cities

Auto Added by WPeMatico

Auto Added by WPeMatico

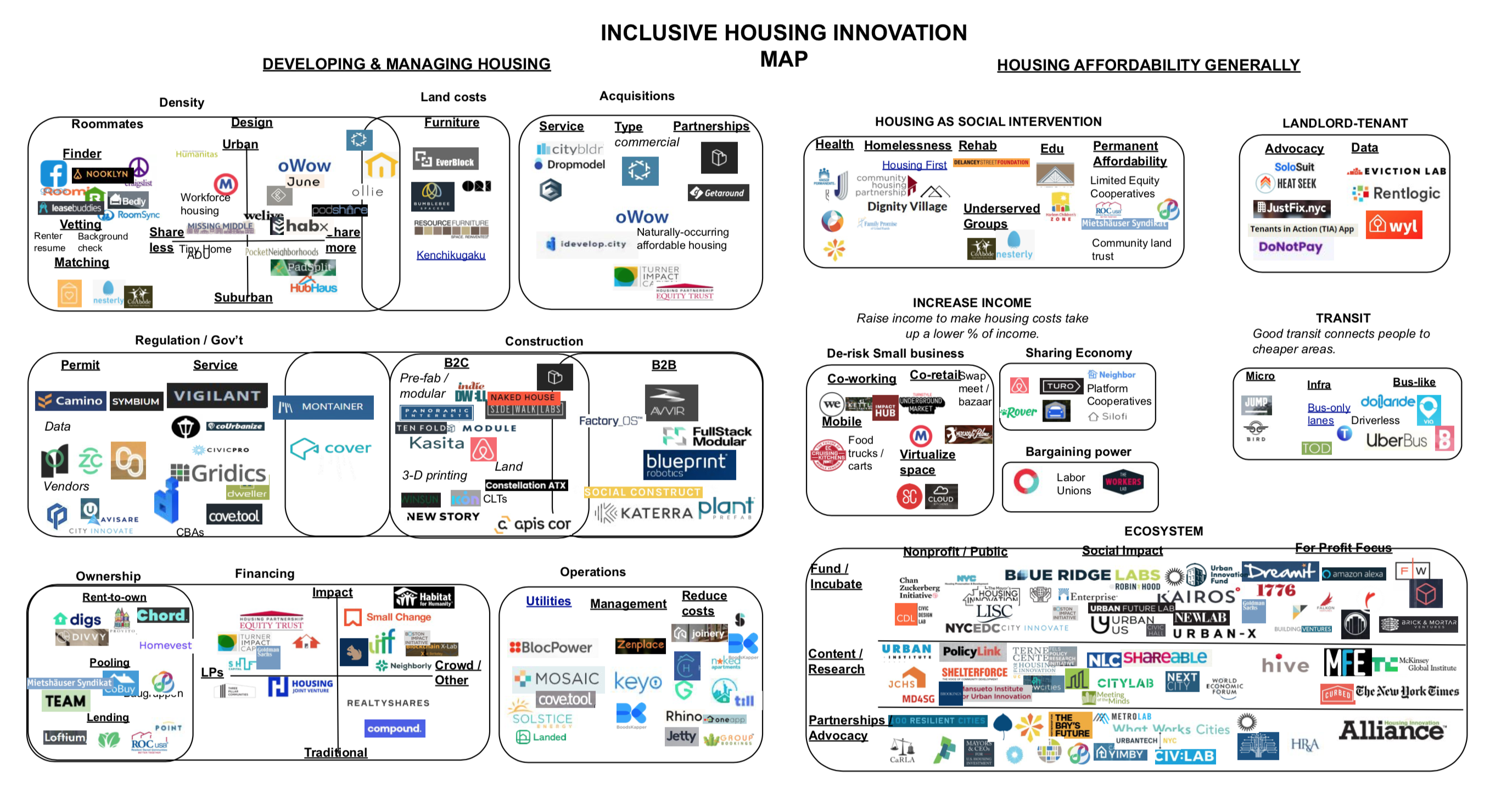

Housing is big money. The industry has trillions under management and hundreds of billions under development.

And investors have noticed the potential. Opendoor raised nearly $1.3 billion to help homeowners buy and sell houses more quickly. Katerra raised $1.2 billion to optimize building development and construction, and Compass raised the same amount to help brokers sell real estate better. Even Amazon and Airbnb have entered the fray with high-profile investments.

