Companies built atop the burgeoning cryptocurrency space could be enjoying a boom as the price of bitcoin advances; as trading activity and consumer interest tend to rise along with the price of bitcoin, and companies like Coinbase make money from trading activity and consumer use, 2021 is starting off strongly.

Coinbase has filed to go public, and intends to pursue a direct listing in short order.

What’s driving up the price of bitcoin and its sister-tokens in the short-term? In a market melt-up its hard to point fingers with any accuracy. But broadly speaking, if it feels that nearly every asset class is setting new all-time records, so why not bitcoin as well?

Powered by WPeMatico

The rest of the world may be slowing down as we prepare for Christmas and the new year, but we are not taking our foot off the gas.

Alex Wilhelm keeps a close watch on the public markets in his column The Exchange, but this week, he branched out to look at some of the metrics underpinning soaring cryptocurrency prices and turned his gaze on StockX, the consumer reseller marketplace that just raised $275 million in a Series E that values the company at approximately $2.8 billion.

“Selling a tenth of your company for north of a quarter-billion may be somewhat common among late-stage software startups with tremendous growth,” he says, but “don’t laugh — the round actually makes pretty OK sense.”

Our staff continues to file their end-of-year stories: We ran a post this morning by Manish Singh that studies India’s massive total addressable market for retail. The nation has more than 60 million mom-and-pop neighborhood stores, and companies like Walmart and Amazon are eager to offer help with payments, logistics and inventory management — as are hundreds of native and foreign startups.

In an interview with author and MIT professor Sinan Aral, Managing Editor Danny Crichton discussed some of the debates currently swirling around the desire in some quarters to regulate social media platforms. In “The Hype Machine,” Aral explores topics like neuroscience, economics and misinformation before offering potential solutions for resolving what he calls “a full-blown social media crisis.”

The stories that follow are an overview of Extra Crunch from the last five days. Complete articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Thank you very much for reading Extra Crunch this week; I hope you have a safe, relaxing weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman (opens in a new window)

How did fashion marketplace Poshmark go from posting regular losses in 2019 to generating net income in 2020?

After the company filed a public S-1 last night, Alex Wilhelm pondered the question this morning in The Exchange.

Like many e-commerce platforms, Poshmark saw a surge in activity during the COVID-19 pandemic, but it also slashed its marketing spend, which helped boost profits. As the cash-rich company prepares its road show, “Poshmark is valuable,” Alex concluded.

“How valuable the market will decide. But who will it enrich with its final pricing decision?”

WASHINGTON, D.C. – APRIL 22, 2018: A statue of Albert Gallatin, a former U.S. Secretary of the Treasury, stands in front of The Treasury Building in Washington, D.C. The National Historic Landmark building is the headquarters of the United States Department of the Treasury. (Photo by Robert Alexander/Getty Images)

The breach of FireEye and SolarWinds by hackers working on behalf of Russian intelligence is “the nightmare scenario that has worried cybersecurity experts for years,” reports Zack Whittaker.

The intrusion began several months ago, but news of the breach wasn’t made public until this week.

“Given that potential victims include defense contractors, telecoms, banks, and tech companies, the implications for critical infrastructure and national security, although untold at this point, could be significant,” said Erin Kenneally, director of cyber risk analytics at Guidewire, an industry platform for insurance carriers.

In his analysis for Extra Crunch, Zack breaks down the rippling effects of supply-chain attacks that can compromise platforms like SolarWinds, which is used by more than 420 of the Fortune 500.

Image Credits: dowell (opens in a new window) / Getty Images

Embedded finance connects services like payment processing with everyday activities like grabbing a coffee before unlocking an e-scooter.

“The ability to be at the right place at the right time, supporting consumers and merchants alike, where they want it, how they want it and when they want it — cannot be understated,” says Simon Wu, an investment director with Cathay Innovation.

In a post that identifies embedded finance’s top providers and enablers, he offers advice for startups and established brands that are hoping to “earn and build customer loyalty while generating new revenue streams.”

Image Credits: Nigel Sussman (opens in a new window)

Bitcoin is at an all-time high.

CoinMarketCap reports that crypto market values have reached almost $659 billion; that figure was just $140 billion in March 2020.

