Cisco

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

What a Friday. This afternoon (mere hours after we released our regularly scheduled episode no less!), both Pinterest and Zoom dropped their public S-1 filings. So we rolled up our proverbial sleeves and ran through the numbers. If you want to follow along, the Pinterest S-1 is here, and the Zoom document is here.

Got it? Great. Pinterest’s long-awaited IPO filing paints a picture of a company cutting its losses while expanding its revenue. That’s the correct direction for both its top and bottom lines.

As Kate points out, it’s not in the same league as Lyft when it comes to scale, but it’s still quite large.

More than big enough to go public, whether it’s big enough to meet, let alone surpass its final private valuation ($12.3 billion) isn’t clear yet. Peeking through the numbers, Pinterest has been improving margins and accelerating growth, a surprisingly winsome brace of metrics for the decacorn.

Pinterest has raised a boatload of venture capital, about $1.5 billion since it was founded in 2010. Its IPO filing lists both early and late-stage investors, like Bessemer Venture Partners, FirstMark Capital, Andreessen Horowitz, Fidelity and Valiant Capital Partners as key stakeholders. Interestingly, it doesn’t state the percent ownership of each of these entities, which isn’t something we’ve ever seen before.

Next, Zoom’s S-1 filing was more dark horse entrance than Katy Perry album drop, but the firm has a history of rapid growth (over 100 percent, yearly) and more recently, profit. Yes, the enterprise-facing video conferencing unicorn actually makes money!

In 2019, the year in which the market is bated on Uber’s debut, profit almost feels out of place. We know Zoom’s CEO Eric Yuan, which helps. As Kate explains, this isn’t his first time as a founder. Nor is it his first major success. Yuan sold his last company, WebEx, for $3.2 billion to Cisco years ago then vowed never to sell Zoom (he wasn’t thrilled with how that WebEx acquisition turned out).

Should we have been that surprised to see a VC-backed tech company post a profit — no. But that tells you a little something about this bubble we live in, doesn’t it?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Skymind, a Y Combinator-incubated AI platform that aims to make deep learning more accessible to enterprises, today announced that it has raised an $11.5 million Series A round led by TransLink Capital, with participation from ServiceNow, Sumitomo’s Presidio Ventures, UpHonest Capital and GovTech Fund. Early investors Y Combinator, Tencent, Mandra Capital, Hemi Ventures, and GMO Ventures, also joined the round/ With this, the company has now raised a total of $17.9 million in funding.

The inclusion of TransLink Capital gives a hint as to how the company is planning to use the funding. One of TransLink’s specialties is helping entrepreneurs develop customers in Asia. Skymind believes that it has a major opportunity in that market, so having TransLink lead this round makes a lot of sense. Skymind also plans to use the round to build out its team in North America and fuel customer acquisition there.

The inclusion of TransLink Capital gives a hint as to how the company is planning to use the funding. One of TransLink’s specialties is helping entrepreneurs develop customers in Asia. Skymind believes that it has a major opportunity in that market, so having TransLink lead this round makes a lot of sense. Skymind also plans to use the round to build out its team in North America and fuel customer acquisition there.

“TransLink is the perfect lead for this round, because they know how to make connections between North America and Asia,” Skymind CEO Chris Nicholson told me. “That’s where the most growth is globally, and there are a lot of potential synergies. We’re also really excited to have strategic investors like ServiceNow and Sumitomo’s Presidio Ventures backing us for the first time. We’re already collaborating with ServiceNow, and Skymind software will be part of some powerful new technologies they roll out.”

It’s no secret that enterprises know that they have to adapt AI in some form but are struggling with figuring out how to do so. Skymind’s tools, including its core SKIL framework, allow data scientists to create workflows that take them from ingesting the data to cleaning it up, training their models and putting them into production. The promise here is that Skymind’s tools eliminate the gap that often exists between the data scientists and IT.

