Companies

Auto Added by WPeMatico

Auto Added by WPeMatico

Zoom, the only profitable unicorn in line to go public, priced its initial public offering at between $28 and $32 per share Monday morning. The video conferencing business plans to trade on the Nasdaq under the ticker symbol “ZM.”

Zoom, valued at $1 billion in 2017, initially filed to go public in March. According to its amended IPO filing, the company will raise up to $348.1 million by selling 10.9 million Class A shares. The offering will grant Zoom a fully diluted market value of $8.7 billion, a more than 8x increase to its latest private market valuation.

Although the company has garnered praise for its stellar financials — Zoom posted $330 million in revenue in the year ending January 31, 2019, a remarkable 2x increase year-over-year, with a gross profit of $269.5 million — the road to IPO hasn’t been without hiccups.

The company’s founder and chief executive officer Eric Yuan last night published an open letter concerning the conduct of Zoom’s chief financial officer Kelly Steckelberg. According to the letter, Zoom was recently informed by an anonymous source that Steckelberg had an “undisclosed, consensual relationship” during her tenure at a previous employer.

Steckelberg was most recently the CEO of the online dating site Zoosk; before that, she was a senior director in consumer finance at Cisco . The letter does not specify where the relationship took place, when or with whom.

Losing a CFO mere days before an IPO would have been a major loss for Zoom. CFOs often become the face of the IPO, handling the grueling tasks associated with crafting an IPO prospectus, leading the roadshow and more, while also maintaining day-to-day financial operations.

Yuan writes that the Zoom’s board of directors conducted a full investigation into the matter and determined that Steckelberg would stay on as Zoom’s CFO: “Kelly expressed regret for what transpired at her former employer, took ownership for the situation, and made clear to us that she had learned valuable lessons from the experience,” he wrote.

“We appreciated Kelly’s openness and candor during this process,” he continued. “It is clear that this matter related only to circumstances at her former employer. During Kelly’s tenure at Zoom, she has been an incredible contributor, as well as a model steward of our culture, values, and high standards since joining the Company.”

We reached out to Zoosk for comment. Zoom declined to comment further.

Zoom, expected to make the final call on its IPO price next Wednesday, will likely price at the top of the range and see a clean pop on its first day on the markets given its clean track record and positive financials. The business was founded in 2011 by Eric Yuan, an early engineer at WebEx, which sold to Cisco for $3.2 billion in 2007. Before launching Zoom, he spent four years at Cisco as its vice president of engineering.

Zoom has raised $145 million to date from investors, including Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent pre-IPO stake); Digital Mobile Venture (8.5 percent), a fund affiliated with former Zoom board member Samuel Chen; and Bucantini Enterprises Limited (5.9 percent), a fund owned by Li Ka-shing, a Chinese billionaire and among the richest people in the world.

Morgan Stanley, JP Morgan and Goldman Sachs are leading its offering.

Powered by WPeMatico

Razer is summoning a big gun as it bids to develop its mobile gaming strategy. The Hong Kong-listed company — which sells laptops, smartphones and gaming peripherals — said today it is working with Tencent on a raft of initiatives related to smartphone-based games.

The collaboration will cover hardware, software and services. Some of the objectives include optimizing Tencent games — which include megahit PUBG and Fortnite — for Razer’s smartphones, mobile controllers and its Cortex Android launcher app. The duo also said they may “explore additional monetization opportunities for mobile gaming,” which could see Tencent integrate Razer’s services, which include a rewards/loyalty program, in some areas.

The news comes on the same day as Razer’s latest earnings, which saw annual revenue grow 38 percent to reach $712.4 million. Razer recorded a net loss of $97 million for the year, down from $164 million in 2017.

The big-name partnership announcement comes at an opportune time for Razer, which has struggled to convince investors of its business. The company was among a wave of much-championed tech companies to go public in Hong Kong — Razer’s listing raised more than $500 million in late 2017 — but its share price has struggled. Razer currently trades at HK$1.44, which is some way down from a HK$3.88 list price and HK$4.58 at the end of its trading day debut. Razer CEO Min Liang Tan has previously lamented a lack of tech savviness within Hong Kong’s public markets despite a flurry of IPOs, which have included names like local services giant Meituan.

Nabbing Tencent, which is one of (if not the) biggest games companies in the world, is a PR coup, but it remains to be seen just what impact the relationship will have at this stage. Subsequent tie-ins, and potentially an investor, would be notable developments and perhaps positive signals that the market is seeking.

