clearcover

Auto Added by WPeMatico

Auto Added by WPeMatico

Super.mx, an insurtech startup based in Mexico City, has raised $7.2 million in a Series A round led by ALLVP.

Co-founded in 2019 by a trio of former insurance industry executives, Super.mx’s self-proclaimed mission is to design insurance for “the emerging Latin American middle class,” according to CEO Sebastian Villarreal.

“That means insurance that is easy to buy – it can be bought on a cell phone in minutes – and that pays quickly with no adjusters,” he said. The company has built its offering with proprietary models that are used both on the underwriting side to predict risk and on the claims side to make payments automatically.

Goodwater Capital, Kairos Angels and Bridge Partners also participated in the Series A round in addition to angels such as Joe Schmidt IV, vice president of business development at insurtech Ethos and former investor at Accel and Kyle Nakatsuji, founder and CEO of auto insurance startup Clearcover (and also a former VC). Better Tomorrow Ventures led Super.mx’s $2.4 million seed round, which also saw capital from 500 Startups Mexico, Village Global, Anthemis and Broadhaven Ventures, among others.

Unlike most insurtech startups in Latin America, Villarreal emphasizes that Super.mx is neither an aggregator nor a carrier. Instead, it’s an MGA, or managing general agent.

“This lets us have a ‘best of both worlds’ approach,” Villarreal said. “We handle the entire user experience just like a direct to consumer carrier, but with the breadth of product choice offered by an aggregator.”

That product choice includes property, natural disasters and life insurance. The company soon plans to expand to also offer health insurance.

The founding team brings a variety of insurance experience to the table. Villarreal previously co-founded Chicago-based Kin Insurance (which raised over $150 million in funding from the likes of Flourish Ventures, Commerce Ventures and QED Investors). He was also once head of auto product at Avant, a growth-stage company funded by General Atlantic and Tiger Global, among others.

With over two decades of insurance industry experience, Dario Luna once served as Mexico’s insurance regulator and helped develop Mexico’s disaster risk management strategy. Marco Ahedo has designed parametric insurance products for 19 Caribbean countries. He was also once a solvency expert for life and health insurance lines at MetLife, and has developed financial models for several P&C carriers.

Villarreal lived in the U.S. for a while before deciding to move back to Mexico, which he recognized was home to an “underinsurance problem.”

“That’s actually a very acute problem,” he said. “People in Latin America buy a lot less insurance than they do in the U.S., and people in Mexico, in particular, buy a lot less insurance than they do in other Latin countries.”

Some have blamed the lack of insurance coverage on the country’s culture but Super.mx operates under the belief that this notion is “total BS.”

“It’s not a cultural problem,” Villarreal said. “The problem is that the insurance products that exist in the market just suck. They’re super expensive. They’re really hard to buy, and they pay very little.”

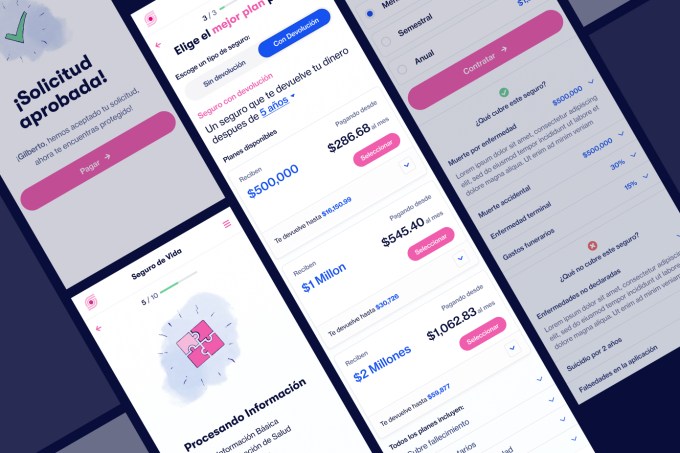

Image Credits: Super.mx

So far, Super.mx has sold “thousands of policies” but is more focused now on increasing the number of products that it’s selling. The company started out by selling earthquake insurance before adding COVID insurance, and more recently, in April, it launched life insurance. Next, it’s going to offer property, renter’s and health insurance.

“It’s really a different strategy than what you would find in the U.S.,” Villarreal said. “In the U.S, when you look at insurtechs, it’s like everyone just does one thing, but here, it’s very different because when someone says ‘I want insurance,’ really what they’re saying is ‘Hey, something happened that makes me nervous that didn’t make me nervous before.’”

That something could be a new child, for example, that prompts a need for life insurance.

“What we’re trying to do is like Lemonade, Roots and Hippo or Kin all rolled into one,” he added. It’s a big, big play.”

