cloud

Auto Added by WPeMatico

Auto Added by WPeMatico

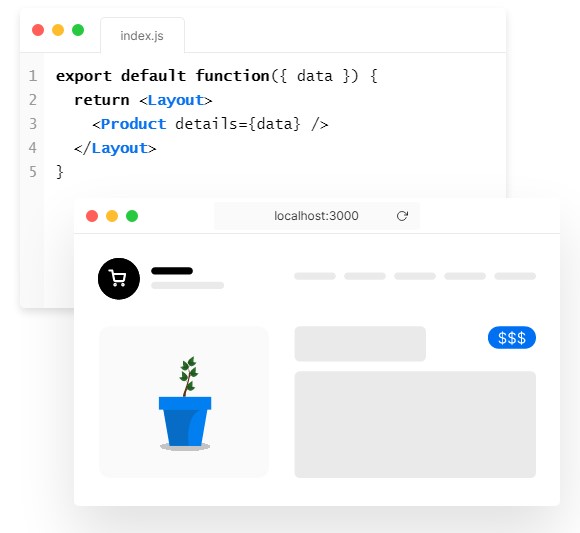

Vercel, the company behind the popular open-source Next.js React framework, today announced that it has raised a $102 million Series C funding round led by Bedrock Capital. Existing investors Accel, CRV, Geodesic Capital, Greenoaks Capital and GV also participated in this round, together with new investors 8VC, Flex Capital, GGV, Latacora, Salesforce Ventures and Tiger Global. In total, the company has now raised $163 million and its current valuation is $1.1 billion.

As Vercel notes, the company saw strong growth in recent months, with traffic to all sites and apps on its network doubling since October 2020. The number of sites among the world’s largest 10,000 websites that use Next.js grew 50% in the same time frame, too.

Image Credits: Vercel

Given the open-source nature of the Next.js framework, not all of these users are obviously Vercel customers, but its current paying customers include the likes of Carhartt, Github, IBM, McDonald’s and Uber.

“For us, it all starts with a front-end developer,” Vercel CEO Guillermo Rauch told me. “Our goal is to create and empower those developers — and their teams — to create delightful, immersive web experiences for their customers.”

With Vercel, Rauch and his team took the Next.js framework and then built a serverless platform that specifically caters to this framework and allows developers to focus on building their front ends without having to worry about scaling and performance.

Older solutions, Rauch argues, were built in isolation from the cloud platforms and serverless technologies, leaving it up to the developers to deploy and scale their solutions. And while some potential users may also be content with using a headless content management system, Rauch argues that increasingly, developers need to be able to build solutions that can go deeper than the off-the-shelf solutions that many businesses use today.

Rauch also noted that developers really like Vercel’s ability to generate a preview URL for a site’s front end every time a developer edits the code. “So instead of just spending all your time in code review, we’re shifting the equation to spending your time reviewing or experiencing your front end. That makes the experience a lot more collaborative,” he said. “So now, designers, marketers, IT, CEOs […] can now come together in this collaboration of building a front end and say, ‘that shade of blue is not the right shade of blue.’”

“Vercel is leading a market transition through which we are seeing the majority of value-add in web and cloud application development being delivered at the front end, closest to the user, where true experiences are made and enjoyed,” said Geoff Lewis, founder and managing partner at Bedrock. “We are extremely enthusiastic to work closely with Guillermo and the peerless team he has assembled to drive this revolution forward and are very pleased to have been able to co-lead this round.”