Amidst this frenetic growth is the seed of the next wave of innovation in the sector. The housing industry — and its affordability problem — is only likely to balloon. By 2030, 84% of the population of developed countries will live in cities.

Yet innovation in housing lags compared to other industries. In construction, a major aspect of housing development, players spend less than 1% of their revenues on research and development. Technology companies, like the Amazons of the world, spend nearly 10% on average.

Innovations in older, highly regulated industries, like housing and real estate, are part of what Steve Case calls the “third wave” of technology. VCs like Case’s Revolution Fund and the SoftBank Vision Fund are investing billions into what they believe is the future.

These innovations are far from silver bullets, especially if they lack involvement from underrepresented communities, avoid policy and ignore distributive questions about who gets to benefit from more housing.

Yet there are hundreds of interventions reworking housing that cannot be ignored. To help entrepreneurs, investors and job seekers interested in creating better housing, I mapped these innovations in this package of articles.

To make sense of this broad field, I categorize innovations into two main groups, which I detail in two separate pieces on Extra Crunch. The first (Part 1) identifies the key phases of developing and managing housing. The second (Part 2) section identifies interventions that contribute to housing inclusion more generally, such as efforts to pair housing with transit, small business creation and mental rehabilitation.

Unfortunately, many of these tools don’t guarantee more affordability. Lowering acquisition costs, for instance, doesn’t mean that renters or homeowners will necessarily benefit from those savings. As a result, some tools likely need to be paired with others to ensure cost savings that benefit end users — and promote long-term affordability. I detail efforts here so that mission-driven advocates as well as startup founders can adopt them for their own efforts.

Today:

Coming Tomorrow:

Please feel free to let me know what else is exciting by adding a note to your LinkedIn invite here.

If you’re excited about this topic, feel free to subscribe to my future of inclusive housing newsletter by viewing a past issue here.

Powered by WPeMatico

It feels like there’s a WeWork on every street nowadays. Take a walk through midtown Manhattan (please don’t actually) and it might even seem like there are more WeWorks than office buildings.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

Co-working has permeated cities around the world at an astronomical rate. The rise has been so remarkable that even the headline-dominating SoftBank seems willing to bet the success of its colossal Vision Fund on the shift continuing, having poured billions into WeWork – including a recent $4.4 billion top-up that saw the co-working king’s valuation spike to $45 billion.

And there are no signs of the trend slowing down. With growing frequency, new startups are popping up across cities looking to turn under-utilized brick-and-mortar or commercial space into low-cost co-working options.

It’s a strategy spreading through every type of business from retail – where companies like Workbar have helped retailers offer up portions of their stores – to more niche verticals like parking lots – where companies like Campsyte are transforming empty lots into spaces for outdoor co-working and corporate off-sites. Restaurants and bars might even prove most popular for co-working, with startups like Spacious and KettleSpace turning restaurants that are closed during the day into private co-working space during their off-hours.

Before you know it, a startup will be strapping an Aeron chair to the top of a telephone pole and calling it “WirelessWorking”.

But is there a limit to how far co-working can go? Are all of the storefronts, restaurants and open spaces that line city streets going to be filled with MacBooks, cappuccinos and Moleskine notebooks? That might be too tall a task, even for the movement taking over skyscrapers.

Photo: Vasyl Dolmatov / iStock via Getty Images

So why is everyone trying to turn your favorite neighborhood dinner spot into a part-time WeWork in the first place? Co-working offers a particularly compelling use case for under-utilized space.

First, co-working falls under the same general commercial zoning categories as most independent businesses and very little additional infrastructure – outside of a few extra power outlets and some decent WiFi – is required to turn a space into an effective replacement for the often crowded and distracting coffee shops used by price-sensitive, lean, remote, or nomadic workers that make up a growing portion of the workforce.

Thus, businesses can list their space at little-to-no cost, without having to deal with structural layout changes that are more likely to arise when dealing with pop-up solutions or event rentals.

On the supply side, these co-working networks don’t have to purchase leases or make capital improvements to convert each space, and so they’re able to offer more square footage per member at a much lower rate than traditional co-working spaces. Spacious, for example, charges a monthly membership fee of $99-$129 dollars for access to its network of vetted restaurants, which is cheap compared to a WeWork desk, which can cost anywhere from $300-$800 per month in New York City.

