credit cards

Auto Added by WPeMatico

Auto Added by WPeMatico

When Anik Khan graduated from college, his first job was working on credit cards and business expenses at Accenture. There, he found that someone could bring in a couple of thousand dollars just by having the right credit cards and following the rewards and promotions.

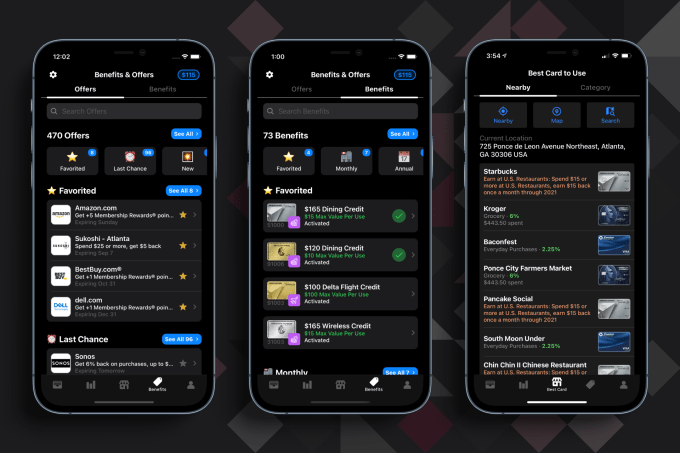

It was back in 2017 when he and David Gao got the idea for his company MaxRewards, a digital wallet app that manages credit cards and automatically activates benefits like rewards, cashback offers and monthly credits. It also makes recommendations at the point of purchase on which card would yield the best reward for that purchase.

Going after the some 83% of Americans that have a credit card, the app version was officially launched in 2019, and now the Atlanta-based company is announcing a $3 million seed round co-led by Dundee Venture Capital and Calano Ventures. Also backing the company are Techstars, Fintech Ventures Fund, Service Provider Capital and Fleetcor president Nick Izquierdo.

Tracking his own credit cards manually prior to MaxRewards, Khan recalled in one year, getting $16,000 in rewards. However, utilizing those benefits was time-consuming and difficult, because the rewards and savings aren’t always made evident by the credit card companies.

“Other companies have tried to do something similar, but the issue is you don’t have the reward information or the offers,” Khan told TechCrunch. “If you were to aggregate this information, you still would have to activate all of these things and use them before they expired.”

Users connect their accounts and when they make a purchase, their location is cross-referenced with the merchant and an algorithm is applied to tell the user which card to use. The average app user has six credit cards.

MaxRewards is free to download and use, and the majority of the app’s functionalities are free. Users who want additional features, like the auto activation or rewards, can join MaxRewards Gold and are given the opportunity to choose their own monthly price — the average is over $25 per month — based on the value they expect to gain, Khan said.

MaxRewards offers and benefits. Image Credits: MaxRewards

Ron Watson, partner at Dundee, said his firm invests in seed-stage companies between the coasts and is interested in consumer and e-commerce companies. Watson said he was impressed with what MaxRewards has been able to do with a team of three. He also relates to the company’s mission, having grown up in a lower, middle-class family that did not frequently go on vacations.

When he got his first job and was suddenly flying everywhere, he recalls building up so many rewards to the point where he was able to go on a vacation to Hawaii and only spend maybe $100, he said.

“I used to put my points into a spreadsheet, but as I got older and had kids, I realized how hard it was for the average person to do that and how important it is to have automation,” Watson said. “I downloaded the app, and on the first day, saved $20.”

The company is often compared to NerdWallet or Mint, but in terms of functionality, Khan said he feels MaxRewards is unique due to its credit card system connectors. Rather than rely on third-party aggregators to discover the rewards, MaxRewards leverages its own proprietary connectors to card systems.

There are hundreds of thousands of offers to be discovered, and consumers are asking for even more features, so Khan decided it was time to go after seed funding. He had raised a small seed, about $200,000, from his time at Techstars, but the new funding will enable him to add to his team of three people. He expects to be at 20 by the end of the year. Khan also wants to accelerate its user acquisition, product improvement and compliance.

Next up, the company is going to automate rewards and savings across additional platforms like debit cards, payment apps and cashback apps, as well as create browser extensions and a web app. Khan also wants to do more on the education side with regard to using credit cards in a smart manner.

Arron Solano, managing partner at Calano, met Khan through Techstars and said he is an advocate for using credit cards in the right way. His firm was looking for a company like MaxRewards.