Powered by WPeMatico

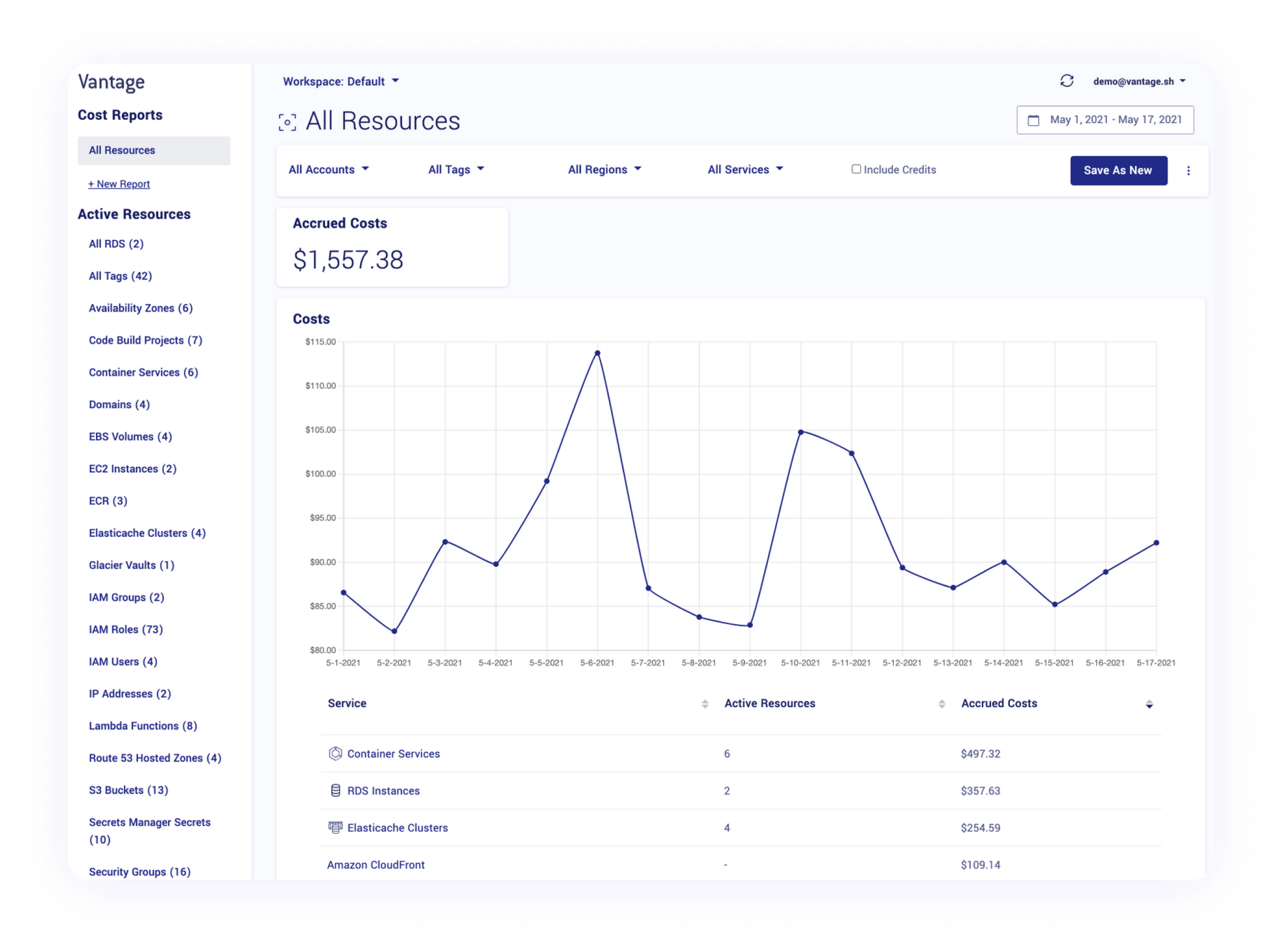

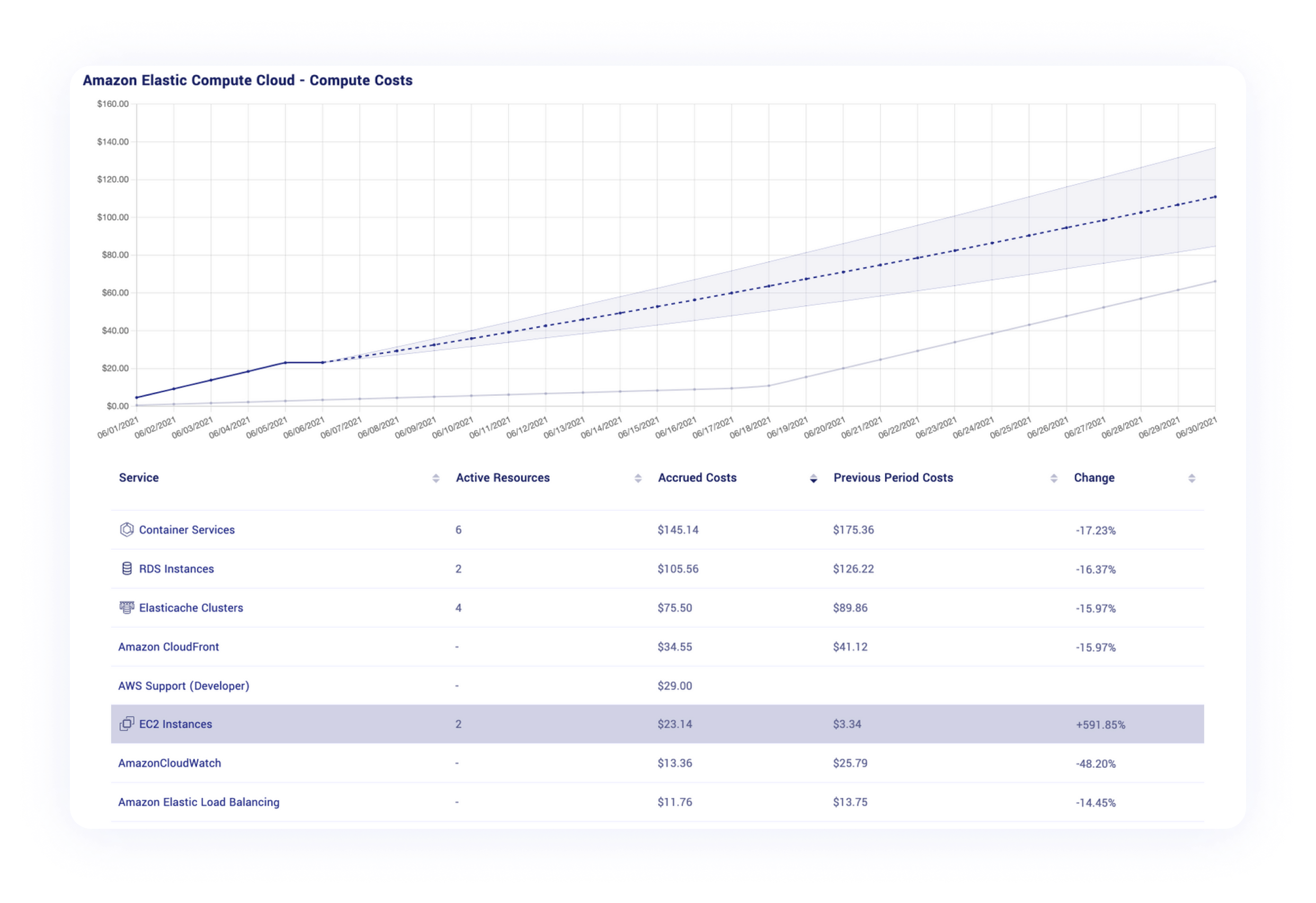

Vantage, a service that helps businesses analyze and reduce their AWS costs, today announced that it has raised a $4 million seed round led by Andreessen Horowitz. A number of angel investors, including Brianne Kimmel, Julia Lipton, Stephanie Friedman, Calvin French Owen, Ben and Moisey Uretsky, Mitch Wainer and Justin Gage, also participated in this round.

Vantage started out with a focus on making the AWS console a bit easier to use — and helping businesses figure out what they are spending their cloud infrastructure budgets on in the process. But as Vantage co-founder and CEO Ben Schaechter told me, it was the cost transparency features that really caught on with users.

“We were advertising ourselves as being an alternative AWS console with a focus on developer experience and cost transparency,” he said. “What was interesting is — even in the early days of early access before the formal GA launch in January — I would say more than 95% of the feedback that we were getting from customers was entirely around the cost features that we had in Vantage.”

Image Credits: Vantage

Like any good startup, the Vantage team looked at this and decided to double down on these features and highlight them in its marketing, though it kept the existing AWS Console-related tools as well. The reason the other tools didn’t quite take off, Schaechter believes, is because more and more, AWS users have become accustomed to infrastructure-as-code to do their own automatic provisioning. And with that, they spend a lot less time in the AWS Console anyway.

“But one consistent thing — across the board — was that people were having a really, really hard time 12 times a year, where they would get a shocking AWS bill and had to figure out what happened. What Vantage is doing today is providing a lot of value on the transparency front there,” he said.

Over the course of the last few months, the team added a number of new features to its cost transparency tools, including machine learning-driven predictions (both on the overall account level and service level) and the ability to share reports across teams.

Image Credits: Vantage

While Vantage expects to add support for other clouds in the future, likely starting with Azure and then GCP, that’s actually not what the team is focused on right now. Instead, Schaechter noted, the team plans to add support for bringing in data from third-party cloud services instead.

“The number one line item for companies tends to be AWS, GCP, Azure,” he said. “But then, after that, it’s Datadog, Cloudflare, Sumo Logic, things along those lines. Right now, there’s no way to see, P&L or an ROI from a cloud usage-based perspective. Vantage can be the tool where that’s showing you essentially, all of your cloud costs in one space.”

That is likely the vision the investors bought into, as well, and even though Vantage is now going up against enterprise tools like Apptio’s Cloudability and VMware’s CloudHealth, Schaechter doesn’t seem to be all that worried about the competition. He argues that these are tools that were born in a time when AWS had only a handful of services and only a few ways of interacting with those. He believes that Vantage, as a modern self-service platform, will have quite a few advantages over these older services.

