corporate venture capital

Auto Added by WPeMatico

Auto Added by WPeMatico

Startups need to live in the future. They create roadmaps, build products and continually upgrade them with an eye on next year — or even a few years out.

Big companies, often the target customers for startups, live in a much more near-term world. They buy technologies that can solve problems they know about today, rather than those they may face a couple bends down the road. In other words, they’re driving a Dodge, and most tech entrepreneurs are driving a DeLorean equipped with a flux-capacitor.

That situation can lead to a huge waste of time for startups that want to sell to enterprise customers: a business development black hole. Startups are talking about technology shifts and customer demands that the executives inside the large company — even if they have “innovation,” “IT,” or “emerging technology” in their titles — just don’t see as an urgent priority yet, or can’t sell to their colleagues.

How do you avoid the aforementioned black hole? Some recent research that my company, Innovation Leader, conducted in collaboration with KPMG LLP, suggests a constructive approach.

Rather than asking large companies about which technologies they were experimenting with, we created four buckets, based on what you might call “commitment level.” (Our survey had 211 respondents, 62% of them in North America and 59% at companies with greater than $1 billion in annual revenue.) We asked survey respondents to assess a list of 16 technologies, from advanced analytics to quantum computing, and put each one into one of these four buckets. We conducted the survey at the tail end of Q3 2020.

Respondents in the first group were “not exploring or investing” — in other words, “we don’t care about this right now.” The top technology there was quantum computing.

Bucket #2 was the second-lowest commitment level: “learning and exploring.” At this stage, a startup gets to educate its prospective corporate customer about an emerging technology — but nabbing a purchase commitment is still quite a few exits down the highway. It can be constructive to begin building relationships when a company is at this stage, but your sales staff shouldn’t start calculating their commissions just yet.

Here are the top five things that fell into the “learning and exploring” cohort, in ranked order:

Technologies in the third group, “investing or piloting,” may represent the sweet spot for startups. At this stage, the corporate customer has already discovered some internal problem or use case that the technology might address. They may have shaken loose some early funding. They may have departments internally, or test sites externally, where they know they can conduct pilots. Often, they’re assessing what established tech vendors like Microsoft, Oracle and Cisco can provide — and they may find their solutions wanting.

Here’s what our survey respondents put into the “investing or piloting” bucket, in ranked order:

By the time a technology is placed into the fourth category, which we dubbed “in-market or accelerating investment,” it may be too late for a startup to find a foothold. There’s already a clear understanding of at least some of the use cases or problems that need solving, and return-on-investment metrics have been established. But some providers have already been chosen, based on successful pilots and you may need to dislodge someone that the enterprise is already working with. It can happen, but the headwinds are strong.

Here’s what the survey respondents placed into the “in-market or accelerating investment” bucket, in ranked order:

Powered by WPeMatico

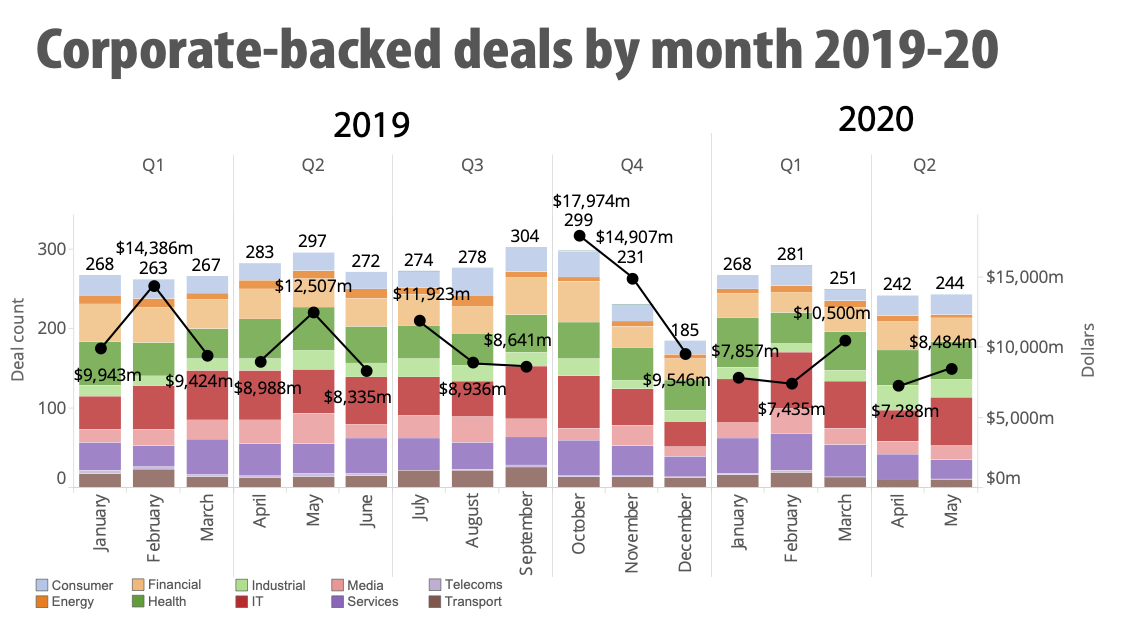

When the going gets tough, it’s common for some corporate VCs to head for the hills.

Today, it’s a narrative that’s emerging again amid the COVID-19 crisis. Global corporate venture deals fell from a total of 580 in April/May of 2019 to 486 in the same period this year, according to Global Corporate Venturing.

However, institutional VC deals are also headed for a decline, with PitchBook anticipating a drop in transaction volume over the next several quarters, as well as a downturn in valuations.

Image Credits: Global Corporate Venturing

It remains to be seen how it will play out this time, but I believe corporate venture capital (CVC) will not only stick around, but also be a vital part of the innovation ecosystem going forward.

I know that Merck Global Health Innovation Fund (MGHIF) remains fully committed to “doing” venture. Now, more than ever, health innovation is vital. Second, we understand that many of today’s most successful companies were funded in times of uncertainty. In fact, to put our money where our mouth is, we’ve recently completed two spinouts, three follow-on investments, and two new deals in 2020 — all since COVID hit. We intend to increase that pace going forward in 2020 and beyond.

It hasn’t been easy. It’s hard to do venture when you can’t venture out into the world, meet founders and do diligence the way we did in the past. But it is possible, if you do some innovating of your own and set up a smoothly functioning system to do CVC virtually.

Here’s how we’ve done it.

Powered by WPeMatico

Raising capital from a corporate VC can bring many benefits beyond just money. Strategic CVCs, who measure ROI based on the strength of the strategic partnership with their portfolio companies as well as the financial return, will typically seek to maximize their relationships with startups for a long time after the investment is made.

Specifically, a CVC investor can offer the following to an entrepreneur:

Partnerships. CVCs can leverage their supply chain and operations to build new partnerships that otherwise may have taken months or years for startups to create.

Distribution. Strategic CVCs can become a distribution channel for a startup, connect that startup with their suppliers, or even use the startup to become a channel for the parent company.

Branding halo. If a large company is willing to invest in your startup, it’s a strong signal that your product is good and that your business has a bright future.

Acquisition. Many CVCs invest in startups that they may want to acquire down the line. A CVC may also endorse an exit-seeking portfolio company to their partner companies or suppliers.

Granted, seeing results from these benefits takes time, and even the best of intentions during a capital raise process may not always yield an optimal strategic relationship.

Here’s a list of factors to keep in mind for founders who want the best chances of a productive and successful relationship with their CVC.

