Cleo

Auto Added by WPeMatico

Auto Added by WPeMatico

Parenting benefits company Cleo is partnering with on-demand childcare service UrbanSitter to address a problem facing many parents today amid the pandemic: a lack of childcare, even as they’re required to return to work. With summer camps, daycares and schools shut down for the months ahead, parents who need to work outside the home (or even inside, but without distraction) no longer have options. Cleo’s new solution, Cleo Care, powered by UrbanSitter, aims to address this problem. The company is offering a package to employers that will help connect families with vetted caregivers via concierge support or, as an alternative, with family co-op options, depending on the parents’ preference.

The program will additionally include access to other Cleo support programs, like one-on-one coaching and age-appropriate programs focused on developmental milestones, delivered weekly.

The launch of the new product arrives at a time when the coronavirus outbreak has caused a childcare crisis in the U.S. Working parents have become homeschool teachers, on top of their already overwhelming number of duties. Parents fortunate enough to work from home, however, are continually interrupted by children’s needs, leading to longer working hours to accomplish tasks, and often mental and physical exhaustion.

Cleo surveyed its member base in April 2020, roughly 80% of whom are in the U.S., and found that more than 50% of respondents didn’t have any childcare options due to the pandemic’s impact. It also learned that 1 in 5 families (with two parents) were considering having one partner leave the workforce in order to manage the care of the children. Meanwhile, 37% were considering having family move in.

Among those who were working, more than half felt their productivity was 75% or less than usual. And 1 in 4 felt their productivity was less than 50% of baseline.

Among those who were working, more than half felt their productivity was 75% or less than usual. And 1 in 4 felt their productivity was less than 50% of baseline.

The problem is massive. In the U.S. alone, there are 30.5 million working families, based on Bureau of Labor Statistics.

The Cleo Care solution will be made available to U.S. employers this month to give parents more options, as well as help employers to bring their staff back to work, when the time comes.

Of course, there’s a variety of opinions about how and when the U.S. should re-open its economy. But the reality is that some parents will need to return to their jobs ahead of the re-opening of child care centers or summer camp programs, many of which have been canceled. In Facebook groups, parents are already trying to solve the problem for themselves by organizing with neighbors for childcare co-ops or by hiring teens or college students for daytime babysitting jobs.

But not everyone has these options. And employers can’t just direct staff to Facebook to find a caregiver.

Instead, the Cleo Care program will provide member parents with concierge support for finding vetted care providers from the UrbanSitter network. Or if the families would prefer to work with neighbors, the solution can also offer to match network members interested in co-op solutions.

These features are new to UrbanSitter, which has never before offered co-op matching and is making the new concierge service exclusive to Cleo Care.

“As working moms desperate for a solution to the crisis facing parents today, we were focused on developing a solution that didn’t just work for our members and enterprise clients, but also one that we’d use ourselves. After experimenting and trying everything from virtual care to scheduling shifts to looking for new caregivers ourselves, we realized the only solution that would work for families would require a new model of childcare designed for the unique issues COVID-19 has created,” said Cleo CEO Sarahjane Sacchetti.

Sacchetti, the former chief marketing officer of Collective Health, stepped in to lead Cleo after its original co-founder Shannon Spanhake was ousted following issues around company culture and a falsified resumé. Since then, Cleo has been expanding its business in the form of numerous partnerships, including those with Natalist, Milk Stork, Playfully, Dadi and others.

The solution will roll out in pilot testing with large U.S. employers to start, the company says. International employers will have access to its Cleo Kids coaching solution while Cleo looks for partnerships with care provider networks outside the U.S.

The employers will pay a combined monthly membership fee for access to Cleo Kids and UrbanSitter as well as one-time matching fees for co-op matching or care provider matching and placement, when used by a family. Cleo says it’s working with employers to explore models to cover some of the matching costs, which can be supported if an employer offers a dependent care FSA.

A sign-up form is here.

Image credits: Cleo

Powered by WPeMatico

The world of healthcare has notoriously been described as “broken” — plagued with high-friction workflows, sky-high costs and convoluted business models.

Over the past several years, a long list of innovative startups and salivating venture investors have pinned their focus on repairing the healthcare industry, but its digital transformation still appears to be in the very early innings. After a record-setting 2018, however, digital health investing continued to reach meteoric heights in 2019.