“The two big opportunities with AI are better customer experiences and more efficiency, and both are based on making smarter decisions about data, which is what AI does,” said Nicholson. “The main types of data that matter to enterprises are text and time series data (think web logs or payments). So we see a lot of demand for natural-language processing and for predictions around streams of data, like logs.”

Current Skymind customers include the likes of ServiceNow and telco company Orange, while some of its technology partners that integrate its services into their portfolio include Cisco and SoftBank .

It’s worth noting that Skymind is also the company behind Deeplearning4j, one of the most popular open-source AI tools for Java. The company is also a major contributor to the Python-based Keras deep learning framework.

Powered by WPeMatico

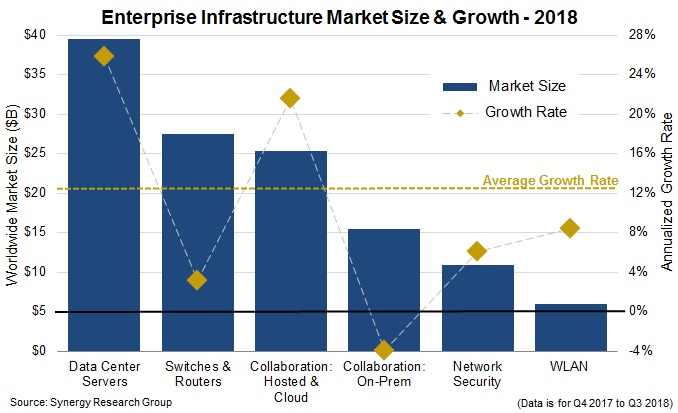

Conventional wisdom would suggest that in 2019, the public cloud dominates and enterprise data centers are becoming an anachronism of a bygone era, but new data from Synergy Research finds that the enterprise data center market had a growth spurt last year.

In fact, Synergy reported that overall spending in enterprise infrastructure, which includes elements like servers, switches and routers and network security; grew 13 percent last year and represents a $125 billion business — not too shabby for a market that is supposedly on its deathbed.

Overall these numbers showed that market is still growing, although certainly not nearly as fast the public cloud. Synergy was kind enough to provide a separate report on the cloud market, which grew 32 percent last year to $250 billion annually.

As Synergy analyst John Dinsdale, pointed out, the private data center is not the only buyer here. A good percentage of sales is likely going to the public cloud, who are building data centers at a rapid rate these days. “In terms of applications and levels of usage, I’d characterize it more like there being a ton of growth in the overall market, but cloud is sucking up most of the growth, while enterprise or on-prem is relatively flat,” Dinsdale told TechCrunch.

Perhaps the surprising data nugget in the report is that Cisco remains the dominant vendor in this market with 23 percent share over the last four quarters. This, even as it tries to pivot to being more of a software and services vendor, spending billions on companies such as AppDynamics, Jasper Technologies and Duo Security in recent years. Yet data still shows that it still dominating in the traditional hardware sector.

Cisco remains the top vendor in the category in spite of losing a couple of percentage points in marketshare over the last year, primarily due to the fact they don’t do great in the server part of the market, which happens to be the biggest overall slice. The next vendor, HPE, is far back at just 11 percent across the six segments.

While these numbers show that companies are continuing to invest in new hardware, the growth is probably not sustainable long term. At AWS Re:invent in November, AWS president Andy Jassy pointed out that a vast majority of data remains in private data centers, but that we can expect that to begin to move more briskly to the public cloud over the next five years. And web scale companies like Amazon often don’t buy hardware off the shelf, opting to develop custom tools they can understand and configure at a highly granular level.

Jassy said that outside the US, companies are one to three years behind this trend, depending on the market, so the shift is still going on, as the much bigger growth in the public cloud numbers indicates.

Powered by WPeMatico

As networks get put under increasing pressure from ever-growing amounts of data, network equipment manufacturers are facing huge challenges to increase data transmission speeds over farther distances. As a premier networking equipment company, Cisco wants to be prepared to meet that demand. Today, it opened up its checkbook and announced its intent to acquire Luxtera for $660 million.

