Covid19

Auto Added by WPeMatico

Auto Added by WPeMatico

India has emerged as one of the fastest growing smartphone markets in the last decade, reporting growth each quarter even as handset shipments slowed or declined elsewhere globally. But the world’s second largest smartphone is beginning to feel the coronavirus heat, too.

The Indian smartphone market grew by a modest 4% year-over-year in the quarter that ended on March 31, research firm Counterpoint said Friday evening. The shipment grew annually in January and February, when several firms launched their smartphones and unveiled aggressive promotional plans.

But in March the shipment saw a 19% year-over-year dip, the firm said. Counterpoint estimated that the smartphone shipments in India will decline by 10% this year, compared to a 8.9% growth in 2019 and 10% growth in 2018.

The research firm also cautioned that India’s lockdown, ordered last month, has severely slowed down the local smartphone industry and it may take seven to eight months to get back on track. Currently, only select items such as grocery products are permitted to be sold in India.

Prachir Singh, Senior Research Analyst at Counterpoint Research, said the COVID-19 impact on India was relatively mild until mid-March. “However, economic activities declined as people save money in expectation of an extended period of uncertainty and an almost complete lockdown. Almost all smartphone manufacturing has been suspended. Further, with the social distancing norms, factories will be running at lower capacities even after the lockdown is lifted,” he said.

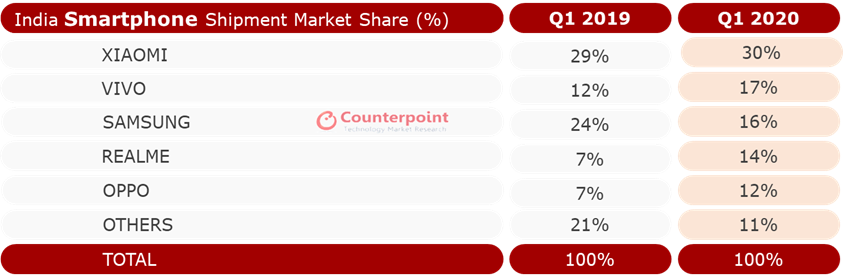

Overall, 31 million smartphone units shipped in India in Q1 2020. Chinese smartphone maker Xiaomi, which has held the tentpole position in what has become its biggest market globally for more than two years, widened its lead to command 30% of the market.

Vivo’s share grew to 17%, up from 12% during the same period last year. Samsung, which once led the Indian market, now sits at the third spot with 16% market share, down from 24% in Q1 2019. Apple maintained its recent momentum and grew by a strong 78% year-over-year in Q1 this year. It now commands 55% of the premium smartphone segment (handsets priced at $600 or above.).

More than 100 smartphone plants in India assemble or produce about 700,000 to 800,000 handsets a day, some of which are exported outside of the country. But the lockdown has halted the production and could cost the industry more than $3 billion to $4 billion in direct loss this year.

“We often draw parallels between India and China. But in China, their factories have adopted automation at various levels, something that is not the case in India,” said Tarun Pathak, a senior analyst at Counterpoint, earlier this week.

China, where smartphone sales declined by 38% annually in February this year, has already started to see recovery. Xiaomi said last month that its phone factories were already operating at more than 80% of their capacity. Globally, smartphone shipment declined by 14% in February, according to Counterpoint.

Powered by WPeMatico

More than six dozen startup founders, venture capitalists and lobby groups in India have requested the government to grant them a “robust relief package” to help combat severe disruptions their businesses face due to the coronavirus outbreak.

In a joint letter to India’s Prime Minister Narendra Modi, startups requested the government to bankroll 50% of their workforce’s salaries for six months, provide interest-free loans from banks, waive rent for three months and offer tax benefits among other things.

“Unfortunately, our startup companies across the nation are inherently young, less resilient and most vulnerable. Many of them face likely devastation during this extraordinary economic downturn. At this dire moment, Indian startups need a robust relief package from the government, lest all our collective efforts of the past few years are in vain,” they wrote.

Among those who have signed the letter include Mohit Bhatnagar, a managing director at Sequoia Capital, which is in advanced stages to close a fresh $1.3 billion fund for India and Southeast Asia, Gaurav Agarwal of online medicine store 1mg, Debjani Ghosh of industry body Nasscom, Karthik Reddy of Blume Ventures, Anand Lunia of India Quotient, Deepinder Goyal of Zomato, and Sriharsha Majety of Swiggy.

Some prominent startup founders and VCs including Vijay Shekhar Sharma of Paytm, and Ritesh Agarwal of Oyo, have also held a meeting with Piyush Goyal, the commerce minister in India, for a similar relief.

“We seek your urgent intervention to help ensure India’s startup ecosystem survives this crisis to emerge as a pillar of growth, employment and innovation to help drive India’s recovery. We need the startup ecosystem to survive in order to help the economy bounce back. We have enclosed herewith our submission for your kind consideration and we look forward to your support in this regard,” the joint letter reads.