Mammoth pools of capital have flooded into various sub-verticals and business models, backing collections of new B2B and B2C companies focused on optimizing healthcare workflows, improving healthcare access and offering lower-cost distribution models. Over the past two years, digital health startups have raised well over $10 billion in funding across nearly 1,000 deals, according to data from Pitchbook and Crunchbase.

As we close out another strong year for innovation and venture investing in the sector, we asked nine leading VCs who work at firms spanning early to growth stages to share what’s exciting them most and where they see opportunity in the sector:

Participants discuss trends in digital therapeutics, telehealth, mental health and the latest in biotech and medical devices, while also diving into startups improving medical practitioner efficiency, evaluating the evolving regulatory environment and debating valuations and offering a ‘temp check’ on the market for digital health startups leveraging ML.

Although Kleiner Perkins has a long history of investing in iconic health companies, we believe it is still the early innings of digital health as a category today.

When I evaluate new opportunities in the space, I often start by thinking through how the company will move the needle on cost, quality, and access to care — the “iron triangle” of health care systems. Conventional wisdom has been that it’s impossible to improve all three dimensions simultaneously, but we are seeing companies leverage technology to shift this paradigm in meaningful ways.

It’s no longer just a promise. For example, Viz.ai is using artificial intelligence to detect and alert stroke teams to suspected large vessel occlusion strokes, enabling patients to get treatment faster. Their workflows improve access to life-saving care, deliver higher quality through reduced time to treatment (every minute counts as ‘time is brain’ in stroke care), and dramatically reduce the costs associated with long-term disability.

We are also seeing companies provide this type of tech-enabled care outside of the hospital setting. Modern Health is a mental health benefits platform that employers are making available to their employees. The platform triages individual employees to the right level of care, providing clinical care to those with diagnosable depression or anxiety, and making self-guided or preventative care available to everyone else. Their solution improves quality and access by offering mental health services to every employee and reduces the cost associated with untreated mental illness, lost productivity, or employee churn.

Heading into 2020, we’re eager to back digital health companies in new areas that leverage technology to impact cost, quality, and access. A few spaces that I’m excited about are behavioral health (mental health, substance abuse, addiction, etc), care navigation, digital therapeutics, and new models integrating telehealth, remote care and AI to better leverage medical professionals’ time.

Below are some thoughts and coming predictions on health tech broadly:

- Digital therapeutics continue to pick up steam — on the back of Pear and Akili, more companies push to FDA and enter the market. In addition, broader consumer platforms like Calm and Headspace look to broaden their offerings by investigating clinical approvals.

- At least one major pharma looks to expand its consumer surface area by acquiring one of the new digital, consumer-facing generics platform (ex Hims, Ro, NuRx).

- Venture funding for biotech continues to boom with at least three Series A’s of $100M or more in size.

- Drug discovery for neurodegeneration sees a renaissance. High-profile failings of Biogen and the beta-amyloid hypothesis sees a shift of innovation to early-stage biotech and venture creation.

- Big pharma has its DeepMind moment acquiring at least one machine-learning (AI) enabled drug discovery company.

- Clinical trial tech investments heat up; new companies and technologies emerge to make trials patients first and systems get smarter at finding the right patients at their point of care; large incumbents like IQVIA, LabCorp and PPD get acquisitive.

- At least three traditional Sand Hill Road tech venture firms open life science practices or raise dedicated funds.

- Machine learning targets chemistry driven by large advancements in transformer (NLP) models; has the time for computational chemistry finally come?

- HCIT sees a renaissance driven by increased CIO responsibility towards data interoperability. Companies either working on federated ML to allow systems to speak to each other or lightweight edge applications enabling rapid clinical deployment will see quick uptake and traction, until now impossible in HC.

Kristin Baker Spohn, CRV

In the last 10 years, digital health has exploded. Over $16B has been invested in the sector by VCs and we’ve seen IPOs from Livongo, Progyny and Health Catalyst, just in the last year alone. That said, there’s still a lot that mystifies people about the sector — there are spots that are overheated and models that will struggle to deliver venture scale outcomes. I’ve seen digital health evolve first hand as both an operator and investor, and I’m more excited than ever about the future of the space.