“During our first call, I remember telling my partner that Anik was a bulldog who knew what he was talking about, especially at that stage,” Solano added. “He had strong team members, his vision lined up well and that checked off a massive box for us. He energized us and showed he could find a market with insanely high ‘super users.’ ”

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

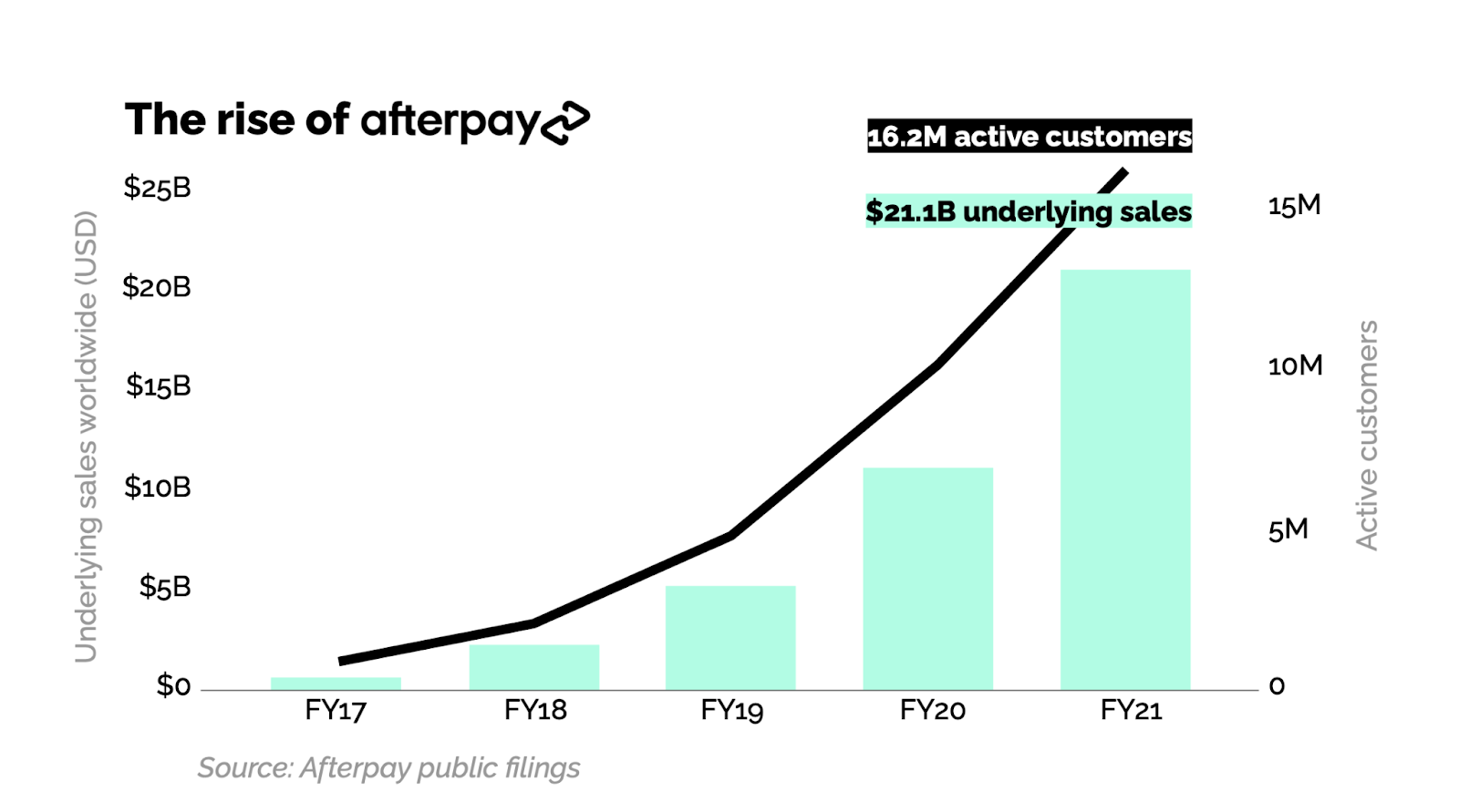

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

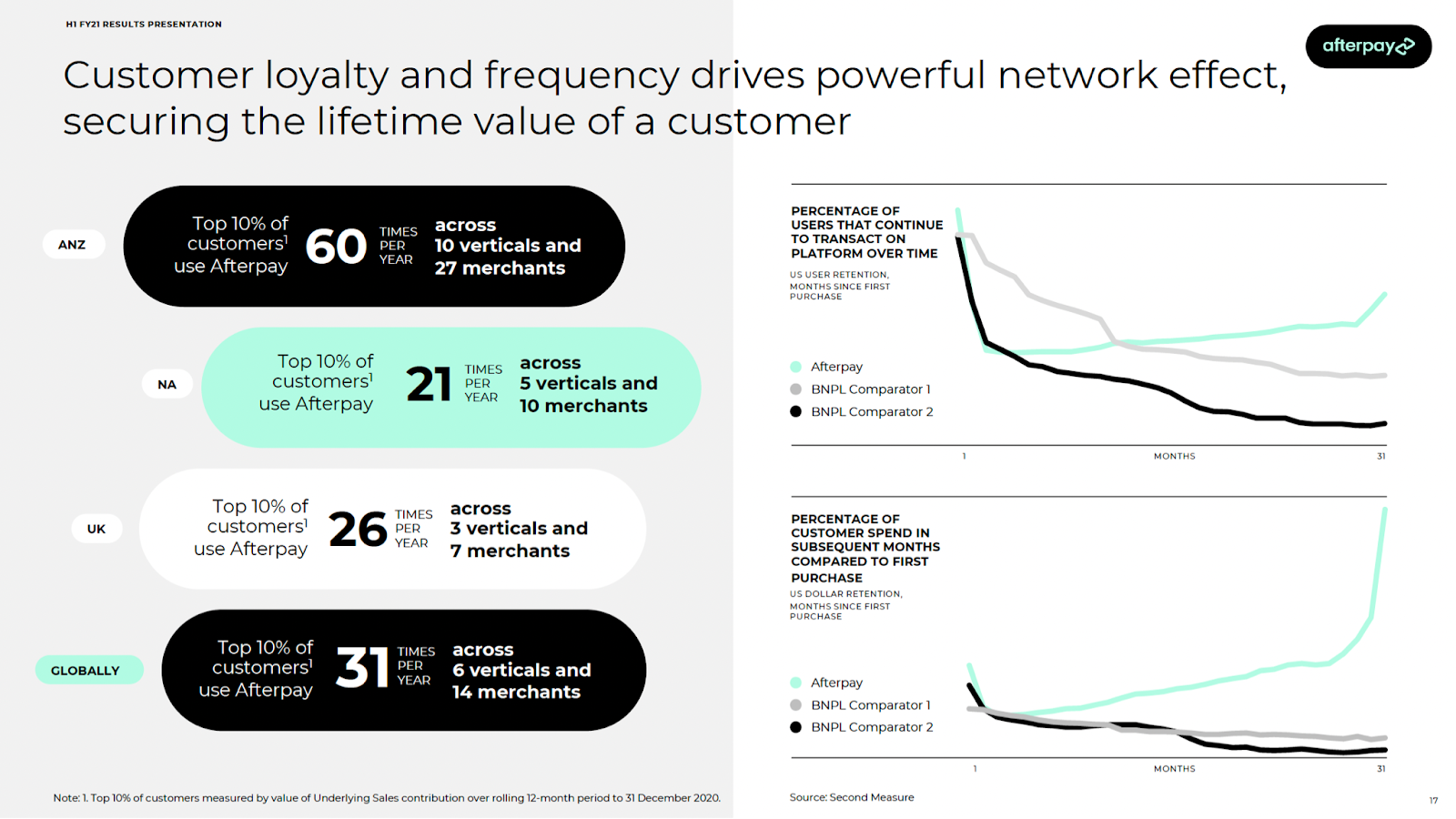

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Cryptocurrency exchange Coinbase is adding a new way to withdraw funds from your Coinbase account. If you’ve added a compatible debit card to your account, you can transfer USD, EUR or GBP to your bank account nearly instantly.

There are some drawbacks, and the main one is that you’ll pay a lot of fees. In the U.S., Coinbase deducts 1.5% from the transaction, or a minimum $0.55 if it’s a small transaction. In the U.K. and Europe, you pay 2% in fees or a minimum fee of £0.45/€0.52, respectively.

You also need to have a compatible card. Not all debit cards support incoming transfers. You need to have a Visa card that supports Visa Fast Funds. In the U.S., you can also use a Mastercard card with Mastercard Send.

It’s hard to know whether your bank or card issuer support those features. The best way to figure it out is probably by adding your card to Coinbase and seeing what Coinbase says.

Coinbase isn’t removing other withdrawal methods. For instance, if you’re looking for a cheaper way to withdraw your funds in Europe, a SEPA bank transfer costs €0.15 per transfer. And Coinbase supports instant SEPA transfers if your bank has enabled that.