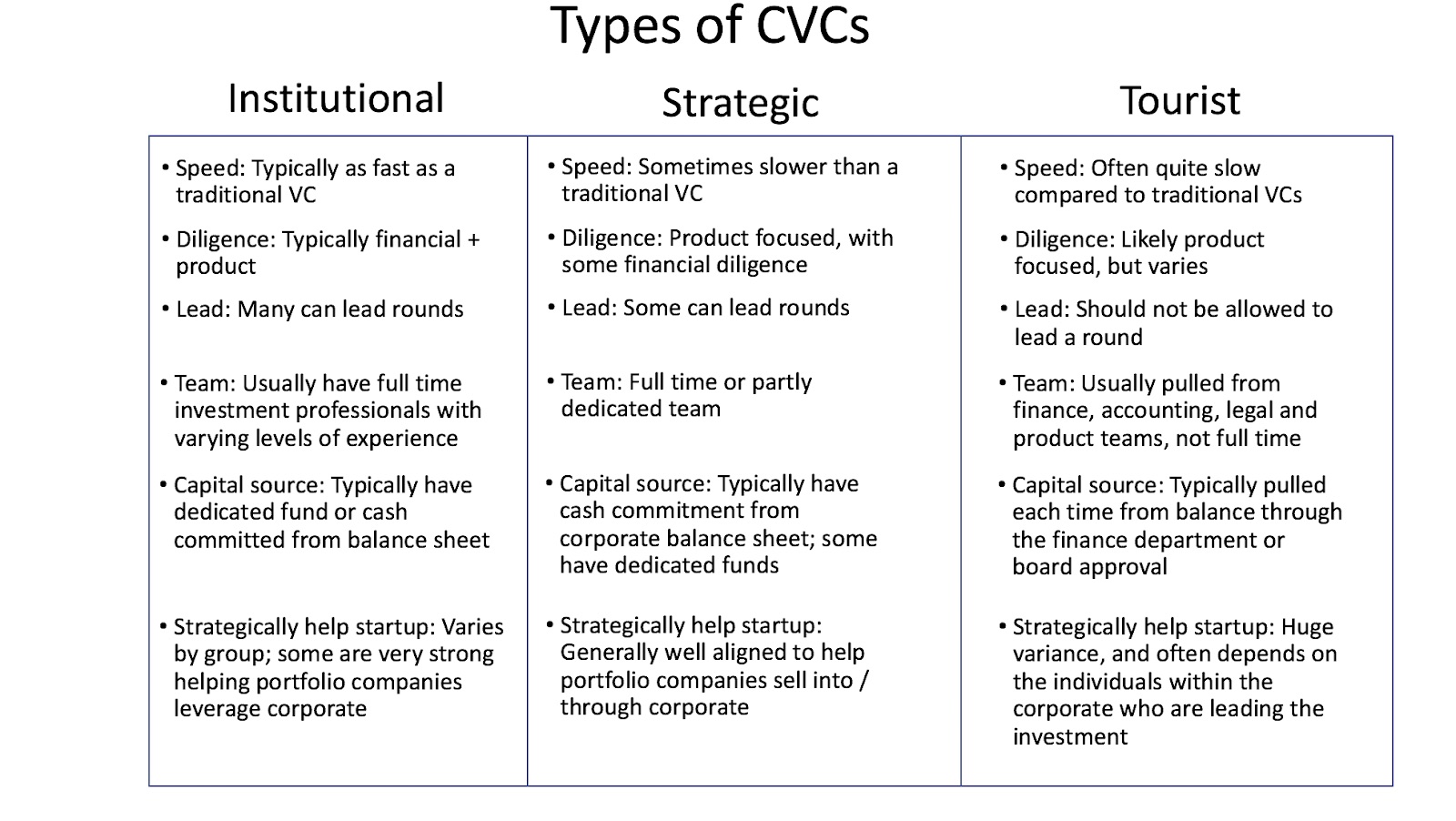

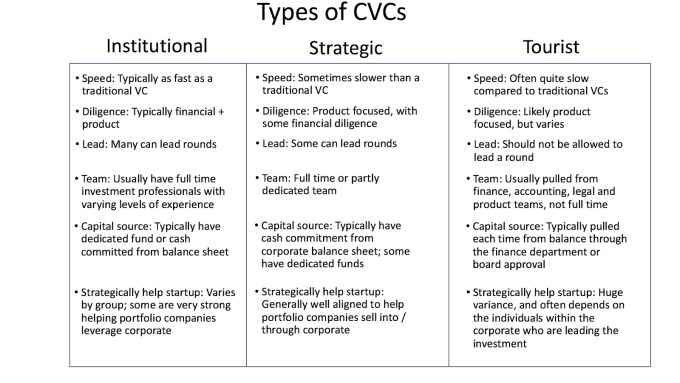

Know which type of CVC you’re dealing with from the outset. In our previous posts, we outlined the three types of CVCs — experienced institutional investors, industry-specific strategics, and beginner or “tourist” CVCs. As we’ve discussed, be sure to spend time interviewing and building relationships with CVCs to determine which type they are, what kinds of benefits and resources they can offer and what their history looks like in terms of successfully partnering with startups over time. When in doubt, ask other founders who have done deals with them!

Powered by WPeMatico

More than $50 billion of corporate venture capital (CVC) was deployed in 2018 and new data indicates that nearly half of all venture rounds will include a corporate investor. The CVC trend is heating up and the need for founders and startup executives to stay informed is higher than ever.

We’ve covered the basics in this series, including how to approach CVCs and what to know before the investment, what to look out for when negotiating, and getting the most out of a CVC partnership after the investment.

