chicago

Auto Added by WPeMatico

Auto Added by WPeMatico

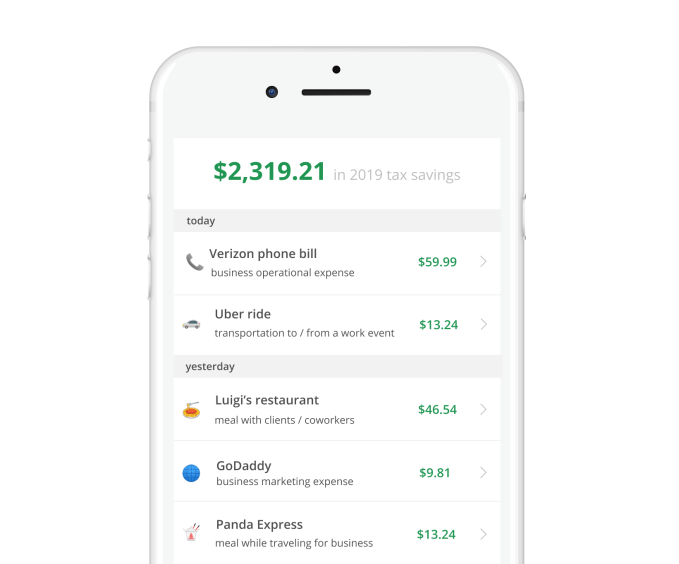

Every year around this time, Uber drivers, Wag dog walkers, Bird scooter chargers, social media influencers and other gig economy workers face the unsightly challenge of paying their taxes.

Companies like Uber and Lyft classify their drivers as independent contractors, which means you aren’t given any benefits and the company doesn’t withhold any of your taxes. This puts gig workers in a tough position come tax day, especially if they aren’t prepared to shell out big sums to the IRS.

Keeper, a startup that’s just graduated from the Y Combinator startup accelerator, is here to make taxes a lot easier for that demographic and to save them as much money as possible.

Founded by childhood buddies and former debate partners Paul Koullick and David Kang, the San Francisco-based company has raised $1.65 million on a $10 million valuation in a round led by Jake Jolis of Matrix Partners.

Keeper co-founders Paul Koullick (left) and David Kang

The pair entered YC this winter with a big idea and little to show for it. Come March, they had developed a full-fledged product and accumulated 200 paying customers. With their first round of funding, they plan to add to their small but growing team and acquire 10,000 customers in the next 18 months.

“There are some companies that are trying to go very broad and trying to cover the whole spectrum of benefits; we’re just trying to go really deep on taxes,” Kang told TechCrunch. “This is a pain point. This is where people are definitely leaving the most money on the table.”

Keeper guesses the average gig worker in the U.S. is overpaying their taxes by more than 20 percent, or about $1,550 for those making more than $25,000 per year. Why? Because these independent contractors aren’t claiming the tax write-offs available to them, like phone bills, car maintenance fees and even a Spotify subscription for drivers.

“If you’re a dog walker, there are so many things you need to be writing off, like your poop bags, your extra leashes, your parking,” Koullick told TechCrunch. “This population needs the guidance of an accountant, but they can’t afford one and we’re trying to create this third option.”

Like a personal accountant, Keeper monitors gig workers’ expenses all year in search of possible tax deductions, saving each user $173 per month on average, it estimates. The startup uses Plaid to follow its customers’ transaction history, and once per day sends a text message asking if there are any tax write-offs to note. Over time, it gets smarter and smarter, keeping the SMS questions to a minimum.

Keeper doesn’t fully file taxes for 1099 workers yet, but will begin offering a quarterly tax filing service in June. Next year, it plans to offer a full-year tax-filing service.

Koullick, Keeper’s chief executive officer, worked in product at Square before joining another startup, called Stride, where he built and scaled Stride Tax, a mileage and expense-tracking app. Kang, for his part, has spent most of his post-graduate career at a trading firm in Chicago, focused on quantitative modeling. The two toyed with a few startup ideas before landing on Keeper’s tax business.

“We wanted to build something that actually mattered to real people,” Koullick explained. “And we wanted to do it in the financial space where we were happy to wade through ugly details and systems on their behalf.”

