citibank

Auto Added by WPeMatico

Auto Added by WPeMatico

U.K.-based startup Sylvera is using satellite, radar and lidar data-fuelled machine learning to bolster transparency around carbon offsetting projects in a bid to boost accountability and credibility — applying independent ratings to carbon offsetting projects.

The ratings are based on proprietary data sets it’s developed in conjunction with scientists from research organisations including UCLA, the NASA Jet Propulsion Laboratory and University College London.

It’s just grabbed $5.8 million in seed funding led by VC firm Index Ventures. All its existing institutional investors also participated — namely: Seedcamp, Speedinvest and Revent. It also has backing from leading angels, including the existing and former CEOs of NYSE, Thomson Reuters, Citibank and IHS Markit. (It confirms it has committed not to receive any investment from traditional carbon-intensive companies.) And it’s just snagged a $2 million research contract from Innovate UK.

The problem it’s targeting is that the carbon offsetting market suffers from a lack of transparency.

This fuels concerns that many offsetting projects aren’t living up to their claims of a net reduction in carbon emissions — and that “creative” carbon accountancy is rather being used to generate a lot of hot air: In the form of positive-sounding PR, which sums to meaningless greenwashing and more pollution as polluters get to keep on pumping out climate changing emissions.

Nonetheless, the carbon offset markets are poised for huge growth — of at least 15x by 2030 — as large corporates accelerate their net zero commitments. And Sylvera’s bet is that that will drive demand for reliable, independent data — to stand up the claimed impact.

How exactly is Sylvera benchmarking carbon offsets? Co-founder Sam Gill says its technology platform draws on multiple layers of satellite data to capture project performance data at scale and at a high frequency.

It applies machine learning to analyze and visualize the data, while also conducting what it bills as “deep analytical work to assess the underlying project quality”. Via that process it creates a standardised rating for a project, so that market participants are able to transact according to their preferences.

It makes its ratings and analysis data available to its customers via a web application and an API (for which it charges a subscription).

“We assess two critical areas of a project — its carbon performance, and its ‘quality’,” Gill tells TechCrunch. “We score a project against these criteria, and give them ratings — much like a Moody’s rating on a bond.”

Carbon performance is assessed by gathering “multi-layered data” from multiple sources to understand what is going on on the ground of these projects — such as via multiple satellite sources such as multispectral image, radar, and lidar data.

“We collate this data over time, ingest it into our proprietary machine learning algorithms, and analyse how the project has performed against its stated aims,” Gill explains.

Quality is assessed by considering the technical aspects of the project. This includes what Gill calls “additionality”; aka “does the project have a strong claim to delivering a better outcome than would have occurred but for the existence of the offset revenue?”.

There is a known problem with some carbon offsets claimed against forests where the landowner had no intention of logging, for example. So if there wasn’t going to be any deforestation the carbon credit is essentially bogus.

He also says it looks at factors like permanence (“how long will the project’s impacts last?”); co-benefits (“how well has the project incorporated the UN’s Sustainability Development Goals?); and risks (“how well is the project mitigating risks, in particular those from humans and those from natural causes?”).

Clearly it’s not an exact science — and Gill acknowledges risks, for example, are often interlinked.

“It is critical to assess these performance and quality in tandem,” he tells TechCrunch. “It’s not enough to simply say a project is achieving the carbon goals set out in its plan.

“If the additionality of a project is low (e.g. it was actually unlikely the project would have been deforested without the project) then the achievement of the carbon goals set out in the project does not generate the anticipated carbon goals, and the underlying offsets are therefore weaker than appreciated.”

Commenting on the seed funding in a statement, Carlos Gonzalez-Cadenas, partner at Index Ventures, said: “This is a phenomenally strong team with the vision to build the first carbon offset rating benchmark, providing comprehensive insights around the quality of offsets, enabling purchase decisions as well as post-purchase monitoring and reporting. Sylvera is putting in place the building blocks that will be required to address climate change.”

Powered by WPeMatico

Financial service companies like banks have seen some of their business cannibalised over the years with the rise of digital-based alternatives — often in the form of apps — that provide lower fees, faster responsiveness and more flexibility to consumers. Today, Toronto-based startup Flybits is announcing $35 million in funding for a platform that it believes can offer these banks a way of continuing to capture their users’ attention and help them pivot into the next generation of services, financial or otherwise.