The request for bailout comes amid a national lockdown in India that has disrupted countless businesses. New Delhi ordered a 21-day lockdown last month in a bid to curtail the spread of Covid-19.

Earlier this month, ten prominent VC and PE funds in India cautioned startups to brace for the “worst” months ahead.

“Assumptions from bull market financings or even from a few weeks ago do not apply. Many investors will move away from thinking about ‘growth at all costs’ to ‘reasonable growth with a path to profitability.’ Adjust your business plan and messaging accordingly,” they said.

As India, where the economy growth has been slowing for several quarters, scrambles to provide for its 1.3 billion citizens, the letter has drawn some criticism from industry figures.

Disappointed to see many startup leaders & investors that I admire add their names to this shameful letter to the govt asking for bailouts – surely at this time the govt has more important things to worry about than pay “50% of salary bills & contract wage bills paid by startups”

— Sumanth Raghavendra (@sumanthr) April 10, 2020

“I can’t fathom how such a list gets made in a country of more than a billion people who are facing a crisis unlike any they’ve seen before. A significant majority of them daily wage earners who have no financial cushion or any idea where their next meal is going to come from. Let’s not even stray into health and the need for medical emergencies; just putting three square meals on the table a day is proving to be impossible for so many,” wrote Ashish K. Mishra in a column on The Morning Context.

“At this very moment, it is they who need the government’s support. Not fat cats with bloated, middling business models and venture capital funds whose begging bowls are now seemingly larger than their risk appetite,” he added.

Companies asking for a bailout is not limited to India. Oil giants have sought similar help from the U.S. President Donald Trump — and VCs and startups are beginning to explore their option. Brent Hoberman, chairman and co-founder of Founders Factory and Firstminute Capital, urged the UK government to provide some relief to startups last month. But the government has yet to do much about it, just ask Deliveroo, Graphcore and other big UK startups.

Powered by WPeMatico

Last valued at $5 billion, restaurant management platform Toast has joined the sweep of startups laying off employees due to the economic impact of the COVID-19 pandemic. Toast reduced the size of its staff by 50% through layoffs and furloughs, according to a blog post from Toast’s CEO, Chris Comparato. It also reduced executive pay across the board, froze hiring, halted bonuses and pulled back offers.

The company’s flagship product helps restaurants process payments and handle orders through a mix of hardware and software. Think handheld ordering pads, self-service kiosks and display systems for kitchens. It also connects businesses to food delivery services like Grubhub.

Toast sits on the bridge between two industries in the spotlight, for better or worse, right now: restaurants and fintech. But restaurants have been hit hard as eateries were forced to close down due to state mandates, or to simply promote social distancing. As a result, fintech companies that help restaurants work better and depend on foot traffic are seeing less transaction volume.

Comparato, in the blog post, cited how restaurant revenue broadly took a huge hit in March, which naturally trickled down to Toast’s operations.

“With limited visibility into how quickly the industry may recover, and facing slower than anticipated growth, we now find ourselves in the unenviable position of reducing our headcount,” he wrote. He noted that before the pandemic hit, Toast revenue grew 109% in 2019. In an interview with Crunchbase News in February, chief financial officer Tim Barash said that the company’s goal in the next few years is to go public.

The Toast employees laid off were offered a “severance package, benefits coverage, mental health support, and an extended window during which they can purchase vested stock options,” the blog post detailed. Toast is also developing a program to help those laid off or furloughed look for new roles, a move that mimics other efforts we’ve seen across the startup world.

Investors in Toast include TCV, Tiger Global Management, Bessemer Venture Partners and T. Rowe Price Associates.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

A few weeks ago, Uber and Lyft, kicking bags of the 2019 stock market and regularly cited as examples of venture-backed excess, were back to fighting form.

After encouraging Q3 2019 reports from both ride-hailing giants that included fresh profitability promises and timelines, Uber upped the ante by moving its profitability goal up when it reported Q4 results earlier this year. Shares of the famous company rallied. When Lyft failed to mimic the declaration in its own Q4 earnings report, it was dinged by investors. But from the time of their Q3 2019 earnings reports to recently, Uber and Lyft were coming back up for air.

Suddenly, it was perfectly reasonable to be optimistic about the two ride-hailing companies that had become more famous for their sticky losses than their growth potential; as the pair had matured from upstart to public company, their money-losing methods appeared increasingly permanent, making the Q3 2019 and Q4 2019 profit declarations investor balm.

But after the rally came the novel coronavirus and COVID-19. Since then, the two companies have lost huge amounts of ground. Their shares fell 9.8% (Uber) and 11.8% (Lyft) yesterday alone. In pre-market trading this morning, they are down even more. I wanted to get my head around what could be causing this, so let’s run through each company’s most recent profit forecasts, results, share price gains and losses, and what investors are telling the world through their recent selloff. (Hint: DoorDash’s IPO probably isn’t happening soon.)

Powered by WPeMatico