“You can get up and running in a few clicks. You don’t have to talk to a sales team. We’re helping a large number of startups at this stage all the way up to the enterprise, whereas Cloudability and CloudHealth are, in my mind, kind of antiquated enterprise offerings. No startup is choosing to use those at this point, as far as I know,” he said.

The team, which until now mostly consisted of Schaechter and his co-founder and CTO Brooke McKim, bootstrapped the company up to this point. Now they plan to use the new capital to build out its team (and the company is actively hiring right now), both on the development and go-to-market side.

The company offers a free starter plan for businesses that track up to $2,500 in monthly AWS cost, with paid plans starting at $30 per month for those who need to track larger accounts.

Powered by WPeMatico

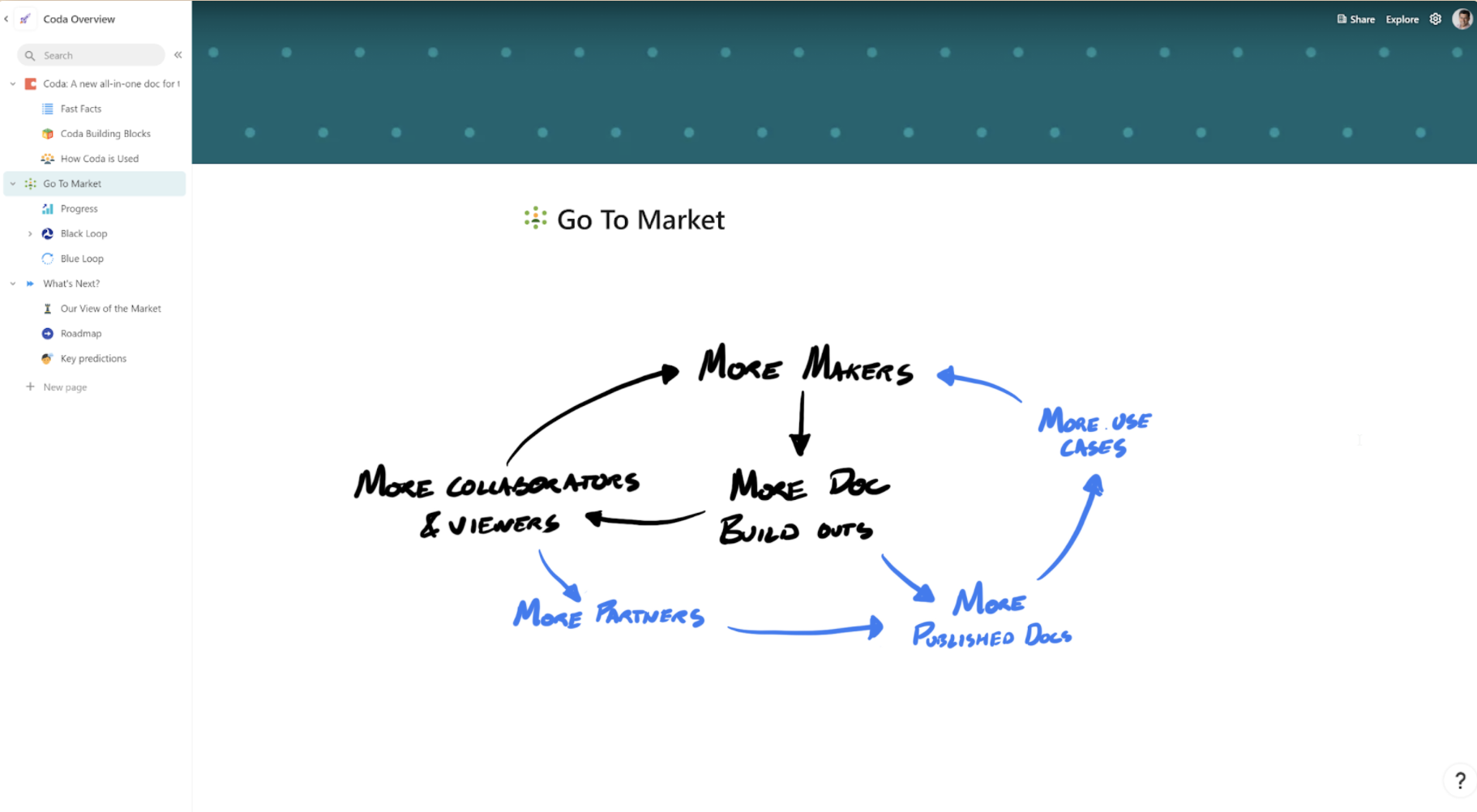

Coda entered the market with an ambitious, but simple, mission. Since launching in 2014, it has seemingly forged a path to realizing its vision with $140 million in funding and 25,000 teams across the globe using the platform.

Coda is simple in that its focus is on the document, one of the oldest content formats/tools on the internet, and indeed in the history of software. Its ambition lies in the fact that there are massive incumbents in this space, like Google and Microsoft.

Co-founder and CEO Shishir Mehrotra told TechCrunch that that level of competition wasn’t a hindrance, mainly because the company was very good at communicating its value and building highly effective flywheels for growth.

Mehrotra was generous enough to let us take a look through his pitch doc (not deck!) on a recent episode of Extra Crunch Live, diving not only into the factors that have made Coda successful, but how he communicated those factors to investors.

A screenshot from Coda’s pitch doc.

Extra Crunch Live also features the ECL Pitch-off, where founders in the audience come “onstage” to pitch their products to our guests. Mehrotra and his investor, Madrona partner S. Somasegar, gave their live feedback on pitches from the audience, which you can check out in the video (full conversation and pitch-off) below.

As a reminder, Extra Crunch Live takes place every Wednesday at 3 p.m. EDT/noon PDT. Anyone can hang out during the episode (which includes networking with other attendees), but access to past episodes is reserved exclusively for Extra Crunch members. Join here.

Like many investors and founders, Mehrotra and Somasegar met well before Mehrotra was working on his own project. They met when both of them worked at Microsoft and maintained a relationship while Mehrotra was at Google.

In their earliest time together, the conversations centered around advice on the Seattle tech ecosystem or on working with a particular team at Microsoft.

“Many people will tell you building relationships with investors … you want to do it outside of a fundraise as much as possible,” said Mehrotra.

Eventually, Mehrotra got to work on Coda and kept in touch with Somasegar. He even pitched him for Series B fundraising — and ultimately got a no. But the relationship persisted.

