craigslist

Auto Added by WPeMatico

Auto Added by WPeMatico

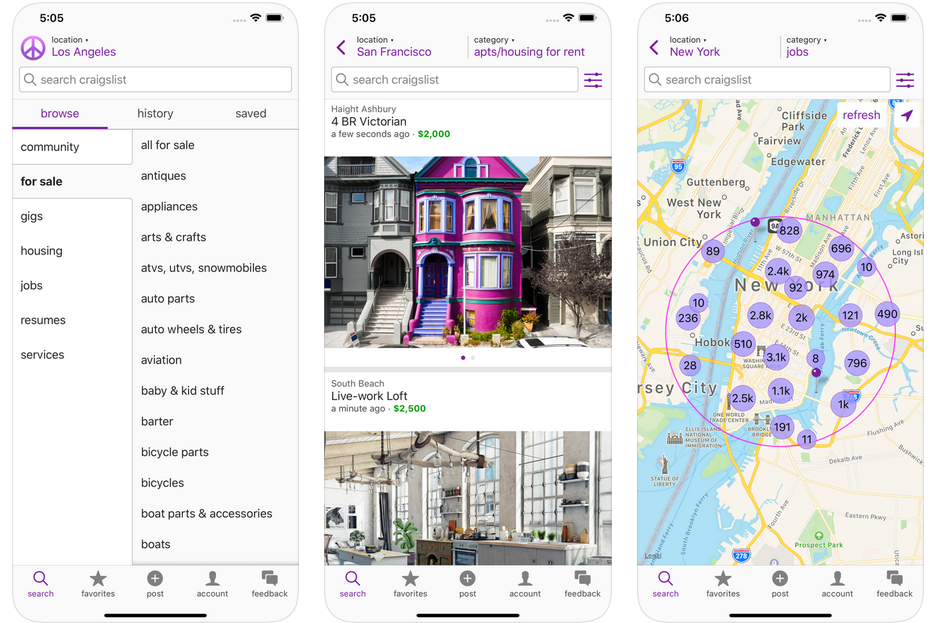

Fancy websites and services come and go, but Craigslist endures. And now one of its main shortcomings is fixed: there’s an official app. Currently available for iOS and in beta for Android, the app provides a true-to-form Craigslist experience: useful, unfussy and anonymous.

There isn’t much to say about the app beyond that it faithfully replicates the website, down to the color scheme. All categories of posts are available to browse or search; you can favorite things, save searches and change the way results look. Different categories have their pertinent settings, so when you look for a car you’ll get odometer, model year and so on the way you do on the site.

No account is required at all to browse listings or contact sellers, and conveniently all their contact info pops up easily, letting you email, text or call as desired.

Obviously the web app is still perfectly serviceable, and some may even prefer it. But it’s nice to have a native app, if only to deter the imitation Craigslist apps that piggyback on the popularity of the original no-frills listings.

The app was released yesterday and is already climbing the charts. Grab it today and start looking for free furniture!

Powered by WPeMatico

The last few decades have produced many successful marketplaces. We went from goods marketplace pioneers such as eBay and Amazon to simple service marketplaces such as Uber, Lyft, Doordash, Upwork, Thumbtack, TaskRabbit, and Fiverr. But why haven’t we seen many successful B2B service marketplaces?

Some would argue that companies such as Upwork, Thumbtack, Fiverr, or TaskRabbit are horizontal B2B marketplaces in the sense that they provide access to suppliers of different services. But while businesses do indeed transact with freelancers on such “horizontal” marketplaces, for most service verticals these are limited-value, one-off transactions. They fail to enable long-term business collaborations.

So, such marketplaces haven’t delivered more valuable services nor introduced a new paradigm for how businesses buy specific services at scale and on an on-going basis. Why is that?

Horizontal services marketplaces don’t provide much value beyond matching clients with quality service providers. In other words, they don’t facilitate collaboration between buyers and suppliers, never mind provide ways for the two parties to collaborate more efficiently over time as they engage in follow-on projects.

In essence, the model these marketplaces were built around is not much different from the likes of Craigslist, which put a convenient UX on traditional classified advertisements.

In their article “What’s Next for Marketplace Startups?,” Andrew Chen and Li Jin found that there aren’t many successful service marketplaces because those offerings are complex, diverse, and difficult to evaluate. It’s challenging to define a successful transaction in a service marketplace because it’s harder to quantify success.

One reason is that several service providers must often work together to complete a single job for a buyer, requiring a complex workflow from end to end. As a result, it’s difficult for marketplaces to not only mediate service delivery but also make it significantly more efficient for buyers and suppliers. If both the buyer and suppliers don’t see a significant efficiency gain other than being initially matched, why would they continue using the marketplace?

(Image via Getty Images / Lidiia Moor)

The $50 billion translation industry is a prime example of complex B2B services marketplaces. On the supply side are roughly 50,000 small agencies around the globe responsible for more than 85% of this $50 billion industry. (Note we are referring to agencies here as suppliers, though they play on both sides.)

On the demand side are businesses that need to translate text from one language into another. Plus about 1,500,000 freelance linguists work in this industry, many of whom are more specialized than professionals in other industries.

