coronavirus

Auto Added by WPeMatico

Auto Added by WPeMatico

Over the past few months, Yelp has been taking steps to help businesses reeling from the impact of the coronavirus pandemic — things like waived fees, virtual service listings and GoFundMe fundraisers (that last one had a mixed reception).

But without getting into the question of whether the United States is reopening at the right time in the right way, it’s clear that the reopening is happening, and businesses are going to need new tools to safely navigate the changing landscape. So Yelp is announcing two of those tools today.

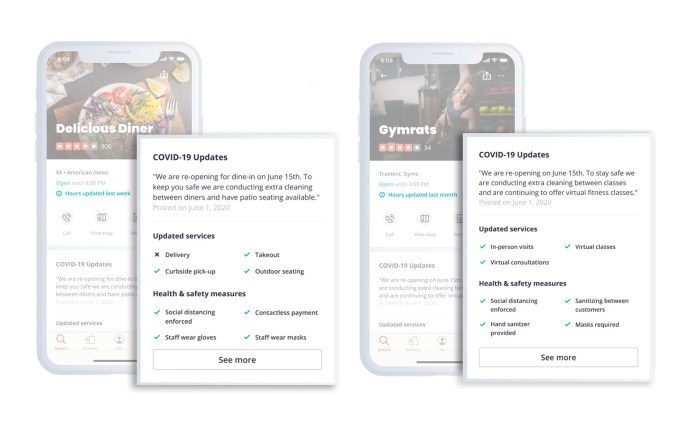

First, it says it’s expanding on its COVID-19 banners, with a full COVID-19 section on each business profile. So those businesses can indicate whether they’re doing things like enforcing social distancing, sanitizing spaces between customer visits, requiring that employees wear masks and/or gloves, requiring that customers wear masks and so on.

These updates will be timestamped. There can, of course, still be a difference between what the business promises and the reality in the store. But as a consumer, at least you’ll know how up-to-date those promises are.

Image Credits: Yelp

In addition, Yelp says it will use a combination of human moderation and machine learning to update these sections with information that businesses have posted elsewhere, like whether they offer curbside pickup or virtual services.

The company is also updating its waitlist feature, which restaurants may be turning to as a way to avoid long lines and crowds. Restaurants will now be able to print a QR code that customers can scan to add themselves to the waitlist in a contactless way. Hosts will also be able to manually adjust wait times, and they’ll get alerts when they’re approaching legally mandated seating capacities.

In a statement, Yelp’s head of consumer product Akhil Kuduvalli Ramesh said that the company’s response to the pandemic has broken down into two phases. During the first phase, “We helped businesses convey how they are updating their operating models and services they offered.”

He added, “In phase two, as people begin to reenter businesses, addressing the health and safety needs in the local marketplaces across the US is of paramount importance.”

Powered by WPeMatico

If you’re a business owner or investor and are wondering about the long-term impacts of the COVID-19 pandemic on the business world, you’re not alone.

Today’s business leaders have been plunged into the deep end of telecommuting with little notice, and the way we do business has been impacted at almost every level. Travel is restricted, meetings are virtual and delivery of goods and even raw materials is being delayed. While some industries that depend on large gatherings are seeing extremely difficult challenges due to the pandemic, others such as the tech industry, see the opportunity and responsibility for innovation and growth.

As many states begin phased reopening, companies are trying to determine what the workplace and business environment will look like in a post-quarantine world. The first obvious step is the integration of personal protective equipment (PPE). Sanitization and face masks will become required and nonessential face-to-face meetings will be a thing of the past, along with shaking hands.

Additionally, relationship-driven careers such as sales and recruiting will have to find new ways to connect to be successful. Physical distancing rules will have to be established, which may include employees coming in alternate days while telecommuting the other days of the week to keep offices at reduced capacity. Large offices of 10 or more may implement thermographic camera technology for fever screening or other real-time technology-based health screenings.

One thing is for sure: IoT devices that enable physical distancing will become an integral part of reopening businesses, facilitating sales connections and embracing a different way of living.

There are a variety of IoT devices available that can help business leaders successfully implement physical distancing in their offices. Thermographic camera technology coupled with facial recognition can create a baseline for each employee and then assist in determining if an employee has a temperature outside of their norm. Other remote health monitoring may also take place with healthcare providers, helping employees determine on a daily basis if they are well enough to go into work.