Luxtera, which was founded in 2001 and raised more than $130 million, will give Cisco a photonic solution for that data networking problem. Rob Salvagno, head of Cisco’s M&A and venture investment team, sees a company that can help modernize Cisco’s networking equipment.

“That’s why today we announced our intent to acquire Luxtera, Inc., a privately-held semiconductor company that uses silicon photonics technology to build integrated optics capabilities for webscale and enterprise data centers, service provider market segments, and other customers. Luxtera’s technology, design and manufacturing innovation significantly improves performance and scale while lowering costs,” he wrote in a blog post announcing the acquisition.

Photonics uses light to move large amounts of data at higher speeds over increased distances via fiber optic cable. Cisco sees this as a way to future-proof customer networking requirements, while keeping them on Cisco equipment. “The combination of Cisco’s and Luxtera’s capabilities in 100GbE/400GbE optics, silicon and process technology will enable customers to build future-proof networks optimized for performance, reliability and cost,” Salvagno wrote.

While Cisco has been acquiring its share of high-profile software properties in recent years, including AppDyanmics for $3.7 billion in 2017 and Jasper Technologies for $1.4 billion in 2016, it also acquired Israeli chip designer Leaba Semiconductor for $320 million in 2016 for its advanced chip making capability.

Today’s announcement would seem to build on that earlier purchase as Cisco tries to modernize its hardware offerings to meet increasingly stringent demands inside large-scale data centers.

The acquisition is subject to the typical regulatory scrutiny, but Cisco expects it to close in its fiscal year 2019 Q3. It reported its Q1 2019 earnings in November.

Powered by WPeMatico

Instana, an application performance monitoring (APM) service with a focus on modern containerized services, today announced that it has raised a $30 million Series C funding round. The round was led by Meritech Capital, with participation from existing investor Accel. This brings Instana’s total funding to $57 million.

The company, which counts the likes of Audi, Edmunds.com, Yahoo Japan and Franklin American Mortgage as its customers, considers itself an APM 3.0 player. It argues that its solution is far lighter than those of older players like New Relic and AppDynamics (which sold to Cisco hours before it was supposed to go public). Those solutions, the company says, weren’t built for modern software organizations (though I’m sure they would dispute that).

What really makes Instana stand out is its ability to automatically discover and monitor the ever-changing infrastructure that makes up a modern application, especially when it comes to running containerized microservices. The service automatically catalogs all of the endpoints that make up a service’s infrastructure, and then monitors them. It’s also worth noting that the company says that it can offer far more granular metrics that its competitors.

Instana says that its annual sales grew 600 percent over the course of the last year, something that surely attracted this new investment.

“Monitoring containerized microservice applications has become a critical requirement for today’s digital enterprises,” said Meritech Capital’s Alex Kurland. “Instana is packed with industry veterans who understand the APM industry, as well as the paradigm shifts now occurring in agile software development. Meritech is excited to partner with Instana as they continue to disrupt one of the largest and most important markets with their automated APM experience.”

The company plans to use the new funding to fulfill the demand for its service and expand its product line.

Powered by WPeMatico

In tech circles, it would be easy to assume that the world of high-impact charitable giving is a rich man’s game where deals are inked at exclusive black tie galas over fancy hors d’oeuvre. Both Mark Zuckerberg and Marc Benioff have donated to SF hospitals that now bear their names. Gordon Moore has given away $5B – including $600M to Caltech – which was the largest donation to a university at the time. And of course, Bill Gates has already donated $27B to every cause imaginable (and co-founded The Giving Pledge, a consortium of billionaires pledging to donate most of their net worth to charity by the end of their lifetime.)

For Bill, that means he has about $90B left to give.

For the average working American, this world of concierge giving is out of reach, both in check size, and the army of consultants, lawyers and PR strategists that come with it. It seems that in order to do good, you must first do well. Very well.

Bright Funds is looking to change that. Founded in 2012, this SF-based startup is looking to democratize concierge giving to every individual so they “can give with the same effectiveness as Bill and Melinda Gates.” They are doing to philanthropy what Vanguard and Wealthfront have done for asset management for retail investors.