“These gains have created a huge amount of wealth for crypto holders,” Alex Wilhelm wrote yesterday.

To get a better handle on why crypto values are sky-bound, he parsed some basic industry metrics, including the number of unique bitcoin addresses, fees paid and transactions per day.

“Do the price gains make sense in the short term? Who knows,” he wrote, “but they are not based on nothing.”

Stage Light on Black. Image Credits: Fotograzia / Getty Images

For his year-end Extra Crunch story, security reporter Zack Whittaker looked back at the myriad security challenges and vulnerabilities COVID-19 brought to the fore.

The hacks of Fire Eyes and SolarWinds were just one link in the chain: How well is your company prepared to deal with file-encrypting malware, hackers backed by nation-states or employees accessing secure systems from home?

“With 2020 wrapping up, much of the security headaches exposed by the pandemic will linger into the new year,” says Zack.

Zoox Fully Autonomous, All-electric Robotaxi. Image Credits: Zoox

After six years of research and development, autonomous vehicle company Zoox this week unveiled an electric robotaxi that can carry four people at a maximum speed of 75 miles per hour.

Automotive writer Kirsten Korosec interviewed Zoox co-founder and CTO Jesse Levinson to learn more about the vehicle’s development and how the company overcame a series of technical and legal challenges.

“I would say that if you have a big idea and you’re confident that it makes sense, you should at least explore the idea, rather than giving up because the current regulations aren’t designed for it,” said Levinson.

Kirsten only had 15 minutes to interview Levinson, but this comprehensive interview covers topics like regulatory compliance, Zoox’s relationship with parent company Amazon and the highest (and lowest) moments he experienced along the way.

Fairy dust flying in gold light rays. Computer-generated abstract raster illustration. Image Credits: gonin / Wikimedia Commons

In one of the largest enterprise acquisitions of 2020, Visa Equity Partners this week purchased Utah-based edtech startup Pluralsight for $3.5 billion.

According to the entrepreneurs and investors reporter Natasha Mascarenhas spoke to, this deal “shows the strength of edtech’s capital options as the pandemic continues.”

“What’s happening in edtech is that capital markets are liquidating,” a major change from “the old days where the options to exit were very narrow,” says Deborah Quazzo, a managing partner at GSV Advisors and seed investor in Pluralsight.

Image Credits: Sophie Alcorn

Dear Sophie:

I’m on an F1 OPT and am about to incorporate a startup with my two American co-founders.

What were the biggest immigration changes in 2020 affecting us?

—Ambitious in Albany

High angle view of young man walking towards white doorways on blue background Image Credits: Klaus Vedfelt / Getty Images

Founders and the VCs who back them may not be friends, but they’re usually friendly.

Investors are on a first-name basis with entrepreneurs from their portfolio companies and frequently have candid conversations with them about life, work and the world in general. In the before times, they might even have shared a meal or attended a baseball game together.

But make no mistake, it is a top-down relationship — the investor will always have the upper hand. When an entrepreneur accepts a check, they are hiring their next boss.

In an Extra Crunch guest post, Quiq CEO and founder Mike Myer poses two questions for founders who are considering a new relationship with a VC:

NEW DELHI, INDIA – 2011/12/18: Rice is sold at a night market in Paharganj, the urban suburb opposite New Delhi Railway Station. (Photo by Frank Bienewald/LightRocket via Getty Images)

In India, about 90% of consumers buy their everyday goods from neighborhood-based kirana stores instead of supermarkets.

As a result, U.S. retail giants like Walmart and Amazon have adopted an “if you can’t beat them, join them” approach, offering the nation’s 60 million mom-and-pop shops software for inventory control, payments and e-commerce.

India’s retail market will be worth an estimated $1.3 trillion by 2025, but e-commerce represents just 3% of that activity today, reports Manish Singh.

For his final Extra Crunch story of 2020, he looked at the startups and major players who are hoping to carve out their niche in one of the world’s largest retail ecosystems.

Image Credits: PM Images / Getty Images

Earlier this year, business productivity software startup ClickUp raised a $35 million Series A.

Now, just six months later, the company has closed a second round of $100 million that values the San Diego-based startup at $1 billion.

