coinbase

Auto Added by WPeMatico

Auto Added by WPeMatico

“Most of the startups I give advice to about how to raise venture capital shouldn’t be raising venture capital,” an investor recently told me. While the idea that every startup isn’t venture-backable might run counter to the narrative to the barrage of funding news each week, I think it’s important to double click on the topic. Plus, it keeps coming up, off the record, on phone calls with investors!

As venture grows as an asset class, the access to capital has broadened from a dollar perspective, but I do think the difficulties that remain is an important dynamic to call out (and something no one talks about during an upmarket). Beyond the fact that only a small subset of startups truly can pull off scaling to the point of venture-level returns, it is still hard for even qualified founders to raise venture capital. Venture capital is still a heavily white, male-led industry, and as a result contains bias that disproportionately limits access for underrepresented founders.

Eniac founding partner Hadley Harris applied this dynamic to the current market boom in a recent tweet: A lot of people are misunderstanding this VC funding market. More money is flowing into the market but the increase is not evenly distributed. The market believes winners can be much bigger but not necessary that there will be more winners. It’s still very hard for most to raise a VC.

To say otherwise is to gaslight the early-stage or first-time founders that have spent months and months trying to raise their first institutional dollars and failed. So ask yourself: Seed rounds have indeed grown bigger, but for who? What comes at the cost of the $30 million seed round? Are the founders that can raise overnight from diverse backgrounds? Are investors backing first-time founders as much as they are backing second- or third-time entrepreneurs?

The answers might leave you debating about the boundaries, and limitations, of the upcoming hot-deal summer.

A few weeks ago, I wrote about the disconnect between due diligence and fundraising right now. Now we’ve moved onto the disconnect, and bifurcation, within first-check fundraising itself. There is so much more we can get into about the fallacy of “democratization” in venture capital, from who gets to start a rolling fund to the lack of assurance within equity crowdfunding campaigns.

We’ll get through it all together, and in the meantime make sure to follow me on Twitter @nmasc_ for more hot takes throughout the week.

In the rest of this newsletter, we will talk about fintech politics, the Affirm model with a twist, and sneakers-as-a-service.

The inimitable Mary Ann Azevedo has been dominating the fintech beat for us, covering everything from the latest Uruguayan unicorn to Acorn’s scoop of a debt management startup. But the story I want to focus on this week is her interview with ex-Coinbase counsel & former Treasury official, Brian Brooks.

Here’s what to know: Coinbase CEO Brian Armstrong notoriously released a memo last year denouncing political activism at work, calling it a distraction. In this exclusive interview, Brooks spoke about how blockchain is the answer to financial inclusion, and argued why politics needs to be taken out of tech.

We don’t want bank CEOs making those decisions for us as a society, in terms of who they choose to lend money to, or not. We need to take the politics out of tech. All of us do a lot of different things, and we have no idea on a given day, whether what we’re doing is popular with our neighbors or popular with our bank president or not. I don’t want the fact that I sometimes feel Republican to be a reason why my local bank president can deny me a mortgage.

Image Credits: Bryce Durbin/TechCrunch

While Affirm may have popularized the “buy now, pay later” model, the consumer-friendly business strategy still has room to be niched down into specific subsectors. I ran into one such startup when covering Plaid’s inaugural cohort of startups in its accelerator program.

Here’s what to know: Walnut is a new seed-stage startup that is a point-of-sale loan company with a healthcare twist. Unlike Affirm, it doesn’t make money off of fees charged to consumers.

Image Credits: Bryce Durbin/TechCrunch

Everything you could ever want to know about StockX

In our latest EC-1, reporter Rae Witte has covered a startup that leads one of the most complex and culturally relevant marketplaces in the world: sneakers.

Here’s what to know: StockX, in her words, has built a stock market of hype, and her series goes into its origin story, authentication processes and a market map.

Image Credits: Nigel Sussman

Found, a new podcast joining the TechCrunch network, has officially launched! The Equity team got a behind-the-scenes look at what triggered the new podcast, the first guests and goals of the show. Make sure to tune into the first episode.

Also, if you run into any paywalls while browsing today’s newsletter, make sure to use discount code STARTUPSWEEKLY to get 25% off an annual or two-year Extra Crunch subscription.