In particular, they are looking to unlock dollars from the underutilized corporate benefit of matching funds for donations, which according to Bright Funds is offered by over 60% of medium to large enterprises, but only used by 13% of employees at these companies. The need for such a service is clear — these programs are cumbersome, transactional, and often offline. Make a donation, submit a receipt, and wait for it to churn through the bureaucratic machine of accounting and finance before matching funds show up weeks later.

Bright Funds is looking to make your company’s matching funds benefit as accessible and important to you as your free lunches or massages. Plus, Bright Funds charges companies per seat, along with a transaction fee to cover the cost of payment processing, sparing employees any expense.

It’s a model that is working. According to Bright Fund’s CEO Ty Walrod, Bright Funds customers see on average a 40% year-over-year increase in funds donated through the platform. More importantly, Bright Funds not only transforms an employee’s relationship to personal philanthropy, but also to the company they work for.

This model of bottoms-up giving is a welcome change from the big foundation model which has recently been rocked by scandal. The Silicon Valley Community Foundation was the go-to foundation for The Who’s Who of Silicon Valley elite. It rode the latest tech boom to become the largest community foundation in eleven short years with generous stock donations from donors like Mark Zuckerberg ($1.8 billion), GoPro’s Nicholas Woodman ($500 million), and WhatsApp co-founder Jan Koum ($566 million). Today, at $13.5 billion, it surpasses the 80+ year old Ford Foundation in endowment size.

However, earlier this year, their star fundraiser Mari Ellen Loijens (credited with raising $8.3B of the $13.5B) was accused of repeatedly bullying and sexually harassing coworkers, allegations that the Foundation had “known about for years” but failed to act upon. In 2017, a similar case occurred when USC’s star fundraiser David Carrera stepped down on charges of sexual harassment after leading the university’s historic $6 billion fundraising campaign.

While large foundations and endowments do important work, their structure relies too much on whale hunting for big checks, giving an inordinate amount of power to the hands of a small group of talented fund raisers.

This stands in contrast to Bright Funds’ ethos — to lead a grassroots movement in empowering individual employees to make their dollar of giving count.

Bright Funds is the latest iteration of a lineup of workplace giving platforms. MicroEdge and Cybergrants paved the way in the 80s and 90s by digitizing the giving experience, but was mainly on-premise, and lacked a focus on user experience. Benevity and YourCause arrived in 2007 to bring workplace giving to the cloud, but they were still not turnkey solutions that could be easily implemented.

Bright Funds started as a consumer platform, and has retained that heritage in its approach to product design, aiming to reduce friction for both employee and company adoption. This is why many of their first customers were midsized tech startups with limited resources and looking for a turnkey solution, including Eventbrite, Box, Github, and Contently . They are now finding their way upmarket into larger, more established enterprises like Cisco, VMWare, Campbell’s Soup Company, and Sunpower.

Bright Funds approach to product has brought a number of innovations to this space.

The first is the concept of a cause-focused “fund.” Similar to a mutual fund or ETF, these funds are portfolios of nonprofits curated by subject-matter experts tailored to a specific cause area (e.g. conservation, education, poverty, etc.). This solves one of the chief concerns of any donor — is my dollar being put to good use towards the causes I care about? Passionate about conservation? Invest with Jim Leape from the Stanford Woods Institute for the Environment, who brings over three decades of conservation experience in choosing the six nonprofits in Bright Fund’s conservation portfolio. This same expertise is available across a number of cause areas.

Additionally, funds can also be created by companies or employees. This has proven to be an important rallying point for emergency relief during natural disasters, where employees at companies can collectively assemble a list of nonprofits to donate to. In 2017, Cisco employees donated $1.8 million (including company matching) through Bright Funds to Hurricanes Harvey, Maria, and Irma as well as the central Mexico earthquakes, the current flooding in India and many more.