Today, a typical end product for a customer of Flybits’ services will use insights to upsell a customer by offering financial services; for example, a bank providing an offer of a specific kind of loan or credit card that you are more likely to take; or to offer a loyalty program or rewards for usage. But the longer-term goal, said CEO and co-founder Hossein Rahnama, is to help its customers take on a bigger role as repositories that can be used for more than just money, and used beyond the walls of the bank.

“We don’t think banks will go away, as some do, but we think that they could have a role not just as money vaults, but as data vaults: a place where you can deposit data, which you trust,” he said in an interview. Indeed, some of the funding will be used to put into action some of the AI and machine learning patents the startup has amassed, with the building of a “data” marketplace for banks, fintechs and other data providers to partner and build more services together.

The Series C comes from an interesting group of investors that includes both strategic backers using Flybits’ services, as well as backers of the more non-strategic, financial kind. Led by Point72 Ventures (hedge fund supremo Steve Cohen’s VC fund), the list also includes Mastercard, Citi Ventures and Reinventure (the fund backed by Australia’s Westpac Banking Corporation), Portag3 Ventures, TD Bank and Information Venture Partners. Valuation is not being disclosed, and prior to this the company had raised around $15 million.

Much like another marketing tech company, Near — which today announced $100 million in funding — the premise that underpins Flybits’ technology is that there is a lot of disparate data out there that, if it’s treated correctly, can uncover a lot more insights about consumer behavior, and that by and large many companies are missing this opportunity because they haven’t found the right way of merging the data to unlock insights.

While Near is applying this to location-based data and a range of different verticals, Flybits’ primary target has been banks and the data that they and other financial services providers already possess.

Many smaller startups in the world of financial services have stolen a march on bigger incumbents by building personalization into their products from the ground up. (Indeed, some like Step, aimed at teens, are so personalised that they will actually change their service mix as their customer base grows up and needs new products.) This is something that incumbents might have been more readily able to do in the old days, when people knew their bank managers and tellers and made daily trips into branches to transact. In the digital age they have fallen behind and are now catching up.

Flybits’ investors have spotted that and this in part is why they are banking on technologies like this to help bigger companies catch up, not just in financial services (although with banking alone estimated to be a €6.9 trillion industry, this is clearly a good start).

“Personalization is mission-critical for all D2C businesses in the digital age. Flybits’ integrated platform allows financial services firms to offer contextualized experiences, driving product awareness and adding significant value to the lives of their customers,” said Ramneek Gupta, managing director and co-head of Venture Investing at Citi Ventures, in a statement. “We look forward to partnering with Flybits in its next phase of growth as it continues to set the bar for hyper-personalized customer experiences.”

Indeed, it’s not just banks that are working on upselling, or that have large repositories of data that are not used as well as they could be.

“Mastercard and Flybits share a vision on using data driven insights to enrich consumers’ experiences,” said Francis Hondal, president, Loyalty & Engagement at Mastercard, in a statement. “Our ultimate goal is to develop products and services that engage consumers in a highly contextual manner. Through this collaboration with Flybits, we’ll be able to offer rich, personalized experiences for them throughout their journeys.”

Powered by WPeMatico

In the early 2000s, journalists popularized the term “PayPal mafia” to describe the PayPal founders and employees who left to start their own wildly successful tech companies, including Peter Thiel, Reid Hoffman, and Elon Musk. Drawing from that idea, this article seeks to cover the formation and flow of talent within the crypto landscape today.

I’m fascinated by the concept of tech mafias, popularized by Paypal in the early 00s.

Early signs of crypto mafias:

Coinbase

@0xProject @dydxprotocol

Ethereum/ConsenSys

MIT

IC3Others?

— Ash Egan (@AshAEgan) April 3, 2019

The crypto world is in a constant state of flux, with new startups entrants joining the industry every single day. These new startups have the potential either to be superstars within a portfolio company or to start the next Coinbase. Additionally, there are already impressive spin-outs from some of the more established crypto companies.

For ease of framing, I’ve separated these early-forming mafias into four categories: Crypto, Tech, Wall Street, and Academia. Since 2009, there have been 186 spinout companies originating from those four categories (33% from Academia, 28% from Crypto, 24% from Tech, and 15% from Wall Street).

Obvious but important disclaimer: this article does not intend to promote organized crime within crypto.

Powered by WPeMatico

Paytm, India’s largest mobile wallet app, has branched out to several businesses in recent years as threat from Google and Facebook grows. On Tuesday, it added another category to the list: credit cards.