Anyone can find and hire a translator on Fiverr or Upwork. Both provide a vast selection of language translators. However, the quality and cost of the translation depends on the translation tools available to the translator as well as their subject expertise.

Neither Fiverr nor Upwork provide computer-aided translation (CAT) and collaborative workflow solutions for users of their platforms. Additionally, neither provides an effective way for all parties to collaborate and continuously improve the efficiency and quality.

But the problem with traditional marketplaces goes even further: Multiple translators and reviewers are usually needed to complete a single job for a customer. Multi-language translation projects are even more complicated. Such projects require multiple service providers and cost estimates, in addition to project management tools.

This is why building a B2B service marketplace is difficult. Service marketplaces must not only connect buyers and suppliers, but also provide tools to enable an efficient and collaborative workflow that reduces wasted time and effort.

In addition to the problems already outlined, traditional marketplaces experience another issue that prevents them from growing and retaining market participants: Buyer and supplier attrition.

Many business services are based on regularly recurring engagements. In some cases, a buyer and a service provider interact daily, requiring a different workflow than gig-marketplaces are built around.

Buyers and suppliers have little motivation to continue interacting on a platform with no workflow automation solutions. They lack a way to improve service efficiency and quality, automate collaboration, payment, paperwork, and other basic processes required for a business.

This is why many traditional marketplaces suffer from slow network effects and high attrition. (A network effect is what happens when a platform, product, or service delivers more value the more it is used.

Think Facebook, eBay, WhatsApp.) Why wouldn’t companies work directly with service providers outside of a marketplace after they were introduced? What incentives keep the service transaction on the marketplace? These are critical questions to answer when building a marketplace.

Traditional marketplaces target broad services, making it nearly impossible to provide workflow solutions for buyers and suppliers. Going forward, successful service marketplaces will be developed relying on an industry-specific SaaS workflow. This will focus buyers and suppliers on longer-term projects and interactions that serve the unique needs of collaborations and transactions in a specific vertical.

Image via Getty Images / OstapenkoOlena

In “The next 10 Years Will Be About Market Networks,” James Currier, Managing Partner at NFX Ventures, defines a new era of service marketplaces, which he calls market networks.

A market network is a platform that combines elements of an n-sided marketplace, a network, and workflow solutions. An n-sided marketplace is one that requires coordination of multiple supply-side parties to provide a complex service for a single buyer.

Market networks enable multiple buyers and suppliers to interact, collaborate, and transact on the same platform. They provide users with industry-specific workflow solutions that enable efficient, ongoing collaboration on long-term projects. This reduces costs and leads to a higher quality of services and increased overall value for all users.

But how do you actually build a successful market-network platform? While the answer to that varies from company to company, here is our approach. We were able to build a market network for the translation industry that combines the components: network, marketplace, and workflow solution.

The first step to building an effective complex market network is to develop a workflow that is easy for users to embrace. It might not seem like much, but this increases productivity by enabling teams to perform tasks that were previously impossible.

Powered by WPeMatico

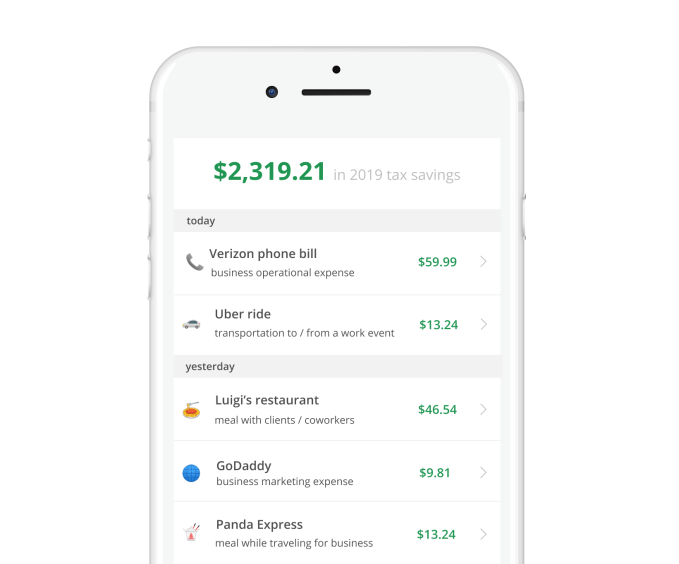

Every year around this time, Uber drivers, Wag dog walkers, Bird scooter chargers, social media influencers and other gig economy workers face the unsightly challenge of paying their taxes.

Companies like Uber and Lyft classify their drivers as independent contractors, which means you aren’t given any benefits and the company doesn’t withhold any of your taxes. This puts gig workers in a tough position come tax day, especially if they aren’t prepared to shell out big sums to the IRS.

Keeper, a startup that’s just graduated from the Y Combinator startup accelerator, is here to make taxes a lot easier for that demographic and to save them as much money as possible.

Founded by childhood buddies and former debate partners Paul Koullick and David Kang, the San Francisco-based company has raised $1.65 million on a $10 million valuation in a round led by Jake Jolis of Matrix Partners.