The second key feature of their product is the impact timeline, a central news feed to understand where your dollars are going across all your cause areas. This transforms giving from a black box transaction to an ongoing dialogue between you and your charities.

Lastly, Bright Funds wants to take away all the administrative burden that might come with giving and volunteering — everything from tracking your volunteer opportunities and hours, to one-click tax reporting across all your charitable donations. In short, no more shoeboxes of receipts to process through in April.

Although Bright Funds is focused on transforming the individual giving experience, it’s paying customer at the end of the day is the enterprise.

And although it is philanthropic in nature, Bright Funds is not exempt from the procurement gauntlet that every enterprise software startup faces — what’s in it for the customer? What impact does workplace giving and volunteering have on culture and the bottom line?

To this end, there is evidence to show that corporate social responsibility has a an impact on recruiting the next generation of workers. A study by Horizon Media found that 81% of millennials expect their companies to be good corporate citizens. A separate 2015 study found that 62% of millennials said they’d take a pay cut to work for a company that’s socially responsible.

Box, one of Bright Fund’s early customers, has seen this impact on recruiting firsthand (disclosure: Box is one of my former employers). Like most tech companies competing for talent in the Valley, Box used to give out lucrative bonuses for candidate referrals. They recently switched to giving out $500 in Bright Funds gift credit. Instead of seeing employee referrals dip, Box saw referrals “skyrocket,” according to Box.org Executive Director Bryan Breckenridge. This program has now become “one of the most cherished cultural traditions at Box,” he said.

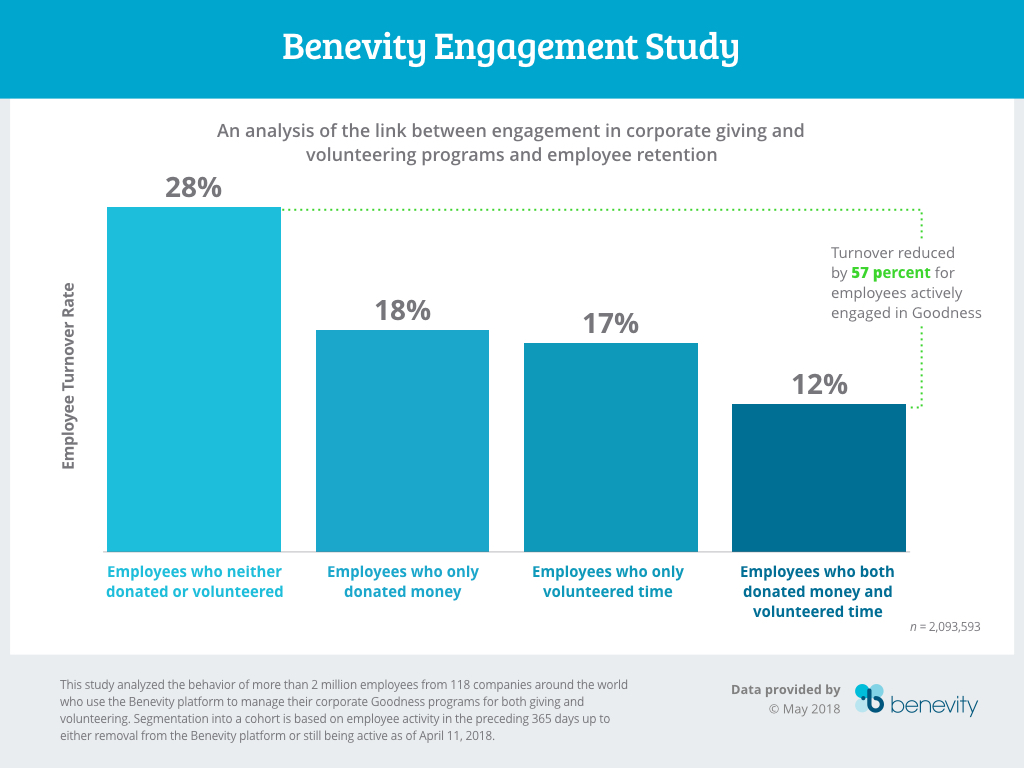

Additionally, like any corporate benefit, there should be metrics tied to employee retention. Benevity released a study of 2 million employees across 118 companies on their platform that showed a 57% reduction in turnover for employees engaged in corporate giving or volunteering efforts. VMware, one of Bright Fund’s customers, has seen an astonishing 82% of their 22,000 employees participate in their Citizen Philanthropy program of giving and volunteering, according to VMware Foundation Director Jessa Chin. Their full-time voluntary turnover rate (8%) is well below the software industry average of 13.2%.