Customers realize more affordable co-working alternatives, while tight-margin businesses facing increasing rents for under-utilized property are able to pool resources into a network and access a completely new revenue stream at very little cost. The value proposition is proving to be seriously convincing in initial cities – Spacious told the New York Times, that so many restaurants were applying to join the network on their own volition that only five percent of total applicants were ultimately getting accepted.

Basically, the business model here checks a lot of the boxes for successful marketplaces: Acquisition and transaction friction is low for both customers and suppliers, with both seeing real value that didn’t exist previously. Unit economics seem strong, and vetting on both sides of the market creates trust and community. Finally, there’s an observable network effect whereby suppliers benefit from higher occupancy as more customers join the network, while customers benefit from added flexibility as more locations join the network.

Photo: Caiaimage / Robert Daly via Getty Images

So is this the way of the future? The strategy is really compelling, with a creative solution that offers tremendous value to businesses and workers in major cities. But concerns around the scalability of demand make it difficult to picture this phenomenon becoming ubiquitous across cities or something that reaches the scale of a WeWork or large conventional co-working player.

All these companies seem to be competing for a similar demographic, not only with one another, but also with coffee shops, free workspaces, and other flexible co-working options like Croissant, which provides members with access to unused desks and offices in traditional co-working spaces. Like Spacious and KettleSpace, the spaces on Croissant own the property leases and are already built for co-working, so Croissant can still offer comparatively attractive rates.

The offer seems most compelling for someone that is able to work without a stable location and without the amenities offered in traditional co-working or office spaces, and is also price sensitive enough where they would trade those benefits for a lower price. Yet at the same time, they can’t be too price sensitive, where they would prefer working out of free – or close to free – coffee shops instead of paying a monthly membership fee to avoid the frictions that can come with them.

And it seems unclear whether the problem or solution is as poignant outside of high-density cities – let alone outside of high-density areas of high-density cities.

Without density, is the competition for space or traffic in coffee shops and free workspaces still high enough where it’s worth paying a membership fee for? Would the desire for a private working environment, or for a working community, be enough to incentivize membership alone? And in less-dense and more-sprawl oriented cities, members could also face the risk of having to travel significant distances if space isn’t available in nearby locations.

While the emerging workforce is trending towards more remote, agile and nomadic workers that can do more with less, it’s less certain how many will actually fit the profile that opts out of both more costly but stable traditional workspaces, as well as potentially frustrating but free alternatives. And if the lack of density does prove to be an issue, how many of those workers will live in hyper-dense areas, especially if they are price-sensitive and can work and live anywhere?

To be clear, I’m not saying the companies won’t see significant growth – in fact, I think they will. But will the trend of monetizing unused space through co-working come to permeate cities everywhere and do so with meaningful occupancy? Maybe not. That said, there is still a sizable and growing demographic that need these solutions and the value proposition is significant in many major urban areas.

The companies are creating real value, creating more efficient use of wasted space, and fixing a supply-demand issue. And the cultural value of even modestly helping independent businesses keep the lights on seems to outweigh the cultural “damage” some may fear in turning them into part-time co-working spaces.

Powered by WPeMatico

In order to have innovative smart city applications, cities first need to build out the connected infrastructure, which can be a costly, lengthy, and politicized process. Third-parties are helping build infrastructure at no cost to cities by paying for projects entirely through advertising placements on the new equipment. I try to dig into the economics of ad-funded smart city projects to better understand what types of infrastructure can be built under an ad-funded model, the benefits the strategy provides to cities, and the non-obvious costs cities have to consider.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

When we talk about “Smart Cities”, we tend to focus on these long-term utopian visions of perfectly clean, efficient, IoT-connected cities that adjust to our environment, our movements, and our every desire. Anyone who spent hours waiting for transit the last time the weather turned south can tell you that we’ve got a long way to go.

But before cities can have the snazzy applications that do things like adjust infrastructure based on real-time conditions, cities first need to build out the platform and technology-base that applications can be built on, as McKinsey’s Global Institute explained in an in-depth report released earlier this summer. This means building out the network of sensors, connected devices and infrastructure needed to track city data.