Keeper isn’t the only recent YC alum focused on the growing gig economy. Another, Catch, sells health insurance, retirement savings plans and tax-withholding services directly to freelancers, contractors or anyone uncovered. Given the rapid rise of Uber and other gig platforms, it’s no wonder YC startups are tapping into the various business opportunities available there.

“We’re willing to tackle some of these topics that are kind of boring and mundane and really intensive,” Kang added. “Like the average person doesn’t want to think about taxes or filling out forms. We saw that as an opportunity for us to step in and be like, hey, we’ll take it.”

Powered by WPeMatico

MaaS Global, the company behind the all-in-one mobility app Whim, which offers a subscription service for public transportation, ridesharing, bike rentals, scooter rentals, taxis or car rentals, will be making its U.S. debut later this year.

The company will choose its American launch city from Austin, Boston, Chicago, Dallas and Miami, according to Sampo Hietanen, the company’s chief executive.

The Whim app is currently available in Antwerp, Birmingham, U.K., Helsinki and Vienna, according to Hietanen, and offers a range of subscription options. The top of the line version is a €500 per month all-inclusive package giving users unlimited access to ride hailing, bike and car rentals and public transportation.

“Cars take 70 percent of the market and it’s used 4 percent of the time so you’re paying for the optional capacity,” says Hietanen. Using Whim, which, at the high end costs about as much as a car in Europe, users can get all of the optionality without paying for the unused capacity. It should ideally reduce transportation costs and cut down on emissions, if Hietanen’s claims are accurate.

The Helsinki-based company uses APIs to connect with the back end of a number of service providers. For car rentals, it’s working with businesses like Hertz, Enterprise and EuropeCar; for ridesharing, the company has linked with Gett and local European taxi companies, according to Hietanen.

Users have already booked 3 million trips through the company’s app since its launch and the company is continuing to expand not just in North America, but in Asia as well. There are plans in the works for the company to launch operations in Singapore.

Giving consumers more options for transit through a single gateway could reduce demand for vehicles, but some analysts argue that it won’t do much to alleviate congestion on roads. Consumers, they argue, will choose the convenience of rideshare over mass transit and could actually increase.

As Richard Rowson, a mobility consultant from the U.K., noted in this post:

MaaS doesn’t implicitly mean a net decrease nor increase in the number of road vehicle miles. The changes are complex, but in balance look likely to result in an increase.

Factors such as migration from private car to public transport should cause a reduction, but migration from train and bus, to private hire and smaller demand responsive buses will cause an increase. Other factors such as ‘positioning’ movements as ‘on demand’ vehicles are positioned to exploit demand also create journeys.

Smart journey planning and navigation systems should make better use of available road capacity, such as identifying alternative routes – but at the expense of migrating through traffic to local access roads.

There is the potential that having a single point of access to mobility may actually help cities push riders to favor public transportation by offering a window into the amount of time using each service would take and showing users the fastest route.

Last August the company said it had raised a €9 million round from undisclosed investors. It had previously received capital from Toyota Financial Services and its insurance partner Aioi Nissay Dowa Insurance.

Powered by WPeMatico

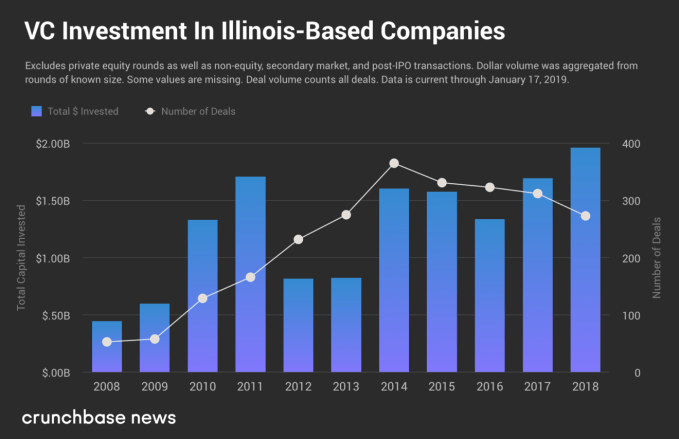

Illinois’s startup market in 2018 was very strong, and it’s not slowing down as we settle into 2019. There’s already almost $100 million in new VC funding announced, so let’s take a quick look at the state of venture in the Land of Lincoln (with a specific focus on Chicago).

