coinbase

Auto Added by WPeMatico

Auto Added by WPeMatico

Before Ram Palaniappan founded Earnin, he developed a system for employees at a payments company called UniRush, where he spent eight years as president. If you needed money before payday, he would write you a check from his checking account and when payday rolled around, employees would reimburse him.

Despite being paid what Palaniappan thought were fair wages, his workers often found themselves in a bind, needing access to wages they couldn’t expect to see in their own bank accounts for days.

“This is such a core pain point,” Palaniappan told TechCrunch. “Over three-fourths of the country live paycheck to paycheck … It’s an issue of fairness. We all have gotten used to getting paid every two weeks, but most employees would rather be paid before they work.”

Palaniappan decided to transform what he had been doing as a favor to employees into a real business with Earnin (formerly known as Activehours), a startup that helps hourly, gig and salary workers track their earnings and transfer them to their checking accounts in real time using a mobile application. Today, the company is announcing a $125 million Series C funding from top-tier investors DST Global, Andreessen Horowitz, Spark Capital, Matrix Partners, March Capital Partners, Coatue Management and Ribbit Capital. Palaniappan declined to disclose the valuation.

Earnin founder and chief executive officer Ram Palaniappan

Here’s how it works: An employee signs up on the Earnin app and connects their bank account. Earnin infers the person’s pay cycle and debits their account the amount they’ve borrowed on their payday. Earnin charges no fees or interest; instead, it operates on a pay it forward revenue model some would balk at. Earnin users have the option to “tip” the app after each transaction and that tip, in turn, is used to fund the next user’s withdrawal. If a user tips more than Earnin thinks is reasonable for the given withdrawal, it will notify the user and give them the option to dial back the tip amount.

What the company has found is that users are usually more than happy to contribute to the Earnin community of workers.

“So often, people are trying to help each other out,” Palaniappan said. “That’s the most powerful piece — how much support the community is providing to each other.”

Earnin was launched in 2014 and has previously raised $65 million in venture capital funding. With the latest investment, it will expand its engineering and product teams across its offices in Palo Alto — where it’s headquartered — as well as in Cincinnati and Vancouver.

The app, often among the App Store’s top 10 financial apps, has more than 1 million downloads, the company says, and is used by employees at more than 50,000 companies — many of which check the app every day. Palaniappan says its users are working more than 15 million hours per week. If each user works an estimated 40 hours per week, that means the app has roughly 375,000 weekly active users.

He added that the startup’s growth in the last four years has been “quite remarkable.” Given the investor support it’s received, it’s likely to step into “unicorn” territory soon. Ribbit Capital, for example, is a leading fintech investing firm with capital invested in Coinbase, Revolut, Gusto, Wealthfront, NuBank, Brex and more.

Powered by WPeMatico

Coinbase acquired Earn.com for at least $120 million back in April. And the company now plans to transform Earn.com into Coinbase Earn, a website with educational content to learn more about cryptocurrencies. Users who complete those classes will earn tokens.

Coinbase bought Earn.com partly so that it could appoint Earn.com co-founder and CEO Balaji Srinivasan as Coinbase’s CTO. The previous iteration of Earn.com wasn’t a priority for Coinbase.

Earn.com started as a service where you can contact busy people for a small fee. Busy people would get paid in cryptocurrencies to accept those requests. The platform quickly became a way to massively contact Earn.com’s user base for initial coin offerings and airdrops.

Coinbase Earn is launching today in private beta. But at the time of this article, the new Coinbase Earn service is not live (Update: Coinbase Earn is now live and is a separate website from Earn.com). Some Coinbase users will receive an invitation to the service. The company says that educational content will go beyond Bitcoin and Ethereum. Developing education pages for obscure cryptocurrencies makes sense as Coinbase plans to add dozens of cryptocurrencies over the coming months.

At first, there is just one track. Users can learn more about 0x (ZRX), a protocol that lets you create decentralized exchanges. Cryptocurrency trades can be executed without a centralized exchange thanks to 0x .

0x content includes video lessons and quizzes — and yes, writing this makes me feel like it’s 2005 and webinars are cool again. Even if you’re not invited to Coinbase Earn, you can view the content. But those who are part of Coinbase Earn will receive a small amount of ZRX at the end of the track.