The company also lets you link your PayPal account with your Coinbase account. Your funds should hit your PayPal account within a few seconds, and there are no fees on Coinbase’s side.

As you can see, there are many ways to move money from your bank account to your Coinbase account. Some of them are slower than others, some of them are more expensive than others. Crypto-to-crypto transactions are a bit simpler by comparison, as you only need your recipient’s wallet address to send tokens.

Image Credits: Coinbase

Powered by WPeMatico

At a time when more transactions than ever are happening online, payments behemoth Stripe is announcing three new features to continue expanding its reach.

The company today announced that it will now offer card issuing services directly to businesses to let them in turn make credit cards for customers tailored to specific purposes. Alongside that, it’s going to expand the number of accepted local, large card networks to cut down some of the steps it takes to make transactions in international markets. And finally, it’s launching a “revenue optimization” feature that essentially will use Stripe’s AI algorithms to reassess and approve more flagged transactions that might have otherwise been rejected in the past.

Together the three features underscore how Stripe is continuing to scale up with more services around its core payment processing APIs, a significant step in the wake of last week announcing its biggest fundraise to date: $600 million at a $36 billion valuation.

The rollouts of the new products are specifically coming at a time when Stripe has seen a big boost in usage among some (but not all) of its customers, said John Collison, Stripe’s co-founder and president, in an interview. Instacart, which is providing grocery delivery at a time when many are living under stay-at-home orders, has seen transactions up by 300% in recent weeks. Another newer customer, Zoom, is also seeing business boom. Amazon, Stripe’s behemoth customer that Collison would not discuss in any specific terms except to confirm it’s a close partner, is also seeing extremely heavy usage.

But other Stripe users — for example, many of its sea of small business users — are seeing huge pressures, while still others, faced with no physical business, are just starting to approach e-commerce in earnest for the first time. Stripe’s idea is that the launches today can help it address all of these scenarios.

“What we’re seeing in the COVID-19 world is that the impact is not minor,” said Collison. “Online has always been steadily taking a share from offline, but now many [projected] years of that migration are happening in the space of a few weeks.”

Stripe is among those companies that have been very mum about when they might go public — a state of affairs that only become more set in recent times, given how the IPO market has all but dried up in the midst of a health pandemic and economic slump. That has meant very little transparency about how Stripe is run, whether it’s profitable and how much revenues it makes.

But Stripe did note last week that it had some $2 billion in cash and cash reserves, which at least speaks to a level of financial stability. And another hint of efficiency might be gleaned from today’s product news.

While these three new services don’t necessarily sound like they are connected to each other, what they have underpinning them is that they are all building on top of tech and services that Stripe has previously rolled out. This speaks to how, even as the company now handles some 250 million API requests daily, it’s keeping some lean practices in place in terms of how it invests and maximises engineering and business development resources.

The card issuing service, for example, is built on a card service that Stripe launched last year. Originally aimed at businesses to provide their employees with credit cards — for example to better manage their own work-related expenses, or to make transactions on behalf of the business — now businesses can use the card issuing platform to build out aspects of its customer-facing services.

For example, Stripe noted that the first customer, Zipcar, will now be placing credit cards in each of its vehicles, which drivers can use to fuel up the vehicles (that is, the cards can only be used to buy gas). Another example Collison gave for how these could be implemented would be in a food delivery service, for example for a Postmates delivery person to use the card to pay for the meal that a customer has already paid Postmates to pick up and deliver to them.

Collison noted that while other startups like Marqeta have built big businesses around innovative card issuing services, “this is the first time it’s being issued on a self-serving basis,” meaning companies that want to use these cards can now set this up more quickly as a “programmatic card” experience, akin to self-serve, programmatic ads online.

It seems also to be good news for investors. “Stripe Issuing is a big step forward,” said Alex Rampell, general partner at Andreessen Horowitz, in a statement. “Not just for the millions of businesses running on Stripe, but for credit cards as a fundamental technology. Businesses can now use an API to create and issue cards exactly when and where they need them, and they can do it in a few clicks, not a few months. As investors, we’re excited by all the potential new companies and business models that will emerge as a result.”

Meanwhile, the revenue “optimization” engine that Stripe is rolling out is built on the same machine learning algorithms that it originally built for Radar, its fraud prevention tool that originally launched in 2016 and was extended to larger enterprises in 2018. This makes a lot of sense, since oftentimes the reason transactions get rejected is because of the suspicion of fraud. Why it’s taken four years to extend that to improve how transactions are approved or rejected is not entirely clear, but Stripe estimates that it could enable a further $2.5 billion in transactions annually.