However, reaching the technological base needed for data gathering and smart communication means building out hard physical infrastructure, which can cost cities a ton and can take forever when dealing with politics and government processes.

Many cities are also dealing with well-documented infrastructure crises. And with limited budgets, local governments need to spend public funds on important things like roads, schools, healthcare and nonsensical sports stadiums which are pretty much never profitable for cities (I’m a huge fan of baseball but I’m not a fan of how we fund stadiums here in the states).

As city infrastructure has become increasingly tech-enabled and digitized, an interesting financing solution has opened up in which smart city infrastructure projects are built by third-parties at no cost to the city and are instead paid for entirely through digital advertising placed on the new infrastructure.

I know – the idea of a city built on ad-revenue brings back soul-sucking Orwellian images of corporate overlords and logo-paved streets straight out of Blade Runner or Wall-E. Luckily for us, based on our discussions with developers of ad-funded smart city projects, it seems clear that the economics of an ad-funded model only really work for certain types of hard infrastructure with specific attributes – meaning we may be spared from fire hydrants brought to us by Mountain Dew.

While many factors influence the viability of a project, smart infrastructure projects seem to need two attributes in particular for an ad-funded model to make sense. First, the infrastructure has to be something that citizens will engage – and engage a lot – with. You can’t throw a screen onto any object and expect that people will interact with it for more than 3 seconds or that brands will be willing to pay to throw their taglines on it. The infrastructure has to support effective advertising.

Second, the investment has to be cost-effective, meaning the infrastructure can only cost so much. A third-party that’s willing to build the infrastructure has to believe they have a realistic chance of generating enough ad-revenue to cover the costs of the projects, and likely an amount above that which could lead to a reasonable return. For example, it seems unlikely you’d find someone willing to build a new bridge, front all the costs, and try to fund it through ad-revenue.

A LinkNYC kiosk enabling access to the internet in New York on Saturday, February 20, 2016. Over 7500 kiosks are to be installed replacing stand alone pay phone kiosks providing free wi-fi, internet access via a touch screen, phone charging and free phone calls. The system is to be supported by advertising running on the sides of the kiosks. ( Richard B. Levine) (Photo by Richard Levine/Corbis via Getty Images)

To get a better understanding of the types of smart city hardware that might actually make sense for an ad-funded model, we can look at the engagement levels and cost structures of smart kiosks, and in particular, the LinkNYC project. Smart kiosks – which provide free WiFi, connectivity and real-time services to citizens – have been leading examples of ad-funded smart city projects. Innovative companies like Intersection (developers of the LinkNYC project), SmartLink, IKE, Soofa, and others have been helping cities build out kiosk networks at little-to-no cost to local governments.

LinkNYC provides public access to much of its data on the New York City Open-Data website. Using some back-of-the-envelope math and a hefty number of assumptions, we can try to get to a very rough range of where cost and engagement metrics generally have to fall for an ad-funded model to make sense.

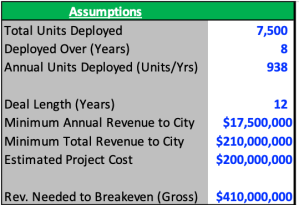

To try and retrace considerations for the developers’ investment decision, let’s first look at the terms of the deal signed with New York back in 2014. The agreement called for a 12-year franchise period, during which at least 7,500 Link kiosks would be deployed across the city in the first eight years at an expected project cost of more than $200 million. As part of its solicitation, the city also required the developers to pay the greater of either a minimum annual payment of at least $17.5 million or 50 percent of gross revenues.

Let’s start with the cost side – based on an estimated project cost of around $200 million for at least 7,500 Links, we can get to an estimated cost per unit of $25,000 – $30,000. It’s important to note that this only accounts for the install costs, as we don’t have data around the other cost buckets that the developers would also be on the hook for, such as maintenance, utility and financing costs.

Source: LinkNYC, NYC.gov, NYCOpenData

Turning to engagement and ad-revenue – let’s assume that the developers signed the deal with the expectations that they could at least breakeven – covering the install costs of the project and minimum payments to the city. And for simplicity, let’s assume that the 7,500 links were going to be deployed at a steady pace of 937-938 units per year (though in actuality the install cadence has been different). In order for the project to breakeven over the 12-year deal period, developers would have to believe each kiosk could generate around $6,400 in annual ad-revenue (undiscounted).