Seen on TechCrunch

Okta launches a new free developer plan

New Jersey announces $10M seed fund aimed at Black and Latinx founders

Education nonprofit Edraak ignored a student data leak for two months

6 VCs talk the future of Austin’s exploding startup ecosystem

Dear Sophie: Help! My H-1B wasn’t chosen!

Seen on Extra Crunch

5 machine learning essentials nontechnical leaders need to understand

How we dodged risks and raised millions for our open-source machine language startup

Giving EV batteries a second life for sustainability and profit

And that’s a wrap! Thanks for making it this far, and now I dare you to go make the most out of the rest of your day. And by make the most, I mean listen to Taylor’s Version.

Warmly,

Powered by WPeMatico

Today Coinbase, an American cryptocurrency trading platform and software company, said that it will begin to trade via a direct listing on April 14th. In a separate release the company also said that it will provide a financial update on April 6th, after the close of trading.

Coinbase’s impending public debut comes at an interesting market moment. As some tech companies delay their offerings over demand concerns, Coinbase is pushing ahead with its flotation perhaps in part because it will not price its debut in the traditional sense; direct listings forgo raising capital at a specific price point, and instead merely begin to trade, albeit with a reference price attached.

That Coinbase will release new numbers before beginning to trade is at once interesting and pedestrian. It’s interesting as TechCrunch cannot recall a private company looking to go public holding a similar event. And, Coinbase deciding to share “first quarter 2021 estimated results” and “provide a financial outlook for 2021” is also in part a common move, as many companies provide updated financials in their S-1 documents if time passes from when they first file to when they actually trade.

We’ll be tuned into that call, as the numbers shared will impact not only how Coinbase trades when it does float, but will also provide insight into how active consumer trading is writ large, and particularly in the cryptocurrency space; more than one startup in the market today depends on trading incomes to generate top-line, so seeing new numbers from Coinbase will be welcome.

The company will trade under the ticker symbol “COIN.”

Powered by WPeMatico

What happens to hot fintech startups that have benefited from a rise in consumer trading activity if regular folks lose interest in financial wagers?

That’s the question facing Robinhood, Coinbase and other trading platforms that have ridden an upward cycle. Each has performed well in recent quarters: Robinhood by securing huge payment-for-order-flow revenues, while Coinbase’s trading fees have proven incredibly lucrative, something we learned when it filed to go public.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

According to recent reporting, the consumer trading frenzy could be slowing: Bloomberg recently noted that options trading volume is slipping, Robinhood’s app store ranking is falling, and some alternative assets are also losing steam. Other reporting from the publication notes that many SPAC shares are underwater while Google trends data indicates falling consumer trading interest, perhaps limiting the inflow of new users for equities-focused apps.

There are other indications that the red-hot speculative consumer market is cooling. Bitcoin is off around 10% in the last week after a blistering rise in recent quarters. Hot stocks like Peloton, once a darling of traders, fell more than 10% yesterday alone.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

There’s a historical precedent for such declines. Coinbase’s historical revenues, to pick an example, have proved variable based on consumer interest in cryptocurrencies, with the company benefiting from rising demand and trading activity and seeing its top line decline in periods of restrained enthusiasm.

Robinhood and its fellow free trading apps have yet to undergo a similar rise-and-fall in trading volume, I’d reckon. At least of the sort of extreme up-and-down that Coinbase endured after the 2017-2018 bitcoin boom. Our question is, what would happen to Robinhood and its cohorts if the apparent cooling in consumer trading demand continues? Let’s talk about it.

Coinbase was a famously lucrative organization during the 2017-2018 bitcoin boom.

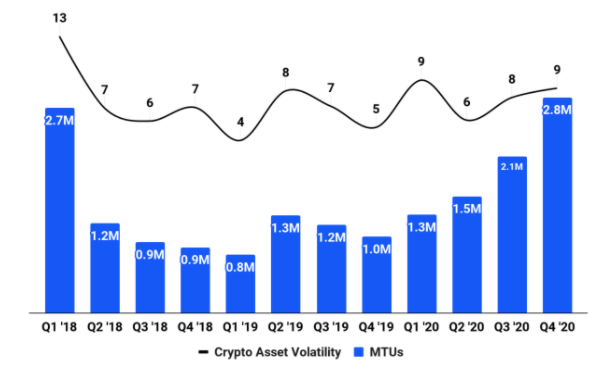

Indeed, we can see from the following chart from its S-1 filing that the company’s monthly transacting users (MTUs) dropped sharply into 2018. The percentage decline from 2.7 million to 800,000 is just over 70%.