One reason why the revenue optimization may have taken some time to roll out was because while Stripe offers a very seamless, simple API for users, it’s doing a lot of complex work behind the scenes knitting together a lot of very fragmented payment flows between card issuers, banks, businesses, customers and more in order to make transactions possible.

The third product announcement speaks to how Stripe is simplifying a bit more of that. Now, it’s able to provide direct links into six big card networks — Visa, Mastercard, American Express, Discover, JCB and China Union Pay, which effectively covers the major card networks in North and Latin America, Southeast Asia and Europe. Previously, Stripe would have had to work with third parties to integrate acceptance of all of these networks in different regions, which would have cut into Stripe’s own margins and also given it less flexibility in terms of how it could handle the transaction data.

Launching the revenue optimization by being able to apply machine learning to the transaction data is one example of where and how it might be able to apply more innovative processes from now on.

While Stripe is mainly focused today on how to serve its wider customer base and to just help business continue to keep running, Collison noted that the COVID-19 pandemic has had a measurable impact on Stripe beyond just boosts in business for some of its customers.

The whole company has been working remotely for weeks, including its development team, making for challenging times in building and rolling out services.

And Stripe, along with others, is also in the early stages of piloting how it will play a role in issuing small business loans as part of the CARES Act, he said.

In addition to that, he noted that there has been an emergence of more medical and telehealth services using Stripe for payments.

Before now, many of those use cases had been blocked by the banks, he said, for reasons of the industries themselves being strictly regulated in terms of what kind of data could get passed across networks and the sensitive nature of the businesses themselves. He said that a lot of that has started to get unblocked in the current climate, and “the growth of telemedicine has been off the charts.”

Powered by WPeMatico

Last week, when the popular payments startup Stripe made some waves with its first move into money lending through the launch of Stripe Capital, we reported that the company was also soon going to be launching a credit card. Now, that news is official. Today, the company is doubling down on financing with the launch of corporate cards for business customers.

Announced officially today to coincide with the company’s developer event Stripe Sessions, the Stripe Corporate Card — as the product is officially called — is a Visa that will be open to businesses that are incorporated in the U.S., although they can operate elsewhere.

Notably, users are expected to pay their balance in full each month, so for now there is no interest rate, or fee, to use the card, with Stripe making its money by way of the interchange fee that comes with every transaction using the card.

“We’re not freezing cards based on late or no payments,” Cristina Cordova, the business lead overseeing the launch, said in an interview. “A pretty common reason for non-payment is that a person switched bank accounts and forgot to update the information. But we think we’ll have fewer problems because we have banking information for accepting revenue, by way of our payments business.”

The move is another major step ahead for Stripe as it continues to diversify its business and bring on more financial products to become a one-stop shop for e-commerce and other companies for all the transactions they might need to make in the course of their lives. It is a little ironic that it’s taken years for credit cards to get added into the mix, considering Stripe’s earliest homepages and marketing efforts were built around the design of a credit card (a reference to taking payments online, not issuing credit, of course).

In any case, the list of products now offered by Stripe is long — longer, you might say, than it takes to incorporate a Stripe service into a developer workflow. In addition to its API-based flagship payments product — which is available as a direct service or, via Stripe Connect, for third parties via marketplaces and other platforms — it offers billing and invoicing, in-person payment services (via Terminal), business analytics, fraud prevention on transactions (Radar), company incorporation (Atlas) and a range of content around business strategy.

Some of these Stripe products are free to use, and some come at a price: The main point for offering them together is to build more engagement and loyalty from customers to keep them from migrating to other services. In that regard, credit cards are a cornerstone of how businesses operate, to handle day-to-day expenses in a more accountable way, and this is an area that is already well-served by others, including startups like Brex but also a plethora of challenger and traditional banks. So as much as anything else, this is a clear move to help stave off competition.

At the same time, it underscores how Stripe is leveraging the huge amount of data that it has amassed about its users and payments on the platform: It’s not just about enabling single services, but about using the byproducts of those services — data — to put fuel into new products.

Today, to underscore its global ambitions in that regard, Stripe is adding some expansions to several of its existing products. For example, it will now allow businesses to make payouts in local currencies in 45 countries (an important detail, for example, for marketplaces and network-based companies like ridesharing businesses).

The credit card product will follow a model similar to that of Stripe Capital. As with the lending product, there is a single bank issuing the credit and the card. Amber Feng, head of financial infrastructure for Stripe, confirmed to me that it is actually the same bank that’s providing the cash behind Stripe Capital. Stripe is still declining to name the bank itself, but hints that we may hear more about it soon, which leads me to wonder what news might be coming next.