The firm, operated by One97 Communications, today unveiled Paytm First Credit Card with lofty benefits as it races to bulk up its financial offerings. The cards, issued by Citi Bank, will be the first in the country to offer unlimited, one percent cashback on purchases, Paytm claimed in a statement. The company is hoping to rope in about 25 million credit card customers in the coming months.

The penetration of credit cards remains very low in India with under 50 million people possessing one. With people conducting most of their businesses through cash in the nation, banks have little understanding of a customer’s credit history and score. And it also doesn’t help that banks in India are still wary of issuing credit cards to those who don’t perfectly fit the traditional blue collar job.

But why is a company that made its name through a mobile payment wallet open to its customers engaging with credit card companies? Paytm itself is struggling to grow its business and retain existing customers. Some of its recent major bets haven’t exactly paid off. Its ecommerce business Paytm Mall remains tiny despite bleeding money.

Yo! The First. Paytm First. pic.twitter.com/5kAxozc2IH

— Vijay Shekhar (@vijayshekhar) May 13, 2019

But more importantly, payments itself has become a commoditized space. Users park their money in Paytm and do transactions from there. Paytm makes money from this accumulated sum. This business flourished for years, especially in the months after the Indian government invalidated much of the cash in the nation. But then the government launched its own payment infrastructure called UPI, which removes the need for a middleman.

This has made payments more convenient for users, who are increasingly jumping ship. UPI apps such as PhonePe that have emerged in the last two and a half years now see more transactions than wallet apps. To make matter worse for Paytm, Google and Facebook — two companies that have larger userbase in India — have entered the payments space. Google Pay reached 100 million installs on Google Play Store recently, and WhatsApp plans a nation-wide roll out of its payment feature in India later this year.

So Paytm is now expanding its financial offerings and credit card play fits well in it. With more than 200 million active users, Paytm rivals banks on both the number of customers and volume of transaction it processes.

“Our new offering is designed to bring utmost flexibility to our customers in their digital payment options and will help spur large-ticket cashless payments,” Vijay Shekhar Sharma, chairman and CEO of One97 Communications said in a statement.

Backed by SoftBank, Alibaba, and most recently Warren Buffett’s Berkshire Hathaway, Paytm has the capital to spur the adoption of its new credit card. As part of the package, Paytm’s credit card holders will be able to avail dining, shopping, travel and other offers that Citi Bank provides to its privilege customers. In the first four months of issuing a card, the company will offer its customers discounts worth Rs 10,000 ($142) on spending of Rs 10,000.

Paytm First Credit Card will work both in India and elsewhere and support contactless transactions. Like any other credit card, customers will be able to pay back a sum in multiple monthly instalments. Paytm First Credit Card will charge users a nominal fee of Rs 500 ($7.1) that will be waived off if their spendings through the card exceeds Rs 50,000 ($710) in a year.

If the gamble works, Paytm will be able to retain some customers and convince many to do big-ticket transactions. For Citi Bank, this partnership is just an easy ploy to acquire some customers.

In the meantime, Paytm continues to aggressively expand its financial offerings. In recent years, it has launched a digital payments bank, and has started to offer prepaid Forex cards for international purchases. It also lets customers buy gold, and employers issue food allowance wallets for their staff. Last year, the company announced Paytm Money to facilitate purchase of mutual funds.

Earlier this year, the company launched Paytm First, a subscription bundle that includes access to subscriptions from other services such as Zomato, Uber, Gaana, and Eros Now. In an interview with TechCrunch late last month, Paytm’s Sharma said payments is the moat around which you can build a number of services. “Now that’s a business model… payment itself can’t make you money.”

Powered by WPeMatico

Alchemist is the Valley’s premiere enterprise accelerator and every season they feature a group of promising startups. They are also trying something new this year: they’re putting a reserve button next to each company, allowing angels to express their interest in investing immediately. It’s a clever addition to the demo day model.

You can watch the live stream at 3pm PST here.

Videoflow – Videoflow allows broadcasters to personalize live TV. The founding team is a duo of brothers — one from the creative side of TV as a designer, the other a computer scientist. Their SaaS product delivers personalized and targeted content on top of live video streams to viewers. Completely bootstrapped to date, they’ve landed NBC, ABC, and CBS Sports as paying customers and appear to be growing fast, having booked over $300k in revenue this year.

Redbird Health Tech – Redbird is a lab-in-a-box for convenient health monitoring in emerging market pharmacies, starting with Africa. Africa has the fastest growing middle class in the world — but also the fastest growing rate of diabetes (double North America’s). Redbird supplies local pharmacies with software and rapid tests to transform them into health monitoring points – for anything from blood sugar to malaria to cholesterol. The founding team includes a Princeton Chemical Engineer, 2 Peace Corps alums, and a Pharmacist from Ghana’s top engineering school. They have 20 customers, and are growing 36% week over week.