Powered by WPeMatico

In a typical month, an IT department might deal with a small percentage of employees working remotely, but tracking a few thousand employees is one thing — moving an entire company offsite requires next-level planning.

To learn more about how large organizations are adapting to the rapid shift to working from home, we spoke to Liberty Mutual CIO James McGlennon, who helped orchestrate his company’s move about the challenges he faced as he shifted more than 44,000 employees in a variety of jobs, locations, cultures and living situations from office to home in short order.

Insurance company Liberty Mutual is headquartered in the heart of Boston, but the company has offices in 29 countries. While some staffers in parts of Asia and Europe were sent home earlier in the year, by mid-March the company had closed all of its offices in the U.S. and Canada, eventually sending every employee home.

McGlennon said he never imagined such a situation, but the company saw certain networking issues in recent years that gave them an inkling of what it might look like. That included an unexpected incident in which two points on a network ring around one of its main data centers went down in quick succession, first because a backhoe hit a line, and then at another point because someone stole the fiber-optic cable.

That got the CIO and his team thinking about how to respond to worst cases. “We certainly hadn’t contemplated needing to get 44,000 people working from home or working remotely so quickly, but there have been a few things that have happened over the last few years that made me think,” he said.

Powered by WPeMatico

May marked another extremely strong month for gaming sales, according to the latest figures from NPD. Between software, hardware, accessories and game cards, Americans spent around $977 million. That’s a 57% jump since the year prior and the highest it’s been for the month since 2008, when the country was feeling the strain of the Great Recession.

All of this is made more remarkable by the fact that the United States has been struggling with COVID-19-related pains for months now. This week, another 1.5 million Americans filed for unemployment, bringing the total number to 44.2 million since the beginning of shutdowns. But as countless other venues for non-essential spending have suffered, gaming has thrived.

It’s clear that games are how Americans are choosing to spend whatever sort of disposable income they might have, as they’re stuck at home, away from other humans. And that spending has continued for a few months now, even after Microsoft and Sony have begun hyping their next-generation consoles — both due at at the end of the year.

That, perhaps, is part of why Nintendo continued to dominate console sales with the Switch, in spite of hardware shortages. Animal Crossing: New Horizons remained the top-selling title for the console (and third over all), owing to the online cult it has amassed through social-first gameplay. Call of Duty: Modern Warfare and Grand Theft Auto V took the No. 1 and No. 2 spots, respectively, on both the PlayStation 4 and Xbox One.

Powered by WPeMatico

Traditionally, measuring business success requires a greater understanding of your company’s go-to-market lifecycle, how customers engage with your product and the macro-dynamics of your market. But in the most challenging environment in decades, those metrics are out the window.

Enterprise application and SaaS companies are changing their approach to measuring performance and preparing to grow when the economy begins to recover. While there are no blanket rules or guidance that applies to every business, company leaders need to focus on a few critical metrics to understand their performance and maximize their opportunities. This includes understanding their burn rate, the overall real market opportunity, how much cash they have on hand and their access to capital. Analyzing the health of the company through these lenses will help leaders make the right decisions on how to move forward.

Play the game with the hand you were dealt. Earlier this year, our company closed a $40 million Series C round of funding, which left us in a strong cash position as we entered the market slowdown in March. Nonetheless, as the impact of COVID-19 became apparent, one of our board members suggested that we quickly develop a business plan that assumed we were running out of money. This would enable us to get on top of the tough decisions we might need to make on our resource allocation and the size of our staff.

While I understood the logic of his exercise, it is important that companies develop and execute against plans that reflect their actual situation. The reality is, we did raise the money, so we revised our plan to balance ultra-conservative forecasting (and as a trained accountant, this is no stretch for me!) with new ideas for how to best utilize our resources based on the market situation.

Burn rate matters, but not at the expense of your culture and your talent. For most companies, talent is both their most important resource and their largest expense. Therefore, it’s usually the first area that goes under the knife in order to reduce the monthly spend and optimize efficiency. Fortunately, heading into the pandemic, we had not yet ramped up hiring to support our rapid growth, so were spared from having to make enormously difficult decisions. We knew, however, that we would not hit our 2020 forecast, which required us to make new projections and reevaluate how we were deploying our talent.