In the chart below, we’ve plotted venture capital deal and dollar volume for Illinois as a whole. Reported funding data in Crunchbase shows a general upward trend in dollar volume, culminating in nearly $2 billion worth of VC deals in 2018; however, deal volume has declined since peaking in 2014.1

Chicago accounts for 97 percent of the dollar volume and 90.7 percent of total deal volume in the state. We included the rest of Illinois to avoid adjudicating which towns should be included in the greater Chicago area.

In addition to all the investment in 2018, a number of venture-backed companies from Chicago exited last year. Here’s a selection of the bigger deals from the year:

Crain’s Chicago Business reports that 2018 was the best year for venture-backed startup acquisitions in Chicago “in recent memory.” Crunchbase News has previously shown that the Midwest (which is anchored by Chicago) may have fewer startup exits, but the exits that do happen often result in better multiples on invested capital (calculated by dividing the amount of money a company was sold for by the amount of funding it raised from investors).

2018 was a strong year for Chicago startups, and 2019 is shaping up to bring more of the same. Just a couple weeks into the new year, a number of companies have already announced big funding rounds.

Here’s a quick roundup of some of the more notable deals struck so far this year:

Besides these, a number of seed deals have been announced. These include relatively large rounds raised by 3D modeling technology company ThreeKit, upstart futures exchange Small Exchange and 24/7 telemedicine service First Stop Health.

Globally, and in North America, venture deal and dollar volume hit new records in 2018. However, it’s unclear what 2019 will bring. What’s true at a macro level is also true at the metro level. Don’t discount the City of the Big Shoulders, though.

Powered by WPeMatico

London’s transport regulator, TfL has announced a partnership with Bosch for its forthcoming co-working space in Shoreditch.

The civic tech project is intended to run for 18 months as a pilot — though Bosch’s ‘Connectory’ co-working facility won’t open until the end of January. A company spokeswoman confirmed the partnership is nonetheless up and running now.

The aim of the collaborative project is to share data and expertise, including by tapping into London’s startup ecosystem, to land on new ideas for tackling urban mobility issues — from traffic jams to awful air quality.

Transport issues are especially pressing for the city as London’s population is forecast to reach a staggering 10.8 million by 2041 — which would mean around six million additional trips being generated per day.

Specific issues TfL is looking for help with include developing more efficient, greener and safer vehicles; reducing congestion; and encouraging more people to walk, cycle and take public transport across London, it said today.

TfL will be providing technical knowledge and “a wide range” of datasets throughout the pilot to allow participating companies to test ideas and “understand patterns in more detail than has previously been possible”, it added.

The data will be based on its existing Unified API and open data platform, which it notes is already underpinning nearly 700 apps used by approaching half (42 per cent) of Londoners.

Startups selected for the collaboration will be provided with dedicated space within Bosch’s Connectory, alongside TfL staff who will also be based there during the pilot.

Commenting in a statement, Arun Srinivasan, executive VP and head of mobility solutions at Bosch UK said: “We believe that the collaboration between Bosch and TfL will enable us to accelerate the development of technologies, products and services that have a positive impact on city life.”

Startups will be selected by Bosch, according to a TfL spokesman. We’ve asked for more details on selection criteria.

Update: A Bosch spokeswomen told us: “There will be a number of programmes running for start ups in the Connectory. These programmes will be around specific mobility challenges and many will have open calls for start ups to enter. We also welcome direct approaches by small business/start ups who want to be part of the Connectory community feel they have something to offer that will help solve London’s transport challenges. Get in touch!”

She said there is no fixed number of startup planned to be selected for the pilot, saying they will have rolling cohorts “designed around specific London mobility challenges” — launching this process in the New Year.

“This new ‘urban mobility’ lab is the first of its kind with a primary focus on urban mobility, and will provide the forum for private sector partners, academia and public sector to work together to tackle a range of problems facing Londoners in years to come,” the pair added in a press release today.