Coinbase had previously launched a learning hub to understand the basics of cryptocurrencies.

Disclosure: I own small amounts of various cryptocurrencies.

Powered by WPeMatico

It’s hard to believe that you still had to convert your BTC into USD in order to buy ETH on Coinbase. The company is finally adding direct cryptocurrency-to-cryptocurrency conversions.

The feature works with Bitcoin (BTC), Ethereum (ETH), Ethereum Classic (ETC), Litecoin (LTC), 0x (ZRX) and Bitcoin Cash (BCH). It is only available to U.S. customers for now, but the company plans to roll out the feature to other countries too.

Let’s look at the fees more closely. If you live in Europe or the U.S., every time you buy or sell cryptocurrencies using USD or EUR, you pay at least 1.49 percent in fees on top of the spread (the difference between the highest selling price and the lowest purchasing price). Fees are even higher if you’re using a credit or debit card.

Coinbase says that the spread between a fiat currency and a cryptocurrency should be around 0.5 percent but may vary depending on the trading pair and the order queue.

If you buy or sell less than 200 USD or equivalent, fees get much more expensive. For instance, a $10 order will generate $0.99 in fees, or 9.9 percent. Customers pay 3 percent in fees for a $100 order.

But the good news is that it’s a completely different story with token-to-token transactions. Coinbase doesn’t charge you any markup fee — but there’s some inevitable spread. And with some obscure trading pairs (exchanging ZRX for BCH for instance), you might end up paying around 1 percent in spread. Still, it’s a much better user experience for those who just want to trade on Coinbase.

Without even mentioning other exchanges, Coinbase Pro users have been able to trade between multiple cryptocurrencies for a long time. But Coinbase is still the entry gate for many new cryptocurrency users.

Powered by WPeMatico

A few weeks after Circle announced the launch of USD Coin (or USDC for short), Coinbase also announced that customers can now buy, sell, send and receive USDC on Coinbase. A USDC is a token that is worth exactly 1 USD. Its value is going to stay stable against USD — hence the name stablecoin for this type of coins.

Unlike traditional cryptocurrencies, you can be sure that the value of your USDC wallet isn’t going to fluctuate like crazy. It opens up new possibilities and use cases.

While Coinbase lets you hold USD in your Coinbase account, this isn’t safe. If somebody hacks into your account, you could end up with an empty wallet. That’s why you should always try to control the keys of your wallet and transfer your coins to a safer wallet, such as a Ledger wallet or at least a software solution like MyEtherWallet.

But if you want to short cryptocurrencies without sending your USD back to your bank account, you can now convert your tokens to USDC. This way, it’ll be easier to buy cryptocurrencies again in the future. And maybe you can avoid paying taxes by hiding your tokens from taxation authorities…

USDC also works just like a regular token. You just need a wallet address to send some USDC. USDC is an ERC-20 token, which means that it leverages the Ethereum blockchain and ecosystem.

But stablecoins need to be regulated more tightly. Circle, Coinbase and a bunch of other companies have created the CENTRE consortium to define the policies around stablecoins. For instance, if you want to handle stablecoins on your exchange, you need to send regular audited reports that prove that you have as many USD sitting on a bank account as issued tokens.

With both Coinbase and Circle on board, it’s clear that USDC is off to a good start. Now let’s see if there’s enough interest to create other stablecoins based on EUR, CNY and other fiat currencies.

Powered by WPeMatico

Watching the current price madness is scary. Bitcoin is falling and rising in $500 increments with regularity and Ethereum and its attendant ICOs are in a seeming freefall with a few “dead cat bounces” to keep things lively. What this signals is not that crypto is dead, however. It signals that the early, elated period of trading whose milestones including the launch of Coinbase and the growth of a vibrant (if often shady) professional ecosystem is over.

Crypto still runs on hype. Gemini announcing a stablecoin, the World Economic Forum saying something hopeful, someone else saying something less hopeful – all of these things and more are helping define the current market. However, something else is happening behind the scenes that is far more important.

