crowdstrike

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re digging into seed-stage companies, the vanguard of the venture market. In particular, we’re trying to understand why the ratio of seed deals now favor enterprise startups over their consumer-focused brethren. The fact that seed investors recently inverted their preferences, cutting more checks to enterprise (B2B) startups in 2019 than consumer-oriented companies (B2C) was news.

We wrote about the trend here, as regular readers will recall.

To better understand what’s going on, I spoke with a number of early-stage venture investors who recently dropped by Equity, came highly recommended by peers, and several I know personally. The goal was to get a handful of inputs from different firms to get under the skin of the trend.

What in the hell is going on in seed? Let’s find out.

This morning we’ll hear from Jenny Lefcourt at Freestyle Capital, Jomayra Herrera of Cowboy Ventures, Hunter Walk from Homebrew, Iris Choi of Floodgate, Sarah Guo from Greylock and Ajay Agarwal of Bain Capital Ventures. As you can see, we picked a list of investors form firms of different sizes, theses and focus. However, each investing group either focuses on early-stage investments that include seed deals or dabbles in them.

Here’s what we want to know: why did the the majority of seed deals swap from consumer-focused startups to enterprise-focused deals?

Our investing group detailed a number of explanations, a handful of which echoed each other. To best convey their thinking, we’ll quote each investor at moderate length. If you are in a hurry, the most common point made against consumer-focused seed deals is go-to-market difficulty in the current market.

Other reasons include price, secular changes to the technology landscape, and the changing experience profile of the investing class themselves. (Minor edits made to select responses for clarity.)

Freestyle’s Jenny Lefcourt said via email that consumers are an increasingly difficult cohort to sell to, because they “became fickle with the proliferation of VC-backed, consumer-focused startups over the past few years.” As a result, consumers became “harder and more expensive to acquire and even harder to retain,” meaning higher customer acquisition costs (CAC) and lower lifetime value (LTV).

Powered by WPeMatico

A few days before Christmas, TechCrunch caught up with CrowdStrike CEO George Kurtz to chat about his company’s public offering, direct listings and his expectations for the 2020 IPO market. We also spoke about CrowdStrike’s product niche — endpoint security — and a bit more on why he views his company as the Salesforce of security.

The conversation is timely. Of the 2019 IPO cohort, CrowdStrike’s IPO stands out as one of the year’s most successful debuts. As 2020’s IPO cycle is expected to be both busy and inclusive of some of the private market’s biggest names, Kurtz’s views are useful to understand. After all, his SaaS security company enjoyed a strong pricing cycle, a better-than-expected IPO fundraising haul and strong value appreciation after its debut.

Notably, CrowdStrike didn’t opt to pursue a direct listing; after chatting with the CEO of recent IPO Bill.com concerning why his SaaS company also decided on a traditional flotation, we wanted to hear from Kurtz as well. The security CEO called the current conversation around direct listings a “great debate,” before explaining his perspective.

Pulling from a longer conversation, what follows are Kurtz’s four tips for companies gearing up for a public offering, why his company elected chose a traditional public offering over a more exotic method, comments on endpoint security and where CrowdStrike fits inside its market, and, finally, quick notes on upcoming debuts.

The following interview has been condensed and edited for clarity.

What’s most important is the fact that when we IPO’d in June of 2019, we started the process three years earlier. And that is the number one thing that I can point to. When [CrowdStrike CFO Burt Podbere] and I went on the road show everybody knew us, all the buy side investors we had met with for three years, the sell side analysts knew us. The biggest thing that I would say is you can’t go on a road show and have someone not know your company, or not know you, or your CFO.

And we would share — as a private company, you share less — but we would share tidbits of information. And we built a level of consistency over time, where we would share something, and then they would see it come true. And we would share something else, and they would see it come true. And we did that over three years. So we built, I believe, trust with the street, in anticipation of, at some point in the future, an IPO.

We spent a lot of time running the company as if it was public, even when we were private. We had our own earnings call as a private company. We would write it up and we would script it.

You’ve seen other companies out there, if they don’t get their house in order it’s very hard to go [public]. And we believe we had our house in order. We ran it that way [which] allowed us to think and operate like a public company, which you want to get out of the way before you come become public. If there’s a takeaway here for folks that are thinking about [going public], run it and act like a public company before you’re public, including simulated earnings calls. And once you become public, you already have that muscle memory.

The third piece is [that] you [have to] look at the numbers. We are in rarified air. At the time of IPO we were the fastest growing SaaS company to IPO ever at scale. So we had the numbers, we had the growth rate, but it really was a combination of preparation beforehand, operating like a public company, […] and then we had the numbers to back it up.

One last point, we had the [total addressable market, or TAM] as well. We have the TAM as part of our story; security and where we play is a massive opportunity. So we had that market opportunity as well.

On this topic, Kurtz told TechCrunch two interesting things earlier in the conversation. First that what many people consider as “endpoint security” is too constrained, that the category includes “traditional endpoints plus things like mobile, plus things like containers, IoT devices, serverless, ephemeral cloud instances, [and] on and on.” The more things that fit under the umbrella of endpoint security, CrowdStrike’s focus, the bigger its market is.

Kurtz also discussed how the cloud migration — something that builds TAM for his company’s business — is still in “the early innings,” going on to say that in time “you’re going to start to see more critical workloads migrate to the cloud.” That should generate even more TAM for CrowdStrike and its competitors, like Carbon Black and Tanium.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

It’s the second to last day of 2019, meaning we’re very nearly out of time this year; our space for repretrospection is quickly coming to a close. Before we do run out of hours, however, I wanted to peek at some data that former Kleiner Perkins investor and Packagd founder Eric Feng recently compiled.

Feng dug into the changing ratio between enterprise-focused Seed deals and consumer-oriented Seed investments over the past decade or so, including 2019. The consumer-enterprise split, a loose divide that cleaves the startup world into two somewhat-neat buckets, has flipped. Feng’s data details a change in the majority, with startups selling to other companies raising more Seed deals than upstarts trying to build a customer base amongst folks like ourselves in 2019.

The change matters. As we continue to explore new unicorn creation (quick) and the pace of unicorn exits (comparatively slow), it’s also worth keeping an eye on the other end of the startup lifecycle. After all, what happens with Seed deals today will turn into changes to the unicorn market in years to come.

Let’s peek at a key chart from Feng, talk about Seed deal volume more generally, and close by positing a few reasons (only one of which is Snap’s IPO) as to why the market has changed as much as it has for the earliest stage of startup investing.

Feng’s piece, which you can read here, tracks the investment patterns of startup accelerator Y Combinator against its market. We care more about total deal volume, but I can’t recommend the dataset enough if you have the time.

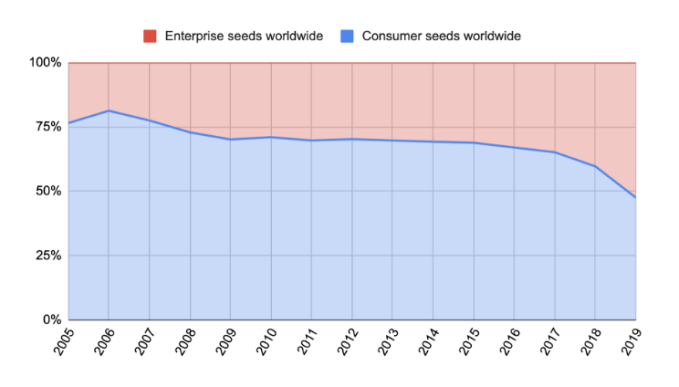

Concerning the universe of Seed deals, here’s Feng’s key chart:

Chart via Eric Feng / Medium

As you can see, the chart shows that in the pre-2008 era, Seed deals were amply skewed towards consumer-focused Seed investments. A new normal was found after the 2008 crisis, with just a smidge under 75% of Seed deals focused on selling to the masses for nearly a decade.

In 2016, however, a new trend emerged: a gradual decline in consumer Seed deals and a shift towards enterprise investments.

This became more pronounced in 2017, sharper in 2018, and by 2019 fewer than half of Seed deals focused on consumers. Now, more than half are targeting other companies as their future customer base. (Y Combinator, as Feng notes, got there first, making a majority of investments into enterprise startups since 2010, with just a few outlying classes.)

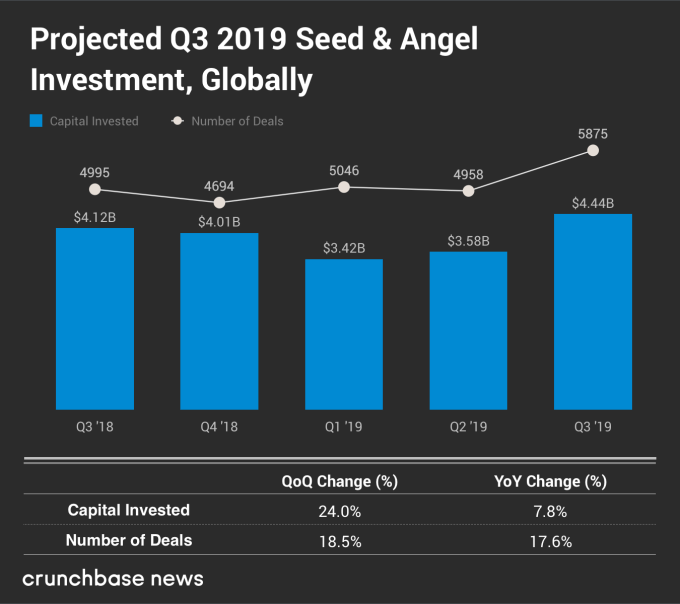

This flip comes as Seed deals sit at the 5,000-per-quarter mark. As Crunchbase News published as Q3 2019 ended, global Seed volume is strong:

So, we’re seeing a healthy number of deals as the consumer-enterprise ratio changes. This means that the change to more enterprise deals as a portion of all Seed investments isn’t predicated on their number holding steady while Seed deals dried up. Instead, enterprise deals are taking a rising share while volume appears healthy.

Now we get to the fun stuff; why is this happening?

As with many trends long in the making, there is no single reason why Seed investors have changed up their investing patterns. Instead, there are likely a myriad that added up to the eventual change. I’m going to ping a number of Seed investors this week to get some more input for us to chew on, but there are some obvious candidates that we can discuss today.

In no particular order, here are a few:

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the proliferation of billion-dollar companies. Before that, I noted the uptick in beverage startup rounds. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Now, time for some quick notes on Peloton’s confirmed initial public offering. The fitness unicorn, which sells a high-tech exercise bike and affiliated subscription to original fitness content, confidentially filed to go public earlier this week. Unfortunately, there’s no S-1 to pore through yet; all I can do for now is speculate a bit about Peloton’s long-term potential.

What I know:

A bullish perspective: Peloton, an early player in the fitness tech space, has garnered a cult following since its founding in 2012. There is something to be said about being an early-player in a burgeoning industry — tech-enabled personal fitness equipment, that is — and Peloton has certainly proven its bike to be genre-defining technology. Plus, Peloton is actually profitable and we all know that’s rare for a Silicon Valley company. (Peloton is actually New York-based but you get the idea.)

A bearish perspective: The market for fitness tech is heating up, largely as a result of Peloton’s own success. That means increased competition. Peloton has not proven itself to be a nimble business in the slightest. As Darrell noted in his piece, in its seven years of operation, “Peloton has put out exactly two pieces of hardware, and seems unlikely to ramp that pace. The cost of their equipment makes frequent upgrade cycles unlikely, and there’s a limited field in terms of other hardware types to even consider making. If hardware innovation is your measure for success, Peloton hasn’t really shown that it’s doing enough in this category to fend of legacy players or new entrants.”

TL;DR: Peloton, unlike any other company before it, sits evenly at the intersection of fitness, software, hardware and media. One wonders how Wall Street will value a company so varied. Will Peloton be yet another example of an over-valued venture-backed unicorn that flounders once public? Or will it mature in time to triumphantly navigate the uncertain public company waters? Let me know what you think. And If you want more Peloton deets, read Darrell’s full story: Weighing Peloton’s opportunity and risks ahead of IPO.

Anyways…

Public company corner

In addition to Peloton’s IPO announcement, CrowdStrike boosted its IPO expectations. Aside from those two updates, IPO land was pretty quiet this week. Let’s check in with some recently public businesses instead.

Uber: The ride-hailing giant has let go of two key managers: its chief operating officer and chief marketing officer. All of this comes just a few weeks after it went public. On the brightside, Uber traded above its IPO price for the first time this week. The bump didn’t last long but now that the investment banks behind its IPO are allowed to share their bullish perspective publicly, things may improve. Or not.

Zoom: The video communications business posted its first earnings report this week. As you might have guessed, things are looking great for Zoom. In short, it beat estimates with revenues of $122 million in the last quarter. That’s growth of 109% year-over-year. Not bad Zoom, not bad at all.

We cover a lot of startup and big tech news here at TechCrunch. Sometimes, the really great features writers put a lot of time and energy into fall between the cracks. With that said, I just want to take a moment this week to highlight a few of the great stories published on our site recently:

A peek inside Sequoia Capital’s low-flying, wide-reaching scout program by Connie Loizos

How to calculate your event ROI by Sarah Shewey

Why four security companies just sold for $1.5B by Ron Miller

In case you missed it, Bird is in negotiations to acquire Scoot, a smaller scooter upstart with licenses to operate in the coveted market of San Francisco. Scoot was last valued at around $71 million, having raised about $47 million in equity funding to date from Scout Ventures, Vision Ridge Partners, angel investor Joanne Wilson and more. Bird, of course, is a whole lot larger, valued at $2.3 billion recently.

On top of this deal, there was no shortage of scooter news this week. Bird, for example, unveiled the Bird Cruiser, an electric vehicle that is essentially a blend between a bicycle and a moped. Here’s more on the booming scooter industry.

Thumbtack is raising up to $120M on a flat valuation

Depop, a shopping app for millennials, bags $62M

Fitness startup Mirror nears $300M valuation with fresh funding

Step raises $22.5M led by Stripe to build no-fee banking services for teens

Possible Finance lands $10.5M to provide kinder short-term loans

Voatz raises $7M for its mobile voting technology

Flexible housing startup raises $2.5M

Legacy, a sperm testing and freezing service, raises $1.5M

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I discuss how a future without the SoftBank Vision Fund would look, Peloton’s IPO and data-driven investing.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a newsletter published every Saturday that dives into the week’s noteworthy venture capital deals, funds and trends. Before I dive into this week’s topic, let’s catch up a bit. Last week, I wrote about the sudden uptick in beverage startup rounds. Before that, I noted an alternative to venture capital fundraising called revenue-based financing. Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets.

Here’s what I’ve been thinking about this week: Unicorn scarcity, or lack thereof. I’ve written about this concept before, as has my Equity co-host, Crunchbase News editor-in-chief Alex Wilhelm. I apologize if the two of us are broken records, but I think we’re equally perplexed by the pace at which companies are garnering $1 billion valuations.

Here’s the latest data, according to Crunchbase: “2018 outstripped all previous years in terms of the number of unicorns created and venture dollars invested. Indeed, 151 new unicorns joined the list in 2018 (compared to 96 in 2017), and investors poured more than $135 billion into those companies, a 52% increase year-over-year and the biggest sum invested in unicorns in any one year since unicorns became a thing.”

2019 has already coined 42 new unicorns, like Glossier, Calm and Hims, a number that grows each and every week. For context, a total of 19 companies joined the unicorn club in 2013 when Aileen Lee, an established investor, coined the term. Today, there are some 450 companies around the globe that qualify as unicorns, representing a cumulative valuation of $1.6 trillion.

We’ve clung to this fantastical terminology for so many years because it helps us classify startups, singling out those that boast valuations so high, they’ve gained entry to a special, elite club. In 2019, however, $100 million-plus rounds are the norm and billion-dollar-plus funds are standard. Unicorns aren’t rare anymore; it’s time to rethink the unicorn framework.

Petition to stop using the term “unicorn” unless the company is valued at more than $1 billion *and* profitable.

— Kate Clark (@KateClarkTweets) May 22, 2019

Last week, I suggested we only refer to profitable companies with a valuation larger than $1 billion as unicorns. Understandably, not everyone was too keen on that idea. Why? Because startups in different sectors face barriers of varying proportions. A SaaS company, for example, is likely to achieve profitability a lot quicker than a moonshot bet on autonomous vehicles or virtual reality. Refusing startups that aren’t yet profitable access to the unicorn club would unfairly favor certain industries.

So what can we do? Perhaps we increase the valuation minimum necessary to be called a unicorn to $10 billion? Initialized Capital’s Garry Tan’s idea was to require a startup have 50% annual growth to be considered a unicorn, though that would be near-impossible to get them to disclose…

While I’m here, let me share a few of the other eclectic responses I received following the above tweet. Joseph Flaherty said we should call profitable billion-dollar companies Pegasus “since [they’ve] taken flight.” Reagan Pollack thinks profitable startups oughta be referred to as leprechauns. Hmmmm.

The suggestions didn’t stop there. Though I’m not so sure adopting monikers like Pegasus and leprechaun will really solve the unicorn overpopulation problem. Let me know what you think. Onto other news.

Image by Rafael Henrique/SOPA Images/LightRocket via Getty Images

CrowdStrike has set its IPO terms. The company has inked plans to sell 18 million shares at between $19 and $23 apiece. At a midpoint price, CrowdStrike will raise $378 million at a valuation north of $4 billion.

Slack inches closer to direct listing. The company released updated first-quarter financials on Friday, posting revenues of $134.8 million on losses of $31.8 million. That represents a 67% increase in revenues from the same period last year when the company lost $24.8 million on $80.9 million in revenue.

Online lender SoFi has quietly raised $500M led by Qatar

Groupon co-founder Eric Lefkofsky just-raised another $200M for his new company Tempus

Less than 1 year after launching, Brex eyes $2B valuation

Password manager Dashlane raises $110M Series D

Enterprise cybersecurity startup BlueVoyant raises $82.5M at a $430M valuation

Talkspace picks up $50M Series D

TaniGroup raises $10M to help Indonesia’s farmers grow

Stripe and Precursor lead $4.5M seed into media CRM startup Pico

Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, has closed on another $180 million to invest in early-stage consumer startups. The capital represents the firm’s seventh fundraise and largest since 2000. To keep the fund from reaching mammoth proportions, the firm’s general partners said they turned away more than $70 million amid high demand for the effort. There’s more where that came from, here’s a quick look at the other VCs to announce funds this week:

This week, I penned a deep dive on Slack, formerly known as Tiny Speck, for our premium subscription service Extra Crunch. The story kicks off in 2009 when Stewart Butterfield began building a startup called Tiny Speck that would later come out with Glitch, an online game that was neither fun nor successful. The story ends in 2019, weeks before Slack is set to begin trading on the NYSE. Come for the history lesson, stay for the investor drama. Here are the other standout EC pieces of the week.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I debate whether the tech press is too negative or too positive in its coverage of tech startups. Plus, we dive into Brex’s upcoming round, SoFi’s massive raise and CrowdStrike’s imminent IPO.

Powered by WPeMatico

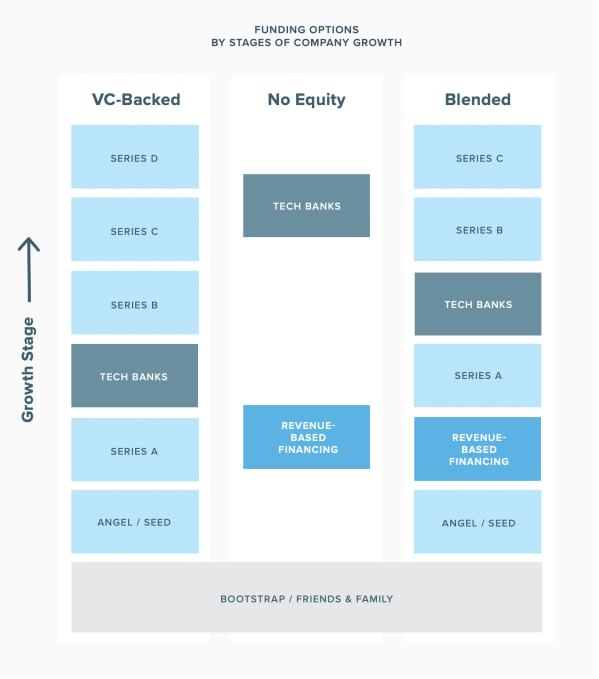

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

If you thought Uber’s disastrous initial public offering last week would deter fellow venture-backed technology companies from pursuing the public markets in 2019, you thought wrong.

CrowdStrike, yet another multi-billion-dollar Silicon Valley “unicorn,” has filed to go public. The cloud-based cybersecurity platform valued at $3.3 billion in 2018 revealed its IPO prospectus Tuesday afternoon.

The company plans to trade on the Nasdaq under the ticker symbol “CRWD.” According to the filing, it intends to raise an additional $100 million, though that figure is typically a placeholder amount. To date, CrowdStrike has raised $480 million in venture capital funding from Warburg Pincus, which owns a 30.3% pre-IPO stake, Accel (20.3%) and CapitalG (11.2%).

As we’ve come to expect of these companies, CrowdStrike’s financials are a bit concerning. While its revenues are growing at an impressive rate, from $53 million in 2017 to $119 million in 2018 to $250 million in the year ending January 31, 2019, its spending is far outweighing its gross profit. Most recently, the company posted a gross profit of $163 million on total operating expenses of about $300 million.

CrowdStrike is not yet profitable. Its total losses are increasing year-over-year from $91 million in 2017, to $135 million in 2018 and $140 million in 2019.

Headquartered in Sunnyvale, the business was founded in 2011 by chief executive officer George Kurtz and chief technology officer Dmitri Alperovitch, former McAfee executives. CrowdStrike, which develops security technology that looks at changes in user behavior on networked devices and uses that information to identify potential cyber threats, has reportedly pondered an IPO for some time.

The business sells its endpoint protection software to enterprises on a subscription basis, competing with Cylance, Carbon Black and others. In its S-1, CrowdStrike makes a case for its offering based on the rise of cloud computing and the growing threat of cybersecurity breaches. It estimates a total addressable market worth $29.2 billion by 2021.

“We founded CrowdStrike in 2011 to reinvent security for the cloud era,” the company writes. “When we started the company, cyberattackers had a decided, asymmetric advantage over existing security products. We turned the tables on the adversaries by taking a fundamentally new approach that leverages the network effects of crowdsourced data applied to modern technologies such as artificial intelligence, or AI, cloud computing, and graph databases.”

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

")

There’s been plenty of fanfare surrounding Uber and Lyft’s initial public offerings — slated for early 2019 — since the two companies filed confidential IPO paperwork with the U.S. Securities and Exchange Commission in early December. On top of that, public and private investors have had plenty to say about Slack and Pinterest’s rumored 2019 IPOs but those aren’t the only “unicorn” exits we should expect to witness in the year ahead.

Using its proprietary company rating algorithm, data provider CB Insights ranked five billion dollar companies most likely to perform IPOs next year in its latest tech IPO report. The algorithm analyzes non-traditional public signals, including hiring activity, web traffic and mobile app data to make its predictions. These are the startups that topped their list.

Peloton Co-Founder and CEO John Foley speaks onstage during TechCrunch Disrupt SF 2018 on September 6, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch).

Peloton, dubbed the “Netflix of fitness,” has raised nearly $1 billion in venture capital funding in the six years since it was founded by John Foley, most recently raising $550 million at a $4 billion valuation. The manufacturer of tech-enabled exercise equipment is more than doubling in size every year and is “weirdly profitable,” an unusual characteristic for a venture-backed business of its age. Headquartered in New York, Peloton doesn’t have any public IPO plans, though Foley recently told The Wall Street Journal that 2019 “makes a lot of sense” for its stock market debut.

Select investors: L Catterton, True Ventures, Tiger Global

Cloudflare co-founder and CEO Matthew Prince appears on stage at the 2014 TechCrunch Disrupt Europe/London. (Photo by Anthony Harvey/Getty Images for TechCrunch)

Cybersecurity unicorn Cloudflare is likely to transition to the public markets in the first half of 2019 in what is poised to be a strong year for IPOs in the security industry. The web performance and security platform is said to be preparing for an IPO at a potential valuation of more than $3.5 billion after last raising capital in 2015 at a $1.8 billion valuation. Since it was founded in 2009, the San Francisco-based company has raised just north of $250 million in VC funding. CrowdStrike, another security unicorn, is also on track to go public next year and it wouldn’t be surprising to see Illumio and Lookout make the jump to the public markets as well.

Select investors: Pelion Venture Partners, NEA, Venrock

San Jose-based Zoom Video Communications has reportedly tapped Morgan Stanley to lead its upcoming IPO.

Zoom, a provider of video conferencing services, online meeting and group messaging tools that’s raised $160 million in VC cash to date, is eyeing a multi-billion IPO in 2019 and has reportedly hired Morgan Stanley to lead the offering. Founded in 2011, the company most recently brought in a $100 million Series D financing, entirely funded by Sequoia, at a $1 billion valuation in early 2017. Based in San Jose, Zoom is hoping to garner a valuation significantly larger than $1 billion when it IPOs, according to Reuters.

Select investors: Sequoia, Emergence Capital Partners, Horizons Ventures

Data management company Rubrik co-founder and CEO Bipul Sinha.

Data management company Rubrik has quietly made moves indicative of an impending IPO. The startup, which provides data backup and recovery services for businesses across cloud and on-premises environments, hired former Atlassian chief financial officer Murray Demo as its CFO earlier this year, as well as its first chief legal officer, Peter McGoff. Palo Alto-based Rubrik was valued at over of $1 billion with a $180 million funding round in 2017. The company has raised nearly $300 million to date.

Select investors: Lightspeed Venture Partners, Greylock, Khosla Ventures

Medallia, a customer experience management platform that’s nearly two decades old, may finally become a public company in 2019. The San Mateo-based company, which has been rumored to be planning an IPO for several years, hired a new CEO this year and reported $250 million in GAAP revenue for the year ending Jan. 31, 2018, according to Forbes. Medallia hasn’t raised capital since 2015, when it secured a $150 million funding deal at a $1.2 billion valuation. It has raised a total of just over $250 million.

Select investor: Sequoia

Powered by WPeMatico

America’s mayors have spent the past nine months tripping over each other to curry favor with Amazon.com in its high-profile search for a second headquarters.

More quietly, however, a similar story has been playing out in startup-land. Many of the most valuable venture-backed companies are venturing outside their high-cost headquarters and setting up secondary hubs in smaller cities.

Where are they going? Nashville is pretty popular. So is Phoenix. Portland and Raleigh also are seeing some jobs. A number of companies also have a high number of remote offerings, seeking candidates with coveted skills who don’t want to relocate.

Those are some of the findings from a Crunchbase News analysis of the geographic hiring practices of U.S. unicorns. Since most of these companies are based in high-cost locations, like the San Francisco Bay Area, Boston and New York, we were looking to see if there is a pattern of setting up offices in smaller, cheaper cities. (For more on survey technique, see Methodology section below.)

Here is a look at some of the hotspots.

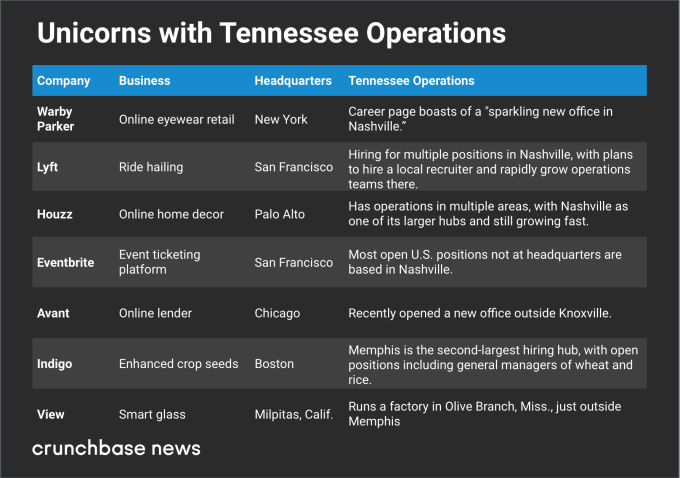

One surprise finding was the prominence of Nashville among secondary locations for startup offices.

We found at least four unicorns scaling up Nashville offices, plus another three with growing operations in or around other Tennessee cities. Here are some of the Tennessee-loving startups:

When we referred to Nashville’s popularity with unicorns as surprising, that was largely because the city isn’t known as a major hub for tech startups or venture funding. That said, it has a lot of attributes that make for a practical and desirable location for a secondary office.

Nashville’s attractions include high quality of life ratings, a growing population and economy, mild climate and lots of live music. Home prices and overall cost of living are also still far below Silicon Valley and New York, even though the Nashville real estate market has been on a tear for the past several years. An added perk for workers: Tennessee has no income tax on wages.

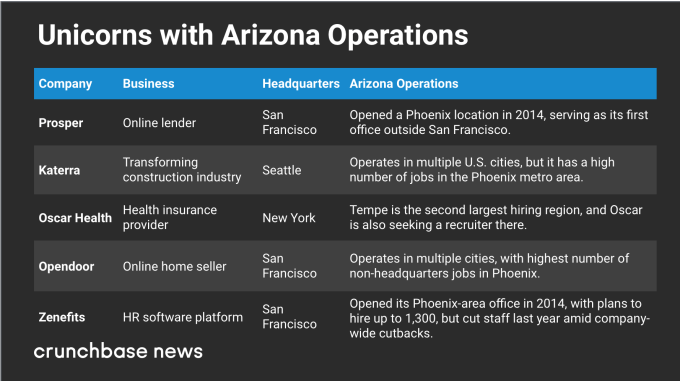

Phoenix is another popular pick for startup offices, particularly West Coast companies seeking a lower-cost hub for customer service and other operations that require a large staff.

In the chart below, we look at five unicorns with significant staffing in the desert city:

Affordability, ease of expansion and a large employable population look like big factors in Phoenix’s appeal. Homes and overall cost of living are a lot cheaper than the big coastal cities. And there’s plenty of room to sprawl.

One article about a new office opening also cited low job turnover rates as an attractive Phoenix-area attribute, which is an interesting notion. Startup hubs like San Francisco and New York see a lot of job-hopping, particularly for people with in-demand skill sets. Scaling companies may be looking for people who measure their job tenure in years rather than months.

Nashville and Phoenix aren’t the only hotspots for unicorns setting up secondary offices. Many other cities are also seeing some scaling startup activity.

Let’s start with North Carolina. The Research Triangle region is known for having a lot of STEM grads, so it makes sense that deep tech companies headquartered elsewhere might still want a local base. One such company is cybersecurity unicorn Tanium, which has a lot of technical job openings in the area. Another is Docker, developer of software containerization technology, which has open positions in Raleigh.

The Orlando metro area stood out mostly due to Robinhood, the zero-fee stock and crypto trading platform that recently hit the $5 billion valuation mark. The Silicon Valley-based company has a significant number of open positions in Lake Mary, an Orlando suburb, including HR and compliance jobs.

Portland, meanwhile, just drew another crypto-loving unicorn, digital currency transaction platform Coinbase. The San Francisco-based company recently opened an office in the Oregon city and is currently in hiring mode.

But you don’t have to be anywhere in particular to score jobs at many fast-growing startups. A lot of unicorns have a high number of remote positions, including specialized technical roles that may be hard to fill locally.

GitHub, which makes tools developers can use to collaborate remotely on projects, does a particularly good job of practicing what it codes. A notable number of engineering jobs open at the San Francisco-based company are available to remote workers, and other departments also have some openings for telecommuters.

Others with a smattering of remote openings include Silicon Valley-based cybersecurity provider CrowdStrike, enterprise software developer Apttus and also Docker.

Of course, not every unicorn is opening large secondary offices. Many prefer to keep staff closer to home base, seeking to lure employees with chic workplaces and lavish perks. Other companies find that when they do expand, it makes strategic sense to go to another high-cost location.

Still, the secondary hub phenomenon may offer a partial antidote to complaints that a few regions are hogging too much of the venture capital pie. While unicorns still overwhelmingly headquarter in a handful of cities, at least they’re spreading their wings and providing more jobs in other places, too.

For this analysis, we were looking at U.S. unicorns with secondary offices in other North American cities. We began with a list of 125 U.S.-based companies and looked at open positions advertised on their websites, focusing on job location.

We excluded job offerings related to representing a local market. For instance, a San Francisco company seeking a sales rep in Chicago to sell to Chicago customers doesn’t count. Instead, we looked for openings for team members handling core operations, including engineering, finances and company-wide customer support. We also excluded secondary offices outside of North America.

Additionally, we were looking principally for companies expanding into lower-cost areas. In many cases, we did see companies strategically adding staff in other high-cost locations, such as New York and Silicon Valley.

A final note pertains to Austin, Texas. We did see several unicorns based elsewhere with job openings in Austin. However, we did not include the city in the sections above because Austin, although a lower-cost location than Silicon Valley, may also be characterized as a large, mature technology and startup hub in its own right.

Powered by WPeMatico