Powered by WPeMatico

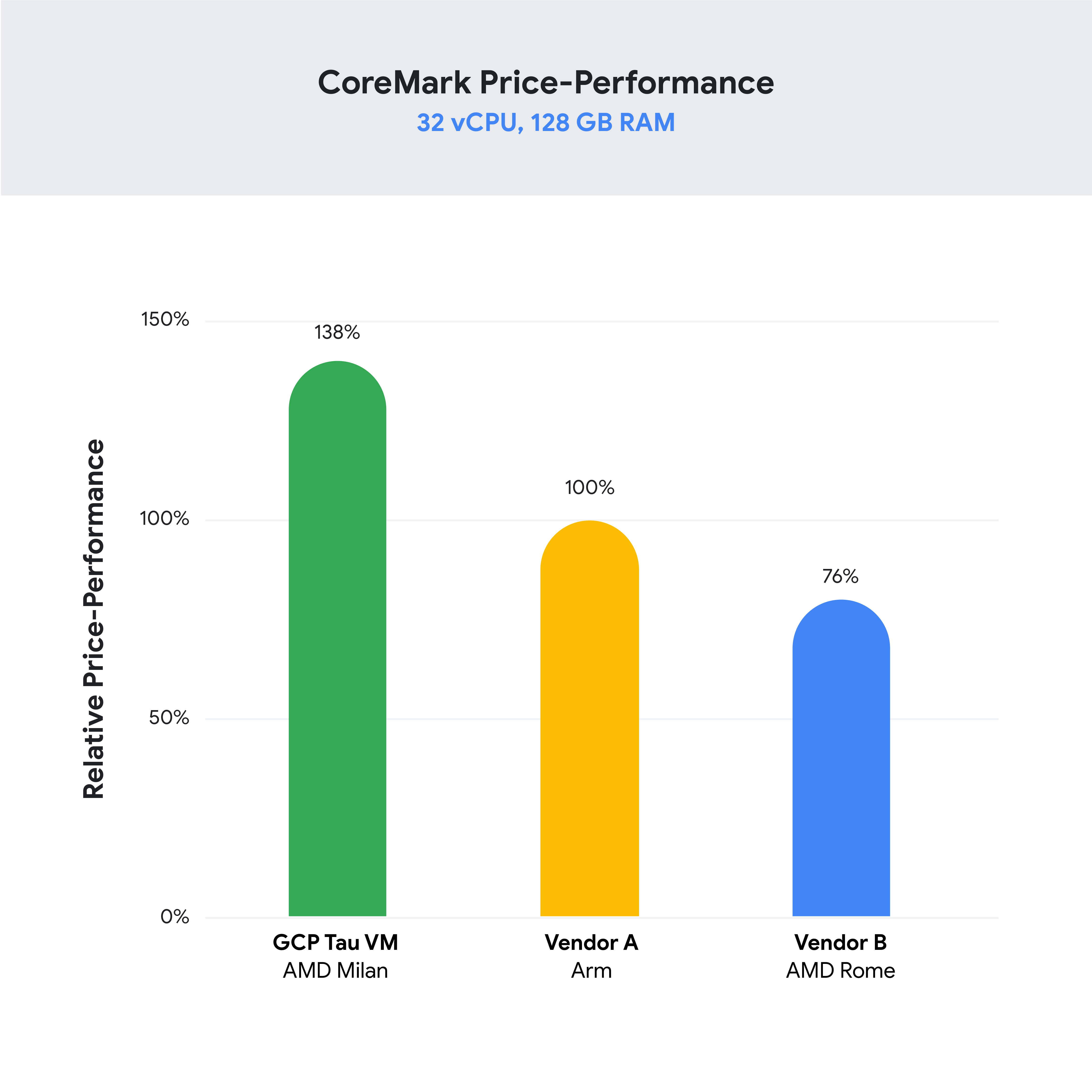

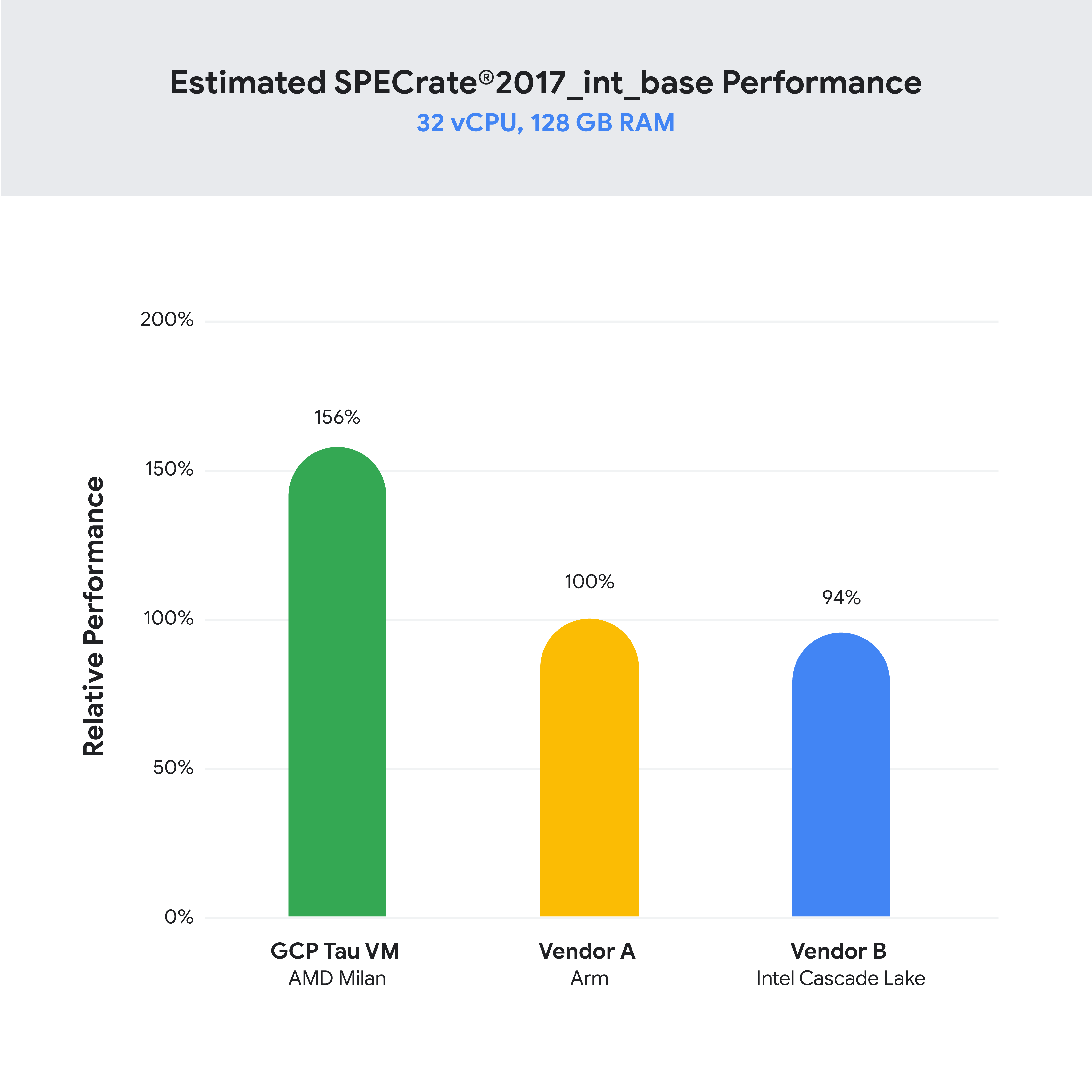

Google this morning announced the launch of Tau, a new family of virtual machines built on AMD’s third-gen EPYC processor. According to the company, the new x86-compatible system offers a 42% price-performance boost over standard VMs. Google notably first started utilizing AMD EPYC processors for Cloud back in 2017, while Amazon Cloud’s offerings date back to 2018.