As I’ve written before, the socialization and general acceptance of entrepreneurs and entrepreneurial pursuits is a very recent thing. In the old days – circa 2000 – building your own business was considered somehow sordid. Chancers who gave it a go were considered get-rich-quick schemers and worth of little more than derision.

As the dot-com market exploded, however, building your own business wasn’t so wacky. But to do it required the imprimaturs and resources of major corporations – Microsoft, Sun, HP, Sybase, etc. – or a connection to academia – Google, Netscape, Yahoo, etc. You didn’t just quit school, buy a laptop, and start Snapchat.

It took a full decade of steady change to make the revolutionary thought that school wasn’t so great and that money was available for all good ideas to take hold. And take hold it did. We owe the success of TechCrunch and Disrupt to that idea and I’ve always said that TC was career pornography for the cubicle dweller, a guilty pleasure for folks who knew there was something better out there and, with the right prodding, they knew they could achieve it.

So in looking at the crypto markets currently we must look at the dot-com markets circa 1999. Massive infrastructure changes, some brought about by Y2K, had computerized nearly every industry. GenXers born in the late 70s and early 80s were in the marketplace of ideas with an understanding of the Internet the oldsters at the helm of media, research, and banking didn’t have. It was a massive wealth transfer from the middle managers who pushed paper since 1950 to the dot-com CEOs who pushed bits with native ease.

Fast forward to today and we see much of the same thing. Blockchain natives boast about having been interest in bitcoin since 2014. Oldsters at banks realize they should get in on things sooner than later and price manipulation is rampant simply because it is easy. The projects we see now are the Kozmo.com of the blockchain era, pie-in-the-sky dream projects that are sucking up millions in funding and will produce little in real terms. But for every hundred Kozmos there is one Amazon .

And that’s what you have to look for.

Will nearly every ICO launched in the last few years fail? Yes. Does it matter?

Not much.

The market is currently eating its young. Early investors made (and probably lost) millions on early ICOs but the resulting noise has created an environment where the best and brightest technical minds are faced with not only creating a technical product but also maintaining a monetary system. There is no need for a smart founder to have to worry about token price but here we are. Most technical CEOs step aside or call for outside help after their IPO, a fact that points to the complexity of managing shareholder expectations. But what happens when your shareholders are 16-year-olds with a lot of Ethereum in a Discord channel? What happens when little Malta becomes the de facto launching spot for token sales and you’re based in Nebraska? What happens when the SEC, FINRA, and Attorneys General from here to Beijing start investigating your hobby?

Basically your hobby stops becoming a hobby. Crypto and blockchain has weaponized nerds in an unprecedented way. In the past if you were a Linux developer or knew a few things about hardware you could build a business and make a little money. Now you can build an empire and make a lot of money.

Crypto is falling because the people in it for the short term are leaving. Long term players – the Amazons of the space – have yet to be identified. Ultimately we are going to face a compression in the ICO and, for a while, it’s going to be a lot harder to build an ICO. But give it a few years – once the various financial authorities get around to reading the Satoshi white paper – and you’ll see a sea change. Coverage will change. Services will change. And the way you raise money will change.

VC used to be about a team and a dream. Now it’s about a team, $1 million in monthly revenue, and a dream. The risk takers are gone. The dentists from Omaha who once visited accelerator demo days and wrote $25,000 checks for new apps are too shy to leave their offices. The flashy VCs from Sand Hill have to keep Uber and Airbnb’s plates spinning until they can cash out. VC is dead for the small entrepreneur.

Which is why the ICO is so important and this is why the ICO is such a mess right now. Because everybody sees the value but nobody – not the SEC, not the investors, not the founders – can understand how to do it right. There is no SAFE note for crypto. There are no serious accelerators. And all of the big names in crypto are either goldbugs, weirdos, or Redditors. No one has tamed the Wild West.

They will.

And when they do expect a whole new crop of Amazons, Ubers, and Oracles. Because the technology changes quickly when there’s money, talent, and a way to marry the two in which everyone wins.

Powered by WPeMatico

Brian Armstrong, the CEO of cryptocurrency trading platform Coinbase, wants to take his company public — maybe on the blockchain.

Onstage at TechCrunch Disrupt SF 2018, Armstrong dished on his ambitions for the future of Coinbase.