Still, Razer CEO Min Liang Tan is bullish about the company’s prospects on mobile.

The company’s Razer smartphones were never designed to be “iPhone-killers” that sold on volume, but there’s still uncertainty around the unit with recent reports suggesting the third-generation phone may have been canceled following some layoffs. (Tan declined to comment on that.)

Mobile is tough — just ask past giants like LG and HTC about that… and Razer’s phone and gaming-focus was quickly copied by others, including a fairly brazen clone effort from Xiaomi, to make sales particularly challenging. But Liang maintains that, in doing so, Razer created a mobile gaming phone market that didn’t exist before, and ultimately that is more important than shifting its own smartphones.

“Nobody was talking about gaming smartphones [before the Razer phone], without us doing that, the genre would still be perceived as casual gaming,” Tan told TechCrunch in an interview. “Even from day one, it was about creating this new category… we don’t see others as competition.”

With that in mind, he said that this year is about focusing on the software side of Razer’s mobile gaming business.

Tan said Razer “will never” publish games as Tencent and others do, instead, he said that the focus is on helping discovery, creating a more immersive experience and tying in other services, which include its Razer Gold loyalty points.

Outside of gaming, Razer is also making a push into payments through a service that operates in Southeast Asia. Fueled by the acquisition of MOL one year ago, Razer has moved from allowing people to buy credit over-the-counter to launch an e-wallet in two countries, Malaysia and Singapore, as it goes after a slice of Southeast Asia’s fintech boom, which has attracted non-traditional players that include AirAsia, Grab and Go-Jek, among others.

Powered by WPeMatico

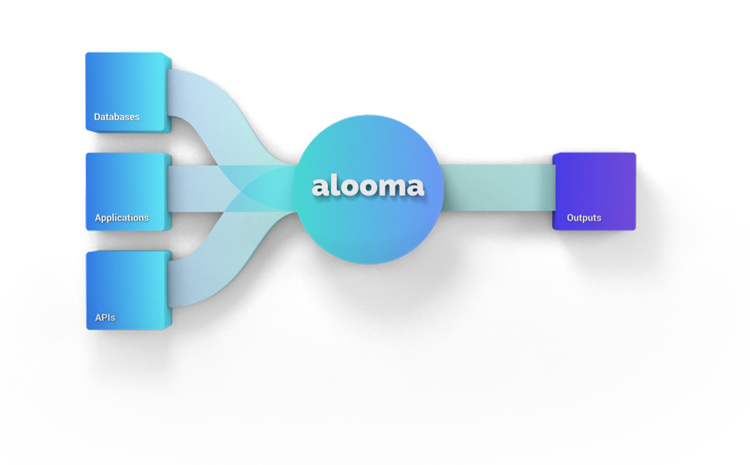

Google today announced its intention to acquire Alooma, a company that allows enterprises to combine all of their data sources into services like Google’s BigQuery, Amazon’s Redshift, Snowflake and Azure. The promise of Alooma is that it handles the data pipelines and manages them for its users. In addition to this data integration service, though, Alooma also helps with migrating to the cloud, cleaning up this data and then using it for AI and machine learning use cases.

“Here at Google Cloud, we’re committed to helping enterprise customers easily and securely migrate their data to our platform,” Google VP of engineering Amit Ganesh and Google Cloud Platform director of product management Dominic Preuss write today. “The addition of Alooma, subject to closing conditions, is a natural fit that allows us to offer customers a streamlined, automated migration experience to Google Cloud, and give them access to our full range of database services, from managed open source database offerings to solutions like Cloud Spanner and Cloud Bigtable.”

Before the acquisition, Alooma had raised about $15 million, including an $11.2 million Series A round led by Lightspeed Venture Partners and Sequoia Capital in early 2016. The two companies did not disclose the price of the acquisition, but chances are we are talking about a modest price, given how much Alooma had previously raised.

Before the acquisition, Alooma had raised about $15 million, including an $11.2 million Series A round led by Lightspeed Venture Partners and Sequoia Capital in early 2016. The two companies did not disclose the price of the acquisition, but chances are we are talking about a modest price, given how much Alooma had previously raised.

Neither Google nor Alooma said much about what will happen to the existing products and customers — and whether it will continue to support migrations to Google’s competitors. We’ve reached out to Google and will update this post once we hear more.