Shuttle – Shuttle is getting a head start on the future of space travel by building a commercial spaceflight booking platform. Space tourism may be coming sooner than you think. Shuttle wants to democratize access to the heavens above. Founded by a Stanford Computer Science alum active in Stanford’s Student Space Society, Shuttle has partnerships with the leading spaceflight operators, including Virgin Galactic, Space Adventures, and Zero-G. Tickets to space today will set you back a cool $250K, but Shuttle believes that prices will drop exponentially as reusable rockets and landing pads become pervasive. They have $1.6m in reservations and growing.

Birdnest – Threading the needle between communal and private, Birdnest is the Goldilocks of office space for startups. Communal coworking spaces are accessible but have too many distractions. Traditional office spaces are private but inflexible on their terms. Birdnest brings the best of each without the drawbacks: finding, leasing, and operating a network of underutilized spaces inside of private offices. The cofounders, a duo of Duke and Kellogg MBA grads, are at $300K ARR with a fast-growing 50+ client waitlist.

Tag.bio – Tag.bio wants to make data science actionable in healthtech. The founding team is comprised of a former Ayasdi bioinformatician and a former Honda Racing engineer with a Stanford MBA. They’ve developed a next-generation data science platform that makes it easy and fast to build data apps for end users, or as they say, “WordPress for data science.” The result they claim is lightning-fast analysis apps that can be run by end users, dramatically accelerating insight discovery. They count the UCSF Medical Center and a “large Swiss pharma company” as early customers.

nCorium – They’ve built a new server architecture to handle the onslaught of AI to come with what they claim is the world’s first AI accelerator on memory to deliver 30x greater performance than the status quo. The quad founding team is intimidatingly technical — including a UCSD Professor, and former engineers from Qualcomm and Intel with 40 patents among them. They have $300K in pilots.

Spiio – Software eats landscaping with Spiio, which combines cloud-driven AI with physical sensors to monitor watering and landscaping for big companies. Their smart system knows when to water and when not to. This reduces water consumption by 50%, which means their system pays for itself in less than 30 days for big companies. They want to connect every plant to the internet, and look like they are off to a good start — $100K in orders from brand name Valley tech firms, and they are doubling monthly.

Element42 – Fraud is a major problem — For example, if you buy a Rolex on eBay, you run the risk of winding up with a counterfeit. Started by ex-VPs from Citibank, the founders are using risk models and technologies that banks use to help brands combat fraud and counterfeiting. Designed with token economics, they also incentivize customers to buy genuine products by serving exclusive content and promotions only to genuine product holders. Built on blockchain at the core, they claim to be the world’s first peer-to-peer authentication platform for physical assets. They have 45 customers across two industry verticals, 800K in ARR and are a member of World Economic Forum’s global initiatives against corruption.

My90 – Distrust between the public and the police has rarely been more strained than it is today. My90 wants to solve that by collecting data about interactions between the police and the public—think traffic stops, service calls, etc.—and turn these into actionable intelligence via an online analytics dashboard. Users text My90 anonymously about their interactions, and My90’s dashboard analyzes the results using natural language processing. Customers include major city police departments like the San Jose Police Department and the world’s largest community policing program. They have booked $150K in pilots and are expanding aggressively across the US.

Nunetz – A Stanford Computer Science grad and UCSF Neurosurgeon have come together to try to build a single unifying interface to replace the deluge of monitors and data sources in today’s clinical health environment. The goal is to prepare a daily “battle map” for physicians, nurses, and other providers, with an initial focus on the Intensive Care Unit (ICU). They have closed 3 paid pilots with hospitals through grants.

When Labs – If you hate managing people, When Labs wants to unburden you. Using an AI-powered assistant that texts with employees to negotiate assignments for hourly work, WhenLabs is trying to free customers like Hilton from spending money on managers who would normally do this manually. As the system gets smarter, they claim employees will prefer interfacing with their AI bot more than a human. AI and HR is a crowded space, but this might be the team to separate from the pack: the founding team’s previous company had a 9 figure exit to IBM.