“We are self-sustaining,” Armstrong said. “You know, we’ve been profitable for quite a while. We don’t have any plans to raise additional capital at this point, but never say never … Someday I’d love to run a public company.”

Armstrong didn’t rule out going public on the blockchain. He said he’s even considered going public on his own platform.

“I think it would be very on mission for us to do that because, of course, we are creating an open financial system,” he said. “Companies could list their stock, which are really tokens, and instead of a cap table, you tokenize the cap table. But I don’t have any decisions on that to share at the moment.”

An innovative exit would be very on-brand for Coinbase. As one of the earliest players in crypto-mania, the company has certainly had to make things up as it goes. It’s worked, as Armstrong said; the company is profitable and was the first-ever cryptocurrency startup to garner a billion-dollar valuation.

Founded in 2012, Coinbase is backed by IVP, Spark Capital, Greylock Partners, Battery Ventures, Section 32, Draper Associates and more. The company was valued at $1.6 billion in August 2017 with a $100 million Series D last year. The financing was reportedly the largest-ever for a crypto startup.

Watch the full interview with Brian Armstrong below.

Powered by WPeMatico

A year ago I felt a panic that still reverberates in me today. Hackers swapped my T-Mobile SIM card without my approval and methodically shut down access to most of my accounts and began reaching out to my Facebook friends asking to borrow crypto. Their social engineering tactics, to be clear, were laughable but they could have been catastrophic if my friends were less savvy.

Flash forward a year and the same thing happened to me again – my LTE coverage winked out at about 9pm and it appeared that my phone was disconnected from the network. Panicked, I rushed to my computer to try to salvage everything I could before more damage occurred. It was a false alarm but my pulse went up and I broke out in a cold sweat. I had dealt with this once before and didn’t want to deal with it again.

Sadly, I probably will. And you will, too. The SIM card swap hack is still alive and well and points to one and only one solution: keeping your crypto (and almost your entire life) offline.

Stories about massive SIM-based hacks are all over. Most recently a crypto PR rep and investor, Michael Terpin, lost $24 million to hackers who swapped his AT&T SIM. Terpin is suing the carrier for $224 million. This move, which could set a frightening precedent for carriers, accuses AT&T of “fraud and gross negligence.”

From Krebs:

Terpin alleges that on January 7, 2018, someone requested an unauthorized SIM swap on his AT&T account, causing his phone to go dead and sending all incoming texts and phone calls to a device the attackers controlled. Armed with that access, the intruders were able to reset credentials tied to his cryptocurrency accounts and siphon nearly $24 million worth of digital currencies.

While we can wonder in disbelief at a crypto investor who keeps his cash in an online wallet secured by text message, how many other services do we use that depend on emails or text messages, two vectors easily hackable by SIM spoofing attacks? How many of us would be resistant to the techniques that nabbed Terpin?

Another crypto owner, Namek Zu’bi, lost access to his Coinbase account after hackers swapped his SIM, logged into his account, and changed his email while attempting direct debits to his bank account.

“When the hackers took over my account they attempted direct debits into the account. But because I blocked my bank accounts before they could it seems there are bank chargebacks on that account. So Coinbase is essentially telling me sorry you can’t recover your account and we can’t help you but if you do want to use the account you owe $3K in bank chargebacks,” he said.

Now Zu’bi is facing a different issue: Coinbase is accusing him of being $3,000 in arrears and will not give him access to his account because he cannot reply from the hacker’s email.

“I tried to work with coinbase hotline who is supposed to help with this but they were clueless even after I told them that the hackerchanged email address on my original account and then created a new account with my email address. Since then I’ve been waiting for a ‘specialist’ to email me (was supposed to be 4 business days it’s been 8 days) and I’m still locked out of my account because Coinbase support can’t verify me,” he said.

It has been a frustrating ride.

“As an avid supporter and investor in crypto it baffles me how one of the market leaders who just supposedly launched institutional grade custody solutions can barely deal with a basic account take-over fraud,” Zu’bi said.