(Funding perhaps would make sense? The company has raised a whopping $785 million to date and has a valuation of $22.5 billion at the moment. Given that Stripe has made indications that a public listing is not on the cards soon, that might imply, with the launch of these new financing products, that more capital might be raised soon.)

Also similar to Stripe Capital, the underwriting of the card is based on Stripe data. That is to say, business users are verified and approved based on turnover (revenues) as measured by the Stripe payments platform itself; and in cases where applicants are “pre-revenue,” they can be evaluated based on other data sources. For example, if they have used Stripe Atlas to incorporate their businesses, the paperwork supplied for that is used by Stripe to vet the customer’s suitability for a credit card.

Notably, the cards will be delivered in the spirit of instant gratification: If you are applying and get approved, you can within minutes download a virtual card to your Apple Wallet as you await the physical card to arrive in the post.

Stripe is big on data in its own business, and it’s bringing some of that into this product with spending controls that can be set by person and by category; real-time expense reporting by way of texts; rewards of 2% back on spending in the business’s most-used categories; and integration with financial software like QuickBooks and Expensify.

Powered by WPeMatico

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

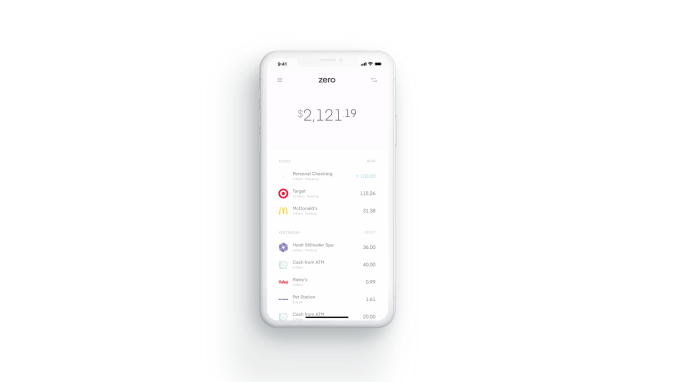

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

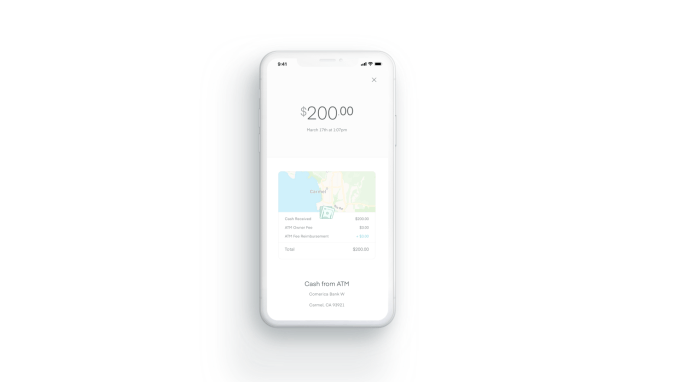

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

The San Francisco-based startup Branch International, which makes small personal loans in emerging markets, has raised $170 million and announced a partnership with Visa to offer virtual, pre-paid debit cards to Branch client networks in Africa, South-Asia and Latin America.

Branch — which has 150 employees in San Francisco, Lagos, Nairobi, Mexico City and Mumbai — makes loans starting at $2 to individuals in emerging and frontier markets. The company also uses an algorithmic model to determine credit worthiness, build credit profiles and offer liquidity via mobile phones.

“We’ll use [the money] to deepen existing business in Africa. Later this year we’ll announce high-yield savings accounts…in Africa,” says Branch co-founder and chief executive Matt Flannery.

The $170 million round from Foundation Capital and its new debit card partner, Visa, will support Branch’s international expansion, which could include Brazil and Indonesia, according to Flannery. Branch launched in Mexico and India within the last year. In Africa, it offers its services in Kenya, Nigeria and Tanzania.

A potential Branch customer

The Branch-Visa partnership will allow individuals to obtain virtual Visa accounts with which to create accounts on Branch’s app. This gives Branch larger reach in countries such as Nigeria — Africa’s most populous country with 190 million people — where cards have factored more prominently than mobile money in connecting unbanked and underbanked populations to finance.

Founded in 2015, Branch started operating in Kenya, where mobile money payment products such as Safaricom’s M-Pesa (which does not require a card or bank account to use) have scaled significantly. M-Pesa now has 25 million users, according to sector stats released by the Communications Authority of Kenya. Branch has more than 3 million customers and has processed 13 million loans and disbursed more than $350 million, according to company stats.