Keeper co-founders Paul Koullick (left) and David Kang

The pair entered YC this winter with a big idea and little to show for it. Come March, they had developed a full-fledged product and accumulated 200 paying customers. With their first round of funding, they plan to add to their small but growing team and acquire 10,000 customers in the next 18 months.

“There are some companies that are trying to go very broad and trying to cover the whole spectrum of benefits; we’re just trying to go really deep on taxes,” Kang told TechCrunch. “This is a pain point. This is where people are definitely leaving the most money on the table.”

Keeper guesses the average gig worker in the U.S. is overpaying their taxes by more than 20 percent, or about $1,550 for those making more than $25,000 per year. Why? Because these independent contractors aren’t claiming the tax write-offs available to them, like phone bills, car maintenance fees and even a Spotify subscription for drivers.

“If you’re a dog walker, there are so many things you need to be writing off, like your poop bags, your extra leashes, your parking,” Koullick told TechCrunch. “This population needs the guidance of an accountant, but they can’t afford one and we’re trying to create this third option.”

Like a personal accountant, Keeper monitors gig workers’ expenses all year in search of possible tax deductions, saving each user $173 per month on average, it estimates. The startup uses Plaid to follow its customers’ transaction history, and once per day sends a text message asking if there are any tax write-offs to note. Over time, it gets smarter and smarter, keeping the SMS questions to a minimum.

Keeper doesn’t fully file taxes for 1099 workers yet, but will begin offering a quarterly tax filing service in June. Next year, it plans to offer a full-year tax-filing service.

Koullick, Keeper’s chief executive officer, worked in product at Square before joining another startup, called Stride, where he built and scaled Stride Tax, a mileage and expense-tracking app. Kang, for his part, has spent most of his post-graduate career at a trading firm in Chicago, focused on quantitative modeling. The two toyed with a few startup ideas before landing on Keeper’s tax business.

“We wanted to build something that actually mattered to real people,” Koullick explained. “And we wanted to do it in the financial space where we were happy to wade through ugly details and systems on their behalf.”

Keeper isn’t the only recent YC alum focused on the growing gig economy. Another, Catch, sells health insurance, retirement savings plans and tax-withholding services directly to freelancers, contractors or anyone uncovered. Given the rapid rise of Uber and other gig platforms, it’s no wonder YC startups are tapping into the various business opportunities available there.

“We’re willing to tackle some of these topics that are kind of boring and mundane and really intensive,” Kang added. “Like the average person doesn’t want to think about taxes or filling out forms. We saw that as an opportunity for us to step in and be like, hey, we’ll take it.”

Powered by WPeMatico

Unlike 2000 and 2008, everyone in the startup world is expecting a crash to come at any moment. But few are taking concrete steps to prepare for it.

If you’re running a venture-backed startup, you should probably get on that. First, go read RIP Good Times from Sequoia to get a sense for how bad it can get, quickly. Then take a look at the checklist below. You don’t need to build a bomb shelter, yet, but adopting a bit of the prepper mentality now will pay dividends down the road.

The first step in preparing for a coming downturn is making a plan for how you’d get to a point of sustainability. Many startups have been lulled into a false sense of confidence that profit is something they can figure out “later.” Keep in mind, it has to be done eventually and it’s easier to do when the broader economy isn’t crashing around you. There are two complicating factors to keep in mind.

In a downturn, business customers skip investing in capital equipment and new software. Likewise, consumer discretionary spending goes way down. The result is you’ll likely have less revenue than you do now. War-game a variety of scenarios — what you’d do if you lost 20 percent, 50 percent or 80 percent of your revenue, and what decisions would have to be taken to survive.

When a downturn comes, capital markets don’t soften, they seize. Depending on how bad a hypothetical financial crisis got, there’s a good chance that investors would close up their checkbooks and triage. If you aren’t one of your investor’s favorite portfolio companies, there’s a decent chance you may be left in the cold. Don’t even assume you’ll be able to close a down round. Fortunately, showing a plan with a clear path to profitability will allay investors concerns that you’ll need their capital indefinitely and make it more likely you’ll be able to raise.

Planning around these three realities — the need for profits, while experiencing dropping revenue, in a world where capital can’t be had at any valuation — is going to lead to unpleasant conclusions. A dramatically diminished business, major layoffs, and a decisive drop in morale are likely outcomes. Thankfully, you can take steps now to help soften the landing, or if you’re really successful, avoid it entirely.

Getting acquisition costs under control will help you in two ways. First, it’ll lower your burn rate. Chasing growth for growth’s sake is always a short-sighted decision, but especially during the late part of the business cycle. Avoid this even if you’re VC is encouraging it. Second, by carefully analyzing the inputs to your acquisition cost, it will force you to examine the dynamics of your business. It gives you an opportunity to decide if a poorly performing channel or lackluster sales reps are actually smart investments. Even cutting your payback period from 12 months to nine will provide an increased measure of visibility and control.

Instagram took over the web with a team of a dozen. Craigslist is a pillar of the internet with a staff of 40 employees. WhatsApp supported hundreds of millions of daily users with fewer than 50 people. Chances are you need fewer people than you think.