Image Credits: Coinbase

And in case you think we’re being rude, we have a related chart from the same SEC filing that shows trading volume falling over the same period, not merely MTUs. We’re not picking a loose proxy to merely infer that trading revenue dipped at Coinbase. We can show it:

Powered by WPeMatico

A big story in the finance world this morning is that the Nasdaq composite index lost ground in pre-market trading while bond yields rose. The concern is that inflation could rise, which led to bonds selling off and falling valuations for expensive stocks. So, tech stocks were broadly lower this morning.

Unlike last night, when New York-based restaurant software company Olo priced its IPO at $25 per share, sharply above its raised IPO target price range.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, we’re checking in on the price investors paid for a block of Olo shares before it began trading. The resulting valuation and its new revenue multiples will help us answer several questions.

First, how hot is the market for high-growth tech shares that also feature profitability? And, second, is Olo pricing ahead of, or behind, known comps? If the latter is true, it could point to a cooling enthusiasm among public investors for tech IPOs, even if the headline numbers coming from the Olo IPO are impressive.

First, how hot is the market for high-growth tech shares that also feature profitability? And, second, is Olo pricing ahead of, or behind, known comps? If the latter is true, it could point to a cooling enthusiasm among public investors for tech IPOs, even if the headline numbers coming from the Olo IPO are impressive.

Then we’re going to chat about Coinbase’s latest S-1/A filing, which helps provide a bit of guidance regarding how its direct listing is scooting along.

Ready to get caught up on the public-private divide that the most successful startups cross? Let’s get into it!

As a quick reminder, Olo initially targeted a $16 to $18 per-share IPO price interval. That was raised, as expected, to $20 to $22 per share. Pricing at $25, then, is a strong 56.25% greater per-share value than the low end of the company’s first estimate.

As Olo featured rapid growth (an acceleration in year-over-year revenue from 59.4% in 2019 to 94.2% in 2020), and GAAP profits (a 2019-era net loss of $8.3 million became 2020 net income of $3.1 million) in its IPO filings, the first price range it rolled out felt a bit light. The second, however, felt more appropriate.

At $25 per share, we have to do new math. Using a simple share count inclusive of the company’s underwriters’ option, Olo is worth $3.62 billion. That figure swells to $4.6 billion when a fully diluted valuation is calculated, per IPO watch group Renaissance Capital.

Powered by WPeMatico

Data is a gold mine for a company.

If managed well, it provides the clarity and insights that lead to better decision-making at scale, in addition to an important tool to hold everyone accountable.

However, most companies are stuck in Data 1.0, which means they are leveraging data as a manual and reactive service. Some have started moving to Data 2.0, which employs simple automation to improve team productivity. The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation. This is our journey to Data 3.0.

The complexity of crypto data has opened up new opportunities in data, namely to move to the new frontier of Data 3.0, where you can scale value creation through systematic intelligence and automation.