“By facilitating closer collaboration, TfL and Bosch hope to support start-ups to develop a range of smart products and help them identify ways to bring them to market more quickly through open procurement.”

The entire co-working facility is focused on urban mobility — but will also be open to other interested companies and startups to rent or bag a space (i.e. via Bosch’s scouting programs where it does take equity), not just to the startups selected for the TfL pilot.

Bosch’s network of Connectory co-innovation spaces also links out to cities internationally, including Chicago and Stuttgart, further expanding potential knowledge-sharing opportunities.

Commenting in a statement, the mayor of London, Sadiq Khan, said: “This initiative will foster closer working between London’s tech sector and other leading tech cities. If we are to use data and smart technology to help solve the biggest problems our city faces, it’s crucial we take a more collaborative approach. I see London’s future as a global ‘test-bed city’ for civic innovation, where the best ideas are developed, amplified and scaled.”

Depending on the outcome of the pilot, TfL said the Greater London Authority may seek similar collaborative approaches to support other aspects of its work — including housing, environment and policing, aligning with the mayor of London’s strategic priorities.

“I’ve been clear I want London to become the world’s smartest city and this is a further step towards realising that ambition,” Khan added.

This report was updated with additional detail about startup selection; and to correct that the lab will focus exclusively on urban mobility — but is also open to interested companies to rent space, as well as to startups Bosch selects to take a stake in

Powered by WPeMatico

The music business is littered with stories about songwriters or studio contributors and session musicians who never get the credit — or money — they’re often due for their work on hit songs.

And for every storied session musician in “The Wrecking Crew” there are perhaps hundreds of other contributors who aren’t getting their just desserts.