Google claims the Tau family “leapfrogs” existing cloud VMs. The systems come in a variety of configurations, ranging up to 60vCPUs per VM, and 4GB of memory per vCPU. Networking bandwidth goes up to 32 Gbps, and they can be coupled with a variety of different network attached storage.

“Customers across every industry are dealing with more demanding and data-intensive workloads and looking for strategic ways to speed up performance and reduce costs,” Google Cloud CEO Thomas Kurian said in a press release. “Our work with key strategic partners like AMD has allowed us to broaden our offerings and deliver customers the best price performance for compute-heavy, business-critical applications– all on the cleanest cloud in the industry.”

Image Credits: Google

Google has already signed up some high-profile customers for an early trial, including Twitter, Snap and DoIT.

“High performance at the right price point is a critical consideration as we work to serve the global public conversation,” Twitter Platform Lead Nick Tornow said in a blog post. “We are excited by initial tests that show potential for double digit performance improvement. We are collaborating with Google Cloud to more deeply evaluate benefits on price and performance for specific compute workloads that we can realize through use of the new Tau VM family.”

Image Credits: Google

The Tau VMs will be arriving for Google Cloud in Q3 of this year. The company has already opened the system up to clients for pre-registration. Pricing is dependent on the configuration. For example, a 32vCPU VM sporting 128GB RAM will run around $1.35 an hour.

Powered by WPeMatico

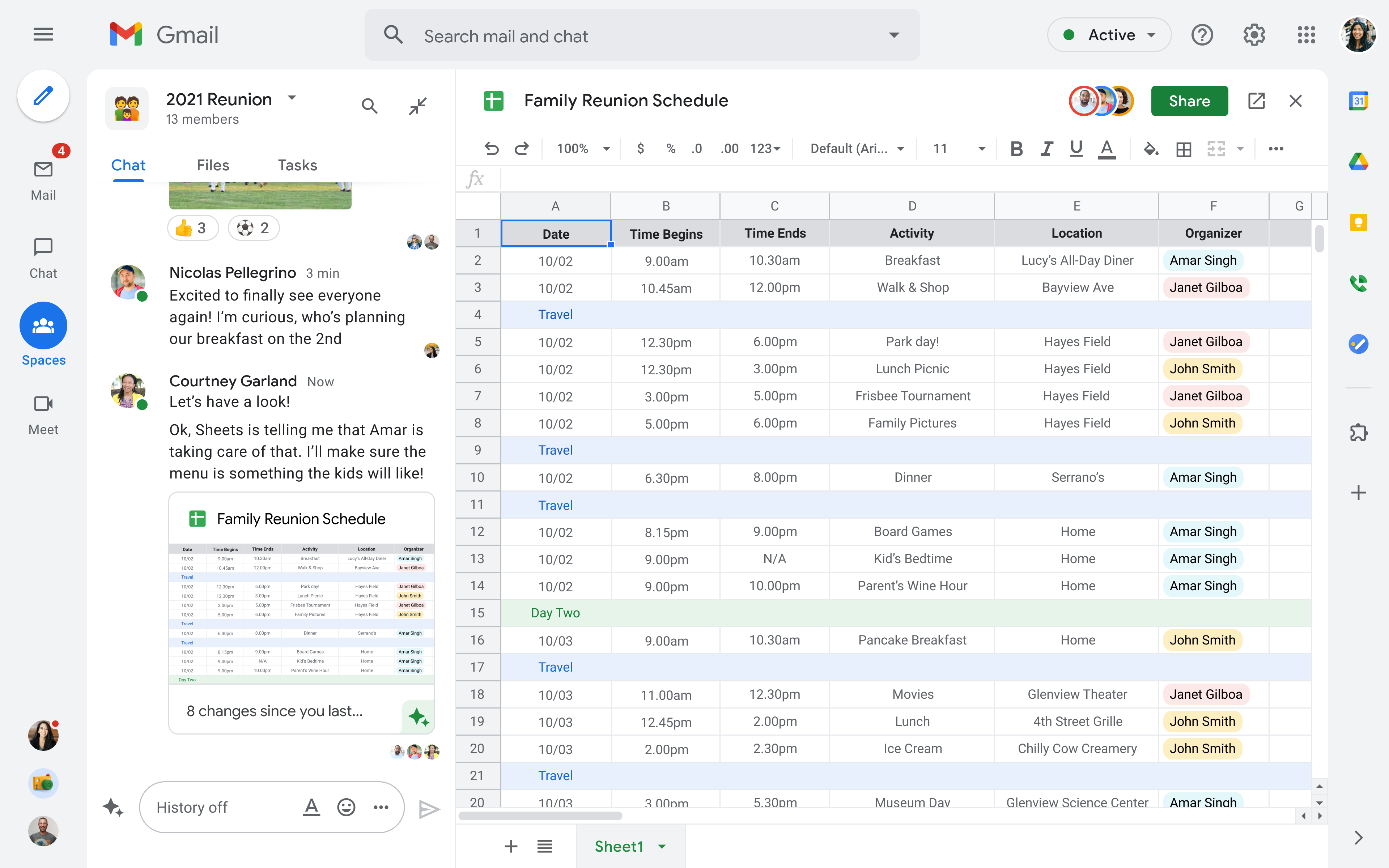

Google today announced that it is making Workspace, the service formerly known as G Suite (and with a number of new capabilities), available to everyone, including consumers on free Google accounts. The core philosophy behind Workspace is to enable deeper collaboration between users. You can think of it as the same Google productivity apps you’re already familiar with (Gmail, Calendar, Drive, Docs, Sheets, Slides, Meet, Chat, etc.), but with a new wrapper around it and deeper integrations between the different apps.

For individual users who want more from their Workspace, there will also be a new paid offering, though Google isn’t saying how much you’ll have to pay yet. (Update: Google Workspace Individual subscription will be $9.99/month, with an introductory price of $7.99/month.) With that, users will get access to “premium capabilities, including smart booking services, professional video meetings and personalized email marketing, with much more on the way.” We’ll likely hear more about this later this year. This new paid offering will be available “soon” in the U.S., Canada, Mexico, Australia, Brazil and Japan.

Consumers will have to switch from the classic Hangouts experience (RIP) to the new Google Chat to enable it — and with this update, all users will now have access to the new Google Chat, too. Until now, only paying G Suite/Workspace users had access to this new Workspace user experience.