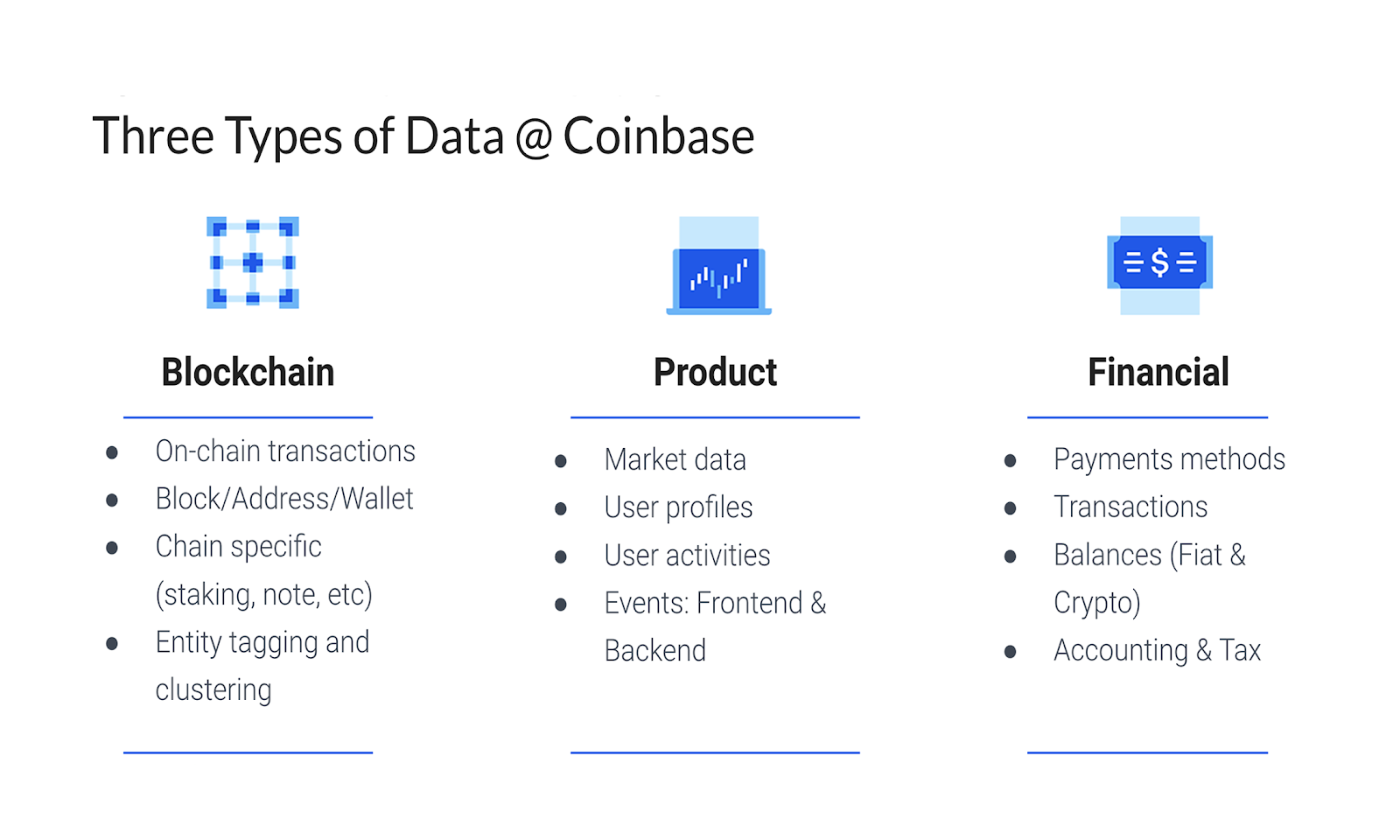

Coinbase is neither a finance company nor a tech company — it’s a crypto company. This distinction has big implications for how we work with data. As a crypto company, we work with three major types of data (instead of the usual one or two types of data), each of which is complex and varied:

Image Credits: Michael Li/Coinbase

Our focus has been on how we can scale value creation by making this varied data work together, eliminating data silos, solving issues before they start and creating opportunities for Coinbase that wouldn’t exist otherwise.

Having worked at tech companies like LinkedIn and eBay, and also those in the finance sector, including Capital One, I’ve observed firsthand the evolution from Data 1.0 to Data 3.0. In Data 1.0, data is seen as a reactive function providing ad-hoc manual services or firefighting in urgent situations.

Powered by WPeMatico

Eco, which has built out a digital global cryptocurrency platform, announced Friday that it has raised $26 million in a funding round led by a16z Crypto.

Founded in 2018, the SF-based startup’s platform is designed to be used as a payment tool around the world for daily-use transactions. The company emphasizes that it’s “not a bank, checking account, or credit card.”

“We’re building something better than all of those combined,” it said in a blog post. The company’s mission has also been described as an effort to use cryptocurrency as a way “to marry savings and spending,” according to this CoinList article.

Eco users can earn up to 5% annually on their deposits and get 5% cash back when transacting with merchants such as Amazon, Uber and others. Next up: The company says it will give its users the ability to pay bills, pay friends and more “all from the same, single wallet.” That same wallet, it says, rewards people every time they spend or save.