In his new book, Scott Belsky shares an algorithm he used building Behance into a $100M company — automate, automate, then hire. His point was that founders should encourage teams to push hard on improving processes and other labor-saving tools before adding more FTEs.

Don’t institute a hiring freeze or take other actions that might spook the staff, but do send the message that new hires should be the last resort, not the first response to a challenge.

Founders often try to change spending habits, and in turn culture, when it’s too late. Is there a fair bit of business class flying among the executive team? Do your employees stretch your free dinner policy by staying just past the dinner hour to take advantage of free food? At most tech ventures, everyone is truly an owner. Try to help the entire team to internalize that they are spending their own money.

The week the market drops 50 percent is not the week to start a M&A conversation. You should be getting to know the five most likely buyers of your company, now. Find out who the decision makers at each of the companies are and build relationships. Make it a point to catch up with these people at conferences and even consider sending them regular updates about your company’s progress (but not too much data). You’re not running a formal sales process, but helping build up the internal desire to buy your company if the opportunity presents itself. It may not be the exit of your dreams, but it’s nice to have options if you need them.

If you’re coming to a T-juncture regarding office space, you may want to prioritize price and lease flexibility over quality and location. I remember one of our offices at my start-up was a twelve month lease with 6 months free. The landlords were desperate, and so were we!

If you’re in the kind of business that will support annual contracts, figure out a way to offer them. Pre-sell credits to consumers at a discount. More fundamentally, think about how you might be able to adjust your business model so you can get paid before you deliver services. Plenty of viable businesses are asphyxiated by delays in accounts receivable, don’t allow your ambitions to be thwarted by accounting.

One lesson learned in the 2000 bubble was that startups that serve other startups tend to be hit hardest. It’s important to think about how a downturn will impact your customer base. If more than 30 percent of your revenue comes from one industry (perhaps start-ups!), or heaven help you, a single customer, start thinking about managing risk by diversifying your customer base.

Topping up your balance sheet at this point isn’t a bad idea, provided you have the discipline to treat it as a rainy day fund. Communicate this rationale to your investors. It’s also important to use this moment to reflect on valuation. An eye-popping valuation will feel good when you sign the term sheet, but it’s going to feel like a millstone if the economy turns, and the market for blue-chip tech stocks drops precipitously.

Many VCs discourage venture debt. They’ll say “if you need more money, we’ll backstop you.” The problem is when things ugly, they may not be there. Debt providers are a good way to extend the runway. The thing is that it’s best to raise debt capital when you don’t need it. Venture debt can add ⅓ to ½ of additional capital to some funding rounds with minimal dilution and relatively modest interest rates. Do note that when things get bad, some debt funds can get aggressive so do your homework before taking the notes.

It’s tough to predict the top of the market. CNN, Time, The Atlantic, The Wall Street Journal, and many others argued Facebook paying $1 billion for Instagram was a sure sign of a bubble — in 2012. Reputable commentators have claimed that we’re in a bubble every year since, see 2013, 2014, 2015, 2016, 2017, and 2018. Going into survival mode in any of those years would have been a serious mistake for most startups.

Still, we’re only two quarters away from marking the longest economic expansion in US history. The good times have got to end at some point. Venture capital is a hell of a drug and withdrawal can be painful. Keep in mind that there’s no correlation between how much a company raised and how well they did on the public markets. If you’re struggling to make your startup’s economics work, read up on dozens of “invisible unicorns” who show that you can get big without relying on outsized amounts of venture capital.

If your house is in order when the downturn hits, you may actually be able to grow through it. As unprepared competitors go out of business, you’ll find that talent is more plentiful and customer acquisition costs plummet. Some of the best companies have been founded and thrived in the worst of times — if you’re prepared.