Powered by WPeMatico

One would think it’s a given that investment strategies would change in the strange times we find ourselves. With the economy staggering and so much general uncertainty, it seems caution would be the watchword of the day, especially in the enterprise. But enterprise investors aren’t necessarily looking at what’s going on right now.

As startups make their way into the enterprise, they often grow from a single product to a platform offering, which means such investments tend to be a long haul that can take a decade or longer to mature and exit or IPO. The bigger the approach, the longer the sales cycle, so even though sales motion could be stalling now, it doesn’t mean VCs are just giving up on these types of investments.

Savvy investors understand that this is going to be a long game, and the current situation driven by a worldwide pandemic won’t necessarily change their approach significantly.

We asked a number of enterprise investors if they have changed their approach in light of the pandemic and its knock-on economic impacts, how the current environment has changed their relationship with existing portfolio clients and how well those clients are coping with the new reality.

[Editor’s note: Our prior enterprise survey failed to include any responses from female VCs and did not meet TechCrunch’s standards for diversity and inclusion. We regret the error.]

With the pandemic having such a huge impact on the economy, how has this changed your investment approach and the types of companies you are more likely to invest in?

We remain committed to our five core thesis areas: security & infrastructure modernized, financial services rebuilt, work reimagined, data interconnected, and community activated. We break out each of our thesis areas into anywhere from 10-20 sub-sectors.

We have been continuously reprioritizing which sub-sectors will likely see business growth as well as opportunities to make a positive difference to a world grappling with COVID. There are still many unknowns and we closely watch company formation and funding to see where there might be particular concentration of entrepreneurial activity, which we take to be a positive sign that a market is robust and ready for significant investment.

Within enterprise software, we’ve unsurprisingly seen an acceleration in enterprise demand for communication and collaboration software. We’ve historically maintained a thesis that enterprise communication is an untapped, shadow set of data about workplace productivity and knowledge. With swaths of workers working remotely, capturing insights from these conversations provides a significant opportunity. This applies to industry verticals as much as it applies to functional software that sells across industries and focuses on a particular type of communication. We believe the key is that both employees and employers find these insights to be beneficial.

Lastly, we’ve also seen a growth in software and data that help enterprises navigate disruptions in supply, demand, or other aspects of their business.

Powered by WPeMatico

One of the earliest disruptions created by the novel coronavirus manifested in the form of event cancellations. Some of the world’s biggest tech conferences, like F8 and Google NEXT, got postponed and others turned to digital options to still connect. Even Disrupt is going digital this year.

It is an unprecedented time for the events world, so we are bringing someone right in the center of it to our Extra Crunch Live stage: Eventbrite CEO Julia Hartz. In fact, Extra Crunch members can ask their own questions directly to the CEO and are encouraged to do so live on the call.

Hartz is leading the publicly traded company as it grows more popular than ever with hundreds of millions of dollars in revenue. At the same time, the global slowdown of in-person event ticketing due to COVID-19 has had a material impact on Eventbrite’s business. What does that mean for employee morale? Collaboration with other companies? And overall culture at the business?

Eventbrite has swiftly transitioned to virtual events, with thousands of listings across categories like professional events, classes, health and wellness, science and tech, community and culture and more. Hartz also told Billboard that the company remains committed to serving independent music venues, which have been hit hard by the global health crisis, and hinted that Eventbrite may shift to a self-service ticket model.

The company reported that, since enhancing its online events service in 2019, and in the midst of social distancing, Eventbrite users are posting nearly 20k online events every day, with a 2,000+ percent year-over-year increase of online events taking place in April 2020 compared to April 2019. This announcement came after Eventbrite said it would cut $100 million in costs, which included layoffs.

We’ll talk with Hartz about how she is leading her company through a crisis and what the future holds for bringing people together. We’ll also discuss how widespread layoffs may impact the future of diversity in our workforces.

Hartz will also be asked to weigh in on advice for other founders hoping to emerge from COVID-19 from fundraising to strategy. As always, EC subscribers are invited to log onto the call to ask questions live.

Details are below for Extra Crunch subscribers; if you need a pass, get a cheap trial here.

Chat with you all in a week!

