Chime

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Danny was back, joining Natasha and Alex and Grace and Chris to chat through the week’s coming and goings. But, before we get to the official news, here’s some personal news: Danny is stepping back from his role as co-host of the Friday show! Yes, Mr. Crichton will still take part in our mid-week, deep-dive episodes, but this is the conclusion of his run as part of the news roundup. We will miss him, glad that his transitions and wit will continue to be part of the Equity universe.

Who will take the third chair? Well, stay tuned. We have some neat things planned.

Now, the rundown:

Powered by WPeMatico

In 2010, Google’s autonomous vehicle project placed self-driving cars on Bay Area streets and freeways, but practical applications were thought to be at least a decade away.

The futurists were right on schedule: In 2020, Mountain View-based Nuro was testing its second-generation R2 robotic vehicle, the first to earn a federal exemption to operate an autonomous vehicle.

But before Nuro could even consider reaching product-market fit, its founders had to overcome technological challenges, win over regulators and strike partnerships with a range of consumer-facing companies.

“Neither JZ nor I think of ourselves as classic entrepreneurs or that starting a company is something we had to do in our lives,” says co-founder Dave Ferguson. “It was much more the result of soul searching and trying to figure out what is the biggest possible impact that we could have.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Across four articles, reporter Mark Harris (The Guardian, Wired, MIT Technology Review) explores Nuro’s origins and operations, including the founders’ decision to focus on creating autonomous delivery vehicles instead of entering the passenger EV market.

I’ve lived inside the San Francisco Bay Area bubble for most of my adult life, so it’s interesting to see how people in Houston’s Woodland Heights neighborhood react to seeing Nuro’s R2 delivering pizza and prescriptions on a limited basis.

As one Redditor recently posted in r/houston: “With these self-driving cars, it’s only a matter of time before a country song is written about a guy’s truck leaving him.”

Part 1: How Google’s self-driving car project accidentally spawned its robotic delivery rival

Part 2: Why regulators love Nuro’s self-driving delivery vehicles

Part 3: How Nuro became the robotic face of Domino’s

Part 4: Here’s what the inevitable friendly neighborhood robot invasion looks like

Thanks very much for reading Extra Crunch!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Peter Dazeley (opens in a new window) / Getty Images

Why bother to beat the competition when you can buy them outright?

“It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry,” Ryan Lawler writes.

“But lately, fintech upstarts are the ones doing the acquiring.”

Image Credits: Jasmin Merdan (opens in a new window) / Getty Images

“With audiences spread out over so many platforms, reaching cult status requires some level of hacking,” Jenny Wang, a principal investor at Neo, writes in a guest column.

Covering everything from collecting user-generated content to launching splashy guerrilla marketing strategies that can take advantage of someone else’s events, she shares several growth tactics for startups, plus the metrics required to track their success.

Image Credits: ppengcreative / Getty Images

Salesforce announced last week that it plans to launch a video streaming service.

The industry analysts who enterprise reporter Ron Miller interviewed said the initiative has tremendous potential, but one noted that Salesforce will have to dig deep to compete in today’s crowded media landscape.

Salesforce hasn’t released details on the type of programming it plans to offer, but given its vast and diverse customer base, its options are many. Said Brent Leary of CRM Essentials:

“A customer could sponsor a show, advertise a show or possibly collaborate on a show. And have leads generated from the show [which could be] directly tied to the activity from those options and track ROI. And it’s all done on one platform. And the content lives on with ads living on with them.”

Image Credits: Ann Schwede (opens in a new window) / Getty Images

Karl Laughton, president and COO of Insightly, offers best practices for companies looking to make the move to a remote model.

“Employers are at a crucial crossroads when it comes to deciding where and how to let employers do their jobs,” he writes in a guest column. “There are those who will adopt the work-from-anywhere model and those who resist it.

“Those who resist it will likely struggle to keep employees.”

Image Credits: Getty Images under a Olivier Le Moal (opens in a new window) license.

YL Ventures’ Yoav Leitersdorf and Michael Cortez lay out a roadmap for founders of early-stage cybersecurity companies that are heading toward unicorn status.

“The early days of any young startup decide how successful it can be, which is why we’ve developed a focused, value-add program to support cybersecurity founders during this most critical stage and maximize their potential in building market-leading companies,” they write in a guest column.

“It’s never too early to think big, and, with the right support, launch the next industry titan.”

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm considers last week’s funding news from Carta, Chime and Discord and noodles on what the recent rounds mean for startups.

“Understanding why investors are so willing to buy minute stakes in dozens of private companies worth billions of dollars is key to grokking the crush of investment we see among younger technology startups.”

Powered by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

Chime can apparently call itself the “fastest-growing fintech in the U.S.,” but it has agreed to stop referring to itself as a “bank,” per a new report out of American Banker.

Evidently, the eight-year-old, San Francisco-based outfit was the target of an investigation by the California Department of Financial Protection and Innovation after Chime used “chimebank” in its website address, as well as used “bank” and “banking” elsewhere in its advertisements, according to the agency in a settlement agreement.