I’ve been using Trezor hardware wallets for a while, storing them in safe places outside of my home and maintaining a separate record of the seeds in another location. I have very little crypto but even for a fraction of a few BTC it just makes sense to practice safe storage. Ultimately, if you own crypto you are now your own bank. That you would trust anyone – including a fiat bank – to keep your digital currency safe is deeply delusional. Heck, I barely trust Trezor and they seem like the only solution for safe storage right now.

When I was first hacked I posted recommendations by crypto exchange Kraken. They are still applicable today:

Call your telco and:

Set a passcode/PIN on your account

- Make sure it applies to ALL account changes

- Make sure it applies to all numbers on the account

- Ask them what happens if you forget the passcode

- Ask them what happens if you lose that too

Institute a port freeze

Institute a SIM lock

Add a high-risk flag

Close your online web-based management account

Block future registration to online management system

Hack yo’ self

See what information they will leak

See what account changes you can make

They also recommend changing your telco email to something wildly inappropriate and using a burner phone or Google Voice number that is completely disconnected from your regular accounts as a sort of blind for your two factor texts and alerts.

Sadly, doing all of these things is quite difficult. Further, carriers don’t make it easy. In May a 27-year-old man named Paul Rosenzweig fell victim to a SIM-swapping hack even though he had SIM lock installed on his account. A rogue T-Mobile employee bypassed the security, resulting in the loss of a unique three character Twitter and Snapchat account.

Ultimately nothing is secure. The bottom line is simple: if you’re in crypto expect to be hacked and expect it to be painful and frustrating. What you do now – setting up real two-factory security, offloading your crypto onto physical hardware, making diligent backups, and protecting your keys – will make things far better for you in the long run. Ultimately, you don’t want to wake up one morning with your phone off and all of your crypto siphoned off into the pocket of a college kid like Joel Ortiz, a hacker who is now facing jail time for “13 counts of identity theft, 13 counts of hacking, and two counts of grand theft.” Sadly, none of the crypto he stole has surfaced after his arrest.

Powered by WPeMatico

Coinbase wants to be Facebook Connect for crypto. The blockchain giant plans to develop “Login with Coinbase” or a similar identity platform for decentralized app developers to make it much easier for users to sign up and connect their crypto wallets. To fuel that platform, today Coinbase announced it has acquired Distributed Systems, a startup founded in 2015 that was building an identity standard for dApps called the Clear Protocol.

The five-person Distributed Systems team and its technology will join Coinbase. Three of the team members will work with Coinbase’s Toshi decentralized mobile browser team, while CEO Nikhil Srinivasan and his co-founder Alex Kern are forming the new decentralized identity team that will work on the Login with Coinbase product. They’ll be building it atop the “know your customer” anti-money laundering data Coinbase has on its 20 million customers. Srinivasan tells me the goal is to figure out “How can we allow that really rich identity data to enable a new class of applications?”

Distributed Systems had raised a $1.7 million seed round last year led by Floodgate and was considering raising a $4 million to $8 million round this summer. But Srinivasan says, “No one really understood what we’re building,” and it wanted a partner with KYC data. It began talking to Coinbase Ventures about an investment, but after they saw Distributed Systems’ progress and vision, “they quickly tried to move to find a way to acquire us.”

Distributed Systems began to hold acquisition talks with multiple major players in the blockchain space, and the CEO tells me it was deciding between going to “Facebook, or Robinhood, or Binance, or Coinbase,” having been in formal talks with at least one of the first three. Of Coinbase the CEO said, they “were able to convince us they were making big bets, weaving identity across their products.” The financial terms of the deal weren’t disclosed.

Coinbase’s plan to roll out the Login with Coinbase-style platform is an SDK that others apps could integrate, though that won’t necessarily be the feature’s name. That mimics the way Facebook colonized the web with its SDK and login buttons that splashed its brand in front of tons of new and existing users. This turned Facebook into a fundamental identity utility beyond its social network.

Developers eager to improve conversions on their signup flow could turn to Coinbase instead of requiring users to set up whole new accounts and deal with crypto-specific headaches of complicated keys and procedures for connecting their wallet to make payments. One prominent dApp developer told me yesterday that forcing users to set up the MetaMask browser extension for identity was the part of their signup flow where they’re losing the most people.