Source: LinkNYC, NYC.gov, NYCOpenData

The reason the kiosks can generate this revenue (and in reality a lot more) is because they have significant engagement from users. There are currently around 1,750 Links currently deployed across New York. As of November 18th, LinkNYC had over 720,000 weekly subscribers or around 410 weekly subscribers per Link. The kiosks also saw an average of 18 million sessions per week, or 20-25 weekly sessions per subscriber, or around 10,200 weekly sessions per kiosk (seasonality might even make this estimate too low).

And when citizens do use the kiosks, they use it for a long time! The average session for each Link unit was four minutes and six seconds. The level of engagement makes sense since city-dwellers use these kiosks in time or attention-intensive ways, such making phone calls, getting directions, finding information about the city, or charging their phones.

The analysis here isn’t perfect, but now we at least have a (very) rough idea of how much smart kiosks cost, how much engagement they see, and the amount of ad-revenue developers would have to believe they could realize at each unit in order to ultimately move forward with deployment. We can use these metrics to help identify what types of infrastructure have similar profiles and where an ad-funded project may make sense.

Bus stations, for example, may cost about $10,000 – $15,000, which is in a similar cost range as smart kiosks. According to the MTA, the NYC bus system sees over 11.2 million riders per week or nearly 700 riders per station per week. Rider wait times can often be five-to-ten minutes in length if not longer. Not to mention bus stations already have experience utilizing advertising to a certain degree. Projects like bike-share docking stations and EV charging stations also seem to fit similar cost profiles while having high engagement.

And interactions with these types of infrastructure are ones where users may be more receptive to ads, such as an EV charging station where someone is both physically engaging with the equipment and idly looking to kill up sometimes up to 30 minutes of time as they charge up. As a result, more companies are using advertising models to fund projects that fit this mold, like Volta, who uses advertising to offer charging stations free to citizens.

When it makes sense for cities and third-party developers, advertising-funded smart city infrastructure projects can unlock a tremendous amount of value for a city. The benefits are clear – cities pay nothing, citizens are offered free connectivity and real-time information on local conditions, and smart infrastructure is built and can possibly be used for other smart city applications down the road, such as using locational data tracking to improve city zoning and congestion.

Yes, ads are usually annoying – but maybe understanding that advertising models only work for specific types of smart city projects may help quell fears that future cities will be covered inch-to-inch in mascots. And ads on projects like LinkNYC promote local businesses and can tap into idiosyncratic conditions and preferences of regional communities – LinkNYC previously used real-time local transit data to display beer ads to subway riders that were facing heavy delays and were probably in need of a drink.

Like everyone’s family photos from Thanksgiving, the picture here is not all roses, however, and there are a lot of deep-rooted issues that exist under the surface. Third-party developed, advertising-funded infrastructure comes with externalities and less obvious costs that have been fairly criticized and debated at length.

When infrastructure funding is derived from advertising, concerns arise over whether services will be provided equitably across communities. Many fear that low-income or less-trafficked communities that generate less advertising demand could end up having poor infrastructure and maintenance.

Even bigger points of contention as of late have been issues around data consent and treatment. I won’t go into much detail on the issue since it’s incredibly complex and warrants its own lengthy dissertation (and many have already been written).

But some of the major uncertainties and questions cities are trying to answer include: If third-parties pay for, manage and operate smart city projects, who should own data on citizens’ living behavior? How will citizens give consent to provide data when tracking systems are built into the environment around them? How can the data be used? How granular can the data get? How can we assure citizens’ information is secure, especially given the spotty track records some of the major backers of smart city projects have when it comes to keeping our data safe?

The issue of data treatment is one that no one has really figured out yet and many developers are doing their best to work with cities and users to find a reasonable solution. For example, LinkNYC is currently limited by the city in the types of data they can collect. Outside of email addresses, LinkNYC doesn’t ask for or collect personal information and doesn’t sell or share personal data without a court order. The project owners also make much of its collected data publicly accessible online and through annually published transparency reports. As Intersection has deployed similar smart kiosks across new cities, the company has been willing to work through slower launches and pilot programs to create more comfortable policies for local governments.