Powered by WPeMatico

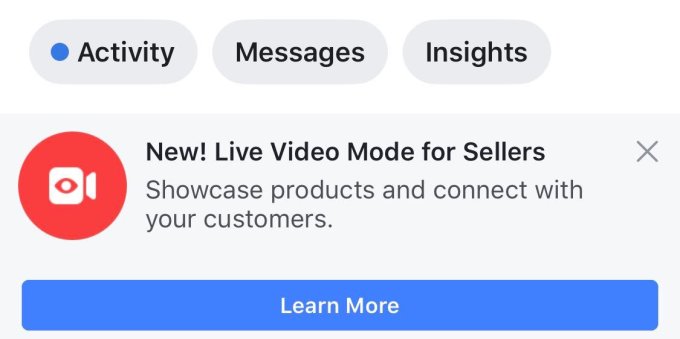

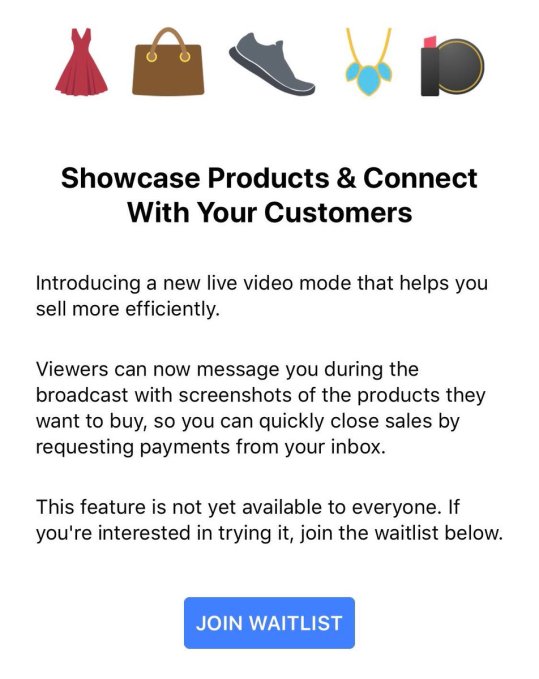

Want to run your own home shopping network? Facebook is now testing a Live video feature for merchants that lets them demo and describe their items for viewers. Customers can screenshot something they want to buy and use Messenger to send it to the seller, who can then request payment right through the chat app.

Facebook confirms the new shopping feature is currently in testing with a limited set of Pages in Thailand, which has been a testbed for shopping features. The option was first spotted by social media and reputation manager Jeff Higgins, and re-shared by Matt Navarra and Social Media Today. But now Facebook is confirming the test’s existence and providing additional details.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

Now it’s running the Live shopping test, which allows Pages to notify fans that they’re broadcasting to “showcase products and connect with your customers.” Merchants can take reservations and request payments through Messenger. Facebook tells me it doesn’t currently have plans to add new partners or expand the feature. But some sellers without access are being invited to join a waitlist for the feature. It also says it’s working closely with its test partners to gather feedback and iterate on the live video shopping experience, which would seem to indicate it’s interested in opening the feature more widely if it performs well.

Facebook doesn’t take a cut of payments through Messenger, but the feature could still help earn the company money at a time when it’s seeking revenue streams beyond News Feed ads as it runs out of space there, Stories take over as the top media form and user growth plateaus. Hooking people on video viewing helps Facebook show lucrative video ads. The more that Facebook can train users to buy and sell things on its app, the better the conversion rates will be for businesses, and the more they’ll be willing to spend on ads. Facebook could also convince sellers who broadcast Live to buy its new Marketplace ad units to promote their wares. And Facebook is happy to snatch any use case from the rest of the internet, whether it’s long-form video viewing or job applications or shopping to boost time on site and subsequent ad views.

Increasingly, Facebook is setting its sights on Craigslist, Etsy and eBay. Those commerce platforms have failed to keep up with new technologies like video and lack the trust generated by Facebook’s real-name policy and social graph. A few years ago, selling something online meant typing up a generic description and maybe uploading a photo. Soon it could mean starring in your own infomercial.

[PostScript: And a Facebook home shopping network could work perfectly on its new countertop smart display Portal.]

Powered by WPeMatico

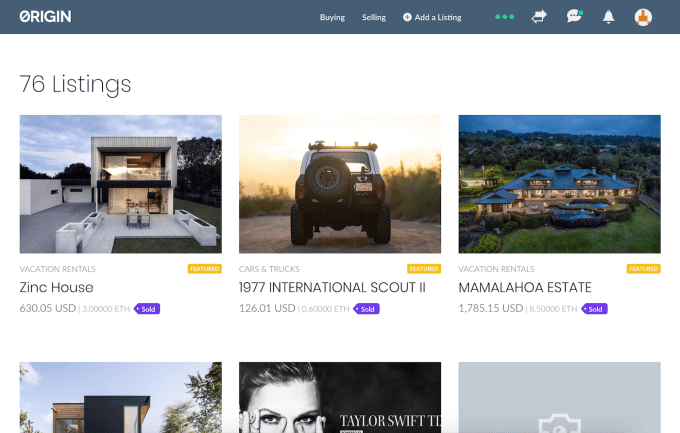

The sharing economy ends up sharing a ton of labor’s earnings with middlemen like Uber and Airbnb, and $38 million-funded Origin wants the next great two-sided marketplace to be decentralized on the blockchain so drivers and riders or hosts and guests can connect directly and avoid paying steep fees that can range up to 20 percent or higher. So today Origin launches its decentralized marketplace protocol on the ethereum mainnet that replaces a central business that connects users and vendors with a smart contract.

“Marketplaces don’t redistribute the profits they make to members. They accrue to founders and venture capitalists,” said Origin co-founder Matt Liu, who was the third product manager at YouTube. “Building these decentralized marketplaces, we want to make them peer-to-peer, not peer-to-corporate-monopoly-to-peer.” When people transact through Origin, it plans to issue them tokens that will let them participate in the governance of the protocol, and could incentivize them to get on these marketplaces early as well as convince others to use them.

Origin’s in-house marketplace DApp

Today’s mainnet beta sees Origin offering its own basic decentralized app that operates like a Craigslist on the blockchain. Users can create a profile, connect their ethereum wallet through services like MetaMask, browse product and service listings, message each other to arrange transactions through smart contracts with no extra fees, leave reviews and appeal disputes to Origin’s in-house arbitrators.