Lucas Matney interviewed CEO Zeb Evans this week to learn more about how the company was buoyed by pandemic-based behavior shifts that doubled its customer base and multiplied revenue by a factor of nine.

“I think that the biggest thing that we’ve always focused on is shipping a new version of ClickUp every week. That is our differentiation,” he said. “We’ve kind of created these iterative cycles called natural product-market fit and it’s been hard to keep up with that.”

Multi Colored Bling Bling Dollar Sign Shape Bokeh Backdrop on Dark Background, Finance Concept. Image Credits: MirageC / Getty Images.

In 2018, the total value of the year’s 10 top enterprise mergers and acquisitions reached $87 billion; last year, that figure fell to just $40 billion.

But in 2020, 10 M&A deals accounted for $165.2 billion.

“Last year’s biggest deal — Salesforce buying Tableau for $15.7 billion — would have only been good for fifth place on this year’s list,” notes enterprise reporter Ron Miller. “And last year’s fourth largest deal, where VMware bought Pivotal for $2.7 billion, wouldn’t have even made this year’s list at all.”

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

As North America’s fourth-largest city, Toronto is one of the world’s top startup ecosystems.

After spawning companies like Eventbrite and Crowdmark, Ontario’s capital has attracted international talent that complements its homegrown population of entrepreneurs and technical talent.

Six investors we surveyed who work and live in the area said they believe Toronto will continue to thrive after the COVID-19 storm passes. Some of them focus exclusively on the region, while others invest elsewhere as well. As they explained, the city has a lot going for it: It’s diverse, has access to locally trained engineering and business workers, and the area has already fostered many companies that are doing very well.

Fintech is one of the city’s top industries, and the investors in this survey expect this to continue. Stephanie Choo, head of investments at Portag3 Ventures, said “fintech continues to see massive tailwinds from the fallout from COVID-19 as incumbents struggle to fully digitize their offerings.”

Ameet Shah of Golden Ventures listed fintech as one of Toronto’s key industries. Eva Lau of Two Small Fish Ventures agreed, adding that “blockchain has also been doing well because many blockchain-related technologies or companies were started in Toronto.”

Other investors point to fintech business leaders in Toronto like CEOs Mike Katchen of Wealthsimple, Daniel Eberhard of Koho, Andrew D’Souza and Michele Romanow of Clearbanc and Kirk Simpson of Wave Financial.

Nearly all of the surveyed investors cited diversity as a key reason to live and work in Toronto. Probal Lala, chairman of Maple Leaf Angels, says, “Beyond having a vibrant technology ecosystem, Toronto has one of the most diverse communities in North America and is not only a great place to find the intellectual horsepower and funding to build a great global startup, but also the mosaic of social communities that makes it a great place to live and raise a family.”

Choo said the United States’ current battles over immigration could benefit Canada. “Small, nimble teams that need to move fast may still choose to co-locate in person — and many will still want access to amenities that only a large, vibrant and diverse city like Toronto can offer.”

She also pointed to Toronto’s claim of being one of the most diverse cities in the world. “[This] not only makes the city interesting but also very welcoming for those who relocate from elsewhere; a strong startup and tech scene, and, lastly, a vibrant cultural and food scene, especially through the lens of cost-of-living compared to comparable major cities.”

Several VCs listed Shopify executives as local leaders, while others acknowledged the growing unicorn’s impact. Ameet Shah of Golden Ventures says, “Toronto has traditionally been strong in fintech, B2B SaaS, crypto and AI. The explosion of Shopify should also benefit companies focused on e-commerce and supply chain solutions.”

Adam McNamara and Ameet Shah, when asked about local business leaders, both listed Satish Kanwar. Kanwar is GM and VP of Product at Shopify after the company purchased Jet Cooper, a startup co-founded by Kanwar. McNamara also points to Farhan Thawar, Shopify’s VP of Engineering, as a local leader.

How much is local investing even a focus for you now? If you are investing remotely in general now, are you filtering for local founders?

Prior to COVID-19 hitting, a requirement for the majority of my investments was a face-to-face visit with the founding team. For the most part, this meant founders spending time in Toronto. As we primarily invest in seed and pre-seed, this usually meant local founders.