A great CVC investor can be the best of both worlds — a strong corporate champion who provides insights and connections to help your startup succeed and a committed financial partner who provides the capital you need to grow. But CVCs aren’t just VCs with different business cards. Finding the right CVC requires the right approach and strategy, and getting the right CVC on your cap table can bring unique and lasting value to your startup.

To wind down this series, here’s a list of the top 15 things every founder should know before signing a term sheet with a CVC.

Image credits: Orn/Growney

There are plenty of benefits to taking CVC investments. Many CVC investments lead to acquisitions, and even if the discussions with a CVC fall apart, your meeting can result in valuable introductions that yield new business relationships. The rising CVC trend offers a brave new world for entrepreneurs. If you know the ropes of CVC investing, you could be in for a partnership that benefits you both.

Powered by WPeMatico

Corporate venture capitalists (CVCs) are booming in the startup space as large companies look to take advantage of the fast-paced innovation and original thinking that entrepreneurs offer.

For startups, taking funding from CVCs can come with many benefits, including new opportunities for marketing, partnerships and sales channels. Still, no founder should consider a corporate investor “just another VC.” CVCs come with their own set of priorities, strategic objectives and rules.

When it comes to choosing a CVC with which to enter negotiations, the most important step is doing your own diligence beforehand. An entrepreneur’s goal is to find the perfect match to partner with and guide you as you grow your business. So before you start discussing terms, you’ll want to understand what’s driving the CVC’s interest in venture investing.

While traditional VCs are purely financially driven, CVCs can be in the venture game for a variety of reasons, including finding new technology that might generate marketplace demand for their products. An example is Amazon’s Alexa fund, which invested into emerging companies that drive use and adoption of Alexa. Alternatively, a CVC’s parent company may be looking to invest in tech that will help them operate their own products more efficiently, such as Comcast Ventures investing in DocuSign.

As a rule of thumb, the bigger CVC funds like GV and Comcast tend to be financially driven, meaning they’ll be approaching negotiations through a financial lens. As such, the negotiating process more closely resembles an institutional fund. You as a founder have to do the work to figure out what’s driving your CVC — is this a customer acquisition or distribution opportunity? Or are they seeking to find a source of knowledge transfer and/or bring new tech into their parent company?

“Before negotiating, always look at a CVC’s existing portfolio,” says Rick Prostko, managing director at Comcast Ventures. “Have they made a lot of investments, at what stage, and with whom? From this information you’ll see the strategic thinking of the CVC, and you can determine how best to position yourself when you begin negotiations.”

Powered by WPeMatico

Corporate venture capital (CVC) is booming, with more than $50 billion of CVC capital deployed in 2018. The rise in capital expenditures by CVCs between 2013 and 2018 was an impressive 400%, according to Corporate Venturing Research Data. There are currently more than a hundred active CVC investors, and some sources suggest that almost half of all venture rounds include a strategic investor.

This rise has been driven by two factors: 1) the tech landscape is moving at a faster pace and bigger companies know they need to innovate quicker to meet market demand; and 2) the number of startups seeking CVC capital is growing as founders look beyond traditional venture funds to help grow their businesses.

Kruze Consulting and Goodwin have worked with hundreds of startups through the funding process, including those working with CVCs. Together, the two firms and their principals have decades of experience advising founders during and after their capital raises.

To help startups navigate CVC transactions, we’ve created a guide to working with CVCs. In this segment, we’ll discuss the types of CVCs, the best way to approach each type and the key things to keep in mind during initial discussions.

Roughly put, CVCs fall into three categories:

As the realm of CVCs becomes increasingly professionalized, more and more CVCs fall into the first category. For entrepreneurs seeking CVC investors, those in the institutional or strategic category can provide tremendous value — though it’s important that a startup know which type of CVC they’re speaking to, and have clear objectives going in that align with the CVC’s goals and strengths.

Before engaging with a CVC, or any potential investor for that matter, the most important step is to do your research. Who is the individual you’re meeting with? What’s his/her background and what deals has he/she done with this venture group? These are Must Knows before walking into the initial meeting.

Once you’re in early discussions, ask the CVC whether he or she has carry in the fund and whether the venture arm is autonomous. The answers to these questions will help you clarify whether you’re dealing with institutional versus strategic CVCs.