Eventually, with the Origin protocol, developers will be able to quickly build their own sub-marketplaces for specific services like dog walking, house cleaning, ridesharing and more. These developers can opt to charge fees, though Origin hopes the cost-savings from its blockchain platform will let them undercut non-blockchain services. And vendors can offer a commission to any marketplace that gets their listing matched/sold.

It might be years before the necessary infrastructure like login systems and simple wallets make it easy for developers and mainstream users to build and adopt DApps built on Origin. But it has plenty of runway thanks to $3 million in seed token sale funding from Pantera Capital, $6.6 million raised through a Coinlist token sale, plus $26.4 million in traditional venture funding from Pantera Capital, Foundation Capital, Garry Tan, Alexis Ohanian, Gil Penchina, Kamal Ravikant, Steve Jang and Randall Kaplan.

“Marketplaces are at the core of what makes the internet so valuable and useful and the Origin team has one of the most promising blockchain platforms for the new sharing economy — with currency baked in — this could be really disruptive (and one of the best utilizations of the ethereum blockchain),” says Ohanian, the Reddit and Initialized Capital co-founder.

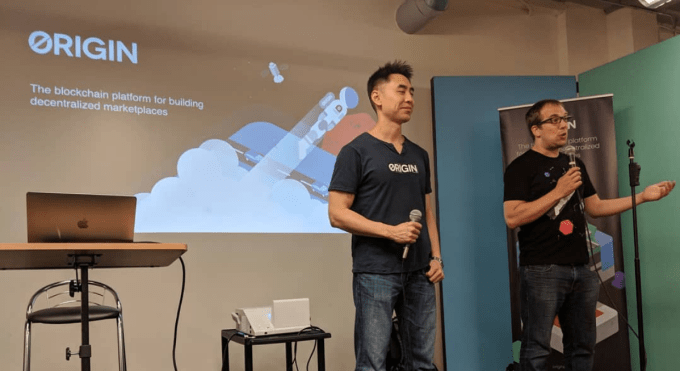

Liu and co-founder Josh Fraser came up with the idea after trying to imagine the downstream effects of ethereum. Liu recalls thinking, “What if we could replace dozens of multi-million and multi-billion-dollar companies with open-source protocols that aren’t owned or controlled by anyone?”

Origin co-founders (from left): Matthew Liu and Josh Fraser

So why would marketplaces want to build on Origin instead of creating their own blockchain or traditional proprietary system? Fraser tells me smart contracts can save money, but that “these individual pieces are incredibly difficult to build,” so he sees Origin as “analogous to Stripe — able to abstract away all the friction of building on the blockchain.” Indeed, 40 marketplaces have already signed letters of intent to build on the protocol.

If Origin reaches critical mass, it could also benefit from the concept of shared network effect. Users only have to sign up once, and can then interact with any marketplace built on Origin. That means new marketplaces that builds on the protocol instantly has a registered user base.

Origin will face some stiff challenges, though. There’ll be a chicken-and-egg problem of getting the first marketplaces signed up before there are users on its self-sovereign identity platform, or getting those users aboard when there’s little for them to do. Liu admits that timing is the startup’s biggest threat. “We believe that decentralized marketplaces are inevitable, but a lot of smart people seem to think we’re too early and that we should be focused on building lower-level infrastructure instead,” the co-founder says. For us, we’d rather be too early than too late.”

There’s also the trouble of leaving actors in a capitalist system to treat each other properly without a centralized authority. If an Uber driver treats you terribly, you can complain and get them kicked off the platform. Even with Origin’s review system, abusers of the system may be able to continue operating. It’s easy to imagine its arbitration service becoming completely overwhelmed with disputes. Luckily, Origin has made some strong hires to tackle these challenges, including Yu Pan, who it says was a PayPal co-founder, former head of Dropbox’s NYC engineering team Cuong Du, and Franck Chastagnol who previously led engineering teams at PayPal, YouTube, Google and Dropbox.

There’s also the trouble of leaving actors in a capitalist system to treat each other properly without a centralized authority. If an Uber driver treats you terribly, you can complain and get them kicked off the platform. Even with Origin’s review system, abusers of the system may be able to continue operating. It’s easy to imagine its arbitration service becoming completely overwhelmed with disputes. Luckily, Origin has made some strong hires to tackle these challenges, including Yu Pan, who it says was a PayPal co-founder, former head of Dropbox’s NYC engineering team Cuong Du, and Franck Chastagnol who previously led engineering teams at PayPal, YouTube, Google and Dropbox.

Origin’s success will all come down to usability. Your average Uber driver or Airbnb host is no blockchain expert. They vend through those apps because it’s easy. Those centralized organizations are also highly incentivized to fulfill transactions quickly and smoothly in ways prohibited by eliminating fees. Origin will have to effectively make the blockchain aspects of its service disappear so all users and vendors know is that they’re paying less or earning more.