A few areas and trends that I’ve been following recently include:

Powered by WPeMatico

Cleo, the London-based “digital assistant” that wants to replace your banking apps, has quietly taken venture debt from U.S.-based TriplePoint Capital, according to a regulatory filing.

The amount remains undisclosed, though I understand from sources that the figure is somewhere in the region of mid-“single-digit” millions and will bridge the gap before a larger Series B round later this year. Cleo declined to comment on the fundraising.

However, sources tell me the need to raise debt financing is partly related to Cleo Plus, the startup’s stealthy premium offering that is currently being tested and set to launch more widely soon. The new product offers Cleo users a range of perks, including rewards and an optional £100 cash advance as an alternative to using your bank’s overdraft facility. The credit facility is, for the time bring at least, being financed from the startup’s own balance sheet, hence the need for additional capital.

The new funding also relates to Cleo’s U.S. launch, which began tentatively around a year ago. This has been more successful than was expected, seeing Cleo add 650,000 active U.S. users to date. The U.S. currently makes up more than 90% of new users now, too. Overall, the fintech claims 1.3 million users have signed up to the Cleo chatbot and app, with 350,000 active in the U.K.

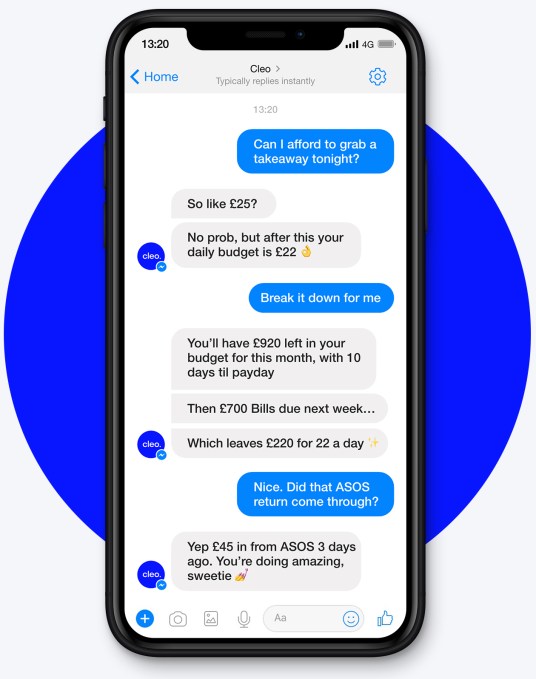

Accessible via Facebook Messenger and the company’s iOS app, Cleo is an AI-powered chatbot that gives you insights into your spending across multiple accounts and credit cards, broken down by transaction, category or merchant. In addition, Cleo lets you take a number of actions based on the financial data it has gleaned. This includes choosing to put money aside for a rainy day or specific goal, sending money to your Facebook Messenger contacts, donating to charity and setting spending alerts and more.

Meanwhile, alongside TriplePoint, Cleo is backed by some of the biggest VC names in the London tech scene — including Balderton Capital, Entrepreneur First, Moonfruit co-founders Wendy Tan White and Joe White, Skype founder Niklas Zennström, Wonga founder Errol Damelin, TransferWise founder Taavet Hinrikus and LocalGlobe.

Powered by WPeMatico

When Cleo, the London-based “digital assistant” that wants to replace your banking apps, quietly entered the U.S., the company couldn’t have expected to be an instant hit. Many better-funded British startups have failed to “break America.” However, just four months later, the fintech upstart counts 350,000 users across the pond — claiming more than 600,000 active users in the U.K., U.S. and Canada in total — and says it is adding 30,000 new signups each week. All of which hasn’t gone unnoticed by investors.

Already backed by some of the biggest VC names in the London tech scene — including Entrepreneur First, Moonfruit founder Wendy Tan White, Skype founder Niklas Zennström, Wonga founder Errol Damelin, TransferWise founder Taavet Hinrikus and LocalGlobe — Cleo is adding Balderton Capital to the list.

The European venture capital firm, which has previously invested in fintech unicorn Revolut and the well-established GoCardless, has led Cleo’s $10 million Series A round, in which I understand most early backers, including Zennström, also followed on. One source told me the Series A gives the hot London startup a post-money valuation of around £30 million (~$39.7m), although Cleo declined to comment.