Update. Here is Google’s statement about the future of the platform:

For now, it’s business as usual for Alooma and Google Cloud as we await regulatory approvals and complete the deal. After close, the team will be joining us in our Tel Aviv and Sunnyvale offices, and we will be leveraging the Alooma technology and team to provide our Google Cloud customers with a great data migration service in the future.

Regarding supporting competitors, yes, the existing Alooma product will continue to support other cloud providers. We will only be accepting new customers that are migrating data to Google Cloud Platform, but existing customers will continue to have access to other cloud providers.

Alooma’s co-founders do stress, though, that “the journey is not over. Alooma has always aimed to provide the simplest and most efficient path toward standardizing enterprise data from every source and transforming it into actionable intelligence,” they write. “Joining Google Cloud will bring us one step closer to delivering a full self-service database migration experience bolstered by the power of their cloud technology, including analytics, security, AI, and machine learning.”

Powered by WPeMatico

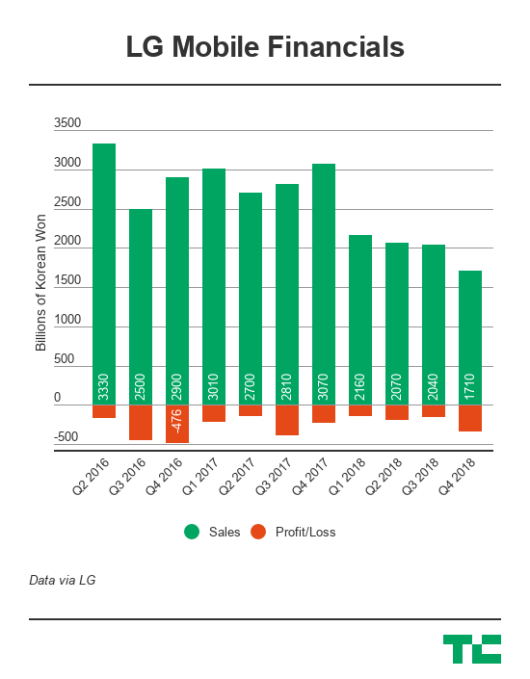

We’ve written extensively about LG’s struggling mobile business, which has suffered at the hands of aggressive Chinese Android makers, and now that unit has dragged its parent company into posting its first quarterly loss for two years.

The Korean electronics giant is generally in good health — it posted a $2.4 billion profit for 2018 — but its smartphone business’s failings saw it post a loss in Q4 2018, its first quarterly negative since Q4 2016.

Overall, the company posted a KRW 75.7 billion ($67.1 million) operating loss as revenue slid seven percent year-on-year to KRW 15.77 trillion ($13.99 billion). LG said the change was “primarily due to lower sales of mobile products.”

We’ve known for some time that LG’s mobile business is struggling — the division got another new head last November — but things went from bad to worse in Q4. LG Mobile saw revenue fall by 42 percent to reach KRW 1.71 trillion, $1.51 billion. The operating loss for the period grew to KRW 322.3 billion, or $289.8 million, from KRW 216.3 billion, $194 million, one year previous.

Over the full year, LG Mobile posted a $700 million loss (KRW 790.1 billion) but the company claimed things are improving thanks to “better material cost controls and overhead efficiencies based on the company’s platform modularization strategy.”

LG used CES to showcase a range of home entertainment products — that division is doing far better than mobile, with a record annual profit of $1.35 billion in 2018 — so we’ll have to wait until Mobile World Congress in February to see exactly what LG has in mind. Already, though, we have a suggestion, and it isn’t exactly set-the-world-on-fire stuff.

“LG’s mobile division will push 5G products and smartphones featuring different form factors while focusing on key markets where the LG brand remains strong,” the company said in a statement.

It will certainly take something very special to turn things around. It seems more likely that LG Mobile head Brian Kwon — who also heads up that hugely profitable home entertainment business — will focus on cutting costs and squeezing out the few sweet spots left. Continued losses, particularly against success from other units, might eventually see LG shutter its mobile business.

Still, things could be worse for LG — it could be HTC.

Powered by WPeMatico

Are more Theranos -style scandals looming for investors in healthcare startups?

A team of researchers associated with the Meta-Research Innovation Center at Stanford thinks so. They’ve published a paper warning investors in life sciences startups that a systemic lack of transparency exists in their portfolio companies — creating the possibility for more multi-billion-dollar implosions and scandals like the one that toppled Theranos and its charismatic founder, Elizabeth Holmes.