After a “successful” alpha test with millions of dollars deposited, the company’s Eco App is now available to the public.

A slew of other VC firms participated in Eco’s latest financing, including Founders Fund, Activant Capital, Slow Ventures, Coinbase Ventures, Tribe Capital, Valor Capital Group and more than one hundred other funds and angels. Expa and Pantera Capital co-led the company’s $8.5 million funding round.

CoinList co-founder Andy Bromberg stepped down from his role last fall to head up Eco. The startup was originally called Beam before rebranding to Eco “thanks to involvement by founding advisor, Garrett Camp, who held the Eco brand,” according to Coindesk. Camp is an Uber co-founder and Expa is his venture fund.

For a16z Crypto, leading the round is in line with its mission.

In a blog post co-written by Katie Haun and Arianna Simpson, the firm outlined why it’s pumped about Eco and its plans.

“One of the challenges in any new industry — crypto being no exception — is building things that are not just cool for the sake of cool, but that manage to reach and delight a broad set of users,” they wrote. “Technology is at its best when it’s improving the lives of people in tangible, concrete ways…At a16z Crypto, we are constantly on the lookout for paths to get cryptocurrency into the hands of the next billion people. How do we think that will happen? By helping them achieve what they already want to do: spend, save, and make money — and by focusing users on tangible benefits, not on the underlying technology.”

Eco is not the only crypto platform offering rewards to users. Lolli gives users free bitcoin or cash when they shop at over 1,000 top stores.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Kaltura, a software company focused on providing video technology to other concerns, has filed to go public.

The Kaltura S-1 filing only partially surprised. TechCrunch previously covered the company as part of our ongoing $100 million ARR series focusing on private companies that have reached material scale. (TechCrunch has also covered its product life to a moderate degree.)

The company’s IPO documentation details a business that did more than merely accelerate its growth in 2020, and more specifically, during the COVID-19 era. Seeing a company that powers video tooling do well when much of the world has transitioned to remote work and education is not a bolt from the blue. What is notable, however, is that the company’s revenue growth has accelerated yearly since at least 2018 and its final quarter of 2020 placed the company at a new growth rate maximum.

Public investors, hungry for growth, may find such a progression compelling.

Kaltura also has an interesting profitability profile: As its GAAP net losses scaled in the last year, its adjusted profitability improved. Depending on your stance regarding adjusted metrics, Kaltura’s bottom line will either irk or delight you.

This afternoon, let’s rip into the company’s S-1 and yank out what we need to know. It is IPO season, with SPACs galore and other private companies taking more traditional routes to the public markets, including Coupang announcing a price range for its traditional debut today and Coinbase’s impending direct listing.

For now we’ll focus on Kaltura. Let’s get into it.

When TechCrunch last covered Kaltura’s financial results, we noted that the company founded in 2006 had raised just north of $166 million, crossed the $100 million ARR mark, and was, per its own reporting, “profitable on an EBITDA.” Kaltura also told TechCrunch that it had margins in the 60% range and was growing at around 25% year over year. That was just over a year ago.

Do those figures hold up? In the Q1 2020 period Kaltura recorded $25.9 million in revenue, software margins of around 78% and blended gross margins of 59.8%. And the company had grown 16.6% from the year-ago quarter. In Kaltura’s defense, the company’s growth accelerated to 24% in the year, so its self-reported numbers were mostly fair. Better than, I think, most numbers we get from private companies.

Powered by WPeMatico

“A lot of founders mix up raising money with making money.”

This quote, which Career Karma founder Ruben Harris mentioned off-hand on a phone call with me, has been on my mind for months. In fact, raising money can cost you money, in the form of that sweet, sweet ownership and equity.

That’s why Clearbanc, a startup I have covered for years, has always had a compelling pitch.

The company, co-founded by Michele Romanow and Andrew D’Souza, positions itself as an alternative equity-free capital solution for early-stage founders. Flexing its “20-minute term sheet” the startup uses an algorithm to shift through a startup’s data, and if it has positive ad spend and positive unit economics, they make an investment worth anything from $10,000 to over $10 million. It makes money through a revenue-share agreement versus an equity stake.

“While we’ve invested in over 4,000 businesses using this model, we’ve also turned away over 50,000 who weren’t at this scale or level of repeatability,” D’Souza tells TechCrunch. So, the startup told me this week that they have raised $10 million to create a new product: ClearAngel.