But consequential decisions related to third-party owned smart infrastructure are only going to become more frequent as cities become increasingly digitized and connected. By having third-parties pay for projects through advertising revenue or otherwise, city budgets can be focused on other vital public services while still building the efficient, adaptive and innovative infrastructure that can help solve some of the largest problems facing civil society. But if that means giving up full control of city infrastructure and information, cities and citizens have to consider whether the benefits are worth the tradeoffs that could come with them. There is a clear price to pay here, even when someone else is footing the bill.

Powered by WPeMatico

A steep and rapid rise in tourism has left behind a wake of economic and environmental damage in cities around the globe. In response, governments have been responding with policies that attempt to limit the number of visitors who come in. We’ve decided to spare you from any more Amazon HQ2 talk and instead focus on why cities should shy away from reactive policies and should instead utilize their growing set of technological capabilities to change how they manage tourists within city lines.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

Well – it didn’t take long for the phrase “overtourism” to get overused. The popular buzzword describes the influx of tourists who flood a location and damage the quality of life for full-time residents. The term has become such a common topic of debate in recent months that it was even featured this past week on Oxford Dictionaries’ annual “Words of the Year” list.

But the expression’s frequent appearance in headlines highlights the growing number of cities plagued by the externalities from rising tourism.

In the last decade, travel has become easier and more accessible than ever. Low-cost ticketing services and apartment-rental companies have brought down the costs of transportation and lodging; the ubiquity of social media has ticked up tourism marketing efforts and consumer demand for travel; economic globalization has increased the frequency of business travel; and rising incomes in emerging markets have opened up travel to many who previously couldn’t afford it.

Now, unsurprisingly, tourism has spiked dramatically, with the UN’s World Tourism Organization (UNWTO) reporting that tourist arrivals grew an estimated 7% in 2017 – materially above the roughly 4% seen consistently since 2010. The sudden and rapid increase of visitors has left many cities and residents overwhelmed, dealing with issues like overcrowding, pollution, and rising costs of goods and housing.

The problems cities face with rising tourism are only set to intensify. And while it’s hard for me to imagine when walking shoulder-to-shoulder with strangers on tight New York streets, the number of tourists in major cities like these can very possibly double over the next 10 to 15 years.

China and other emerging markets have already seen significant growth in the middle-class and have long runway ahead. According to the Organization for Economic Co-operation and Development (OECD), the global middle class is expected to rise from the 1.8 billion observed in 2009 to 3.2 billion by 2020 and 4.9 billion by 2030. The new money brings with it a new wave of travelers looking to catch a selfie with the Eiffel Tower, with the UNWTO forecasting international tourist arrivals to increase from 1.3 billion to 1.8 billion by 2030.

With a growing sense of urgency around managing their guests, more and more cities have been implementing policies focused on limiting the number of tourists that visit altogether by imposing hard visitor limits, tourist taxes or otherwise.

But as the UNWTO points out in its report on overtourism, the negative effects from inflating tourism are not solely tied to the number of visitors in a city but are also largely driven by touristy seasonality, tourist behavior, the behavior of the resident population, and the functionality of city infrastructure. We’ve seen cities with few tourists, for example, have experienced similar issues to those experienced in cities with millions.

While many cities have focused on reactive policies that are meant to quell tourism, they should instead focus on technology-driven solutions that can help manage tourist behavior, create structural changes to city tourism infrastructure, while allowing cities to continue capturing the significant revenue stream that tourism provides.

THOMAS COEX/AFP/Getty Images

Yes, cities are faced with the headwind of a growing tourism population, but city policymakers also benefit from the tailwind of having more technological capabilities than their predecessors. With the rise of smart city and Internet of Things (IoT) initiatives, many cities are equipped with tools such as connected infrastructure, lidar-sensors, high-quality broadband, and troves of data that make it easier to manage issues around congestion, infrastructure, or otherwise.

On the congestion side, we have already seen companies using geo-tracking and other smart city technologies to manage congestion around event venues, roads, and stores. Cities can apply the same strategies to manage the flow of tourist and resident movement.

And while you can’t necessarily prevent people from people visiting the Louvre or the Coliseum, cities are using a variety of methods to incentivize the use of less congested space or disperse the times in which people flock to highly-trafficked locations by using tools such as real-time congestion notifications, data-driven ticketing schedules for museums and landmarks, or digitally-guided tours through uncontested routes.