Powered by WPeMatico

Twenty months after launching its Craigslist competitor, Marketplace, and relentlessly promoting it with placement in the main navigation bar, Facebook will start earning money off its classifieds section. Facebook today begins testing Marketplace ads in the U.S. that let average users pay to “Boost” their listing to more people through the News Feed. While they’re easy for novices, requiring buyers to only set a budget and how long the ads will run, there are no additional targeting options beyond being shown to age 18+ users in nearby ZIP codes.

Meanwhile, yesterday Facebook announced that it’s launching product ads from businesses that appear within Marketplace. After quietly opening in the U.S. in January and testing in Canada in May, Marketplace ads are now official, and can be bought in those two countries plus New Zealand and Australia. Businesses can extend their existing News Feed, video, Instagram, Messenger and other ad campaigns to Marketplace, and more types of objective-based campaigns will open to the classifieds section soon.

Facebook lets brands show ads within Marketplace

The Boost ads could be a big help if you need to rapidly liquidate your furniture before moving out, or if you’re trying to sell something big at a high price, like Marketplace’s new car, housing, jobs and home services offerings. Yet they seem inefficient, since the lack of targeting means your listing for men’s jewelry might show up to women, or your rock climbing gear ads could show up to senior citizens.

Facebook’s new Boost ads let average users pay to show their Marketplace listings to more people

But Facebook does tell me that ads will be auto-optimized for clicks, so when people start to click your ads, Facebook will show them to people of similar demographics. It will also immediately pause your ad campaign if you mark your item as sold. Boost ads get entered in alongside traditional bids in Facebook’s auction system, which then display what it predicts will be the most appealing ads.

“Many Marketplace sellers have told us that they want the ability to show a listing to more people in their local area, especially if they’re trying to sell it quickly,” Facebook product manager Harshit Agarwal tells TechCrunch. “We’re starting to test a simple way for sellers to boost their listings and help them find a buyer.” For comparison, Craigslist doesn’t run any ads, but charges sellers $5 to $10 for certain product listings for cars and brokered apartments.

One interesting quirk is that Facebook says it won’t allow boosting of listings of political products such as a Bernie Sanders for President t-shirt, as its political advertiser verification and labeling system only works with Pages and not individuals right now.

The Boost ads will only appear to a small percentage of U.S. users and Facebook says it’s too early to know if it will roll them out further. But as the company seems bent on swallowing up every other essential part of the internet, anything that makes Marketplace more useful to sellers and lucrative for the tech giant seems like a good bet for an official launch.

Together, the two formats could unlock new revenue streams for Facebook at a time when it’s starting to run out of ad inventory in the News Feed. The company either needs to open new surfaces like Marketplace to ads, or get people and businesses to pay more to fill its dwindling feed space if it wants to keep Wall Street happy.

Powered by WPeMatico

Why has San Francisco’s startup scene generated so many hugely valuable companies over the past decade?

That’s the question we asked over the past few weeks while analyzing San Francisco startup funding, exit, and unicorn creation data. After all, it’s not as if founders of Uber, Airbnb, Lyft, Dropbox and Twitter had to get office space within a couple of miles of each other.

We hadn’t thought our data-centric approach would yield a clear recipe for success. San Francisco private and newly public unicorns are a diverse bunch, numbering more than 30, in areas ranging from ridesharing to online lending. Surely the path to billion-plus valuations would be equally varied.

But surprisingly, many of their secrets to success seem formulaic. The most valuable San Francisco companies to arise in the era of the smartphone have a number of shared traits, including a willingness and ability to post massive, sustained losses; high-powered investors; and a preponderance of easy-to-explain business models.

No, it’s not a recipe that’s likely replicable without talent, drive, connections and timing. But if you’ve got those ingredients, following the principles below might provide a good shot at unicorn status.

First, lose money until you’ve left your rivals in the dust. This is the most important rule. It is the collective glue that holds the narratives of San Francisco startup success stories together. And while companies in other places have thrived with the same practice, arguably San Franciscans do it best.

It’s no secret that a majority of the most valuable internet and technology companies citywide lose gobs of money or post tiny profits relative to valuations. Uber, called the world’s most valuable startup, reportedly lost $4.5 billion last year. Dropbox lost more than $100 million after losing more than $200 million the year before and more than $300 million the year before that. Even Airbnb, whose model of taking a share of homestay revenues sounds like an easy recipe for returns, took nine years to post its first annual profit.

Not making money can be the ultimate competitive advantage, if you can afford it.

Industry stalwarts lose money, too. Salesforce, with a market cap of $88 billion, has posted losses for the vast majority of its operating history. Square, valued at nearly $20 billion, has never been profitable on a GAAP basis. DocuSign, the 15-year-old newly public company that dominates the e-signature space, lost more than $50 million in its last fiscal year (and more than $100 million in each of the two preceding years). Of course, these companies, like their unicorn brethren, invest heavily in growing revenues, attracting investors who value this approach.

We could go on. But the basic takeaway is this: Losing money is not a bug. It’s a feature. One might even argue that entrepreneurs in metro areas with a more fiscally restrained investment culture are missing out.