This morning Coinbase CEO Brian Armstrong confirmed these plans to work on an identity SDK. When Coinbase investor Garry Tan of Initialized Capital wrote that “The main issue preventing dApp adoption is lack of native SDK so you can just download a mobile app and a clean fiat to crypto in one clean UX. Still have to download a browser plugin and transfer Eth to Metamask for now Too much friction,” Armstrong replied “On it :)”

On it 🙂

— Brian Armstrong (@brian_armstrong) August 15, 2018

In effect, Coinbase and Distributed Systems could build a safer version of identity than we get offline. As soon as you give your Social Security number to someone or it gets stolen, it can be used anywhere without your consent, and that leads to identity theft. Coinbase wants to build a vision of identity where you can connect to decentralized apps while retaining control. “Decentralized identity will let you prove that you own an identity, or that you have a relationship with the Social Security Administration, without making a copy of that identity,” writes Coinbase’s PM for identity B. Byrne, who’ll oversee Srinivasan’s new decentralized identity team. “If you stretch your imagination a little further, you can imagine this applying to your photos, social media posts, and maybe one day your passport too.”

Considering Distributed Systems and Coinbase are following the Facebook playbook, they may soon have competition from the social network. It’s spun up its own blockchain team and an identity and single sign-on platform for dApps is one of the products I think Facebook is most likely to build. But given Coinbase’s strong reputation in the blockchain industry and its massive head start in terms of registered crypto users, today’s acquisition well position it to be how we connect our offline identity with the rising decentralized economy.

Powered by WPeMatico

Facebook is invading the blockchain, but how? Back in May, Facebook formed a cryptocurrency team to explore the possibilities, and today it removed a roadblock to revealing its secret plans.

Former head of Messenger David Marcus, who leads the Facebook Crypto team, today announced he was stepping down from the board of Coinbase, the biggest crypto startup. Marcus was formerly the president of PayPal and helped Facebook Messenger adopt chatbot commerce and peer-to-peer payments, so he was both a natural choice for Coinbase’s board and Facebook’s blockchain skunklabs.

Facebook told CoinDesk this was to avoid the appearance of a conflict of interest, which is exactly what it was. Marcus provided a statement to TechCrunch explaining he was stepping down “because of the new group I’m setting up at Facebook around blockchain,” noting that “Getting to know Brian [Armstrong, CEO of Coinbase], who’s become a friend, and the whole Coinbase leadership team and board has been an immense privilege. I’ve been thoroughly impressed by the talent and execution the team has demonstrated during my tenure, and I wish the team all the success it deserves going forward.”

Now Facebook is cleared to start publicly talking about its plans, though it hasn’t yet. “We are still in the very early stages and we are considering a number of different applications for the blockchain. But we don’t have anything else to share at this time,” a Facebook spokesperson tells me. So what could Facebook be building? I see three main consumer-facing opportunities.

Facebook could build a cryptocurrency wallet with its own token that people could use to pay for things with partnered businesses or that they discover through Facebook ads. Because blockchain can make transactions free or very cheap, Facebook and its partners could sidestep the typical credit card processing fees. That would potentially allow Facebook to offer users “3% off purchases made with FaceCoin” or a similar promotion.

Discounts like this could draw users into Facebook’s cryptocurrency feature. It’s well-positioned to run such a scheme thanks to its extensive connections with more than six million advertisers and 65 million businesses that have Facebook Pages. The social network could eat the costs of running the program, passing the transaction fee savings on to the users, while touting partnerships with Facebook Crypto as ways to boost sales for businesses. That could in turn get clients to spend more money on Facebook ads, as the discounts would enhance conversion rates and drive sales.

One thing we know for sure is that Facebook won’t be building on the Stellar protocol. Facebook debunked a Business Insider report saying it was, telling TechCrunch it was not in talks with Stellar or planning to build on it.

Facebook already lets you send friends money through Messenger for free, but only with a connected debit card or PayPal account. Facebook could offer cryptocurrency-based payments between friends to let a wider range of users settle debts for shared dinners or taxis through Messenger. Users might fund their Facebook Crypto wallet once with a payment, possibly with a one-time transaction fee, and then they could send and receive the tokens for free from then on. Blockchain becoming the backbone of peer-to-peer payments could further increase engagement with Messenger for its 1.3 billion users.