“Collaboration doesn’t stop at the workplace — our products have been optimized for broad participation, sharing and helpfulness since the beginning,” said Javier Soltero, VP and GM, Google Workspace. “Our focus is on delivering consumers, workers, teachers and students alike an equitable approach to collaboration, while still providing flexibility that allows these different subsets of users to take their own approach to communication and collaboration.”

Image Credits: Google

Once enabled, users will encounter quite a few user interface changes. The left rail, for example, will look a little bit like the bottom bar of Gmail on iOS and Android now, with the ability to switch between Mail, Chat, Meet and Spaces (which — yeah — I’m not sure anybody really understands this one, but more about this later). The right rail will continue to bring up various plugins and shortcuts to features like Google Calendar, Tasks and Keep.

A lot of people — especially those who simply want Gmail to be Gmail and don’t care about all of this collaboration stuff in their private lives — will hate this. But at least for the time being, you can still keep the old experience by not switching from Hangouts to the new Google Chat. But for Google, this clearly shows the path Workspace is on.

Image Credits: Google

“Back in October of last year, we announced some very significant updates to our communication and collaboration product line and our business, starting with the new brand and identity that we chose around Google Workspace that’s meant to represent what we believe is the future direction and real opportunity around our product — less around being a suite of individual products and more around being an integrated set of experiences that represent the future of work,” Soltero explained in a press briefing ahead of today’s announcement.

And then there is “Spaces.” Until now, Google Workspace features a tool called “Rooms.” Rooms are now Spaces. I’m not quite sure why, but Google says it is “evolving the Rooms experience in Google Chat into a dedicated place for organizing people, topics, and projects in Google Workspace.”

Best I can tell, these are Slack-like channels where teams can not just have conversations around a given topic but also organize relevant files and upcoming tasks, all with an integrated Google Meet experience and direct access to working on their files. That’s all good and well, but I’m not sure why Google felt the need to change the name. Maybe it just doesn’t want you to confuse Slack rooms with Google rooms. And it’s called Google Workspace, after all, not Workroom.

New features for Rooms/Spaces include in-line topic threading, presence indicators, custom statuses, expressive reactions and a collapsible view, Google says.

Both free and paid users will get access to these new Spaces once they launch later this year.

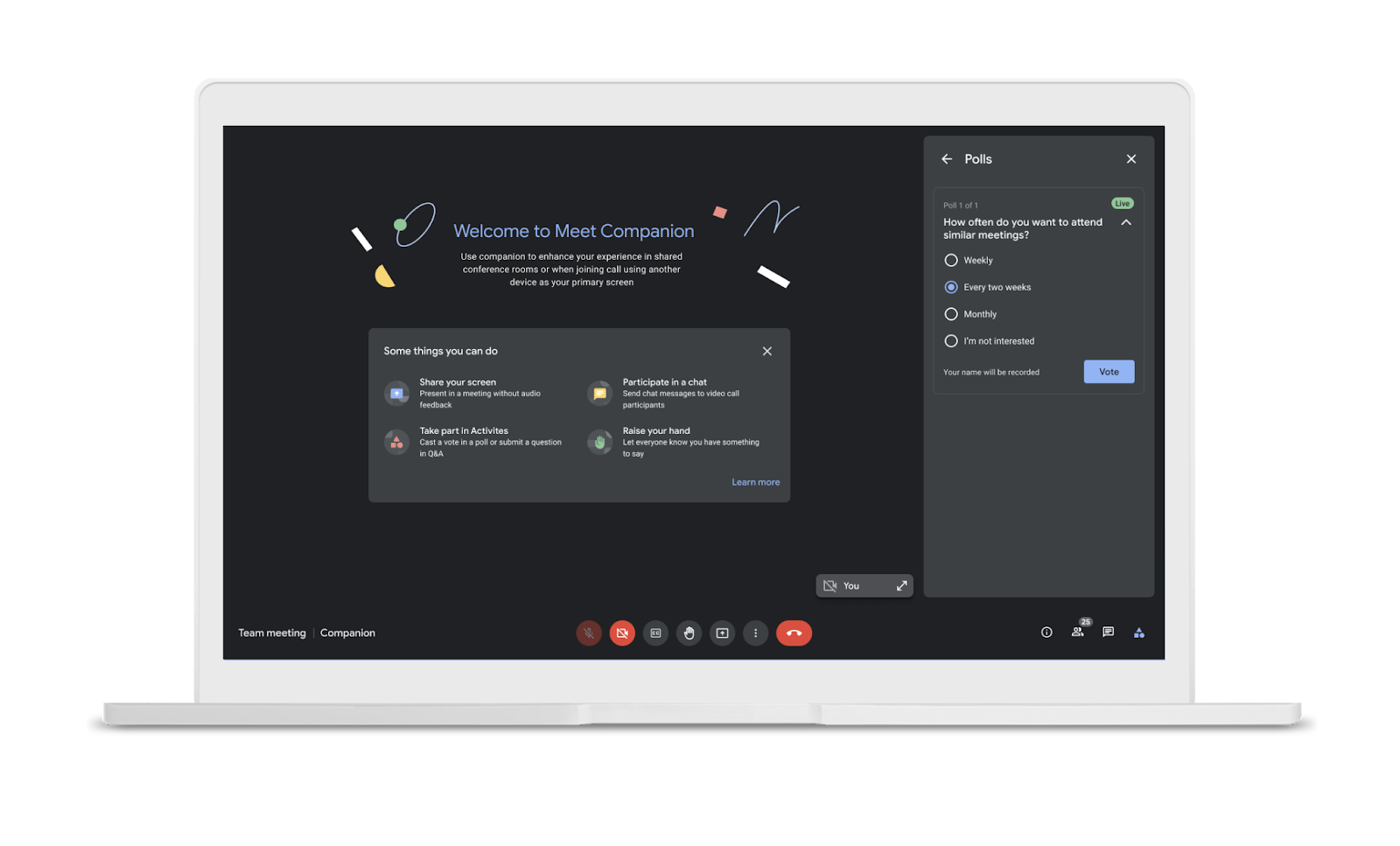

But wait, there’s more. A lot more. Google is also introducing a number of new Workspace features today. Google Meet, for example, is getting a companion mode that is meant to foster “collaboration equity in a hybrid world.” The idea here is to give meeting participants who are in a physical meeting room and are interacting with remote participants a companion experience to use features like screen sharing, polls, in-meeting chat, hand raise and Q&A live captions on their personal devices. Every participant using the companion mode will also get their own video tile. This feature will be available in September.

Image Credits: Google

Also new is an RSVP option that will allow you to select whether you will participate remotely, in a meeting room (or not at all), as well as new moderation controls to allow hosts to prevent the use of in-meeting chat and to mute and unmute individual participants.

On the security side, Google today also announced that it will allow users to bring their own encryption keys. Currently, Google encrypts your data, but it does manage the key for you. To strengthen your security, you may want to bring your own keys to the service, so Google has now partnered with providers like Flowcrypt, Futurex, Thales and Virtru to enable this.