When the pandemic hit, we shifted our process to primarily Zoom meetings (including due diligence) and as a result the mix of founding teams has expanded beyond our typical catchment area (two-hour drive from the city) to a broader base. Investment cycles appear to have slowed a bit due to the remote approach but our reach to founding teams has expanded to a broader base of geographically distributed founding teams (Mostly Canadian although we have recently seen a number of international opportunities).

Powered by WPeMatico

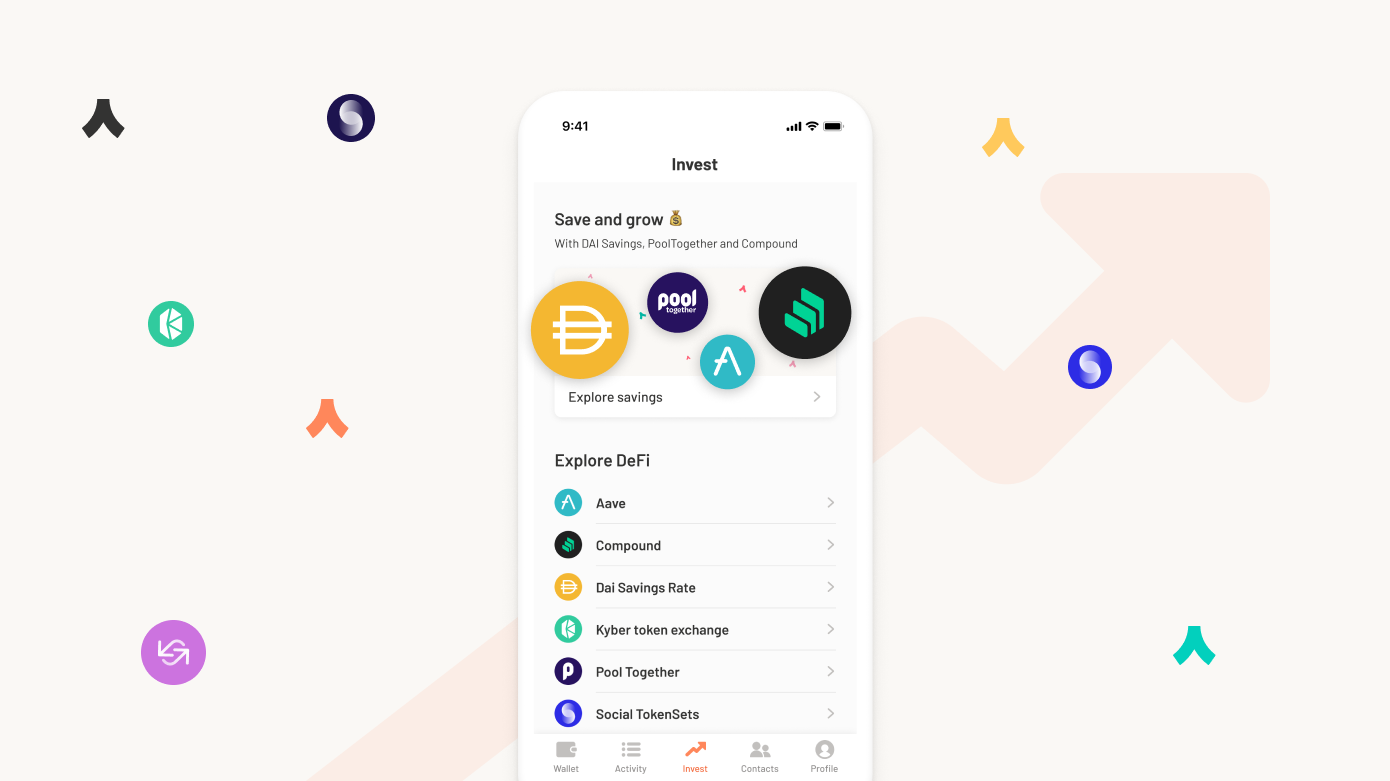

Argent is launching the first public version of its Ethereum wallet for iOS and Android. The company has been available as a limited beta for a few months with a few thousand users. But it has already raised a seed and a Series A round with notable investors, such as Paradigm, Index Ventures, Creandum and Firstminute Capital. Overall, the company has raised $16 million.