The European venture capital firm, which has previously invested in fintech unicorn Revolut and the well-established GoCardless, has led Cleo’s $10 million Series A round, in which I understand most early backers, including Zennström, also followed on. One source told me the Series A gives the hot London startup a post-money valuation of around £30 million (~$39.7m), although Cleo declined to comment.

In a call with co-founder and CEO Barney Hussey-Yeo, he explained that the new capital will be used to continue scaling the company, with further international expansion the name of the game. Hussey-Yeo says Cleo will be targeting Western Europe, the Americas and Australasia, aiming to launch in a whopping 22 countries in the next 12 months, as Cleo bids to become the “default interface” for millennials interacting and managing their money.

Primarily accessed via Facebook Messenger, the AI-powered chatbot gives insights into your spending across multiple accounts and credit cards, broken down by transaction, category or merchant. In addition, Cleo lets you take a number of actions based on the financial data it has gleaned. You can choose to put money aside for a rainy day or specific goal, send money to your Facebook Messenger contacts, donate to charity, set spending alerts and more.

However, in the context of traction and Cleo’s broader global ambitions, it is the decision not to become a bank in its own right that Hussey-Yeo feels is really beginning to bear fruit. His argument has always been that you don’t need to be a bank to become the primary way users interface with their finances, and that without the regulatory and capital burden that becoming a fully licensed bank brings, you can scale much more quickly. I have a feeling that strategy — and its pros and cons — has a long way to play out just yet.

Powered by WPeMatico

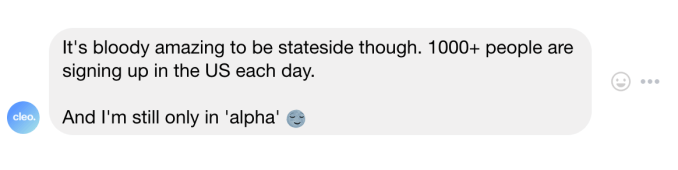

With little fuss or fanfare, Cleo, the London-based startup that offers an AI-powered chatbot as a replacement for your banking apps, has begun quietly offering its service to U.S. customers. Just 21 days in, I understand the U.K. fintech is already signing up 1,000 users across the pond per day.

Described as an “alpha version” by the chatbot itself (see screenshot below), the U.S. version sees Cleo add support for 647 banks and counting, a reflection of how fragmented the banking market in the U.S. is. As you’d expect, Cleo keeps the same conversational interface as its U.K. counterpart, albeit with what I’m told is a developing U.S. dialect (and selection of Gifs!). You can ask for and receive insights into your spending across multiple accounts and credit cards, broken down by transaction, category or merchant.

In addition, Cleo also lets you take a number of actions, including some based on the financial data it has gleaned. You can send money to your Facebook Messenger contacts via Cleo, donate to charity, and set spending goals and alerts and other fun financial antics.

In addition, Cleo also lets you take a number of actions, including some based on the financial data it has gleaned. You can send money to your Facebook Messenger contacts via Cleo, donate to charity, and set spending goals and alerts and other fun financial antics.

The bigger picture is to offer Cleo’s mostly millennial users a more accessible and intelligent way to manage their money, and ultimately become their default financial control centre, including recommending ways to save money and automatically switching to the best value products, whether that be financial or other services such as utilities.

It is a proposition that appears to be resonating with users. In the U.K., Cleo now claims more than 150,000 users, while I understand, following the startup’s stealthy, although tentative, U.S. expansion it is on track for 200,000 users globally. A source tells me the company is also eyeing up further international moves, citing Canada, Australia, New Zealand, Ireland, Singapore, and South Africa as next up on the road map.

What is fascinating now that we can see Cleo’s global ambitions begin to play out is the potential speed the U.K. startup can move because of the decision not to become a bank in its own right, which would otherwise bring significant capital and regulatory friction, not least in the fragmented U.S. market.

Cleo co-founder Barney Hussey-Yeo has always said that it is better to focus on building a better and smarter UI/UX than re-inventing the current account itself, even if the ultimate goal is somewhat the same. Or, to put it more simply, he argues that “nobody needs to be a bank to replace your banking app“.

Powered by WPeMatico