“With Client-side encryption, customer data is indecipherable to Google, while users can continue to take advantage of Google’s native web-based collaboration, access content on mobile devices, and share encrypted files externally,” writes Google directors of product management Karthik Lakshminarayanan and Erika Trautman in today’s announcement.

Image Credits: Google

Google is also introducing trust rules for Drive to give admins control over how files can be shared within an organization and externally. And to protect from real phishing threats (not those fake ones your internal security organization sends out every few weeks or so), Google is also now allowing admins to enable the same phishing protections it already offers today to content within an organization to help guard your data against insider threats.

Powered by WPeMatico

Last year, Seattle-based network security startup ExtraHop was riding high, quickly approaching $100 million in ARR and even making noises about a possible IPO in 2021. But there will be no IPO, at least for now, as the company announced this morning it has been acquired by a pair of private equity firms for $900 million.

The firms, Bain Capital Private Equity and Crosspoint Capital Partners, are buying a security solution that provides controls across a hybrid environment, something that could be useful as more companies find themselves in a position where they have some assets on-site and some in the cloud.

The company is part of the narrower Network Detection and Response (NDR) market. According to Jesse Rothstein, ExtraHop’s chief technology officer and co-founder, it’s a technology that is suited to today’s threat landscape, “I will say that ExtraHop’s north star has always really remained the same, and that has been around extracting intelligence from all of the network traffic in the wire data. This is where I think the network detection and response space is particularly well suited to protecting against advanced threats,” he told TechCrunch.

The company uses analytics and machine learning to figure out if there are threats and where they are coming from, regardless of how customers are deploying infrastructure. Rothstein said he envisions a world where environments have become more distributed with less defined perimeters and more porous networks.

“So the ability to have this high-quality detection and response capability utilizing next generation machine learning technology and behavioral analytics is so very important,” he said.

Max de Groen, managing director at Bain, says his company was attracted to the NDR space, and saw ExtraHop as a key player. “As we looked at the NDR market, ExtraHop, which [ … ] has spent 14 years building the product, really stood out as the best individual technology in the space,” de Groen told us.

Security remains a frothy market with lots of growth potential. We continue to see a mix of startups and established platform players jockeying for position, and private equity firms often try to establish a package of services. Last week, Symphony Technology Group bought FireEye’s product group for $1.2 billion, just a couple of months after snagging McAfee’s enterprise business for $4 billion as it tries to cobble together a comprehensive enterprise security solution.

Powered by WPeMatico

As remote work became the default for many companies during the pandemic, it’s maybe no surprise that services like Microsoft’s Windows Virtual Desktop, which gives users access to a fully managed Windows 10 desktop experience from virtually anywhere, saw a lot of interest from large enterprises and a new crop of small businesses that suddenly had to find ways to better support their remote workers. That’s pretty much what Microsoft saw, too, which had originally targeted Windows Virtual Desktop at some of the world’s largest enterprises. And so as the user base changed, Microsoft’s vision for the product changed as well, leading it to now changing its name from Windows Virtual Desktop to Azure Virtual Desktop.

“When we first went GA with Windows Virtual Desktop, about a year and a half ago, the world was a very different place,” said Kam VedBrat, Microsoft’s general manager for Azure Virtual Desktop. “And to be blunt, we looked at the service and what we were building, who we were building it for, pretty differently. No one at that time had any idea that this global pandemic was going to happen and that it would cause so many organizations around the world and millions of people to have to essentially leave the office and work from home — and the role the service would play in enabling a lot of that.”

Image Credits: Microsoft

While the original idea was to help enterprises move their virtual desktop environments from their data centers to the cloud, the pandemic brought a slew of new use cases to Windows Azure Virtual Desktop. It now hosts anything from virtual school labs to the traditional remote enterprise use cases. These new users also have somewhat different needs and expertise from those users the service was originally meant for, so on top of today’s name change, the company is also launching a set of new features that should make it easier for new users to get started with using Azure Virtual Desktop.

Among those is a new Quickstart experience, which will soon launch in public preview. “One piece of feedback that we saw is that as so many organizations are looking at Azure Virtual Desktop to enable new scenarios for hybrid work, they want to get these environments up and running quickly to understand how they work, how their apps behave in them, how to think about app groups and host pools and some of the new concepts that are there,” VedBrat explained. Ideally, it should now only take a few clicks to set up a full virtual desktop environment from the Azure portal.

Also new in Azure Virtual Desktop is support for managing multi-session virtual machines (VMs) with Microsoft Endpoint Manager, Microsoft’s unified service for device management. This marks the first time Endpoint Manager is able to handle multi-session VMs, which are one of the biggest selling points for Azure Virtual Desktop, since it allows a business to host multiple users on the same machine running Windows 10 Enterprise in the cloud.

In addition, Azure Virtual Desktop now offers enhanced support for Azure Active Directory, in addition to a new per-user access pricing option (in addition to the cost of running on the Azure infrastructure) that will allow users to deliver apps to external users. This, Microsoft argues, will allow software vendors to deliver their apps as a SaaS solution, for example.

As for the name change, VedBrat argues that while Windows is obviously at the core of the experience, a lot of the service’s users care about the underlying Azure infrastructure as well, be that storage or networking, for example. “They look at that broader environment that they’re creating — that window estate that they’re creating in the cloud — and they see that as a larger thing and they look at a lot of Azure as part of that. So we felt like the right thing to do at this point, in order to address that broader view that our customers are taking, was to look at the new name,” he explained.

I thought Windows Virtual Desktop explained the core concept just fine, but nobody has ever accused me of being a marketing genius.

Powered by WPeMatico

Toyota AI Ventures, Toyota’s standalone venture capital fund, has dropped the “AI” and is reborn as, simply, Toyota Ventures. The fund is commemorating its new identity by investing an additional $300 million in emerging technologies and carbon neutrality via two early-stage funds: the Toyota Ventures Frontier Fund and the Toyota Ventures Climate Fund.

The introduction of these two new funds, each worth $150 million, brings Toyota Ventures’ total assets under management to over $500 million. With the new capital infusion into the Frontier Fund comes an expansion of Toyota Ventures’ core thesis, which previously focused on AI, autonomy, mobility, robotics and the cloud, and now is adding smart cities, digital health, fintech and energy. So while Toyota Ventures’ investment approach isn’t changing, it’s broadening the scope of startups it will consider investing in.

“AI is kind of shrinking as a proportion of everything,” Jim Adler, founding managing director of Toyota Ventures, told TechCrunch. “The first mission of the Frontier Fund has always been to discover what’s next for Toyota. Toyota pivoted to cars in the 1930s, and Toyota will grow to other businesses in the future. Startups are experiments in the marketplace, and this is a way for us to understand and get comfortable with where innovations are coming from.”

Toyota as a global company has more than 370,000 employees that cover a range of business units in which the company at large stands to benefit from investing, such as financial technology. The Frontier Fund is a step outside of mobility. It not only seeks to bring emerging tech to market, but it also wants to bring new innovations onboard, whether as a customer or an acquisition, according to Adler.