Companies and municipalities in cities like London and Antwerp are already working on using tourist movement tracking to manage crowds and help notify and guide tourists to certain locations at the most efficient times. Other cities have developed augmented reality tours that can guide tourists in real-time to less congested spaces by dynamically adjusting their routes.

A number of startups are also working with cities to use collected movement data to help reshape infrastructure to better fit the long-term needs and changing demographics of its occupants. Companies like Stae or Calthorpe Analytics use analytics on movement, permitting, business trends or otherwise to help cities implement more effective zoning and land use plans. City planners can use the same technology to help effectively design street structure to increase usable sidewalk space and to better allocate zoning for hotels, retail or other tourist-friendly attractions.

Focusing counter-overtourism efforts on smart city technologies can help adjust the behavior and movement of travelers in a city through a number of avenues, in a way tourist caps or tourist taxes do not.

And at the end of the day, tourism is one of the largest sources of city income, meaning it also plays a vital role in determining the budgets cities have to plow back into transit, roads, digital infrastructure, the energy grid, and other pain points that plague residents and travelers alike year-round. And by disallowing or disincentivizing tourism, cities can lose valuable capital for infrastructure, which can subsequently exacerbate congestion problems in the long-run.

Some cities have justified tourist taxes by saying the revenue stream would be invested into improving the issues overtourism has caused. But daily or upon-entry tourist taxes we’ve seen so far haven’t come close to offsetting the lost revenue from disincentivized tourists, who at the start of 2017 spent all-in nearly $700 per day in the US on transportation, souvenirs and other expenses according to the U.S. National Travel and Tourism Office.

In 2017, international tourism alone drove to $1.6 trillion in earnings and in 2016, travel & tourism accounted for roughly 1 in 10 jobs in the global economy according to the World Travel and Tourism Council. And the benefits of travel are not only economic, with cross-border tourism promoting transfers of culture, knowledge and experience.

But to be clear, I don’t mean to say smart city technology initiatives alone are going to solve overtourism. The significant wave of growth in the number of global travelers is a serious challenge and many of the issues that result from spiking tourism, like housing affordability, are incredibly complex and come down to more than just data. However, I do believe cities should be focused less on tourist reduction and more on solutions that enable tourist management.

Utilizing and allocating more resources to smart city technologies can not only more effectively and structurally limit the negative impacts from overtourism, but it also allows cities to benefit from a significant and high growth tourism revenue stream. Cities can then create a virtuous cycle of reinvestment where they plow investment back into its infrastructure to better manage visitor growth, resident growth, and quality of life over the long-term. Cities can have their cake and eat it too.

Powered by WPeMatico

Earlier this week in a new experimental newsletter I’ve been helping Danny Crichton on, we briefly discussed transit pundit Jarrett Walker’s article in The Atlantic arguing against the view that ridesharing and microtransit will be the future of mass transit. Instead, his thesis is that a properly operated and well-resourced bus system is much more efficient from a coverage, cost, space, and equality perspective.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

From an output perspective, Walker argues that by operating along variable routes based on at-your-door pick ups, microtransit actually takes more time to pick up fewer people on average. Walker also gives buses the edge from a cost and input perspective, since labor makes up 70% of transit operating costs in a pre-autonomous world and buses allow you to service more customers for the price of one driver.

“The driver’s time is far more expensive than maintenance, fuel, and all the other costs involved. In almost every public meeting I attend, citizens complain about seeing buses with empty seats, lecturing me about how smaller vehicles would be less wasteful. But that’s not the case. Because the cost is in the driver, a wise transit agency runs the largest bus it will ever need during the course of a shift. In an outer suburb, that empty big bus makes perfect sense if it will be mobbed by schoolchildren or commuters twice a day.”

But transit is not solely an issue of volume and unit economics, but one of managing public space. Walker explains that to ensure citizens don’t use more than their fair share of space, cities can either provide vehicles that are only marginally bigger than a human body, i.e. bikes and scooters, or have many people share large-scale vehicles, i.e. mass transit. Doing the latter through a mass fleet of on-demand microtransit solutions, Walker argues, increases congestion and makes it harder to manage scheduling and allocate infrastructure.