I managed to get an invitation to the beta a few months ago and have been playing around with it. It’s a well-designed Ethereum wallet with some innovative security features. It also integrates really well with DeFi projects.

Many people leave their crypto assets on a cryptocurrency exchange, such as Coinbase or Binance. But it’s a centralized model — you don’t own the keys, which means that an exchange could get hacked and you’d lose all your crypto assets. Similarly, if there’s a vulnerability in the exchange API or login system, somebody could transfer all your crypto assets to their own wallets.

At heart, Argent is a non-custodial Ethereum wallet, like Coinbase Wallet or Trust Wallet. You’re in control of the keys. Argent can’t initiate a transaction without your authorization for instance.

But that level of control brings a lot of complexities. Hardware wallets, such as Ledger wallets, ask you to write down a seed phrase so that you can recover your wallet if you lose your device. It requires some discipline and it’s hard to understand if you’re not familiar with the concept of seed phrases.

Even Coinbase Wallet tells you to back up your seed phrase when you first create a wallet. “We see them as advanced tools for developers,” Argent co-founder and CEO Itamar Lesuisse told me.

That’s why a new generation of wallets tries to hide the complexity from the end user, such as ZenGo and Argent. Creating a wallet on Argent is one of the best experiences in the cryptocurrency space. Your wallet is secured by something called ‘guardians’.

A guardian can be someone you know and trust, a hardware wallet (or another phone) or a MetaMask account. Argent also provides a guardian service, which requires you to confirm your identity with a text message and an email. If you lose your phone and you want to recover your wallet on another phone, you need to speak to your guardians and get a majority of confirmations. If they can all confirm that, yes, indeed, your phone doesn’t work anymore and you want to recover your crypto assets, the recovery process starts.

Let’s take an example. Here’s your list of guardians:

In total, there are five different factors involved, you including. If you lose your phone, you can recover your wallet by downloading Argent on another phone (factor #1), asking Argent’s guardian service to send you a text and an email to confirm your identity (factor #2) and confirming your identity with the Ledger Nano S (factor #3).

You have reached a majority and the recovery process starts. You’ll get your funds in 36 hours so that you have enough time to cancel it it’s a hijacking attempt.

But you could also have downloaded the Argent app on another phone (factor #1) and pinged your two friends (factor #2 and #3) directly. If they can confirm the same sequence of characters (emojis in that case), the recovery process would start as well.

“I’m interested in social recovery, multi-key schemes,” Ethereum creator Vitalik Buterin said in a TechCrunch interview in July 2018. It’s not a new concept as social media apps already use social recovery systems. On WeChat, if you lose your password, WeChat asks you to select people in your contact list within a big list of names.

In Argent’s case, social recovery adds an element of virality as well. The experience gets better as more people around you start using Argent.

In addition to wallet recovery, Argent uses guardians to put some limits. Just like you have some limits on your bank account, you can set a daily transaction limit to prevent attackers from grabbing all your crypto assets. You can ask your guardians to waive transactions above your daily limits.

Similarly, you can ask your guardians to lock your account for 5 days in case your phone gets stolen.

Argent is focused on the Ethereum blockchain and plans to support everything that Ethereum offers. Of course, you can send and receive ETH. And the startup wants to hide the complexity on this front as well as it covers transaction fees (gas) for you and gives you usernames. This way, you don’t have to set the transaction fees to make sure that it’ll go through.

The startup plans to integrate DeFi projects directly in the app. DeFi stands for decentralized finance. As the name suggests, DeFi aims to bridge the gap between decentralized blockchains and financial services. It looks like traditional financial services, but everything is coded in smart contracts.

There are dozens of DeFi projects. Some of them let you lend and borrow money — you can earn interest by locking some crypto assets in a lending pool for instance. Some of them let you exchange crypto assets in a decentralized way, with other users directly.

Argent lets you access TokenSets, Compound, Maker DSR, Aave, Uniswap V2 Liquidity, Kyber and Pool Together. And the company already has plans to roll out more DeFi features soon.