“I think the vision of the company really is that machines are here to stay, they amplify the human experience, and Toyota understands how machines amplify humans really well for the benefit of society, which sounds incredibly corny, but the company really believes that,” said Adler.

By that same token, the new Climate Fund seeks to invest in startups that can help Toyota accelerate its goal of reaching carbon neutrality by 2050. The company has been investing in hydrogen for years, including a recent partnership with Japanese fuel company ENEOS, but it’s open to whatever technology will help achieve carbon neutrality, according to Adler.

“We think renewable energies will play a role,” said Adler. “Hydrogen production, storage distribution and utilization will play a role. We think carbon capture and storage will play a role. We’re not going to get dogmatic about hydrogen because we’ve been at it for decades and maybe things will change. Hydrogen hasn’t been crowdsourced across the startup community because there just wasn’t a market for it, but I think the market may be emerging.”

The fund is accepting online pitches on its website from entrepreneurs seeking early-stage funding. On Thursday, Toyota Ventures also announced it would be expanding its team and working with a new Advisor Network as a resource for founders looking for guidance on anything from product development to diversity and recruitment.

“Toyota Ventures has been an invaluable partner for Boxbot since they invested in our seed round in 2018,” said Austin Oehlerking, co-founder and CEO of Boxbot, in a statement. “They have been instrumental in helping us to navigate complicated, existential challenges on our journey from concept to product/market fit. Jim and the team really understand how corporate venture capital should function in order to successfully partner with startups.”

Adler says he and his team come from an entrepreneurial background, so they understand what it’s like on the other side of the table. Toyota Ventures’ focuses on early-stage startups because that’s where it believes some of the most interesting innovations come from.

“I’m a big believer that early-stage venture capital is a telescope into the future,” said Adler. “I think we can actually find those incredibly valuable innovations that make this all worthwhile.”

Powered by WPeMatico

Software as a service has been thriving as a sector for years, but it has gone into overdrive in the past year as businesses responded to the pandemic by speeding up the migration of important functions to the cloud. We’ve all seen the news of SaaS startups raising large funding rounds, with deal sizes and valuations steadily climbing. But as tech industry watchers know only too well, large funding rounds and valuations are not foolproof indicators of sustainable growth and longevity.

Failing to come across as a unique, differentiated company will likely mean settling for an exit that feels mediocre instead of incredible.

To scale sustainably, grow its customer base and mature to the point of an exit, a SaaS startup needs to stand apart from the herd at every phase of development. Failure to do so means a poor outcome for founders and investors.

As a founder who pivoted from on-premise to SaaS back in 2016, I have focused on scaling my company (most recently crossing 145,000 customers) and in the process, learned quite a bit about making a mark. Here is some advice on differentiation at the various stages in the life of a SaaS startup.

Differentiation is crucial early on, because it’s one of the only ways to attract customers. Customers can help lay the groundwork for everything from your product roadmap to pricing.

The more you know about your target customers’ pain points with current solutions, the easier it will be to stand out. Take every opportunity to learn about the people you are aiming to serve, and which problems they want to solve the most. Analyst reports about specific sectors may be useful, but there is no better source of information than the people who, hopefully, will pay to use your solution.

The key to success in the SaaS space is solving real problems. Take DocuSign, for example — the company found a way to simply and elegantly solve a niche problem for users with its software. This is something that sounds easy, but in reality, it means spending hours listening to the customer and tailoring your product accordingly.

Powered by WPeMatico

When Cloudera announced its sale to a pair of private equity firms yesterday for $5.3 billion, along with a couple of acquisitions of its own, the company detailed a new path that could help it drive back toward relevance in the big data market.

When the company launched in 2008, Hadoop was in its early days. The open-source project developed at Yahoo three years earlier was built to deal with the large amounts of data that the internet pioneer generated. It became increasingly clear over time that every company would have to deal with growing data stores, and it seemed that Cloudera was in the right market at the right time.

And for a while things went well. Cloudera rode the Hadoop startup wave, garnering a cool billion in funding along the way, including a stunning $740 million check from Intel Capital in 2014. It then went public in 2018 to much fanfare.

But the markets had already started to shift by the time of its public debut. Hadoop, a highly labor-intensive way to manage data, was being supplanted by cheaper and less complex cloud-based solutions.

“The excitement around the original promise of the Hadoop market has contracted significantly. It’s incredibly expensive and complex to get it working effectively in an enterprise context,” Casey Aylward, an investor at Costanoa Ventures told TechCrunch.

The company likely saw that writing on the wall when it merged with another Hadoop-based company, Hortonworks, in 2019. That transaction valued the combined entity at $5.2 billion, almost the same amount it sold for yesterday, two years down the road. The decision to sell and go private may also have been spurred by Carl Icahn buying an 18% stake in the company that same year.

Looking to the future, Cloudera’s sale could provide the enterprise unicorn room as it regroups.

Patrick Moorhead, founder and principal analyst at Moor Insight & Strategies, sees the deal as a positive step for the company. “I think this is good news for Cloudera because it now has the capital and flexibility to dive head first into SaaS. The company invented the entire concept of a data life cycle, implemented initially on premises, then extended to private and public clouds,” Moorhead said.

Adam Ronthal, Gartner Research VP, agrees that it at least gives Cloudera more room to make necessary adjustments to its market strategy as long as it doesn’t get stifled by its private equity overlords. “It should give Cloudera an opportunity to focus on their future direction with increased flexibility — provided they are able to invest in that future and that this does not just focus on cost cutting and maximizing profits. Maintaining a culture of innovation will be key,” Ronthal said.

Which brings us to the two purchases Cloudera also announced as part of its news package.

If you want to change direction in a hurry, there are worse ways than via acquisitions. And grabbing Datacoral and Cazena should help Cloudera alter its course more quickly than it could have managed on its own.

“[The] two acquisitions will help Cloudera capture some of the value on top of the lake storage layer — perhaps moving into different data management features and/or expanding into the compute layer for analytics and AI/ML use cases, where there has been a lot of growth and excitement in recent years,” Aylward said.

Chandana Gopal, research director for the future of intelligence at IDC, agrees that the transactions give Cloudera some more modern options that could help speed up the data-wrangling process. “Both the acquisitions are geared towards making the management of cloud infrastructure easier for end-users. Our research shows that data prep and integration takes 70%-80% of an analyst’s time versus the time spent in actual analysis. It seems like both these companies’ products will provide technology to improve the data integration/preparation experience,” she said.

The company couldn’t stay on the path it was on forever, certainly not with an activist investor breathing down its neck. Its recent efforts could give it the time away from public markets it needs to regroup. How successful Cloudera’s turnaround proves to be will depend on whether the private equity companies buying it can both agree on the direction and strategy for the company, while providing the necessary resources to push the company in a new direction. All of that and more will determine if these moves pay off in the end.

Powered by WPeMatico