The startup is trying to back anyone with an online business that has early revenue, but pre-broad traction. Clearbanc wants to replace friends and family money, a concept that D’Souza says is “quite elitist,” with its own version of an angel check, while also offering founder services such as supply chain analysis, introductions to networks and competitive landscape analysis.

The startup just needs to make around $1,000 in monthly revenue to qualify for cash. In return for an investment between $10,000 to $50,000, founders have to pay up to 2% of their revenue over four years.

Clearbanc’s repayment works for some startups, but for others, a traditional bank loan could work better. Its biggest hurdle, I’d argue, is that if a startup has great revenue already, you might not want to take a revenue-share agreement loan.

As for if a startup takes ClearAngel capital and doesn’t make the minimum revenue?

“Then the ClearAngel product isn’t working,” he said. “There are bound to be some companies who still can’t make it, that’s the risk we take.”

Alternative capital has pros and cons, just like venture capital has pros and cons. If the end goal is to become a billion-dollar business, what’s the best route to do that? Is taking a revenue-share agreement going to hurt your chances as a pre-seed startup trying to raise capital? Does YC care at all?

Those are some of my biggest questions, and we’ll explore all (and more!) in my alternative financing panel next week for TC Sessions: Justice. It costs $5 to attend the entire conference, and speakers include Backstage Capital’s Arlan Hamilton and Congresswoman Barbara Lee.

Remember that you can get Startups Weekly in your inbox before anyone else, if you subscribe. It’s free! As always, you can find me @nmasc_ on Twitter or e-mail me at natasha.m@techcrunch.com. That is free too!

After being valued at $100 billion in the secondary markets, Coinbase has finally filed to go public. The S-1, as Winnie founder Sara Mauskopf tweeted, is #goals. The crypto unicorn, as my colleague Alex Wilhelm notes, grew just over 139% in 2020, a massive improvement on its 2019 results.

Here’s what to know:

Other notes:

SAN FRANCISCO, CA – SEPTEMBER 07: Coinbase Co-founder and CEO Brian Armstrong speaks onstage during Day 3 of TechCrunch Disrupt SF 2018 at Moscone Center on September 7, 2018 in San Francisco, California. (Photo by Steve Jennings/Getty Images for TechCrunch)

I caught up with Eric Eldon, managing editor at TechCrunch and former Startups Weekly writer, about the recent work he’s been doing with Kirsten Korosec, our transportation editor.

Here’s what he had to say: Startup employees may not be going into the office as often again — or ever. But everyone will still need to go places, or at least want to! How will they do it? What will we do? How will our altered set of needs and wants reshape cities, right as new technologies are fundamentally altering transportation, too? We’re going to be covering this topic in-depth this year, as we all figure out how to go back to work.

Other reading:

Crazy ride on the night by car. Image Credits: franckreporter/Getty Images.

The Spanish government, led by Prime Minister Pedro Sanchez, has announced plans to turn itself into an entrepreneurial nation. The Startup Act is the first piece of dedicated legislation meant to help create tech innovation within Spain. The goals are to promote innovation, new capital through domestic and foreign investments, and to seed the future of Spain as a hub for new companies.

Here’s what to know: Driving innovation can start with relaxing on regulatory concerns.

Among a package of some 50 support measures, the entrepreneurial strategy makes a reference to “smart regulation” and floats the idea of sandboxing for testing products publicly (i.e. without needing to worry about regulatory compliance first).

Other news this week:

Image Credits: MHJ (opens in a new window) / Getty Images

As loyal Equity listeners may have already noticed, we’ve been quietly experimenting with the concept of adding on a third show to our weekly production. This week, we told the world! Along with our current shows, which help listeners start and end the week with tech news, we’re going to bring on a Wednesday deep dive into a topic, subject area or person. Our first mid-week episode went live this week, and it was all about space (so yes, expect a lot of puns and Elon jokes).

The show is about to celebrate its four-year anniversary, and I’m about to celebrate my one-year anniversary as a co-host. We’re all so thankful for your support, and can’t wait to bring you more laughs and learnings.