Branch has one of the most downloaded fintech apps in Africa, per Google Play app numbers combined for Nigeria and Kenya, according to Flannery.

Already profitable, Branch International expects to reach $100 million in revenues this year, with roughly 70 percent of that generated in Africa, according to Flannery.

In addition to Visa and Foundation Capital, the $170 Series C round included participation from Branch’s existing investors Andreessen Horowitz, Trinity Ventures, Formation 8, the IFC, CreditEase and Victory Park, while adding new investors Greenspring, Foxhaven and B Capital.

Branch last raised $70 million in 2018. The company’s overall VC haul and $100 million revenue peg register as pretty big numbers for a startup focused primarily on Africa. Pan-African e-commerce startup Jumia, which also announced its NYSE IPO last month, generated $140 million in revenue (without profitability) in 2018.

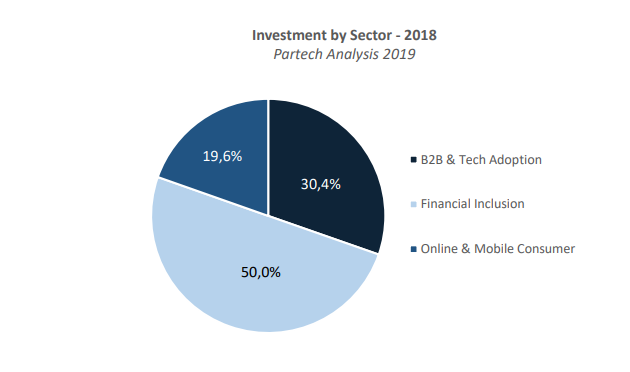

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Startups building financial technologies for Africa’s 1.2 billion population have gained the attention of investors. As a sector, fintech (or financial inclusion) attracted 50 percent of the estimated $1.1 billion funding to African startups in 2018, according to Partech.

Branch’s recent round and plans to add countries internationally also tracks a trend of fintech-related products growing in Africa, then expanding outward. This includes M-Pesa, which generated big numbers in Kenya before operating in 10 countries around the world. Nigerian payments startup Paga announced its pending expansion in Asia and Mexico late last year. And payment services such as Kenya’s SimbaPay have also connected to global networks like China’s WeChat.

Powered by WPeMatico

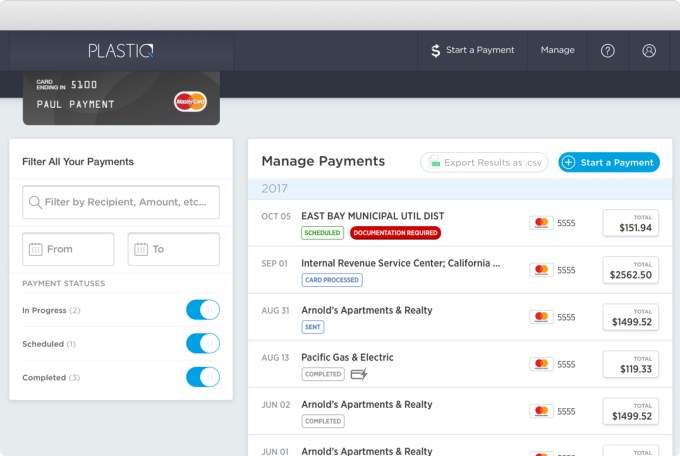

“I wasn’t asking to pay in Bitcoin!” Plastiq CEO and co-founder Eliot Buchanan recalls with a laugh. “I went to pay part of my tuition at Harvard and I was told that they didn’t (and never would) accept credit cards. It was inconvenient and seemed odd. Credit cards had been around for 50 years.” That set off the a light bulb in his head. “Why couldn’t I use a credit card to pay for this important bill? So, I set out to solve my own problem.”

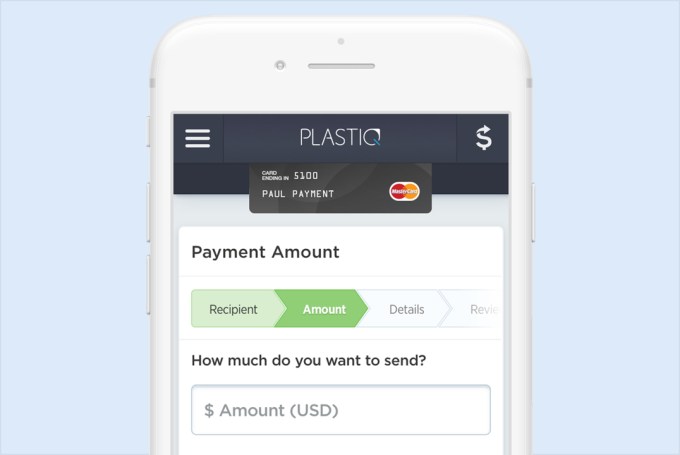

Whether you’re trying to pay your rent or tuition on credit, or you have a business and want to invest in a new opportunity or get a better rate by paying vendors up front, Plastiq can help. For a flat 2.5 percent fee, you pay Plastiq through your credit card, and it issues the proper wire transfer, check or deposit for up to $500,000, or even more, on your behalf to whomever you owe.