FirstCut – FirstCut helps businesses put video content out at scale. Video dominates social media — it creates 10x more comments than text — and is emerging as a necessity for B2B media. But putting video out if you are a B2B marketer normally requires using agencies that charge hefty fees. FirstCut wants to disrupt the agencies with software and marketplaces. They use software automation and an on-demand talent marketplace to offer a fixed price product for video content. They are at $180k revenue, and most of it is moving to recurring subscriptions.

LynxCare – LynxCare claims that 90% of healthcare data goes untapped when doctors make critical decisions about your life. Further, they claim the average person’s life could be extended by 4 years if that data can be converted into insights. Their team of clinicians and data scientists aims to do just that — building a data platform that aggregates disparate data sets and drive insight for better clinical outcomes. And it looks like their platform has fans: they are active in 9 hospitals, count Pharma companies like Pfizer as Partners, and grew 4x over the past year and now are at $800K ARR.

ADIAN – Adian is a B2B SaaS product that digitizes the complex agrochemical supply chain in order to improve the sales process between manufacturers and distributors. The company claims manufacturers reduce costs by 20% and increase sales by 4% by using their online framework. $1.5 Billion and 70,000 orders have gone through the platform to date.

Hardin Scientific – Hardin is building IoT-enabled, Smart Lab Equipment. The hardware becomes a gateway to become the hub for monitoring, controlling, and sharing scientific data across teams. They’ve closed over $1.5m in revenue, and raised $15m in equity and debt financing. One of their smart devices is being used to 3D print bio-tissues and human organs in space.

ZaiNar – This team of 5 Stanford grads — 3 PhD’s and 2 MBAs — joined up with the Co-Founder of BlueKai to build the world’s best time synchronization technology. ZaiNar claims their ability to wirelessly synchronize and distribute time between networked devices is a thousand times better than existing technologies. This enables them to locate RF-emitting devices (i.e. phones, cars, drones, & RFID) at long distances with sub-meter accuracy. Beyond location, this technology has applications across data transmission, 5G communications, and energy grids. ZaiNar has raised a $1.7 million seed from AME Cloud and Softbank, and has built an extensive patent portfolio.

SMART Brain Aging – This startup claims to reduce the onset of dementia by 2.25 years with software. They are the only company approved by Medicare to get reimbursed on a preventative basis for the treatment of dementia. In conjunction with Harvard University, they have developed 20,000 exercises that are clinically proven to reduce the onset of dementia and, they claim, help build neurotransmitters. The company works with 300 patients per week ($2.2 million annual revenue) and is building to a goal of helping 22,000 people in 24 months.

Phoneic – Phoneic believes the data trapped in voice calls from cellphones is a gold mine waiting to be unleashed. Their app records and transcribes cell phones conversations, and the company has built an integration layer to enterprise AI and CRM systems that traditionally didn’t have access to voice data. The team is led by the co-founder of 3jam, one of the first group SMS and virtual number companies, which was acquired by Skype in 2011. He is keenly aware of the power of virality — and like Skype, the use of Phoneic spreads its adoption. The company has already raised $800,000 in seed funding.

Arkose Labs – Whether or not you think Russia interfered with the 2016 election, it’s no secret that bots are having significant impact on society. Arkose Labs wants to fight fraud, without adding friction to legit users. Most fraud prevention platforms today focus on gathering info from the user and providing a probability score that the traffic is good or bad. This leaves companies with a difficult decision where they may be blocking revenue generating users. Arkose has a different approach, and uses a bilateral approach that doesn’t force this tradeoff. They claim to be the only solution to offer a 100% SLA on fraud prevention. Big companies like Singapore Airlines and Electronic Arts are customers. USVP led a $6 million investment into the company.

Powered by WPeMatico

Backlash swelled this morning after Facebook’s aspirations in financial services were blown out of proportion by a Wall Street Journal report that neglected how the social network already works with banks. Facebook spokesperson Elisabeth Diana tells TechCrunch it’s not asking for credit card transaction data from banks and it’s not interested in building a dedicated banking feature where you could interact with your accounts. It also says its work with banks isn’t to gather data to power ad targeting, or even personalize content such as which Marketplace products you see based on what you buy elsewhere.