Powered by WPeMatico

When Larry Liu moved to the U.S. in 2003, one of the first challenges he experienced was the lack of Chinese ingredients available in local groceries. A native of Hubei, a Chinese province famous for its freshwater fish and lotus-inspired dishes, Liu got by with a limited supply found at local Asian groceries in the Bay Area.

His yearning for home food eventually prompted him to quit a stable financial management role at microcontroller company Atmel and go on to launch Weee!, an online market selling Asian produce, snacks and skincare products.

Like other players in grocery e-commerce, the five-year-old startup has seen exponential growth since the coronavirus outbreak as millions are confined to cooking and eating at home. Nearly a quarter of Americans purchased groceries online to avoid offline shopping during the pandemic, according to Statista data. Online grocery giants Instacart and Walmart Grocery boomed, both hitting record downloads.

In a Zoom call with TechCrunch, Liu, who’s now chief executive of Weee!, said that COVID-19 played a “very important role” in his company’s recent growth, and paved its way to profitability.

“It happened a lot faster than we expected, but we were growing rapidly with even more ambitious plans for expansion prior to COVID-19,” he said. “People are buying more because restaurants are closed. Many are first-time users of grocery delivery.”

The startup’s revenue is up 700% year-over-year and is estimated to generate an annual revenue in the lower hundreds of millions of dollars.

Powered by WPeMatico

The world feels as fragile as ever, and those with any options at all are looking to get away this summer.

For many, planes and hotel rooms won’t be an option they consider owing to continued concerns about the coronavirus (not to mention the expense, which 40 million fewer Americans can likely afford). That leaves perhaps renting a local Airbnb this summer or, for a growing number of people, looking for the first time to rent an RV or camper van, including as a way to visit far-flung family members who might otherwise be unreachable.

Last week, we talked with Jeff Cavins, a serial operator and the co-founder and CEO of a company that’s poised to benefit from the latter trend: Outdoorsy, a peer-to-peer RV rental company that was founded in 2015, bootstrapped by its founders for a couple of years, and has more recently attracted $88 million in venture funding, $13 million of it an extension to a $50 million Series B round that it quietly closed early this year.

We wanted to know what trends the company — which collects fees from both the vehicle owners and the renters on its platform — is seeing, including how its customers are changing and where they’re looking to park themselves this summer. Below are some excerpts from our chat, edited lightly for length.

TC: How has your model changed because of the coronavirus?

JC: We had typically seen an average rental on our platform would run about six days. That’s now over nine days. With COVID, as with many other companies, we saw a lot of de-bookings in the platform, but then they all roared back and then some. We’ve seen a 2,645% increase in bookings from the low point of COVID, which was late March, to right now.

TC: What percentage of those booking trips are first-time customers?

JC: In the month of May, 88% of our bookings were by first-time renters, which is a record for us. And more than half of them have come back and already booked their second trip. So some booked in May; they went away for the Memorial Day weekend [and] came right back. And they booked another one for, in this case, like the Fourth of July or [trips in] June. As you know, a lot of people are at home with their kids, so everybody in America has this big, long extended summer break. And with the kids, they’re finding this is the safer option for travel.

TC: Are their expectations different? Are they looking for certain things that maybe more seasoned RV campers wouldn’t think to ask?

JC: The big trend that we’re seeing in the RV industry, and this is not unique to America, is the new consumers don’t want those big land barges. What they want are camper vans, because the average user on our platform is under the age of 40, which was a big surprise to this industry because it’s always leaned a little bit towards the Boomer or the retiree demographic. And they like camping off the grid. They like to operate with vehicles that feel comfortable to them, that have a smaller footprint, that are easier on the environment. And so things that have become popular are solar power, potable water that can be transportable, hookups for mountain bikes, sporting gear . . . They also want to be able to head to unique locations where they can build those Instagram mobile moments. So we’re starting to see that trend, and it has become a global phenomenon.

TC: When we last talked, in January of last year, Outdoorsy had around 35,000 vehicles available to rent on the platform. How many are on the platform now?

JC: We have 48,000 peer-to-peer listings; when we add our international users and we have a lot of these mega fleets that are connected to our site via an API like Indies Campers or Jucy, that puts our supply at 68,000 units.

TC: And how are you making sure that these vehicles are free of germs and don’t transmit diseases?