Digital adoption in Mexico, and Latin America in general, has increased exponentially in recent years. The bigger hurdle for Super.mx, according to Villarreal, has less to do with technology and more to do with Mexicans getting over what he describes a “deep mistrust” based on bad experiences in the past.

“People are really distrustful and that’s a huge hurdle, but once you show them that you actually are different,” Villarreal told TechCrunch, “that you actually do things in a different way, you get this incredible emotional response.”

Eventually, Super.mx plans to outside of Mexico to other countries in Latin America.

ALLVP’s Federico Antoni said his Mexico City-based firm had been looking for a team building in this space “for years” before investing in Super.mx. The venture firm was impressed with the company’s technical knowledge and industry expertise. It was also drawn to their multi-product approach and “capacity to ship highly complex products to the market quickly” — both of which he believes are “unique” in the region.

Citing statistics from MAPFRE Economics, Antoni pointed out that globally, the insurance market has been growing over the last 10 years. During that time, Latin America expanded faster on average (4.4% vs. 2.4% worldwide), albeit with more volatility. Life insurance has been driving this growth, at 6.1%, over the period.

“Insurtech may be even bigger than fintech. Also, harder,” he told TechCrunch via email. “We knew the team to unlock the market potential would need to be highly competent and highly disruptive.”

Antoni said he is also convinced that Insurtech is the “next frontier” in financial inclusion in Latin America especially as digitization continues to increase.

“Providing risk coverage to individuals and businesses in the region, brings financial stability to families and unlocks economic potential for SMEs,” he said. “Moreover, the insurance incumbents have been unable to address a growing and underserved market.”

Powered by WPeMatico

Last night neo-insurance provider and former startup Root priced its IPO at $27 per share, $2 per share ahead of its $22 to $25 target price range.

According to Root, it sold 26,830,845 shares in its IPO, including 24,249,330 from the company itself. Its underwriting banks have the option to buy another 4,024,626 at the IPO price, less “underwriting discounts and commissions.” The remaining shares are being sold by existing shareholders.

At $27 per share, Root raised $654,731,910, but that figure will rise to $763,396,812 if its underwriters exercise their option in full, using the full $27 price for our calculation. Per its S-1 filings, both Dragoneer and Silver Lake will purchase $250 million of Root stock at the IPO price once the IPO has closed.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, in a first, we have two editions of The Exchange for you. Get hype.

Root will therefore raise north of $1 billion in its IPO, once all shares sold are counted. Doing some loose math, Root is worth around $6.8 billion at its IPO price, though Renaissance Capital, an IPO specialist, puts the figure at $7.1 billion on a fully diluted basis.

For the Midwest, Ohio-based Root’s IPO is a win. The company shows that it is possible to build high-growth technology companies worth billions of dollars far from coastal hubs. For the broader insurtech space, Root’s IPO is a win. The company follows Lemonade to the public markets, setting a strong valuation mark again for the neo-insurance startup market.

For the Midwest, Ohio-based Root’s IPO is a win. The company shows that it is possible to build high-growth technology companies worth billions of dollars far from coastal hubs. For the broader insurtech space, Root’s IPO is a win. The company follows Lemonade to the public markets, setting a strong valuation mark again for the neo-insurance startup market.

For similar companies like Clearcover, MetroMile and all startups that related to Root and Lemonade, it’s a good day. Let’s get into what we can learn from Root’s pricing.

Insurance multiples are hot. Key from Root’s IPO is the fact that we can now see insurance revenue being treated similarly to software revenue. How so? In multiples terms. Let me explain.

Root generated $245.4 million in revenue during the first and second quarters of 2020. That’s a run rate of around $491 million. At $7 billion, that’s a 14x revenue multiple. For an insurance provider with scant gross margins! Wild. Given Root’s weak-looking Q3 2020 revenues, that number isn’t going to fall anytime soon.

For companies that are not pure-play software outfits and want to go public, Root’s strong, above-range pricing makes it plain that there is investor demand for more than one type of revenue growth.

Investors are betting that Root’s history of growth will continue. In the first half of 2019, the company’s revenues were a mere 42% of what it pulled off during the same period in 2020. If the company can more than double again next year, then, hey, maybe all the numbers work. But to see public shareholders take such a growth-and-valuation flyer on an insurtech player is notable.

Kyle Nakatsuji, co-founder and CEO of Clearcover, another neo-insurance provider, explained to TechCrunch via email what he thinks is going on: “It’s clear that the market is aware of the massive opportunity for technology-enabled disruption in the category and it is rewarding those companies that focus on customer-oriented, digital innovation. The rapid growth of key players in the space is now proving this will play out and the winners will be consumers seeing lower prices and investors seeing better returns. ”

Powered by WPeMatico