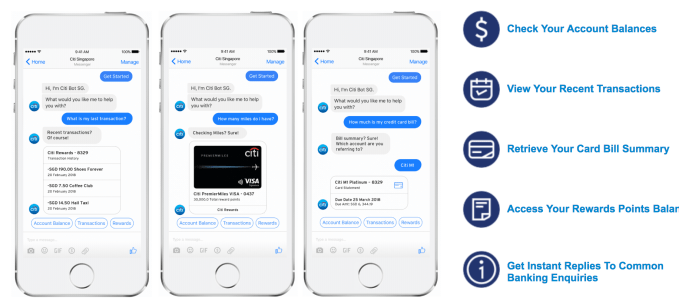

Instead, Facebook already lets Citibank customers in Singapore connect their accounts so they can ping their bank’s Messenger chatbot to check their balance, report fraud or get customer service’s help if they’re locked out of their account without having to wait on hold on the phone. That chatbot integration, which has no humans on the other end to limit privacy risks, was announced last year and launched this March. Facebook works with PayPal in more than 40 countries to let users get receipts via Messenger for their purchases.

Expansions of these partnerships to more financial services providers could boost usage of Messenger by increasing its convenience — and make it more of a centralized utility akin to China’s WeChat. But Facebook’s relationships with banks in the current form aren’t likely to produce a steep change in ad targeting power that warrants significant heightening of its earning expectations. The reality of today’s news is out of step with the 3.5 percent share price climb triggered by the WSJ’s report.

“A recent Wall Street Journal story implies incorrectly that we are actively asking financial services companies for financial transaction data – this is not true. Like many online companies with commerce businesses, we partner with banks and credit card companies to offer services like customer chat or account management. Account linking enables people to receive real-time updates in Facebook Messenger where people can keep track of their transaction data like account balances, receipts, and shipping updates,” Diana told TechCrunch. “The idea is that messaging with a bank can be better than waiting on hold over the phone – and it’s completely opt-in. We’re not using this information beyond enabling these types of experiences – not for advertising or anything else. A critical part of these partnerships is keeping people’s information safe and secure.”

Diana says banks and credit card companies have also approached it about potential partnerships, not just the other way around as the WSJ reports. She says any features that come from those talks would be opt-in, rather than happening behind users’ backs. The spokesperson stressed these integrations would only be built if they could be privacy safe. For example, signing up to use the Citibank Messenger chatbot requires two-factor authentication through your phone.

But renewed interest in Facebook’s dealings with banks comes at a time when many are pointing to its poor track record with privacy following the Cambridge Analytica scandal, where people were duped into volunteering the personal info of them and their friends. Facebook hasn’t had a big traditional data breach where data was outright stolen, as has befallen LinkedIn, eBay, Yahoo [part of TechCrunch’s parent company] and others. But users are rightfully reluctant to see Facebook ingest any more of their sensitive data for fear it could leak or be misused.

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook has recently cracked down on the use of data brokers that suck in public and purchased data sets for ad targeting. It no longer lets data brokers upload Managed Custom Audience lists of user contact info or power Partner Categories for targeting ads based on interests. It also more adamantly demands that advertisers have the consent of users whose email addresses or phone numbers they upload for Custom Audience targeting, though Facebook does little to verify that consent and advertisers could still buy data sets from brokers and upload them themselves

Facebook’s statement today shows more scruples than Google, which last year struck ad measurement data deals with data brokers that have access to 70 percent of credit and debit card transactions in the U.S. That led to a formal complaint to the FTC from the Electronic Privacy Information Center. [Correction: Google tells us the deals are for ad measurement data, not ad targeting as we originally published. It only learns the aggregate purchase value, not what the items were bought, and the data is encrypted.]

Cambridge Analytica has brought on an overdue era of scrutiny regarding privacy and how internet giants use our data. Practices that were overlooked, accepted as industry standard or seen as just the way business gets done are coming under fire. Internet users aren’t likely to escape ads, and some would rather have those they see be relevant thanks to deep targeting data. But the combination of our offline purchase behavior with our online identities seems to trigger uproar absent from sites using cookies to track our web browsing and buying.

Facebook’s probably better off backing away from anything that involves sensitive data like checking account balances until Cambridge Analytica blows over and it’s proven its newfound sense of responsibility translates into a safer social networking. But at least for now, it’s not slurping up our banking data wholesale.

Powered by WPeMatico

One of life’s puzzles that eludes me most is how a person could enjoy corporate trainings enough to spend their time designing and running them. Perhaps only with disdain for the status quo can a startup create something that people not only don’t hate, but find helpful. The idea for Butterfly originated from poor experiences the founders had when receiving leadership training. Read More

One of life’s puzzles that eludes me most is how a person could enjoy corporate trainings enough to spend their time designing and running them. Perhaps only with disdain for the status quo can a startup create something that people not only don’t hate, but find helpful. The idea for Butterfly originated from poor experiences the founders had when receiving leadership training. Read More

Powered by WPeMatico