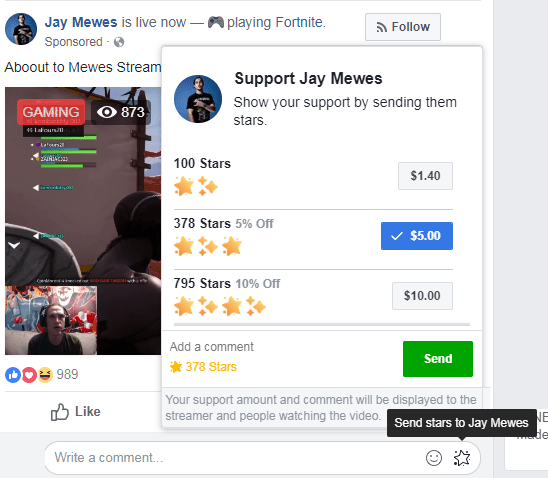

Meanwhile, Facebook could also potentially use cryptocurrency to let fans send micropayments to their favorite creators, like video stars and game streamers. Facebook recently debuted its own virtual (not crypto) currency, called Facebook Stars, that users can buy and send to creators, who can then cash them out for one cent each. Facebook takes an undisclosed cut, but gives to the creator the majority of what users spend on Stars.

Facebook could potentially undergird this system with cryptocurrency to alleviate transaction fees and let people tip creators smaller amounts of cash for exclusive content or just to show their appreciation. Facebook started with a minimum of $3 tips at a time so that transaction fees wouldn’t be too high of a percentage of the total purchase. A cryptocurrency solution could let users efficiently tip much smaller amounts, which could lure people toward the behavior. The more money Facebook can deliver to internet celebrities, the more popular ones it can recruit to live on its platform and the more content they’ll produce.

Facebook Stars. Image via KiwiFarm

A top problem in the world of decentralized blockchain apps is how you bring your identity with you. Securely connecting your wallet, blockchain-based virtual goods and biographical info to new dApps can be a laborious process. Users typically have to type in long, complicated alphanumeric keys that are tough to remember and annoying to input. User experience design around identity in the blockchain space lags far behind what we’re used to with mainstream social apps like Facebook Connect, which uses a OAuth single sign-on to let you instantly join apps without creating a new username and password, or filling out a profile and uploading a photo.

Facebook could use its expertise in operating a popular identity platform to ease login to dApps. While the company has faced plenty of privacy issues and attacks on election integrity, Facebook has a strong record of not being traditionally hacked. It hasn’t suffered a massive user data breach like LinkedIn, Twitter and other social networks. Using an overtly centralized identity system to connect with decentralized apps might be counterintuitive, but Facebook could deliver the UX convenience necessary to unlock a new wave of blockchain utility.

For now it’s unclear if Facebook will end up directly competing with Coinbase in the exchange and wallet space, or if it might instead partner with the blockchain mainstay to accelerate its efforts. And on the enterprise engineering side, Facebook could build some decentralized storage infrastructure to cut its massive server bills. But with deep pockets, tons of tech talent and ubiquity amongsts social networkers and businesses, Facebook Crypto’s primary limits are its ambitions and the extent of user trust.

Powered by WPeMatico

Centralized crypto exchanges like Coinbase are easy but expensive because they introduce a middleman. Not-for-profit project 0x allows any developer to quickly build their own decentralized cryptocurrency exchange and decide their own fees. It acts like Craigslist, connecting traders without ever holding the tokens itself. And instead of having to bootstrap their way to enough users trading tokens on their app alone so that there’s liquidity, 0x offers cross-platform liquidity between users on the different projects it powers.

The problem is the user experience of decentralized apps is often crappy compared to the consumer apps we’re used to across the rest of tech. From sign-in to recovering accounts to conducting transactions, it’s a lot more complicated than Facebook Login, PayPal, or Shopify. Bitcoin and Ethereum prices remain well below half their peaks because it’s difficult to do much with cryptocurrency right now. Until the decentralized infrastructure improves, the dreams of how blockchains can improve the world remain distant.