Bright Funds still has a lot of work to do. CEO Walrod says that one of his top priorities is to expand the platform beyond US charities, finding ways to evaluate and incorporate international nonprofits.

They have also not given up their dream of becoming a truly consumer platform, perhaps one day competing in the world of donor-advised funds, which today is largely dominated by big names like Fidelity and Schwab who house over $85B of assets. In the short term, Walrod wants to make every Bright Funds account similar to a 401K account. It goes wherever you work, and is a lasting record of the causes you care about, and the time and resources you’ve invested in them.

Whether the impetus is altruism around giving or something more utilitarian like retention, companies are increasingly realizing that their employees represent a charitable force that can be harnessed for the greater good. Bright Funds has more work to do like any startup, but it is empowering the next set of donors who can give with the same effectiveness as Gates, and one day, at the same scale as him as well.

Powered by WPeMatico

When Cisco bought Ann Arbor, Michigan security company, Duo for a whopping $2.35 billion earlier this month, it showed the growing value of security and security startups in the view of traditional tech companies like Cisco.

In yesterday’s earnings report, even before the ink had dried on the Duo acquisition contract, Cisco was reporting that its security business grew 12 percent year over year to $627 million. Given those numbers, the acquisition was top of mind in CEO Chuck Robbins’ comments to analysts.

“We recently announced our intent to acquire Duo Security to extend our intent-based networking portfolio into multi- cloud environments. Duo’s SaaS delivered solution will expand our cloud security capabilities to help enable any user on any device to securely connect to any application on any network,” he told analysts.

Indeed, security is going to continue to take center stage moving forward. “Security continues to be our customers number one concern and it is a top priority for us. Our strategy is to simplify and increase security efficacy through an architectural approach with products that work together and share analytics and actionable threat intelligence,” Robbins said.

That fits neatly with the Duo acquisition, whose guiding philosophy has been to simplify security. It is perhaps best known for its two-factor authentication tool. Often companies send a text with a code number to your phone after you change a password to prove it’s you, but even that method has proven vulnerable to attack.

What Duo does is send a message through its app to your phone asking if you are trying to sign on. You can approve if it’s you or deny if it’s not, and if you can’t get the message for some reason you can call instead to get approval. It can also verify the health of the app before granting access to a user. It’s a fairly painless and secure way to implement two-factor authentication, while making sure employees keep their software up-to-date.

Duo Approve/Deny tool in action on smartphone.

While Cisco’s security revenue accounted for a fraction of the company’s overall $12.8 billion for the quarter, the company clearly sees security as an area that could continue to grow.

Cisco hasn’t been shy about using its substantial cash holdings to expand in areas like security beyond pure networking hardware to provide a more diverse recurring revenue stream. The company currently has over $54 billion in cash on hand, according to Y Charts.

Cisco spent a fair amount money on Duo, which according to reports has $100 million in annual recurring revenue, a number that is expected to continue to grow substantially. It had raised over $121 million in venture investment since inception. In its last funding round in September 2017, the company raised $70 million on a valuation of $1.19 billion.

The acquisition price ended up more than doubling that valuation. That could be because it’s a security company with recurring revenue, and Cisco clearly wanted it badly as another piece in its security solutions portfolio, one it hopes can help keep pushing that security revenue needle ever higher.

Powered by WPeMatico

Cisco today announced its intention to buy Ann Arbor, MI-based security firm, Duo Security. Under the terms of the agreement, Cisco is paying $2.35 billion in cash and assumed equity awards for Duo.