Overall, Argent is a polished app that manages to find the right balance between security and simplicity. Many cryptocurrency startups want to build the ‘Revolut of crypto’. And it feels like Argent has a real shot at doing just that with such a promising start.

Powered by WPeMatico

Coinbase’s mobile wallet app Coinbase Wallet puts you in control of your crypto assets. The app already lets you access decentralized crypto apps (dapps) using a dapp browser. But Coinbase is going one step further, with deep integrations with some of the most popular DeFi projects.

DeFi means “decentralized finance,” and it has been a hot trend in the cryptocurrency space. DeFi projects try to reproduce traditional financial products in the blockchain. For instance, you can lend and borrow money, invest in derivative assets and more.

A popular category of DeFi projects has been lending protocols, such as Compound and dYdX. Those protocols work pretty muck like LendingClub, but on the blockchain. Some users send money to a DeFi lending project to contribute to liquidity pools. Other users borrow money from that pool. Interest rates go up and down depending on supply and demand.

With today’s update, you can contribute to lending protocols much more easily. Coinbase Wallet lets you pick a cryptocurrency, compare interest rates across multiple DeFi protocols, interact with those protocols and view your balances in a unified dashboard, you don’t have to use Coinbase Wallet’s dapp browser.

Interest rates will change over time. At any time, you can check the current interest rate, see how much you’ve earned already and withdraw your crypto assets.

Those protocols rely on collateralized borrowing in order to avoid default payments. It means that borrowers have to lock crypto assets as collateral. You often have to provide a bigger collateral than what you’re trying to borrow with those DeFi protocols — that’s the downside of not relying on credit history and external financial data.

Again, this isn’t a traditional finance product. Your deposits are not insured and there could be some bugs in DeFi protocols. For instance, bZx recently suffered from a “flash loan” attack. But it’s an interesting crypto use case.

Powered by WPeMatico

Fintech startup Revolut has introduced a new trading feature for premium users. Starting today, Premium and Metal users can access gold exposure from the app.

Revolut works with a gold services partner (London Bullion Market Association) so that money you spend on gold exposure is backed by real gold held by this partner. In other words, you’re not going to receive gold coins in the mail. You can just invest money based on the price of gold.

The startup has been building a financial hub and already lets you purchase cryptocurrencies and buy public shares. Gold is part of a new feature called Commodities.

There are multiple ways to invest in gold. You can purchase gold exposure directly at market price, set a limit price to auto-exchange gold when it reaches a certain price or get cashback in gold for Metal customers.

At any time, you can convert your gold investment back into fiat currencies or cryptocurrencies. If you spend money with your Revolut card and you only have gold, Revolut will use your gold exposure automatically. You can also transfer gold exposure to another Revolut user.

According to the company’s website, Revolut charges a 0.25% markup when you trade gold during the week and a 1% markup from Saturday at midnight to Monday at midnight U.K. time.

It’s worth noting that gold isn’t protected through the Financial Services Compensation Scheme in the U.K. “However, in the unlikely event of Revolut’s insolvency, all Precious Metals holdings will be sold and proceeds will be credited to your e-money account,” Revolut says. You’ll have to trust their word.