What’s also noteworthy is the propensity of so many city startups to wreak havoc on existing, profitable industries without generating big profits themselves. Craigslist, a San Francisco nonprofit, may have started the trend in the 1990s by blowing up the newspaper classified business. Today, Uber and Lyft have decimated the value of taxi medallions.

Not making money can be the ultimate competitive advantage, if you can afford it, as it prevents others from entering the space or catching up as your startup gobbles up greater and greater market share. Then, when rivals are out of the picture, it’s possible to raise prices and start focusing on operating in the black.

You can’t lose money on your own. And you can’t lose any old money, either. To succeed as a San Francisco unicorn, it helps to lose money provided by one of a short list of prestigious investors who have previously backed valuable, unprofitable Northern California startups.

It’s not a mysterious list. Most of the names are well-known venture and seed investors who’ve been actively investing in local startups for many years and commonly feature on rankings like the Midas List. We’ve put together a few names here.

You might wonder why it’s so much better to lose money provided by Sequoia Capital than, say, a lower-profile but still wealthy investor. We could speculate that the following factors are at play: a firm’s reputation for selecting winning startups, a willingness of later investors to follow these VCs at higher valuations and these firms’ skill in shepherding portfolio companies through rapid growth cycles to an eventual exit.

Whatever the exact connection, the data speaks for itself. The vast majority of San Francisco’s most valuable private and recently public internet and technology companies have backing from investors on the short list, commonly beginning with early-stage rounds.

Generally speaking, you don’t need to know a lot about semiconductor technology or networking infrastructure to explain what a high-valuation San Francisco company does. Instead, it’s more along the lines of: “They have an app for getting rides from strangers,” or “They have an app for renting rooms in your house to strangers.” It may sound strange at first, but pretty soon it’s something everyone seems to be doing.

It’s not a recipe that’s likely replicable without talent, drive, connections and timing.

A list of 32 San Francisco-based unicorns and near-unicorns is populated mostly with companies that have widely understood brands, including Pinterest, Instacart and Slack, along with Uber, Lyft and Airbnb. While there are some lesser-known enterprise software names, they’re not among the largest investment recipients.

Part of the consumer-facing, high brand recognition qualities of San Francisco startups may be tied to the decision to locate in an urban center. If you were planning to manufacture semiconductor components, for instance, you would probably set up headquarters in a less space-constrained suburban setting.

While it can be frustrating to watch a company lurch from quarter to quarter without a profit in sight, there is ample evidence the approach can be wildly successful over time.

Seattle’s Amazon is probably the poster child for this strategy. Jeff Bezos, recently declared the world’s richest man, led the company for more than a decade before reporting the first annual profit.

These days, San Francisco seems to be ground central for this company-building technique. While it’s certainly not necessary to locate here, it does seem to be the single urban location most closely associated with massively scalable, money-losing consumer-facing startups.

Perhaps it’s just one of those things that after a while becomes status quo. If you want to be a movie star, you go to Hollywood. And if you want to make it on Wall Street, you go to Wall Street. Likewise, if you want to make it by launching an industry-altering business with a good shot at a multi-billion-dollar valuation, all while losing eye-popping sums of money, then you go to San Francisco.

Powered by WPeMatico

The upcoming Fight Online Sex Trafficking Act, in addition to making Microsoft move to reduce obscenity on its platform, has hit erotica authors on Amazon. After many authors saw their rankings stripped on the Kindle store, essentially reducing their availability and visibility, while forcing others in the romance category to recategorize or get dinged as well.

The Digital Reader followed the changes this week, reporting that “I have seen numerous reports on Facebook, KBoards, and elsewhere that Amazon has adopted a new policy where some romance titles, most notably those titles that Amazon has identified as erotica, have been removed from the Kindle Store best-seller list.” Amazon’s changes began on March 22.

Delisting titles from the Amazon Kindle store essentially buries them completely, leading to massive revenue loss for indie authors. One author received a note from KDP – Kindle Direct Publishing – discussing the changes:

I’m following up concerning some of your books missing their best sellers ranking.

After hearing from our technical team we have confirmed that this is due to a recent update to the filter option for Erotica ebooks.

All adult themed titles will be filtered from the main category sales rank as part of this update. However, you will still continue to keep all of your category rankings. I know this wasn’t the answer you were looking for but appreciate your understanding on this policy.

Please let us know if you have any further questions.

The FOSTA Bill is ostensibly about preventing online sex trafficking and has already caused Craigslist to shut down its online personals. However, it can also be construed as a bill that prevents sexual material of all kinds from receiving ready distribution online, a fact that is giving some big content providers pause. The Digital Reader notes that “the change in policy only affects the main Amazon site, and not other sites like Amazon UK.”

I have reached out to authors and Amazon for further comment.

Powered by WPeMatico

Everyone wants to be the Craigslist killer. In November, Facebook expanded its Marketplace section to include partners’ housing rentals alongside secondhand merchandise, and today the No. 3 three shopping app letgo is doing the same.

Everyone wants to be the Craigslist killer. In November, Facebook expanded its Marketplace section to include partners’ housing rentals alongside secondhand merchandise, and today the No. 3 three shopping app letgo is doing the same.