“With corporate-backed venture funds, it’s really key up front to know who you’re talking to,” says Allen. “It’s dangerous to call all groups that are nontraditional investors ‘CVCs’ since some are far more serious than others. Most have some degree of strategic mandate but many are increasingly investing for financial gain.”

The next question is: Are you dealing with a financially driven CVC or a strategically driven one? From a founder’s standpoint, you’ll need to know whether you’re meeting with an investor who views deals through the lens of, “I’m looking for a great team, huge market and a chance to bring in funding and connections to make a business as strong as it can be” or, “I’m looking for a solution/product/platform that I can bring into my company or use to expose my company to a brand new marketplace or technology.”

Once again, the way to determine which type of CVC you’re dealing with is to ask the right questions. In the first meeting, ask about their investment process, how investments are made and whether strategic business unit sponsorship is required for a given deal. The answers will tell you whether the CVC falls into Group 1 or 2, and you’ll be in a strong position to then make choices about whether this potential investor is right for you.

“Look for someone who will understand your business, meet with you and decide that there’s something beyond just capital that will form the basis for that relationship,” says Rick Prostko, managing director at Comcast Ventures. “In today’s venture market, founders want money AND value. Seek out a CVC who has valuable experience to provide, and look for someone who’s been an operator in this segment previously or who has valuable insight and experience to offer.”

Once you’ve done your initial diligence, developed a relationship and determined that a CVC could be a strong investor in your business, there are important factors to be aware of as you move into the next stage of discussions. These include:

Expect deeper product and technical diligence. CVCs can call on technical, product and market experts within their corporation during the due diligence process. As such, their level of product diligence is typically more rigorous than traditional VCs. Be prepared for some grilling by subject matter experts. On the flip side, this diligence process provides you with exposure to potential customers and partners inside the corporation, so use this time to your advantage.

Be aware that you’re going to share confidential information with a large company. “CVCs know that you’re only as good as your reputation,” says Eric Budin, director at Touchdown Ventures . “As such, there are very few examples of CVCs abusing confidential information, because news of it would get around so quickly.”

Still, for a founder, the goal is to be thoughtful and strategic with what you share, and to determine whether the CVC is truly interested in doing a deal before you hand over financial, technical and competitive information. It’s possible that commercial teams at the CVC sponsor could gain unfair advantage from seeing your information, or use their CVC to gain valuable intel on the competition.

On the other hand, sharing your intel could be a fantastic way to get in front of an internal team at the parent company. The key is to think carefully about what you are being asked to share and with whom, and set ground rules with the CVC before they begin diligence.

“It’s important to understand how the corporate fund is structured and how they handle any information that’s shared,” says Prostko. “It might be in your interest to loop in a business unit [within the parent company] that could benefit from learning about your business. On the flip side, if the CVC is a potential competitor, you’ll want to be more careful about what you reveal.”

There will be a risk of regime change. Large companies operate like, well, large companies. People leave, management changes happen and priorities shift. At the outset, ask questions such as: Who will support your company if the commercial manager leading your investment leaves? What will happen to the CVC if the person leading the venture arm is fired? Will they do their pro-rata if the person leading your deal is gone? What happens to any commercial relationships that you might be working on? It’s important to have a keen understanding of internal dynamics before you enter the relationship.

“In general, the more successful a firm is, the more likely the CVC will stick around,” says Allen. “Be sure to look at the individual’s history at the firm, how long he or she has been there, and whether he or she has jumped from fund to fund. If the investing partner has come out of the corporate ‘mother ship,’ and lacks any credible venture experience, buyer beware.”

The CVC may be subject to regulatory rules. Depending on the industry, government regulations may impact how your deal is structured. Banks, for example, are subject to rules that can restrict the percentage of voting stock they can own. Foreign investors may need to comply with CFIUS regulations if your company provides certain specified technologies. Generally, the CVCs will understand the regulations that apply to them. They may not, however, bring them up until late in the process, which could lead to delays.

Commercial transactions with the corporate arm can slow things down. Purely strategic CVCs (Group 2) often require a commercial transaction to happen in connection with a venture deal. The process involved in these transactions often takes longer than the financing process, which can cause issues if the CVC is a key (but not sole) investor in the round. If you’re dealing with a Group 2 CVC, discuss this issue ahead of time to see if you can decouple the two transactions and close the investment prior to inking the commercial deal.

CVCs offer a wealth of capital, human resources and corporate partnerships for startups. But whether you choose to take CVC capital or not, you can benefit from merely approaching CVCs if you have business units operating in either the same space or a tangential space. An initial meeting both gives you an opportunity to do a sales pitch and offers the CVC a chance to vet a product or team and gain some deal insight. For founders, you gain a powerful sales opportunity that might have otherwise taken months or years to obtain.

“Even if you’re told ‘no’ by a CVC, the meeting could result in a good business relationship that could turn into a sales opportunity for you in the near future,” says Prostko.

The WRONG way to think about approaching CVC investors is something along the lines of, “I can’t raise what I want from financial VCs so I’ll go to CVCs as my second choice, since they’re more likely to say ‘yes’ and/or give me better terms.” This attitude will shut doors and cut you off from valuable partners, capital and opportunities to strategically grow your business.

Above all, stay informed as you choose whom to bring in as a partner. Ultimately, it’s your business and the responsibility to ensure that you bring in the right capital partners lies with you.

Powered by WPeMatico

When it comes to corporate venture capital, semiconductor giant Intel has shaped up to be one of the most prolific and prescient investors in the tech world, with investments in 1,582 companies worldwide, and a tally of some 692 portfolio companies going public or otherwise exiting in the wake of Intel’s backing.

Today, the company announced its latest tranche of deals: $132 million invested in 11 startups. The deals speak to some of the company’s most strategic priorities currently and in the future, covering artificial intelligence, autonomous computing and chip design.

Many corporate VCs have been clear in drawing a separation between their activities and that of their parents, and the same has held for Intel. But at the same time, the company has made a number of key moves that point to how it uses its VC muscle to expand its strategic relationships and also ultimately expand through M&A. Just earlier this month, it acquired Moovit, an Intel Capital portfolio company, for $900 million (a deal that was knocked down to $840 million when accounting for its previous investment).

“Intel Capital identifies and invests in disruptive startups that are working to improve the way we work and live. Each of our recent investments is pushing the boundaries in areas such as AI, data analytics, autonomous systems and semiconductor innovation. Intel Capital is excited to work with these companies as we jointly navigate the current world challenges and as we together drive sustainable, long-term growth,” said Wendell Brooks, Intel senior vice president and president of Intel Capital, in a statement.

The tranche of deals come at a critical time in the worlds of startups and venture investing. Many are worried that the slowdown in the economy, precipitated by the COVID-19 pandemic, will mean a subsequent slowdown in tech finance. Intel says that it plans to invest between $300 million and $500 million in total this year, so this would go some way to refuting that idea, along with some of the other monster deals and big funds that we’ve written out in the last couple of months.

The list announced today doesn’t include specific investment numbers, but in some cases the startups have also announced the fundings themselves and given more detail on round sizes. These still, however, do not reveal Intel’s specific financial stakes.

Here’s the full list:

Powered by WPeMatico

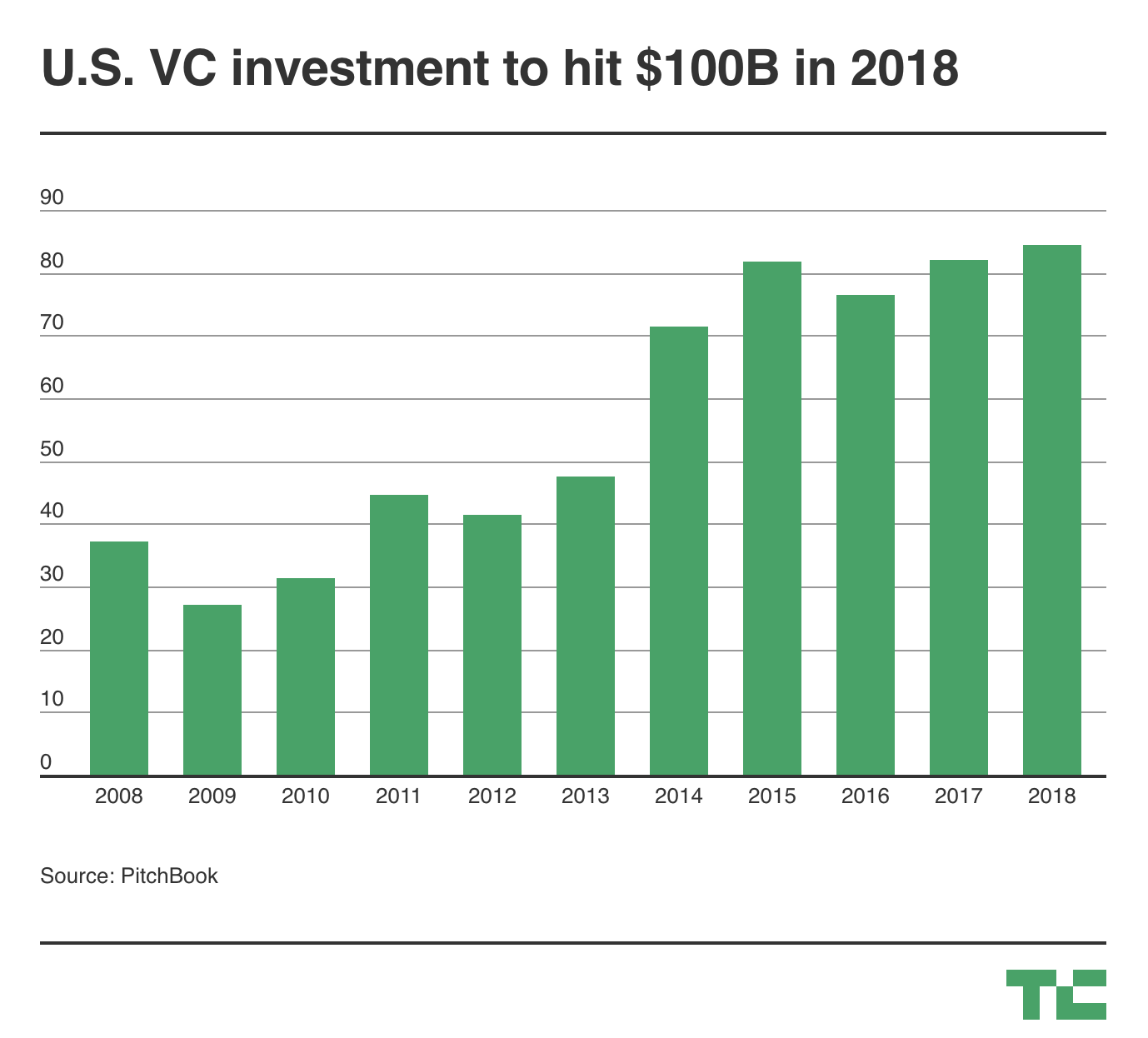

So many new unicorns valued at $1 billion-plus, countless $100 million venture financings, an explosion of giant funds — it’s no surprise 2018 is shaping up to be a banner year for venture capital investment in U.S.-based companies.

There are more than 2.5 months remaining in 2018 and already U.S. companies have raised $84.1 billion — more than all of 2017 — across 6,583 VC deals as of Sept. 30, 2018, according to data from PitchBook’s 3Q Venture Monitor.

Last year, companies raised $82 billion across more than 9,000 deals in what was similarly an impressive year for the industry. Many questioned whether the trend would — or could — continue this year, and oh, boy has it. VC investment has sprinted past decade-highs and shows no signs of slowing down.

Why the uptick? Fewer companies are raising money, but round sizes are swelling. Unicorns, for example, were responsible for about 25 percent of the capital dispersed in 2018. Those companies, which include Slack, Stripe and Lyft, have raised $19.2 billion so far this year — a record amount — up from $17.4 billion in 2017. There were 39 deals for unicorn companies valuing $7.96 billion in the third quarter of 2018 alone.

Some other interesting takeaways from PitchBook’s report on the U.S. venture ecosystem:

Powered by WPeMatico

It has often been said that every company is a software company or even a big data company, but as I attended the Intel Capital Global Summit last week, another thought occurred to me: every company is now also an investment company. The star of the show last week was Intel Capital of course, the venture arm of Intel Corporation, but it’s far from alone. Over dinner strictly by… Read More

It has often been said that every company is a software company or even a big data company, but as I attended the Intel Capital Global Summit last week, another thought occurred to me: every company is now also an investment company. The star of the show last week was Intel Capital of course, the venture arm of Intel Corporation, but it’s far from alone. Over dinner strictly by… Read More

Powered by WPeMatico

What a difference one year makes. Since showing noteworthy signs of a maturing tech ecosystem last summer, corporate venture in Latin America has begun to crescendo in just 12 months, led by Brazil.

What a difference one year makes. Since showing noteworthy signs of a maturing tech ecosystem last summer, corporate venture in Latin America has begun to crescendo in just 12 months, led by Brazil.