As noted by AB, Chime made the decision to settle ahead of a deadline imposed by the regulatory body.

The development shouldn’t surprise anyone familiar with banking laws. No outfit can represent itself as a bank or credit union unless it’s licensed to engage in the business of banking. The commission that pushed back on the startup issues such licenses and regulates state-chartered banks in the state of California through the Department of Financial Protection and Innovation and said in the settlement that “at all relevant times herein, Chime was not licensed to operate as a bank in California or in any other jurisdiction, nor was it exempt from such licensure.”

Chime has at times attempted to draw a distinction between itself and a bank. When the company raised its most recent round of funding — a $485 million Series F round last September that valued the business at $14.5 billion — CEO Chris Britt told CNBC: “We’re more like a consumer software company than a bank . . . It’s more a transaction-based, processing-based business model that is highly predictable, highly recurring and highly profitable.”

Still, Chime, like many newer fintech companies, has seemingly embraced the term “neobank” and “challenger bank,” and perhaps it’s no wonder. It’s certainly easier to convey to consumers what it is selling, which is banking services that include — in this case — debit cards, spending accounts and savings accounts, all offered through users’ mobile phones.

Given the settlement, expect to see more startups like Chime make clearer that in most cases, they do not have a bank charter and instead are being provided services by banks that do. In Chime’s case, for example, it now makes more plain on its website that it is a “financial technology company” and “not a bank” and that its services are being provided by the The Bancorp Bank and Stride Bank, which are both FDIC members.

Powered by WPeMatico

With nearly half a million customers across Mexico and a network of 30,000 retail locations where representatives can take deposits, the challenger bank albo is already on its way to becoming a dominant player in Mexico’s emerging fintech industry.

And the company has recently raised another $45 million to consolidate its position.

“When your mission is to build the biggest bank in Mexico, you will need a ton of money,” said albo founder Angel Sahagún.

The company received its license to operate as a full depository bank in Mexico, and is slowly working toward being the premier internet-based financial services provider for Mexico’s large and growing middle class, Sahagún said.

“We are targeting a similar target market to Chime,” the albo founder and chief executive said. “We are targeting people who are underbanked and don’t have access to all the financial products in the market.”

Sahagún said the money will be used to expand into lending and insurance products the range of services albo offers. That’s a path that has already produced one multi-billion-dollar business in Nubank, Brazil’s wildly successful fintech company, which planted a flag for a new generation of Latin American startups.

While many challenger banks in the region pursued a strategy targeting upper-class and upper-middle-class consumers, Sahagún said his service had chosen a different path.

The company is trying to bring the middle and low-income Mexican consumers into the banking system by making it easy for them to move from a cash-based world to a digital one. “Where 90% of transactions are cash-based you need a value proposition that fits very well on that cash-based society,” Sahagún said.

It’s why the company set up a network of 30,000 locations, including convenience stores and drug stores, so that it can accept deposits at the places where its customers frequent.

That growth, and the company’s 40% share of the digital banking market in Mexico, according to data from Apptopia cited by the company, is why investors like Valar Ventures, Greyhound Capital, Mountain Nazca and Flourish Ventures were willing to invest as part of the $45 million round.

“albo has proven its ability to drive sustainable growth and is leading the market. This is the team that is going to transform banking in the region and we are proud to be supporting them in that,” said James Fitzgerald of Valar Ventures, in a statement.

Powered by WPeMatico

Amount, a new service that helps traditional banks compete in a digital world, has raised $81 million from none other than Goldman Sachs as it looks to help legacy fintech players compete with their more nimble digital counterparts.

The company, which spun out from the startup lending company Avant in January of this year, has already inked deals with Banco Popular, HSBC, Regions Bank and TD Bank to power their digital banking services and offer products like point-of-sale lending to compete with challenger banks like Chime and lenders like Affirm or Klarna.

“Most banks are looking for resources and infrastructure to accelerate their digital strategy and meet the demands of today’s consumer,” said Jade Mandel, a vice president in Goldman Sachs’ growth equity platform, GS Growth, who will be joining the board of directors at Amount, in a statement. “Amount enables banks to navigate digital transformation through its modular and mobile-first platform for financial products. We’re excited to partner with the team as they take on this compelling market opportunity.”

Complementing those customer-facing services is a deep expertise in fraud prevention on the back-end to help banks provide more loans with less risk than competitors, according to chief executive Adam Hughes.

It’s the combination of these three services that led Goldman to take point on a new $81 million investment in the company, with participation from previous investors August Capital, Invus Opportunities and Hanaco Ventures — giving Amount a post-money valuation of $681 million and bringing the company’s total capital raised in 2020 to a whopping $140 million.

Think of Amount as a white-labeled digital banking service provider for Luddite banks that hadn’t upgraded their services to keep pace with demands of a new generation of customers or the COVID-19 era of digital-first services for everything.

Banks pay a pretty penny for access to Amount’s services. On top of a percentage for any loans that a bank processes through Amount’s services, there’s an up-front implementation fee that typically averages at $1 million.