Indeed, one of the study’s authors, Dr. John Ioannidis, the co-director of the Meta-Research Innovation Center at Stanford and director of the University’s PhD program in Epidemiology and Clinical Research, was among the first people to identify the risks associated with Theranos and its “stealth research.”

Now Dr. Ioannidis and his co-authors, Ioana A. Cristea and Eli M. Cahan, have published a study surveying the publicly available research from the largest privately held companies in the healthcare space, and found them lacking.

Most of the highest-valued startups in healthcare have not published any significant scientific literature, the study found. Nearly half of the publications from companies worth more than $1 billion came from only two startups — 23andMe and Adaptive Biotechnologies, according to the paper.

“Many years ago I was the first person to say that Theranos had a problem,” says Ioannidis. “The problem that I had then was that Theranos did not have any peer-reviewed evidence to show.”

In an interview and in their paper, Ioannidis and Cahan warn that investors have overlooked systemic problems created by the lack of transparency among healthcare startups.

They write:

It would be tempting to dismiss the Theranos case as just one rotten apple. However, we worry that the focus on fraud puts aside a more fundamental concern. Fraud is making waves in the news, but stealth research may have a more detrimental impact.

According to the study’s findings, more than half of the healthcare startups that are worth more than $1 billion have published no highly cited papers at all. For companies that were acquired or are publicly traded that number is around 40 percent.

In all, healthcare startups that are currently valued at more than $1 billion published 425 Pubmed papers. And of those papers only 34 (8 percent, including two reviews) were highly cited. For companies with valuations of more than $1 billion that had been acquired or are publicly traded on stock exchanges, the researchers counted 413 papers, of which 47 (11 percent, including nine reviews) were highly cited.

Digging deeper into some of the companies that had high valuations but little or no published research revealed scores of operational and technological issues for the researchers.

For instance, StemCentrx, which was bought for $10.2 billion in 2016 by AbbVie, had published 16 papers — and only one highly cited paper. Since the acquisition, the Food and Drug Administration had imposed a delay on the readout of the company’s phase II trial for its Rova T targeted antibody drug for cancer treatment. In December, a Phase III trial for Rova T as a second-line treatment for patients with advanced small cell lung cancer was halted because the treatment wasn’t working, according to a report in Targeted Oncology.

Acerta Pharma, another healthcare-focused startup focused on cancer treatments, was bought by AstraZeneca for $7.3 billion. That company published nine articles and had one highly cited paper for a very early study of a potential treatment for relapsed chronic lymphocytic leukemia. Acerta received accelerated approval for a drug called acalabrutinib, which treats a rare form of lymphoma called mantle cell lymphoma. Two years ago, AstraZeneca had to retract data and admit that Acerta falsified preclinical data for its drug.

Then there’s Intarcia, the developer of a device for diabetes treatment that’s worth $5.5 billion. That company had its device rejected by the FDA and was forced to lay off staff and halt a couple of later-stage trials. It had only published six papers — none of them very highly cited.

Ultimately, the researchers concluded that highly valued healthcare startups don’t contribute to published research and that the valuation of these companies by investors is divorced from any externally validated data.

For the researchers (and for investors) this should present a problem.

“Many unicorns may be overvalued [21] and subject to unrealistic scientific expectations,” the study’s authors write. And they reject the argument that simply applying for — and receiving — patents is enough to prove that a technology in the healthcare space has been thoroughly vetted. “[Patents] do not offer the same level of documentation as peer-reviewed articles. For example, Theranos had over 100 patents [1], but these were unable to supplant the vacuum in their evidence,” the researchers wrote.

Even if companies want to protect their technology, there are still ways for them to be more transparent about the results or benefits of their technology. The authors acknowledge that publishing isn’t the primary mission of startups. They can, however publish a few high-value articles, secure their technology through patents and then work with researchers, universities or hospitals to validate the technology and have those organizations publish results of the tests, the authors argue.

As the authors conclude:

Start-ups are key purveyors of innovation and disruption. Consequently, holding them to a minimal standard of evaluation from the scientific community is crucial. Participation in peer review, with all its limitations, is the best way we have to uphold this standard. We are not arguing that start-ups should divert excessive resources to having peer-reviewed papers. However, when their products are destined to affect patient health, they should neither be solely doing marketing. Confidential data sharing with potential investors or regulators cannot replace more open scrutiny by the scientific community.

Powered by WPeMatico