Duo Security was founded in 2010 by Dug Song and Jonathan Oberheide and went on to raise $121.M through several rounds of funding. The company has 700 employees with offices throughout the United States and in London, though the company has remained headquartered in Ann Arbor.

Co-founder and CEO Dug Song will continue leading Duo as its General Manager and will join Cisco’s Networking and Security business led by EVP and GM David Goeckeler. Cisco in a statement said they value Michigan’s “resources, rich talent pool, and infrastructure,” and remain committed to Duo’s investment and presence in the Great Lakes State.

The acquisition feels like a good fit for Cisco. Duo’s security apparatus lets employees use their own device for adaptive authentication. Instead of issuing key fobs with security codes, Duo’s solution works securely with any device. And within Cisco’s environment, the technology should feel like a natural fit for CTOs looking for secure two-factor authentication.

“Our partnership is the product of the rapid evolution of the IT landscape alongside a modernizing workforce, which has completely changed how organizations must think about security,” said Dug Song, Duo Security’s co-founder and chief executive officer. “Cisco created the modern IT infrastructure, and together we will rapidly accelerate our mission of securing access for all users, with any device, connecting to any application, on any network. By joining forces with the world’s largest networking and enterprise security company, we have a unique opportunity to drive change at a massive scale, and reshape the industry.”

Over the last few years, Cisco has made several key acquisitions: OpenDNS, Sourcefire, Cloudlock, and now Duo. This latest deal is expected to close in the first quarter of Cisco’s fiscal year 2019.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

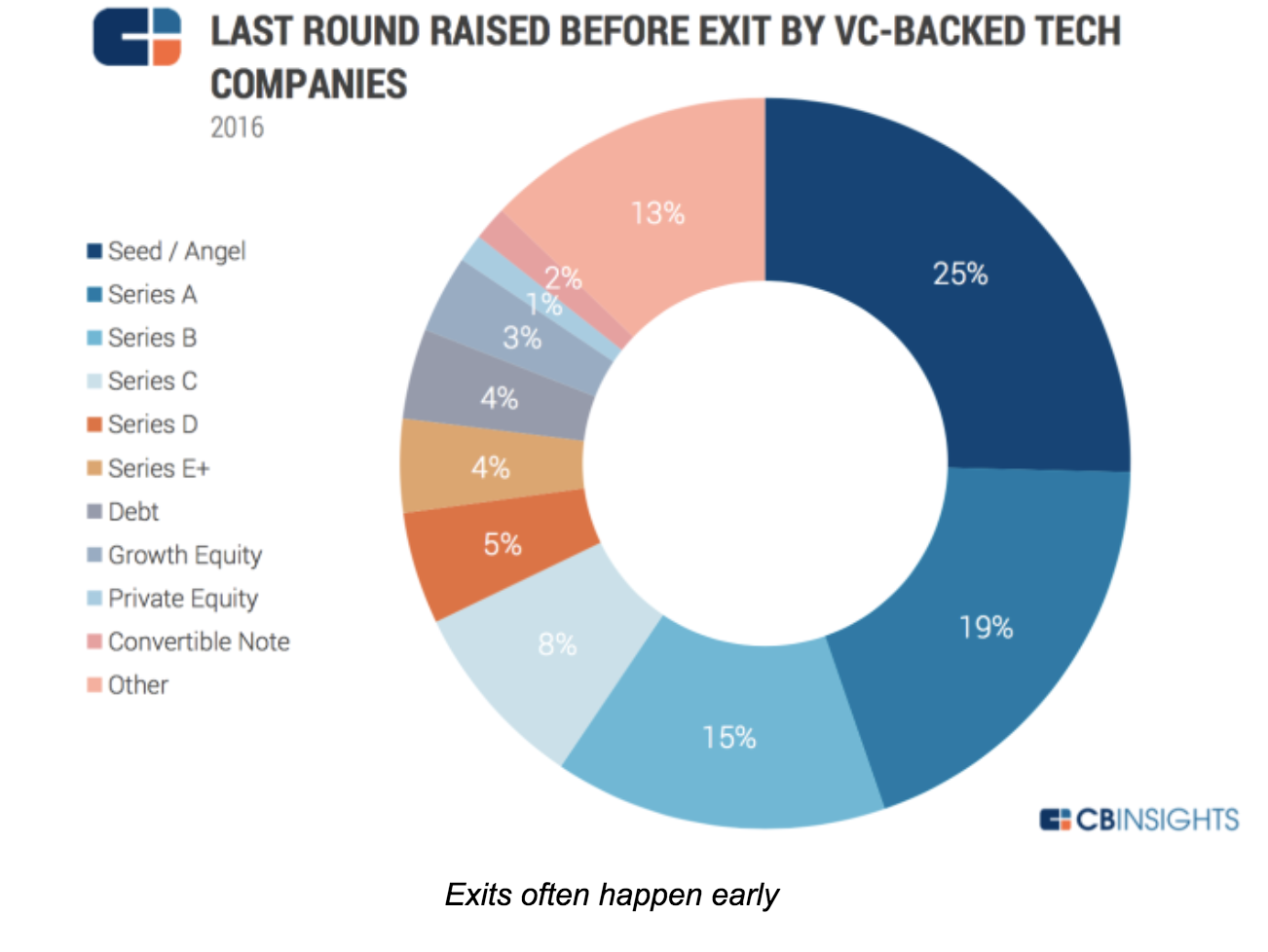

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

Customer experience management is about getting to know your customer’s preferences in an online context, but pulling that information into the real world often proves a major challenge for organizations. This results in a huge disconnect when a customer walks into a physical store. This morning, Cisco announced it has bought July Systems, a company that purports to solve that problem.

The companies did not share the acquisition price.

July Systems connects to a building’s WiFi system to understand the customer who just walked in the door, how many times they have shopped at this retailer, their loyalty point score and so forth. This gives the vendor the same kind of understanding about that customer offline as they are used to getting online.

It’s an interesting acquisition for Cisco, taking advantage of some of its strengths as a networking company, given the WiFi component, but also moving in the direction of providing more specific customer experience services.

“Enterprises have an opportunity to take advantage of their in-building Wi-Fi for a broad range of indoor location services. In addition to providing seamless connectivity, Wi-Fi can help enterprises glean deep visitor behavior insights, associate these learnings with their enterprise systems, and drive better customer and employee experiences,” Cisco’s Rob Salvagno wrote in a blog post announcing the acquisition.

As is often the case with these kinds of purchases, the two companies are not strangers. In fact, July Systems lists Cisco as a partner prominently on the company website (along with AWS). Customers include an interesting variety from Intercontinental Hotels Group to the New York Yankees baseball team.

Ray Wang, founder and principal analyst at Constellation Research says the acquisition is also about taking advantage of 5G. “July Systems gives Cisco the ability to expand its localization and customer experience management (CXM) capabilities pre-5g and post-5g. The WiFi analytics improve CXM, but more importantly Cisco also gains a robust developer community,” Wang told TechCrunch.

According to reports, the company had over $67 billion in cash as of February. That leaves plenty of money to make investments like this one and the company hasn’t been shy about using their cash horde to buy companies as they try to transform from a pure hardware company to one built on services

In fact, they have made 211 acquisitions over the years, according to data on Crunchbase. In recent years they have made some eye-popping ones like plucking AppDynamics for $3.7 billion just before it was going to IPO in 2017 or grabbing Jasper for $1.4 billion in 2016, but the company has also made a host of smaller ones like today’s announcement.

July Systems was founded back in 2001 and raised almost $60 million from a variety of investors including Sequoia Capital, Intel Capital, CRV and Motorola Solutions. Salvagno indicated the July Systems group will become incorporated into Cisco’s enterprise networking group. The deal is expected to be finalized in the first quarter of fiscal 2019.

Powered by WPeMatico