The hefty price tag is a sign of how concerned banks are about their digital challengers. Hughes said that they’ve seen a big uptick in adoption since the launch of their buy-now-pay-later product designed to compete with the fast growing startups like Affirm and Klarna .

Indeed, by offering banks these services, Amount gives Klarna and Affirm something to worry about. That’s because banks conceivably have a lower cost of capital than the startups and can offer better rates to borrowers. They also have the balance sheet capacity to approve more loans than either of the two upstart lenders.

“Amount has the wind at its back and the industry is taking notice,” said Nigel Morris, the co-founder of Capital One and an investor in Amount through the firm QED Investors. “The latest round brings Amount’s total capital raised in 2020 to nearly $140 million, which will provide for additional investments in platform research and development while accelerating the company’s go-to-market strategy. QED is thrilled to be a part of Amount’s story and we look forward to the company’s future success as it plays a vital role in the digitization of financial services.”

FT Partners served as advisor to Amount on this transaction.

Powered by WPeMatico

With $90 million in deposits and $18.25 million in new financing, HMBradley is making moves as the Los Angeles-based entrant into the challenger bank competition.

LA is home to a growing community of financial services startups, and HMBradley is quickly taking its place among the leaders with a novel twist on the banking business.

Unlike most banking startups that woo customers with easy credit and savvy online user interfaces, HMBradley is pitching a better savings account.

The company offers up to 3% interest on its savings accounts, much higher than most banks these days, and it’s that pitch that has won over consumers and investors alike, according to the company’s co-founder and chief executive, Zach Bruhnke.

With climbing numbers on the back of limited marketing, Bruhnke said raising the company’s latest round of financing was a breeze.

“They knew after the first call that they wanted to do it,” Brunke said of the negotiations with the venture capital firm Acrew, a venture firm whose previous exposure to fintech companies included backing the challenger bank phenomenon which is Chime . “It was a very different kind of fundraise for us. Our seed round was a terrible, treacherous 16-month fundraise,” Brunke said.

For Acrew’s part, the company actually had to call Chime’s founder to ensure that the company was okay with the venture firm backing another entrant into the banking business. Once the approval was granted, Brunke said the deal was smooth sailing.

Acrew, Chime and HMBradley’s founders see enough daylight between the two business models that investing in one wouldn’t be a conflict of interest with the other. And there’s plenty of space for new entrants in the banking business, Bruhnke said. “It’s a very, very large industry as a whole,” he said.

As the company grows its deposits, Bruhnke said there will be several ways it can leverage its capital. That includes commercial lending on the back end of HMBradley’s deposits and other financial services offerings to grow its base.

For now, it’s been wooing consumers with one-click credit applications and the high interest rates it offers to its various tiers of savers.

“When customers hit that 3% tier they get really excited,” Bruhnke said. “If you’re saving money and you’re not saving to HMBradley then you’re losing money.”

The money that HMBradley raised will be used to continue rolling out its new credit product and hiring staff. It already poached the former director of engineering at Capital One, Ben Coffman, and fintech thought leader Saira Rahman, the company said.

In October, the company said, deposits doubled month-over-month and transaction volume has grown to over $110 million since it launched in April.

Since launching the company’s cash back credit card in July, HMBradley has been able to pitch customers on 3% cash back for its highest tier of savers — giving them the option to earn 3.5% on their deposits.

The deposit and lending capabilities the company offers are possible because of its partnership with the California-based Hatch Bank, the company said.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s VC-focused podcast (now on Twitter!), where we unpack the numbers behind the headlines.

This week Natasha Mascarenhas, Danny Crichton and your humble servant gathered to chat through a host of rounds and venture capital news for your enjoyment. As a programming note, I am off next week effectively, so look for Natasha to lead on Equity Monday and then both her and Danny to rock the Thursday show. I will miss everyone.

But onto the show itself, here’s what we got into:

Bon voyage for a week, please stay safe and don’t forget to register to vote.

Equity drops every Monday at 7:00 a.m. PDT and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

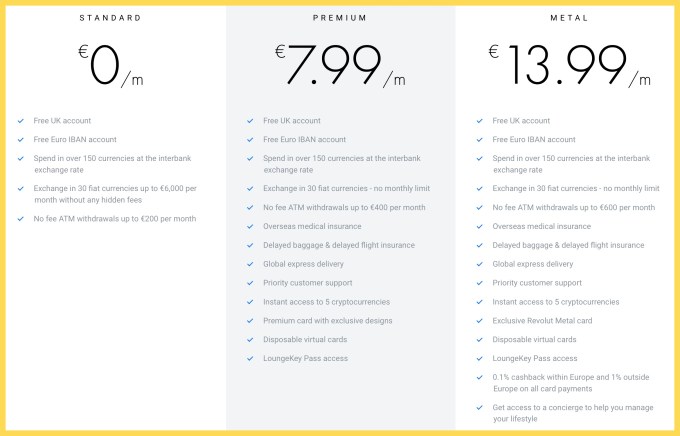

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico