credit

Auto Added by WPeMatico

Auto Added by WPeMatico

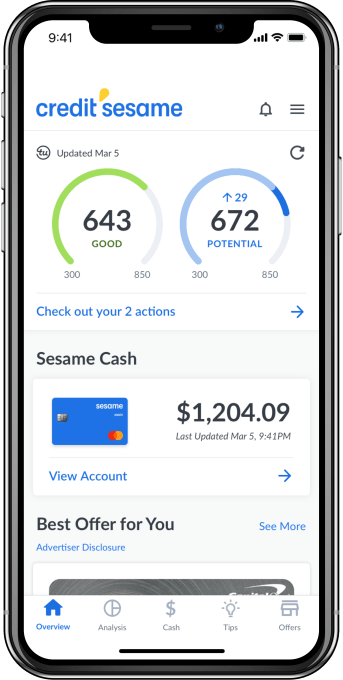

Credit Sesame is getting into digital banking. The credit and loans company, first launched at TechCrunch Disrupt in 2010, has since grown to 15 million registered users and, in 2016, achieved profitability. To date, its focus has been on helping consumers achieve financial health by taking steps to consolidate debt and raise their credit score. Now, it’s expanding to include digital banking, but with the goal of using its better understanding of its banking customers’ finances to better personalize its credit improvement recommendations.

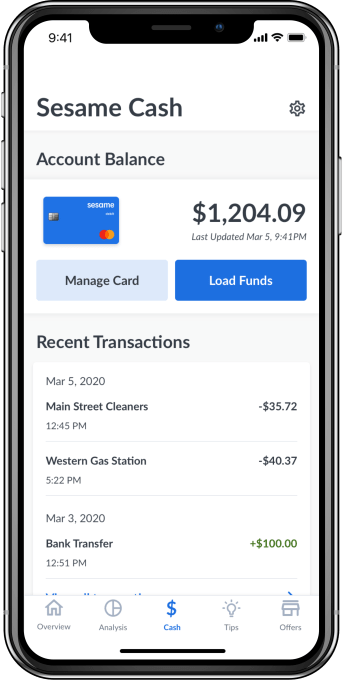

The new service, Sesame Cash, has many features found in other challenger banking apps, like a general lack of fees, real-time notifications, an early payday option, free access to a sizable ATM network, in-app debit card management and more. Specifically, Credit Sesame says it won’t charge monthly fees or overdraft fees, and it provides free access to more than 55,000 ATMs and a no-fee debit card from Mastercard.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

Other features also differentiate Sesame Cash from rival challenger banks, including built-in access to view your daily credit score and a system that rewards consumers with cash incentives — up to $100 per month — for credit score improvements. The banking app includes $1 million in credit and identity theft protection, as well.

In the months following its launch, the company is planning to introduce a smart bill pay service that manages cash to improve credit and lower interest rates on credit balances, plus an auto-savings feature that works by rounding up transactions, a rewards program for everyday purchases and other smart budgeting tools.

“Through the use of advanced machine learning and AI, we’ve helped millions of consumers improve and manage their credit. However, we identified the disconnect between consumers’ cash and credit—how much cash you have, and how and when you use your cash has an impact on your credit health,” said Adrian Nazari, Credit Sesame Founder and CEO, in a statement. “With Sesame Cash, we are now bridging that gap and unlocking a whole new set of benefits and capabilities in a new product category. This underscores our mission and commitment to innovation and financial inclusion, and the importance we place in working with partners who share the same ethos,” he added.

Credit Sesame today caters to consumers interested in bettering their credit. The company says 61% of its members see credit score improvements within their first six months, and 50% see scores improve by more than 10 points during that time. Indeed, 20% see their score improve by more than 50 points during the first six months.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

Credit Sesame is a smaller version of Credit Karma, which was recently acquired by Intuit for $7 billion. Since then, it has been rumored to be another potential acquisition target for Intuit, if it didn’t proceed to go public. The banking service would make Credit Sesame more attractive to a potential acquirer, if that’s the case, as it would offer something Credit Karma did not.

The company says Sesame Cash bank accounts are held with Community Federal Savings Bank, Member FDIC.

The banking service will initially be made available to existing customers, before becoming available to the general public. The Credit Sesame mobile app is a free download for iPhone and Android.

Powered by WPeMatico

I work every day with company founders who are grappling with the challenges of driving business growth while keeping their finances on an even keel. One topic we often discuss is how to take advantage of debt to drive business growth — without it turning into a problem.

In my experience, debt can serve as a valuable piece of a company’s capital structure. The key is to use debt for the right purposes and to understand the implications of doing so. For example, short-term loans (one to two-year terms) are useful for financing receivables and inventory to help manage cash flow. These working capital facilities have attractive interest rates (often in the 5% range) and are well understood by the lending community.

By contrast, mezzanine loans (usually three to five-year terms) are better suited to provide the flexibility and runway needed to prove out certain initiatives prior to securing an equity investment or a liquidity event. These loans tend to have limited covenants, are not secured by specific working capital assets and are junior to the working capital loans. Given their higher-risk profile, they are more expensive than short-term loans, with lenders typically targeting a return of 15% to 20%, split between a current pay interest rate of 10%+ and expected stock appreciation from the receipt of warrant coverage.

Regardless of the type of debt a company takes on, there are certain principles to consider to keep the debt from threatening the success of the business. Should you decide to take on debt, understand the implications and consider the following five rules:

Powered by WPeMatico

After growing its lending business in West Africa, emerging markets credit startup Migo is expanding to Brazil on a $20 million Series B funding round led by Valor Capital Group.

The San Franicso-based company — previously branded Mines.io — provides AI-driven products to large firms so those companies can extend credit to underbanked consumers in viable ways.

That generally means making lending services to low-income populations in emerging markets profitable for big corporates, where they previously were not.

Founded in 2013, Migo launched in Nigeria, where the startup now counts fintech unicorn Interswitch and Africa’s largest telecom, MTN, among its clients.

Offering its branded products through partner channels, Migo has originated more than 3 million loans to over 1 million customers in Nigeria since 2017, according to company stats.

“The global social inequality challenge is driven by a lack of access to credit. If you look at the middle class in developed countries, it is largely built on access to credit,” Migo founder and CEO Ekechi Nwokah told TechCrunch.

“What we are trying to do is to make prosperity available to all by reinventing the way people access and use credit,” he explained.

Migo does this through its cloud-based, data-driven platform to help banks, companies and telcos make credit decisions around populations they previously may have bypassed.

These entities integrate Migo’s API into their apps to offer these overlooked market segments digital accounts and lines of credit, Nwokah explained.

“Many people are trying to do this with small micro-loans. That’s the first place you understand risk, but we’re developing into point of sale solutions,” he said.

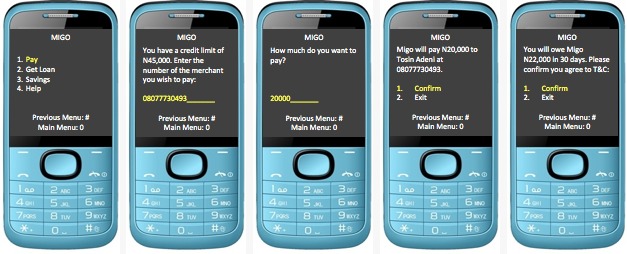

Migo’s client consumers can access their credit lines and make payments by entering a merchant phone number on their phone (via USSD) and then clicking on “Pay with Migo.” Migo can also be set up for use with QR codes, according to Nwokah.

He believes structural factors in frontier and emerging markets make it difficult for large institutions to serve people without traditional credit profiles.

“What makes it hard for the banks is its just too expensive,” he said of establishing the infrastructure, technology and staff to serve these market segments.

Nwokah sees similarities in unbanked and underbanked populations across the world, including Brazil and African countries such as Nigeria.

“Statistically, the number of people without credit in Nigeria is about 90 million people and its about 100 million adults that don’t have access to credit in Brazil. The countries are roughly the same size and the problem is roughly the same,” he said.

On clients in Brazil, Migo has a number of deals in the pipeline — according to Nwokah — and has signed a deal with a big-name partner in the South American country of 210 million, but could not yet disclose which one.

Migo generates revenue through interest and fees on its products. With lead investor Valor Capital Group, Velocity Capital and The Rise Fund joined the startup’s $20 million Series B.

Increasingly, Africa — with its large share of the world’s unbanked — and Nigeria — home to the continent’s largest economy and population — have become proving grounds for startups looking to create scalable emerging market finance solutions.

Migo could become a pioneer of sorts by shaping a fintech credit product in Africa with application in frontier, emerging and developed markets.

“We could actually take this to the U.S. We’ve had discussions with several partners about bringing the technology to the U.S. and Europe,” said founder Ekechi Nwokah. In the near-term, though, Migo is more likely to expand to Asia, he said.

Powered by WPeMatico

Last week, when the popular payments startup Stripe made some waves with its first move into money lending through the launch of Stripe Capital, we reported that the company was also soon going to be launching a credit card. Now, that news is official. Today, the company is doubling down on financing with the launch of corporate cards for business customers.

Announced officially today to coincide with the company’s developer event Stripe Sessions, the Stripe Corporate Card — as the product is officially called — is a Visa that will be open to businesses that are incorporated in the U.S., although they can operate elsewhere.

Notably, users are expected to pay their balance in full each month, so for now there is no interest rate, or fee, to use the card, with Stripe making its money by way of the interchange fee that comes with every transaction using the card.

“We’re not freezing cards based on late or no payments,” Cristina Cordova, the business lead overseeing the launch, said in an interview. “A pretty common reason for non-payment is that a person switched bank accounts and forgot to update the information. But we think we’ll have fewer problems because we have banking information for accepting revenue, by way of our payments business.”

The move is another major step ahead for Stripe as it continues to diversify its business and bring on more financial products to become a one-stop shop for e-commerce and other companies for all the transactions they might need to make in the course of their lives. It is a little ironic that it’s taken years for credit cards to get added into the mix, considering Stripe’s earliest homepages and marketing efforts were built around the design of a credit card (a reference to taking payments online, not issuing credit, of course).

In any case, the list of products now offered by Stripe is long — longer, you might say, than it takes to incorporate a Stripe service into a developer workflow. In addition to its API-based flagship payments product — which is available as a direct service or, via Stripe Connect, for third parties via marketplaces and other platforms — it offers billing and invoicing, in-person payment services (via Terminal), business analytics, fraud prevention on transactions (Radar), company incorporation (Atlas) and a range of content around business strategy.

Some of these Stripe products are free to use, and some come at a price: The main point for offering them together is to build more engagement and loyalty from customers to keep them from migrating to other services. In that regard, credit cards are a cornerstone of how businesses operate, to handle day-to-day expenses in a more accountable way, and this is an area that is already well-served by others, including startups like Brex but also a plethora of challenger and traditional banks. So as much as anything else, this is a clear move to help stave off competition.

At the same time, it underscores how Stripe is leveraging the huge amount of data that it has amassed about its users and payments on the platform: It’s not just about enabling single services, but about using the byproducts of those services — data — to put fuel into new products.

Today, to underscore its global ambitions in that regard, Stripe is adding some expansions to several of its existing products. For example, it will now allow businesses to make payouts in local currencies in 45 countries (an important detail, for example, for marketplaces and network-based companies like ridesharing businesses).

The credit card product will follow a model similar to that of Stripe Capital. As with the lending product, there is a single bank issuing the credit and the card. Amber Feng, head of financial infrastructure for Stripe, confirmed to me that it is actually the same bank that’s providing the cash behind Stripe Capital. Stripe is still declining to name the bank itself, but hints that we may hear more about it soon, which leads me to wonder what news might be coming next.

(Funding perhaps would make sense? The company has raised a whopping $785 million to date and has a valuation of $22.5 billion at the moment. Given that Stripe has made indications that a public listing is not on the cards soon, that might imply, with the launch of these new financing products, that more capital might be raised soon.)

Also similar to Stripe Capital, the underwriting of the card is based on Stripe data. That is to say, business users are verified and approved based on turnover (revenues) as measured by the Stripe payments platform itself; and in cases where applicants are “pre-revenue,” they can be evaluated based on other data sources. For example, if they have used Stripe Atlas to incorporate their businesses, the paperwork supplied for that is used by Stripe to vet the customer’s suitability for a credit card.

Notably, the cards will be delivered in the spirit of instant gratification: If you are applying and get approved, you can within minutes download a virtual card to your Apple Wallet as you await the physical card to arrive in the post.

Stripe is big on data in its own business, and it’s bringing some of that into this product with spending controls that can be set by person and by category; real-time expense reporting by way of texts; rewards of 2% back on spending in the business’s most-used categories; and integration with financial software like QuickBooks and Expensify.

Powered by WPeMatico

Andreessen Horowitz <3 Latin American startups.

Latin America is the only region outside of the U.S. where the venture firm is routinely investing capital, and it just made another commitment, doubling down on its early-stage support for the point-of-sale lending startup ADDI.

ADDI picked up $12.5 million in new financing in April of this year as the company looks to expand its lending services online.

For an American audience, the closest corollary to what ADDI is up to is likely Affirm, the point-of-sale lender that’s raised a ton of cash and come in for some (valid) criticism for its basic business model.

Like Affirm, ADDI lets its borrowers apply for credit at the moment of purchase. The company likens its service to the layaway and credit plans that already exist in Colombia — but involve pretty onerous requirements to use. Company co-founder Santiago Suarez and Andreessen Horowitz general partner Angela Strange both commented on how, in some cases, Colombian shoppers have to have three people vouch for a borrower before a store will issue credit or agree to a layaway plan.

The difference between an ADDI loan — or any loan — and layaway is that an installment payment plan doesn’t charge interest (and even with the fees that installment plans do charge, they are often still cheaper than taking out a loan).

But financial products are coming for consumers in Latin America whether those buyers like it or not — and for the most part, it seems they do like it.

Historically, only the wealthiest clientele in Latin America received anything resembling the kinds of financial products that are more widely available in the United States, according to Strange. And the investment in ADDI is just part of her firm’s thesis in trying to make more services more broadly available in a region where a technological transformation is creating unprecedented opportunities for challengers.

That assessment is what drew Santiago Suarez back to Latin America only two years ago. A former executive at Lending Club who previously had worked as the head of New Product Development and Emerging Services at J.P. Morgan, Suarez saw the tremendous growth happening in Latin America and returned to Colombia to see if he could bring some much needed services to his home country.

Suarez partnered with his childhood friend, Elmer Ortega, who was working as the chief technology officer of the local hedge fund where he had previously been employed as a derivatives trader before learning how to code.

Together, the two men, who had known each other since they were five years old, set out to transform how credit was offered in retail shops. It’s an industry that Suarez had known well since his parents had owned stores.

“In the U.S. there are all of these gaps that fintech companies are filling,” says Suarez. “But the gaps in Latin America are bigger.”

Suarez and Ortega incorporated the company in September 2018, around the same time they raised $2.3 million from the regional investment firm, Monashees, Andreessen and Village Global . They then raised another $1.5 million in an internal round of financing before closing the most recent funding.

The company offers loans at annual percentage rates ranging from 19.99% to 28.90%. The company started with a digital solution for brick and mortar retailers because 90% of retail in Colombia still happens offline.

Although it’s in its early days, the company has already originated 10,000 borrowers and typically loans out roughly $500 since it launched on February 22, according to Suarez. He declined to comment on the company’s default rate on loans.

Now with 40 employees on staff, the company is looking to bring its lending tool to more e-commerce and physical retailers, according to Suarez. And despite the threat of cyclical political turmoil, Suarez says there’s no better time to be investing in Colombia.

“It’s the most stable country outside of Chile… Way more stable than Brazil, way more stable than Argentina and way more stable than Mexico,” Suarez says. “What we’re looking at is more than cyclical instability… those things go beyond that. Nubank was able to build a multibillion business in the worst political and economic crisis in Brazil’s history. I think Colombia is an incredibly attractive space with a deep talent pool.”

Powered by WPeMatico

This week’s episode of Cribs takes us to free credit and financial management platform Credit Karma. This growing financial startup just put the finishing touches on its new office space in the Phelan – a historic building in downtown San Francisco that also houses Nextdoor and Medium.

This week’s episode of Cribs takes us to free credit and financial management platform Credit Karma. This growing financial startup just put the finishing touches on its new office space in the Phelan – a historic building in downtown San Francisco that also houses Nextdoor and Medium.

The Phelan sits just off of Market Street in San Francisco’s bustling financial district. Read More

Powered by WPeMatico