Our latest episodes:

Seen on TechCrunch

The startup bootcamp you’ve always needed is finally here

Scoop: VCs are chasing Hopin upwards of $5-6B valuation

Lisbon’s startup scene rises as Portugal gears up to be a European tech tiger

Contra wants to be a community for independent workers

Seen on Extra Crunch

Ironclad’s Jason Boehmig: The objective of pricing is to become less wrong over time

As BNPL startups raise, a look at Klarna, Affirm and Afterpay earnings

4 essential truths about venture investing

And that’s the jam-packed week! As an insider tip to those that subscribe, I’m starting to cover health tech (along with edtech) for the TC team. So throw me the smartest person you know on the topic, and extra points if that’s you.

N

Powered by WPeMatico

This morning DigitalOcean, a provider of cloud computing services to SMBs, filed to go public. The company intends to list on the New York Stock Exchange (NYSE) under the ticker symbol “DOCN.”

DigitalOcean’s offering comes amidst a hot streak for tech IPOs, and valuations that are stretched by historical norms. The cloud hosting company was joined by Coinbase in filing its numbers publicly today.

DigitalOcean’s offering comes amidst a hot streak for tech IPOs.

However, unlike the cryptocurrency exchange, DigitalOcean intends to raise capital through its offering. Its S-1 filing lists a $100 million placeholder number, a figure that will update when the company announces an IPO price range target.

This morning let’s explore the company’s financials briefly, and then ask ourselves what its results can tell us about the cloud market as a whole.

TechCrunch has covered DigitalOcean with some frequency in recent years, including its early-2020 layoffs, its early-2020 $100 million debt raise and its $50 million investment from May of the same year that prior investors Access Industries and Andreessen Horowitz participated in.

From those pieces we knew that the company had reportedly reached $200 million in revenue during 2018, $250 million in 2019 and that DigitalOcean had expected to reach an annualized run rate of $300 million in 2020.

Those numbers held up well. Per its S-1 filing, DigitalOcean generated $203.1 million in 2018 revenue, $254.8 million in 2019 and $318.4 million in 2020. The company closed 2020 out with a self-calculated $357 million in annual run rate.

During its recent years of growth, DigitalOcean has managed to lose modestly increasing amounts of money, calculated using generally accepted accounting principles (GAAP), and non-GAAP profit (adjusted EBITDA) in rising quantities. Observe the rising disconnect:

Powered by WPeMatico

Mere days after we discussed Coinbase at $77 billion and Stripe at $115 billion in the private markets, those same semi-liquid exchanges have provided a new valuation for the cryptocurrency company. It’s now $100 billion, per Axios’ reporting.

Good thing we argued last week that there could be some merit to Coinbase’s $77 billion secondary market valuation from a particular perspective. We’d look silly today if we’d mocked the $77 billion figure only for it to go up by about a third in just a few days.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Luckily for us, Axios also got its hands on a few numbers regarding Coinbase’s 2019 and 2020 financial performance, so we can get into all sorts of trouble this morning. We’ll look at the data, which stretches to the end of Q3 2020, and then do some creative extrapolating into Q1 2021 to decide whether Coinbase at $100 billion makes no sense, a little sense or perfect sense.

As always, we’re riffing, not giving investment advice. So read on if you want to noodle on Coinbase with me; its impending direct listing will be one of the year’s most watched financial events.

We’ll drag Stripe back in at the end. Given that the companies now nearly share private-market valuations, we’d be remiss to not unfairly stack them against one another. Into the breach!

Axios’ Dan Primack, a good egg in my experience, got the goods on Coinbase’s historical performance. Summarizing the bits we need, here’s what the crypto exchange got up to recently:

It’s simple to take the 2020 data that we have and extrapolate it into full-year data. Indeed, you get revenues of $921.33 million and net income of $188 million. Compared to its 2019 data, Coinbase would have managed around 74% growth while swinging steeply into the profitable domain.

That’s a killer year. But it’s actually a bit better than we are giving Coinbase credit for. Poking around volume data compiled by Bitcoinity.org, Coinbase had its biggest period of 2020 in terms of bitcoin trading volume in the fourth quarter. Thinking about Coinbase’s 2020 from a trading perspective using the same dataset, it had a great Q1, more staid Q2 and Q3, and a blockbuster Q4 that ramped to record highs at the end.

Powered by WPeMatico