JC: Cleanliness is a big factor for any form of accommodation. In our case, we’ve been producing for our listing community CDC guidelines on cleaning standards. We’ve asked our owners to place additional time between rentals so they can let the vehicles take time to manually disinfect. One of our investors at our company is a molecular biologist [whose] doctoral thesis at Harvard won the Nobel Prize for chemistry and he’s been helping us communicate with our owner community on things like these new ultraviolet radiation lamps that are common. You’ll see them installed in ambulances . . . if you let them set for a while, they will help completely decontaminate the environment.

We’re also encouraging renters to bring cleaning supplies with them. A lot of people will feel much more safe if they’re able to control their environment. And we’ve started a contactless key exchange, [meaning] the owner will deliver the vehicle to a campsite, put up the awning, the camping chairs, and so on. And then the renter will come later.

TC: You mentioned changing user behaviors. Out of curiosity, are you you seeing renters who aren’t heading to Yosemite or Yellowstone but instead to an RV down the street so they can, say, work apart from young children?

JC: One of the things that we’ve seen is, I may live in San Diego, for example, and grandma lives in Kansas City, and there’s no way for the kids to go see her. So camper van and RV travel has become that way for families to see those loved ones they haven’t been able to see during quarantine and maintain family connectivity.

TC: You mentioned de-bookings earlier this year. Did you have to lay off staff?

JC: We had about 160 employees prior to COVID. And we did do some right-sizing. Most of the impact in our organization was in our international markets — we had a team in Italy, Germany, France, U.K., Australia, New Zealand [that were cut]. In terms of our domestic employees, rather than cuts, we sat down with the team and said, ‘If everybody is willing to take a salary adjustment, we will reward you with more equity in the business. This could be a period of time where we save those jobs around us.’

I work with no income; I don’t have a salary. And there are a few other executives who elected to [forgo theirs]. So it was a way to align our employees with our investors by compensating them more in equity.

TC: As business picks up again, are you thinking about another round of funding?

JC: There is no plan to [raise more right now]. We were profitable in the month of May. We’ll be profitable again in the month of June. Unless there’s a second wave of COVID and lockdowns, our booking activity is now foretelling a profitable July, August and September, so we’ll possibly produce a year-on-year fiscal profitable year.

The ones we typically get inbound activity from are the late-stage growth investors. We’ll all sit down with the board and we’ll talk about it and decide: Do we want to do something with that or just want to just keep, you know, chopping wood as fast as we can on our own?

Powered by WPeMatico

COVID-19 has transformed the global business landscape.

So much so that in a matter of weeks after the onset of the pandemic in the United States, Congress provided more than $1.1 trillion in fiscal stimulus directly to businesses and distressed industries — four times more than was distributed during the 2008-09 financial crisis.

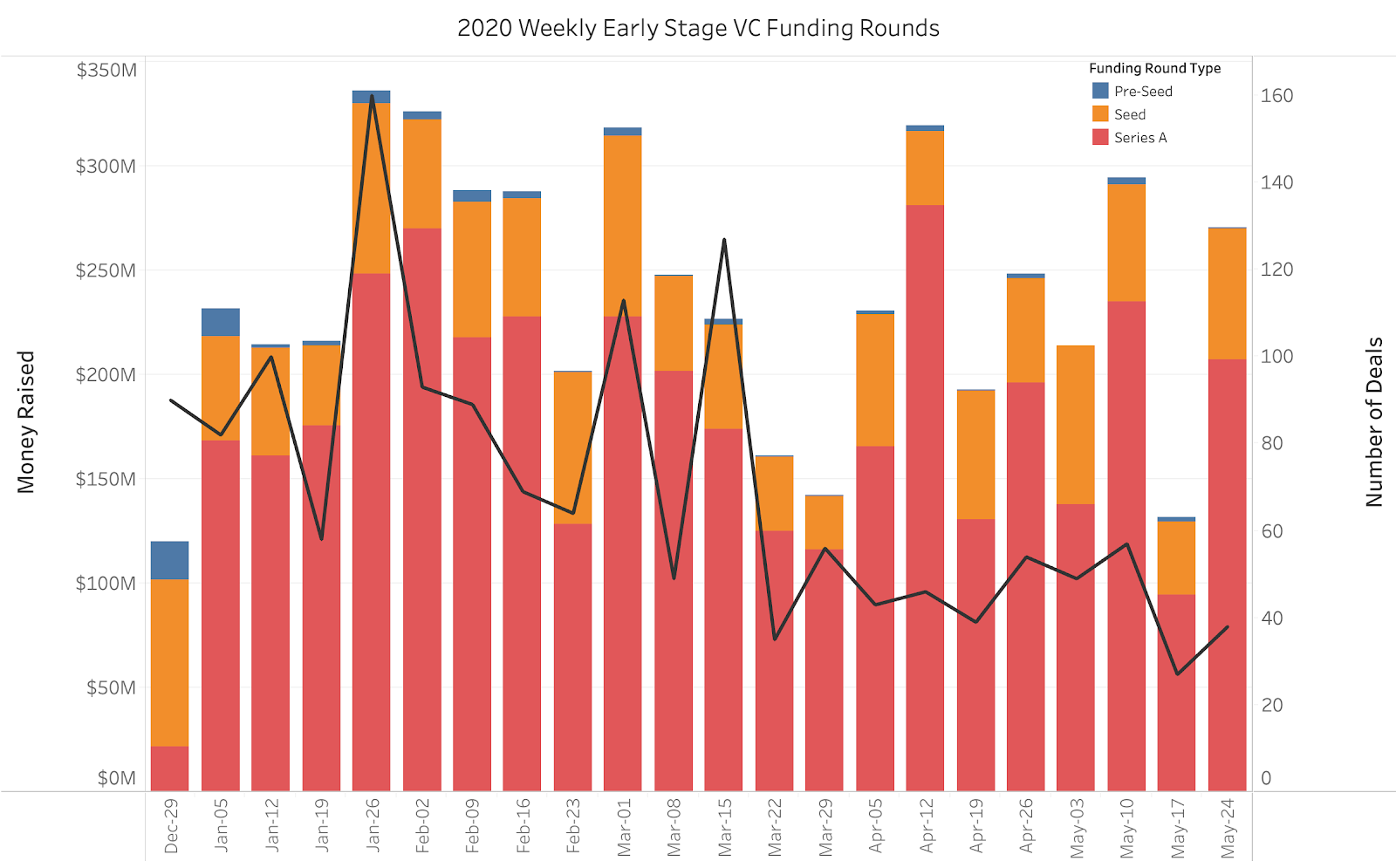

It came as no surprise when, at the start of COVID-19, venture capital investors largely went pencils-down for several weeks and shifted their focus to their existing portfolio companies. Extending company runways, preparing for longer funding cycles and managing operations in a novel business environment became the crux of company resilience. Now, moving into May, we can see this shift reflected in both the decline in number of early-stage companies funded and total capital invested.

As investors begin acclimating to this new normal, they have begun wading into new opportunities in time-proven, healthy industries and new emerging industries that are positioned to succeed during the pandemic. While we are seeing lower valuations, we believe certain B2B technology companies may be uniquely poised to thrive, and are pursuing investment opportunities in this space with a renewed focus.

Image Credits: Crunchbase Data via Tableau Public

*Excluding Biotech & Pharmaceuticals (Source: Crunchbase Data via Tableau Public)

Prior to COVID-19, early-stage B2B investors wanted to see strong growth and healthy unit economics; 3X year-over-year sales growth or 10% monthly growth was the gold standard. An LTV-to-CAC ratio over 3X signified a healthy payback cycle. There was less focus on capital efficiency; for every $1 million invested, investors were happy with $500,000 in generated revenues. Get to these numbers and your next funding round was guaranteed — but no longer.

During COVID, and likely beyond, company expectations and goalposts have been adjusted; 2X year-over-year growth may be the new 3X. While growth and unit economics are important, there are now new health indicators that will determine if a B2B company will thrive in a post-COVID world. With that in mind, we have put together a COVID reslience test that startups can use as a north star to grow their business in this new world.

This COVID-19 test is meant to be a gated checklist that will indicate where efforts should be focused, whether it be sales, product or finance. Before we leave you to your own devices, we wanted to walk through a couple of these new post-COVID questions that you should try to answer (and why they are relevant).

Powered by WPeMatico