Now with more than 1 million clients, growth-stage VCs are taking notice. Kleiner Perkins has just led a $27 million Series C for Plastiq with partner Ilya Fushman joining the board. A source says the raise that also comes from DST Global between doubles and triples Plastiq’s valuation over its 2017 Series B-1 rounds of $11 million and $16 million. Now with $73 million in total funding, it plans to add 100 people to its current team of 60, while building out its small business product and bank partnerships.

“As tens of thousands of business owners started using Plastiq actively for billions of dollars in payments, we realized we had this incredible opportunity to serve as the hub/platform on which they (SMBs) could run all their payments. The very fabric of America’s economy — and certainly much of the world — is run by rising or aspiring small business owners,” Buchanan tells me. He says that’s “the main reason that seeded this Kleiner financing and our renewed vision to ‘accelerate how small businesses grow.’ [Helping people pay with credit cards] is merely the entry point to a much broader play where we are central to how a small business runs.”

For example, if a small business wants to ramp up production of something it’s selling, it’d typically have to pay up front for manufacturing, but wait months until the stuff is shipped and sold to recoup its investment. That can put a major squeeze on the company’s operating capital. With Plastiq, the business can pay with credit up front so they don’t have to worry about being in danger of running out of money in the meantime. Plastiq also lets businesses accept credit card payments, which can win them favor with partners.

Plastiq co-founders (from left): Eliot Buchanan and Dan Choi

Specialty medical clinic chain Metro Vein pays vendors who don’t take credit with Plastiq instead. “I was able to invest in a new line of business that has enabled me to more than double our revenues in the last 10 months,” said CEO Dmitri Ivanov. And thanks to tax write-offs, business users of Plastiq can push its realized fee down to 2 percent.

Buchanan claims Plastiq doesn’t have any direct competitors that allow SMBs to pay for all their bills via credit. It does carry platform risk, though. “Like any payments business, we rely heavily on Visa, MasterCard and American Express. A challenge or risk factor is that you’re relying on very large companies that are very successful. You have to learn to work hand in hand with those partners instead of ‘disrupt them.’” He says Plastiq’s relationships with them are positive right now since it’s driving new revenue for them and helping their customers spend in new areas.

There’s also the risk that people misuse Plastiq to procrastinate on actually paying their personal bills or get in over their head investing in their business. But Plastiq’s new board member Fushman calls the service “this elegant way for businesses to tap into credit they’ve been issued but they haven’t been able to utilize before.” For many who are happy to pay though just need some time and flexibility, Plastiq can pitch in.

Powered by WPeMatico

Birch Finance, a TechCrunch Disrupt 2016 Battlefield alum, has raised a $1 million seed round from AGP Miami, Kevin Johnson, the former CEO of Ebates and Frank Azor, founder of Alienware. The plan is to grow Birch Finance’s user base and increase its opportunities for monetization. Birch Finance aims to help people make the most of the credit cards in their wallets by telling them… Read More

Birch Finance, a TechCrunch Disrupt 2016 Battlefield alum, has raised a $1 million seed round from AGP Miami, Kevin Johnson, the former CEO of Ebates and Frank Azor, founder of Alienware. The plan is to grow Birch Finance’s user base and increase its opportunities for monetization. Birch Finance aims to help people make the most of the credit cards in their wallets by telling them… Read More

Powered by WPeMatico

You might be enjoying the benefits of a credit card with robust rewards today, but odds are when you were first getting started, it was hard to get even close to a card like that. That’s because, for those just getting started or who have a poor credit history, those cards are generally out of reach — and a lot of them are, Petal co-founder Jason Gross said. That’s why he… Read More

You might be enjoying the benefits of a credit card with robust rewards today, but odds are when you were first getting started, it was hard to get even close to a card like that. That’s because, for those just getting started or who have a poor credit history, those cards are generally out of reach — and a lot of them are, Petal co-founder Jason Gross said. That’s why he… Read More

Powered by WPeMatico