0x is trying to fix that by ensuring developers all don’t have to reinvent the exchange wheel.

It began as a for-profit exchange before the team recognized the massive usability gap. So instead it became a decentralized exchange protocol, and raised $24 million in an ICO for its ZRX token. That’s how relayers — the apps who use it to build exchanges for ERC20 tokens atop the Ethereum blockchain — can charge fees. It also gives those who collect the most a say in the governance of the protocol.

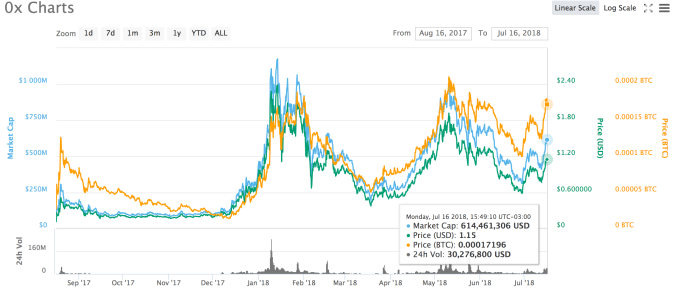

Some of the top projects on 0x like Augur and Dydx are going strong. Last week Coinbase announced it was exploring whether it might list ZRX and several other currencies for trade on its exchange, helping perk up the price after declines since the new year.

0x’s ZRX token price, via CoinMarketCap

Now 0x is putting some of its $24 million to work. It just hired former Facebook designer Chris Kalani to help it improve the usability of its APIs and the products built on top of them. His skills helped Facebook embrace mobile around its 2012 IPO. He then built Wake, raising $3.8 million for the design prototype sharing tool that let teams get instant feedback on their works-in-progress. Kalani sold Wake to design platform InVision in April, and after a few months assisting the transition, he’s joined 0x.

“There are very few designers involved in the [blockchain] space” Kalani tells me. “There’s not a lot of people who had worked on anything at a large-scale or from the consumer perspective. We’re focused on making crypto more approachable.”

After talking to four leaders in different parts of the blockchain industry, the consensus was that 0x was an elegant protocol for spawning decentralized exchanges. But the question kept coming up about whether the project will be sustainable. The company doesn’t have to earn enormous amounts of revenue, but concerns about its longevity could scare away developers. One, who asked to remain anonymous, described 0x saying, “the best analogy is trying to monetize Linux.”

After talking to four leaders in different parts of the blockchain industry, the consensus was that 0x was an elegant protocol for spawning decentralized exchanges. But the question kept coming up about whether the project will be sustainable. The company doesn’t have to earn enormous amounts of revenue, but concerns about its longevity could scare away developers. One, who asked to remain anonymous, described 0x saying, “the best analogy is trying to monetize Linux.”

0x is open source, so it could be forked so developers can sidestep ZRX. 0x hopes that the shared liquidity feature will keep developers in line. It only works with the unforked version, and is now being used by 0x-powered projects, including Radar Relay, ERC dEX, Shark Relay, Bamboo Relay and LedgerDex.

While some centralized exchanges have suffered security troubles and hacks, those with stronger records like Coinbase continue to thrive while banking off high fees. That in turn lets them offer better liquidity and invest more in the user experience, widening the gap versus decentralized apps. “People trust Coinbase with large amounts of capital but they wouldn’t trust themselves,” Kalani admits. But he thinks it’s early in the game, and as users become more knowledgeable and comfortable with holding their own tokens for use on decentralized exchanges, 0x and ZRX will thrive.

There’s also competition within the decentralized exchange space from Kyber’s liquidity network, and AirSwap’s peer-to-peer exchange marketplace. But for any of these to thrive, the mainstream crypto owner will have to get better educated. That could fall to 0x.

One alternative path for the not-for-profit would be selling developer services and consulting to those building on top of it. Or it could always do another ICO. But for now, there are a lot of projects out there that don’t want to foot the upfront cost to build their own secure and compliant exchange from scratch. Kalani concludes, “The way Stripe allowed developers and businesses to build on top of it, and not have to worry about regulatory issues and all the infrastructure necessary to take payments, I think 0x is going to do something similar with exchanges for crypto.”

Powered by WPeMatico