Powered by WPeMatico

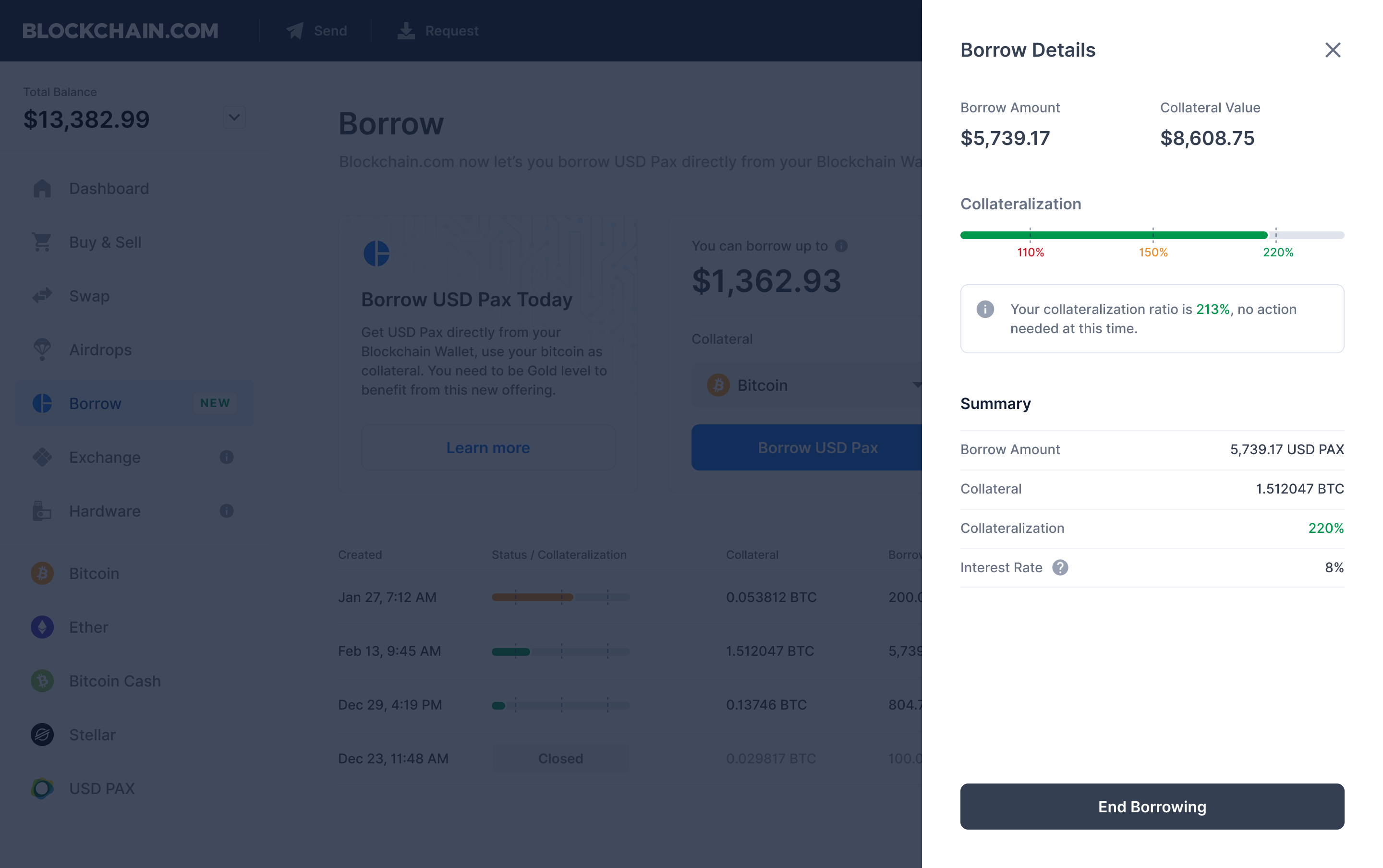

lets you borrow USD PAX against collateral")

What do you do when you’re rich in cryptocurrencies but you don’t want to sell your positions? The company named Blockchain thinks it has found a solution. It lets you borrow money against cryptocurrencies held in your Blockchain wallet.

As soon as you lock cryptocurrencies in your wallet, you receive USD PAX, a stablecoin that is pegged against USD. You can then convert, send and do whatever you want with your stablecoins. You can pay back your loan whenever you want.

The minimum loan size is $1,000 and Blockchain requires a collateralization ratio of 200%. It means that if you want to borrow $5,000, you need to put down the equivalent of $10,000 in cryptocurrencies as collateral.

Blockchain charges interest on loans. Your interest rate may vary but the company tries to be transparent about it before you accept the loan. By default, Blockchain uses your collateral to collect interest. Be careful with the value of your cryptocurrencies, as your collateral could end up losing a ton of value even though you still owe USD.

Behind the scene, Blockchain is running a lending desk for institutional investors. The company launched this feature back in August. Blockchain thinks that it has built a strong liquidity pool that it can leverage with retail investors.

Users in the U.S., Canada and the U.K. are not eligible to the feature for now. Blockchain only accepts collateral in BTC for now.

Powered by WPeMatico