While the article offers an effective comparison of unit economics and acts as a useful primer on the various considerations for city transit agencies, some of the conclusions are a bit binary. The discussion is a bit singular in its focus of microtransit as a replacement of public transit rather than an additive service and doesn’t give much credit to the trip planning and space management capabilities of many microtransit services, nor changes in consumer expectations towards transportation.

But despite some of the gaps in the piece, Walker highlights two ideas that spill over to some broad areas that have caught my interest lately: Tolls and Parking.

Photo by Michael H via Getty Images

“To succeed, microtransit would have to help people get around cities better, not just make them feel good about hailing a ride on a phone. Full automation of vehicles, if indeed it ever arrives, might solve the labor problem—although it would put thousands of drivers out of work. But the congestion problem will remain.”

Like many, Walker argues that ridesharing aggravates city traffic rather than alleviates it. Even though ridesharing’s long-term impact on traffic is widely contested, nearly everyone agrees that a solution to urban congestion is desperately needed.

What’s interesting is that regardless of the discourse that surrounds them, trends in US tolling mechanisms seem to suggest American cities may be moving closer to congestion pricing methods.

As an example, solutions to congestion are top of mind behind the New York state election that saw Democrats taking control of both state legislative houses. Though it seems like the argument resurfaces every few years, the elections have brought renewed debate over the possible implementation of congestion pricing in New York City. In essence, congestion pricing is a system where drivers would pay higher prices for using high-traffic streets or entering high-traffic zones, allowing cities to better dictate the flow of drivers and reduce congestion.

Outside of the obvious political tension created by effectively implementing a new tax, some lawmakers have pushed back on the effectiveness of a congestion pricing policy, with some arguing that it can aggravate income inequality or that a policy addressing construction and pedestrians, rather than vehicles, would have a bigger impact on traffic.

However, over the past year or so, an increasing number of states have been rolling out highway tolls that are priced dynamically, instead of using traditional fixed-price tolls. The exact drivers behind the toll prices vary, with some cities charging prices based on traffic conditions and others charging varying prices for the use of express and HOV lanes.

Several new technologies and companies have also made it easier for local governments to implement more sophisticated, adjustable toll pricing or congestion fees at a much lower cost. In the past, congestion pricing systems around the world have required physical detection systems that can be extremely costly to implement.

Now, companies like ClearRoad are helping governments use a wide range of connected vehicle technologies to establish and collect road usage pricing from any location without the need for physical infrastructure. Oregon is one geography working with ClearRoad to manage its new opt-in road usage program where the state is able to calculate drivers’ usage of certain roads and their gas consumption, and then reimburse them for gas taxes they’re paying.

So even though people are still screaming at each other in state capitols, it seems like we may be closer to seeing congestion pricing in major cities than we think. And while executing these programs can be difficult and painfully slow (often needing to satisfy city regulations and tax laws forty layers deep), if these smaller-scale programs we’re seeing in the US are actually effective, congestion pricing may be a solution to plug chunky budget gaps, better finance infrastructure projects and replace lost gas tax revenue in an electric vehicle future.

In his piece, Walker goes back to some basic principles of urban design, highlighting that at their core, functioning cities come down to how millions of people share a comparatively tiny amount of space.

Walker explains that city dwellers that travel with cars and solo rideshare trips rather than with large-scale shared transit are effectively taking up more than their fair share of public space. While the argument is made in the context of ridesharing and congestion, the same idea applies to the less-discussed impact mass-transit ridesharing can have on city parking.

At least in the near-term, certain cities have seen ridesharing actually increase vehicle usage rather than reduce it (a claim rideshare companies dispute), resulting in an even wider gap between the supply and demand for available parking spots. And if people are using ridesharing but still choosing to own cars regardless, in an indirect fashion, they are similarly reducing the stock of available parking space by more than their fair share.

And while it makes sense that rideshare vehicles should receive a larger portion of the parking stock, given that it serves more passengers, the use of available parking by these vehicles can and has caused tension with local residents that have to store their cars further away.

There are companies like the mobility-focused data platform, Coord, that are working on tools geared towards helping cities and citizens more effectively allocate and plan parking strategies for the future multi-modal transportation network. And theoretically, ridesharing should reduce the number of vehicles in search of parking in the long-term. But at least for now, the impact on parking congestion is just another unintended consequence that weakens the argument for ridesharing as mass transit.

Powered by WPeMatico