China

Auto Added by WPeMatico

Auto Added by WPeMatico

Photographer: Daro Sulakauri/Bloomberg

According to a new study conducted by the Center for American Entrepreneurship and NYU’s Shack Institute of Real Estate, the US may be losing its competitive advantage as the dominant nucleus of the startup and venture capital universe.

The analysis, led by senior Brookings Institution fellow Ian Hathaway and “Rise of the Creative Class” author Richard Florida, examines the flow of venture capital over 100,000 deals from 2005 to 2017 and details how the historically US-centric practice of venture capital has become a global phenomenon.

While the US still appears to produce the largest amount of venture activity in the world, America’s share of the global pie is falling dramatically and doing so quickly.

In the mid-90s, the US accounted for more than 95% of global venture capital investment. By 2012, this number had fallen to 70%. At the end of 2017, the US share of total venture investment had fallen to just 50%.

Over the last decade, non-US countries have propelled growth in the global startup and venture economy, which has swelled from $50 billion to over $170 billion in size. In particular, China, India and the UK now account for a third of global venture deal count and dollars – 2-3x the share held ten years ago. And with VC dollars increasingly circulating into modernizing Asia-Pac and European cities, the researchers found that the erosion in the US share of venture capital is trending in the wrong direction.

We’ve spent the summer discussing the notion of Silicon Valley reaching its parabolic peak – Observing the “rise of the rest” across smaller American tech hubs. In reality, the data reveals a “rise in the rest of the world”, with startup ecosystems outside the US growing at a faster pace than most US hubs.

The Bay Area remains the world’s preeminent beneficiary of VC investment, and New York, Los Angeles, and Boston all find themselves in the top ten cities contributing to global venture growth. However, only six of the top 20 cities are located in the US, while 14 are in Asia or Europe. At the individual level, only two American cities crack the top 20 fastest growing startup hubs.

Still, the authors found the bulk of VC activity remains highly concentrated in a small number of incumbent startup cities. More than 50% of all global venture capital deployed can be attributed to only six cities and half of the growth in VC activity over the last five years can be attributed to just four cities. Despite the growing number of ecosystems playing a role in venture decisions, the dominant incumbent startup hubs hold a firm grip on the majority of capital deployed.

Unsurprisingly, the largest contributor to the globalization of venture capital and the slimming share of the US is the rapid escalation of China’s startup ecosystem.

In the last three years, China has captured nearly a fourth of total VC investment. Since 2010, Beijing contributed more to VC deployment growth than any other city, while three other Chinese cities (Shanghai, Hangzhou, Shenzhen) fell in the top 15.

A major part of China’s ascension can be tied to the idiosyncratic rise of late-stage “mega deals”, which the study defines as $500 million or more in size. Once an extremely rare occurrence, mega deals now make up a significant portion of all venture dollars deployed. From 2005-2007, only two mega deals took place. From 2010-2012, eight of such deals took place. From 2015-2017, there were 80 global mega deals, representing a fifth of the total venture capital activity. Chinese cities accounted for half of all mega deal investment over the same period.

It’s not all bad for the US, with the study highlighting continued ecosystem growth in established US hubs and leading roles for non-valley markets in NY, LA, and Boston.

And the globalization of the startup and venture economy is by no means a “bad thing”. In fact, access to capital, the spread of entrepreneurial spirit, and stronger global economic development and prosperity is almost unquestionably a “good thing.”

However, the US’ share of venture-backed startups is falling, and the US losing its competitive advantage in the startup and venture capital market could have major implications for its future as a global economic leader. Five of the six largest US companies were previously venture-backed startups and now provide a combined value of around $4 trillion.

The intense competition for talent marks another major challenge for the US who has historically been a huge beneficiary of foreign-born entrepreneurs. With the rise of local ecosystems across the globe, entrepreneurs no longer have to flock to the US to build their companies or have access to venture capital. The problem attracting entrepreneurs is compounded by notoriously unfriendly US visa policies – not to mention recent harsh rhetoric and tension over immigration that make the US a less attractive destination for skilled immigrants.

At a recent speaking event, Florida stated he believed the US’ fading competitive advantage was a greater threat to American economic power than previous collapses seen in the steel and auto industries. A sentiment echoed by Techstars co-founder Brad Feld, who in the report’s forward states, “government leaders should read this report with alarm.”

It remains to be seen whether the train has left the station or if the US can hold on to its position as the world’s venture leader. What is clear is that Silicon Valley is no longer the center of the universe and the geography of the startup and venture capital world is changing.

“The Rise of the Global Startup City: The New Map of Entrepreneurship and Venture Capital” tries to illustrate these tectonic shifts and identifies tiers of global startup cities based on size, growth and balance of VC deals and investments.

Powered by WPeMatico

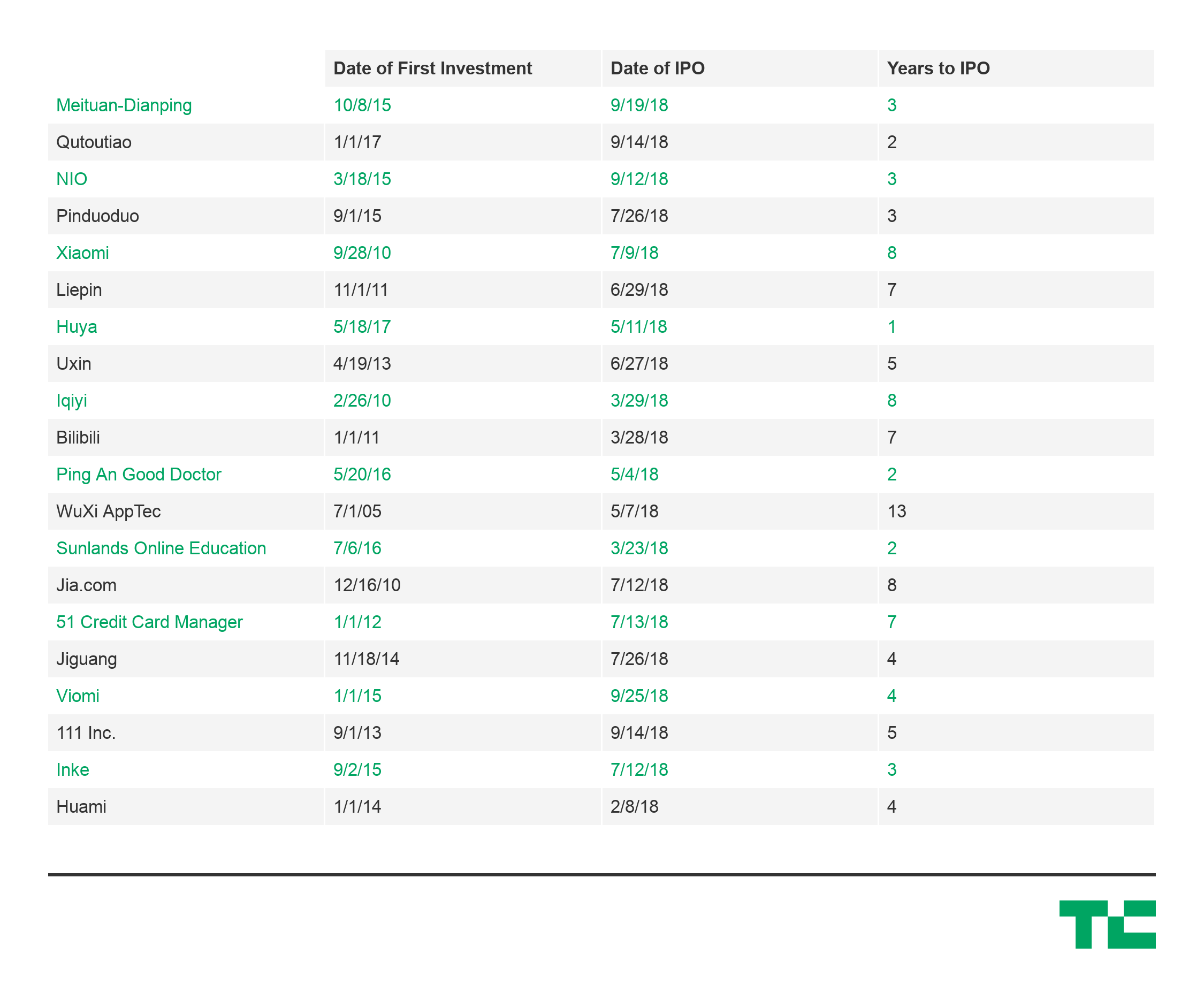

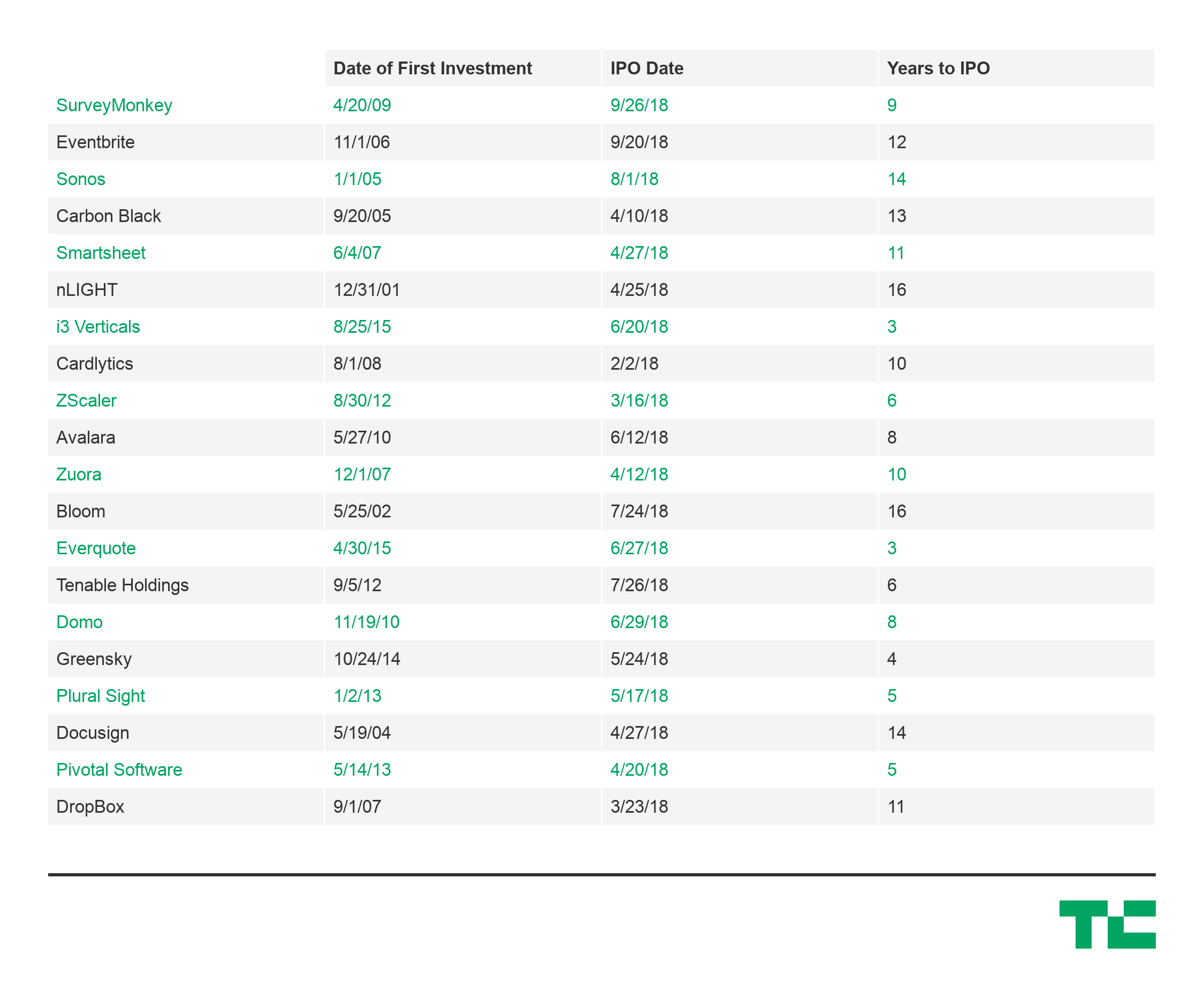

This year’s rush of IPOs from Chinese tech companies has dominated headlines, but what’s more interesting is how quickly they got there.

Traditionally, “going public” represented the gratifying culmination of sleepless nights and missed birthdays that went into building a company. The peak of a lengthy climb, where founders and VCs would finally see the fruits of their labor.

However, Chinese companies appear to be reaching that peak much quicker than their American peers, heading to the public markets only a few years after initial venture investments, and often with little operating history.

Analyzing twenty of the most high profile Chinese tech IPOs this year, the average time from first venture investment to IPO was only around three to five years. Take e-commerce platform Pinduoduo, which pulled in $1.6 billion less than three years after its Series A. Or the recent IPO of EV-manufacturer NIO, which raised a billion dollars just three-and-a-half years after its Series A and having just delivered its first car in June.

China IPO data for 2018 compiled from NASDAQ, Pitchbook, and Crunchbase

That’s less than half the average 10-year timeline for venture-backed US tech companies that went public in 2018, including Dropbox, Eventbrite, and DocuSign, which all IPO’d more than a decade after their initial investments.

Differences in market maturity, government involvement, and support from large tech incumbents all undoubtedly play a factor, but the speed to liquidity for the Chinese companies is still astounding.

Speed to liquidity is a critical metric for the health of a startup ecosystem. It creates a positive cycle where faster liquidity can drive faster fundraising, faster reinvestment, faster startup building, and faster public liquidity again. An accelerated cycle could be especially appealing for funds with LPs that require faster returns due to cash commitments or otherwise.

It’s important to note that venture returns are a function of capital and time, so quicker exits will also drive higher returns for the same amount invested. For example, a $1 million investment with a $5 million exit after ten years would generate an Internal Rate of Return (a commonly used metric to evaluate VC performance) of 20%. If the same exit occurred after five years, the IRR would be 50%.

Liquidity is a key consideration as China’s influence on the flow of global venture capital intensifies. As China’s tech ecosystem sees more of its darlings mature and more consistently deliver smashing exits, investments in China will have to be a more serious consideration for VCs, even if only to minimize the sheer amount of time, resources, and painstaking energy needed to build a company in the U.S.

Powered by WPeMatico

Chinese electric scooter startup Niu Technologies has filed for an initial public offering on Nasdaq to raise up to $150 million. In its form, Niu said it is “the largest lithium-ion battery-powered e-scooters company in China,” according to data from China Insights Consultancy, and also a market leader in Europe based on sales volume.

Founded in 2014 and based in Beijing, Niu says it currently holds a market share of 26% in China based on sales volume. Niu’s debut will the latest in a string of recent Chinese tech IPOs, the most prominent of which include the recent Hong Kong listings of Xiaomi and Meituan.

Niu’s scooters connect with an app that give drivers maintenance and performance data and also delivers firmware updates. As of the end of June, Niu claims it had sold more than 431,500 smart electric scooters in China, Europe and other markets.

According to the CIC’s data, China is the largest market for electric two-wheeled vehicles, with retail sales expected to increase to $13 million by 2022, up from $8 billion in 2017. Niu says its growth markets also include Southeast Asia and India, where scooters are a popular form of transportation.

In its filing, Niu said its net revenue in 2017 was RMB 769.4 million ($116.2 million), an increase of 116.8% from RMB 354.8 million in 2016. Its net losses during that time decreased to RMB 184.7 million ($27.9 million) in 2017 from RMB 232.7 million in 2016. More recently, net revenue for the first six months of 2018 was RMB 557.1 million ($84.2 million), an increase of 95.4% from RMB 285.1 million the same period a year earlier. Net loss was RMB 314.9 million ($47.6 million) during that period, compared to RMB 96.6 million the year before.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

PingCAP co-founder and CEO Max Liu

PingCAP, the company behind MySQL-compatible distributed database TiDB, said today that it plans its global operations after raising a $50 million Series C. The round was led by Chinese venture capital firms Fosun and Morningside Venture Capital, with participation from returning investors including China Growth Capital, Yunqi Partners and Matrix Partners.

Based in Beijing, the company says it will also use the new capital to build more cross-cloud products. PingCAP is focusing on the North American market since it is the most mature cloud market, said Kevin Xu, the company’s general manager of U.S. strategy and operations, in an email.

Founded in 2015 by Dylan Cui, Edward Huang and Max Liu, PingCAP has raised about $72 million so far, including its $15 million Series B announced in June 2017. TiDB is an open-source hybrid transactional and analytical database targeted at companies that need to handle large volumes of data and plan to scale up quickly, but still want to be able to use the same database. Many of its users come from the financial, e-commerce, gaming and travel industries and currently include Mobike, Bank of Beijing, Hulu, Lenovo and Ele.me.

In terms of other distributed databases, TiDB is often compared to CockroachDB and FoundationDB. Xu says one of the main things that differentiatese TiDB from CockroachDB is its ability to handle hybrid transactional and analytical processing workloads at scale, in addition online transaction processing. It is also MySQL compatible, while CockroachDB is PostgreSQL compatible. He adds that FoundationDB is more comparable to TiKV, the key-value storage layer developed by PingCAP that recently became a Cloud Native Computing Foundation project, because FoundationDB is not a relational database like TiDB with a SQL interface.

In a press statement, Morningside Venture Capital managing director Richard Liu said “The database industry has always been a competitive arena, and PingCAP has secured a prominent spot in this crowded field by becoming the go-to solution for many large-scale Internet companies and financial services enterprises in China. Thus, we are glad to grow with PingCAP and continue building the TiDB ecosystem together.”

Powered by WPeMatico

Wednesday is Apple’s big product release day, where analysts expect the company to release the next edition of the iPhone. While the usual upgrades to the screen, CPU, and storage are expected as always, one major lingering question is how the company is going to handle 5G, the next-generation telecommunications standard.

The conventional wisdom among analysts is that Apple will ignore 5G in 2018 and 2019 just as it took extra time to rollout 3G and 4G chipsets in its phones. A typical example of this analysis comes from Chris Smith at BGR, who says that “We already saw what Apple did when 4G LTE came out. The company waited for carriers actually to offer decent coverage before launching the first 4G iPhone. That was the iPhone 5, by the way, which launched more than a year after the first Android-based LTE phones came out.”

I’m not nearly as convinced. There are many reasons for Apple to ignore the tech this year, which I will get to in a moment, but one major factor could drive an earlier discussion of 5G than expected: Apple’s growth markets, particularly in China.

China is becoming one of Apple’s most important markets for its smartphones, and particularly for its flagship iPhone X. Its greater China revenue in the third quarter of this year was $9.6 billion, and its operating income from the region was just shy of Europe’s. More importantly, greater China is just slightly behind the Americas as the fastest-growing region for Apple’s sales.

That makes 5G a particularly challenging issue for the company. China has made 5G leadership a critical pillar of its industrial strategy, and many analysts believe the country will set the pace for 5G rollouts globally. Furthermore, Chinese consumers are deeply interested in buying premium products and experiences, and adoption for 5G is expected to be strong and rapid.

With the technical specifications around the 5G standard complete, companies are racing to build the chipsets and deploy the infrastructure necessary to enable this new standard in smartphones and other devices. Early networks are expected to be deployed in 2019, and chipset maker Qualcomm has publicly unveiled more than a dozen handset manufacturers who are partnering with it on 5G. For instance, Vivo, a Chinese smartphone manufacturer, announced today that it was developing its first “pre-commercial 5G smartphones” for launch next year.

The speed and timing of the 5G rollout is awkward for Apple, which has traditionally timed its iPhone events for September. It almost certainly will make no announcements this week, but its next iPhone launch would likely be September 2019 — giving Chinese handset manufacturers with early 5G devices nearly exclusive access to the local market for the first three quarters of next year.

Apple would find itself falling behind its competitors in a fast-moving and critical growth market. While the company has built a brand in the country with devoted fans, its place in the market is not nearly as secure as in the U.S., particularly as the trade war between the two nations reaches a fevered pitch.

There’s no doubt that the challenges for Apple to include the technology are immense. First is the patent licensing cost, which Jeremy Horwitz at VentureBeat put at roughly $21 per device, up from around $9 for 4G. Second, the leading American company in 5G is believed to be Qualcomm, which Apple has been fighting in a long-running patent war, to the point that the company has been actively trying to remove Qualcomm equipment from its phones. Apple’s name was notably absent from Qualcomm’s 5G partner list.

While some early chip designs are available, they are hardly ready for primetime, and certainly not for a flagship phone like the iPhone X. Nor do I expect that Apple will imply on Wednesday that the company will support 5G in future releases and dampen enthusiasm for its newly-released devices. No one wants to be told that next year’s devices are going to be better than one released just minutes ago.

Instead, I expect Apple will use smoke signals to clearly demonstrate that it intends to remain at the cutting edge of 5G deployment. That could include joining certain industry trade groups, testing the technology in a more public fashion, and potentially releasing a roadmap next year, say at its Worldwide Developers Conference, which is traditionally held in June and thus earlier in the year than its September iPhone events.

What would be concerning though is if we get to the end of 2018 and into 2019 with nary a peep from the company about its plans for the technology. Given its commitment to China, as well as its leading position within the smartphone market, the company has to engage on the technologies around 5G in a public manner in order to prevent a loss in its competitive position.

Ultimately, much will depend on China Mobile and other telcos in China as well as around the world on how fast they can deploy 5G infrastructure (sadly, it looks increasingly like the U.S. faces a bumpy road in that direction). Beyond gold iPhone rumors, 5G may well be the first time that China drives the company’s product roadmaps, and it should be wary of finding itself on the defensive.

Powered by WPeMatico

Chinese Internet giant Tencent has announced it’s bringing in a new system of age checks to its video games which will be linked to a national public security database — in an effort to reliably identify minors so it can limit how long children can play its games.

The new real name-based registration system will initially be mandated for new players of its popular Honour of Kings fantasy multiplayer role-playing battle game.

It will be introduced around September 15, according to Reuters.

Tencent said the planned ID verification system — which Bloomberg couches as equivalent to a police ID check — is the first of its kind in the Chinese gaming industry, and claimed it will enable it to accurately identify underaged players and impose existing play time restrictions.

Last July Tencent said it would impose a playtime maximum of one hour per day for children up to aged 12, and a maximum of two hours a day for those between 13 and 18. But if kids can get around age checks such limits are meaningless.

“Through these measures, Tencent hopes to continue to better guide underaged players to game sensibly,” it said in a statement on its official WeChat account about the beefed up checks. It also said it plans to gradually expand the requirement to its other games.

In total Tencent’s gaming portfolio is reported to have more than 500 million players in China.

The move comes amid a crackdown by the Chinese government on video gaming over fears of health problems and addiction among children.

Late last month a statement posted on the Education Ministry website said new curbs were needed to counter worsening myopia among minors.

Ministers have long said they want to limit the amount of time kids can play games — although achieving that outcome is clearly a major challenge, given the popularity of video games and the proliferation of devices from which they can be accessed.

Tencent’s move to link age verification to a public security database does seem to represent a significant new step towards the government achieving its goal of also controlling kids’ digital activity. And investors reacted negatively to the announcement — pushing Tencent’s shares down more than 3%.

Shares in the company also dived around 3% last week when the government announced its latest gaming crackdown.

Reuters notes that shares in two other major Chinese game developers, China Youzu Interactive and Perfect World, also dropped 5.5% and 3.6%, respectively, as investors digested the regulatory risk.

Last year the Chinese government also tightened general Internet regulations, doubling down on its long standing real-name registration rules.

Powered by WPeMatico

Labor Day is a holiday that just doesn’t fit Silicon Valley. Its purported purpose is to celebrate working men and women and their — our — progress toward better working conditions and fairer workplaces. Yet, few regions in recent times have supposedly done more to “destroy” quality working conditions than the Valley, from the entire creation of the precarious 1099 economy to automation of labor itself.

My colleague John Chen offered the received wisdom on this discrepancy this weekend, arguing that Valley entrepreneurs should take the traditional message of Labor Day to heart, encouraging them to create more equitable, fair, and secure workplaces not just for their own employees, but also for all the workers that power the platforms we create and operate every day.

It’s a nice sentiment that I agree with, but I think he misses the mark.

What Silicon Valley needs — now more than ever before — is to double down on the kind of ambitious, hard-charging, change-the-world labor that created our modern knowledge economy in the first place. We can’t and shouldn’t slow down. We need more technological progress, not less. We need more automation of labor, not less. And we need as much of this innovation to happen in the United States as possible.

The tech industry may have become a dominant force by some metrics, but we are only just getting started. Entire industries like freight have little to no automation. Several billion people lack access to the internet, to say nothing of critical, basic infrastructure. Our drug pipeline is anemic, and costs for education, health care, construction, and government are continuing to skyrocket.

In short, we have barely scratched the surface of what we can achieve with software, with hardware, with better business models and better automation. These aren’t table scraps, but trillions dollar opportunities lying in wait for entrepreneurs to seize them.

And yet, we keep hearing persistent claims that overwork is a problem in the Valley. Discussions of work-life balance are practically de rigueur for startups these days, as are free meals and massages and unlimited vacation time. These demands are coming at a time when some of the most fertile opportunities for innovation in areas as diverse as robotics, space, biotech, cancer, and construction remain ripe for the taking.

It’s a hustlers world out there, and the message that those who want to shape that world should be hearing this Labor Day is simple: work harder. Hell, work today.

Certainly that’s the message ingrained in most places competing with the Valley these days. Mike Moritz wrote a column in the Financial Times earlier this year, comparing the hard-charging work ethic of Chinese tech entrepreneurs and workers with their Silicon Valley brethren. He didn’t mince words, and the piece ignited a firestorm of criticism.

But he’s right, and not just about Chinese founders. Entrepreneurs in developing and middle-income countries from India and South Korea to Brazil and Nigeria now have access to the same tools that top Valley startups use, with experience to boot. And they are hungry to transform their lot in life into something much more ambitious, much more grand.

We need to re-inject their level of urgency back into the Valley ethos and compete ferociously. We can’t rest on companies from the 1990s like Google, or the 1970s like Apple and Microsoft as the final wave of innovative companies. We need the next massive tech companies to be built, and they’re not going to be created 20-hour workweeks at a time.

Entrepreneurship is a rough and solitary life. Hustling isn’t fun, losing deals isn’t enjoyable, and working around the clock under intense pressure is not for the faint of heart. For those who want the easy road, there are many, many pathways today in the modern American economy that will guarantee it, whether that is a big tech giant, or some other Fortune 100 company.

Yet, the spirit of America is always choosing the bigger gamble, the bolder vision. And it is the people who stand up and demand that we make huge strides today — not tomorrow — that are going to own the future.

Of course, founding a company has to be a voluntary choice. No one should have to work for a pittance, or feel coerced into a high-pressure lifestyle when they aren’t ready and willing. No one should be locked into an economic system where they can’t improve their own income and status through tenacity and strategy. Our tech companies should absolutely be more diverse, and fairer to all people. Equity can and should be more widely distributed.

But when it comes to the true meaning of Labor Day in the American sense, we should celebrate the hard-working founders and entrepreneurs who are taking on the biggest challenges and focusing all of their talents on solving these critical human problems. That’s what made Silicon Valley what it is, and it’s the meaning of Labor Day that every founder and dreamer should center on.

Powered by WPeMatico

Xiaomi gave Google’s well-intentioned but somewhat-stalled Android One project a major boost last year when it unveiled its first device under the program, Mi A1. That’s now joined by not one but two sequel devices, after the Chinese phone maker unveiled the Mi A2 and Mi A2 Lite at an event in Spain today.

Xiaomi in Spain? Yes, that’s right. International growth is a major part of the Xiaomi story now that it is a listed business, and Spain is one of a handful of countries in Europe where Xiaomi is aiming to make its mark. These two new A2 handsets are an early push and they’ll be available in over 40 countries, including Spain, France, Italy and 11 other European markets.

Both phones run on Android One — so none of Xiaomi’s iOS-inspired MIUI Android fork — and charge via type-C USB. The 5.99-inch A2 is the more premium option, sporting a Snapdragon 660 processor and 4GB or 6GB RAM with 32GB, 64GB or 128GB in storage. There’s a 20-megapixel front camera and dual 20-megapixel and 16-megapixel cameras on the rear. On-device storage ranges between 32GB, 64GB and 128GB.

The Mi A2 Lite is the more budget option that’s powered by a lesser Snapdragon 625 processor with 3GB or 4GB RAM, and 32GB or 64GB storage options. It comes with a smaller 5.84-inch display, there’s a 12- and 5-megapixel camera array on the reverse and a front-facing five-megapixel camera.

The A2 is priced from €249 to €279 ($291-$327) based on specs. The A2 Lite will sell for €179 or €229 ($210 or $268), against based on RAM and storage selection.

The 40 market availability mirrors the A1 launch last year, but on this occasion, Xiaomi has been busy preparing the ground in a number of countries, particularly in Europe. It has been in Spain for the past year, but it also launched local operations in France and Italy in May and tied up with CK Hutchison to sell phones in other parts of the continent via its 3 telecom business. While it isn’t operational in the U.S., Xiaomi has expanded into Mexico and it has set up partnerships with local retailers in dozens of other countries.

Xiaomi has been successful with its move into India, where it one of the top smartphone sellers, but it has not yet replicated that elsewhere outside of China so far.

China is, as you’d expect, the primary revenue market but Xiaomi is increasingly less dependent on its homeland. For 2017 sales, China represented 72 percent, but it had been 94 percent and 87 percent, respectively, in 2015 and 2016.

Powered by WPeMatico

A number of top executives are out at ZTE as the phone maker works to fulfill the requirements of U.S.-imposed restrictions. Among the big changes up top is new CEO Xu Ziyang, who formerly headed up the company’s operations in Germany. A new CFO, CTO and head of HR have been named, as well, according to The Wall Street Journal.

The move comes a few days after company slowly began to resume some business operations on a one-month waver, following a seemingly D.O.A. seven-year export ban. The ban was announced back in April, after the company failed to appropriately punish top employees over Iran/North Korean trade violations.

Trump, however, was quick to toss the company a lifeline, citing potential job loss in China. The President’s willingness to bail out ZTE has been met with staunch criticism by many, including members of his own party. A bipartisan push in Congress to reinstitute the ban began in Congress last month. Many of the issues appear to stem from ties to the Chinese government that also put Huawei in hot water with U.S. security orgs.

For now, however, the company appears to be springing back to life, as it rushes to comply with the most recent laundry list of restrictions. The moves come in the wake of a $1 billion fine and the effective freeze on operations as the company mulled a way forward without relying on products from U.S. businesses like Google and Qualcomm.

In that time, ZTE has lost billions, and grappled with other…inconveniences. Of course, even with these changes, the company isn’t out of the woods just yet. In addition to on-going financial issues, security and other concerns could be enough to put consumers in the U.S. and other countries off the company altogether.

Powered by WPeMatico