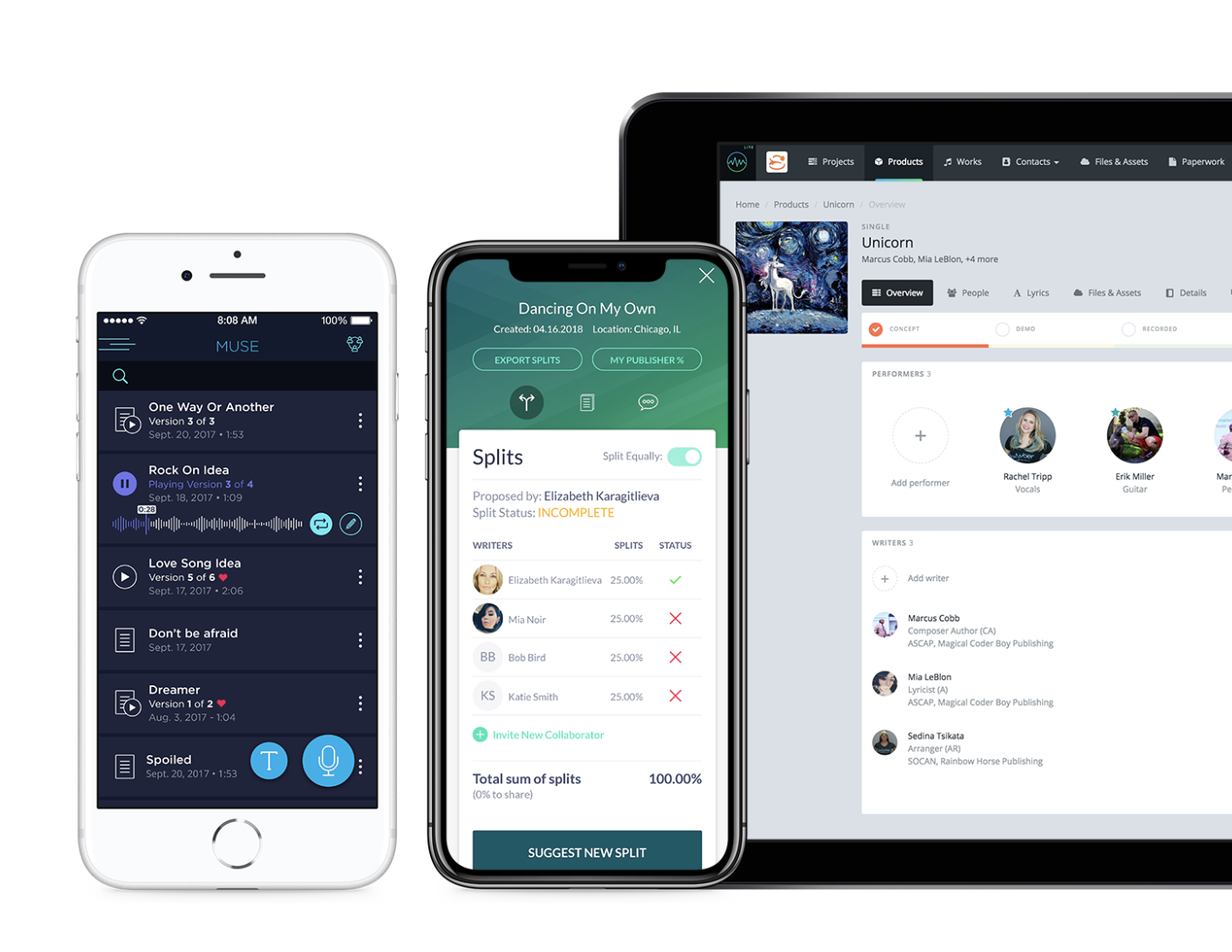

That’s where Jammber comes in. The five-year-old company co-founded by serial entrepreneur Marcus Cobb has developed a suite of tools to manage everything from songwriting credits and rights management to ticketing and touring all from a group of apps on a mobile phone. And has just raised $2.4 million in funding to take those tools to a broader market.

Jammber “Muse” gives collaborators a single platform to exchange lyrics and song ideas, while the company’s “Splits” app tracks ownership and credits of any eventual product from a collaboration. The company’s nStudio tracks songwriting credits to assist with chart and Grammy submission — through a partnership with Nielsen Music — and its “PinPoint” helps organize touring. The recording applications even have a presence feature so session musicians, songwriters and artists can actually be tagged in the studio while they’re working.

“I think we need to get attribution and monetization closer to the creators,” Cobb has said. “Why aren’t we doing that? The industry is growing and thriving. Are we making sure that performers and creators of all different tiers are being equally compensated?”

The answer, sadly, for many in the music industry is no. In fact, while Cobb had originally set out to make a networking tool for creatives with Jammber he wound up shifting the service to the management toolkit after visiting the offices of a music label.

Jammber chief executive Marcus Cobb

“I saw stacks and stacks of payroll checks that were returned to sender,” Cobb, told Crain’s Chicago Business. “These checks were taking three months to two years to print, and they were wrong addresses, or there were stage names instead of legal names.”

That experience convinced Cobb of the demand, but it was Nashville that gave the serial entrepreneur the crucible within which to develop the full suite of tools that now make up Jammber’s soup-to-nuts platform.

Cobb likes to say that Jammber was conceived in Chicago (where the company spun up from the city’s massively influential 1871 entrepreneurship center) and born in Nashville — the home of the multi-billion-dollar American country music industry. All of the tools in Jammber, Cobb says, were created with input from a local musician, producer, artist and repertoire person or a label executive.

In 2015, the company came down to Nashville as part of the first batch of companies in Project Music, a joint venture between the Country Music Association and the Nashville Entrepreneur Center meant to encourage the development of technology for the music industry.

For the 41-year-old Cobb, programming and entrepreneurship has literally been a life saver. Growing up in Texas and Nevada with an abusive, drug-addicted stepfather took a toll on Cobb and programming became an outlet — thanks to a particularly well-equipped computer lab at his high school. “I had moved 24 times,” Cobb said in an interview. “My stepfather was a full-blown crack addict. He would disappear with money; we got evicted a lot.”

But the experience with computers led to an early job out of high school, which launched Cobb’s tech career. He sold his first company, Eido Software in 2007 a year after launching it and has used that money to pursue other endeavors.

And while Cobb is a gifted programmer, that’s not his only interest. His next big foray into business was as the owner and lead designer of Marc Wayne Intimates, a boutique lingerie company that also provided the business-savvy Cobb with his first window into the music business — outfitting dancers in music videos for artists like Pitbull.

Cobb has invested $300,000 of his own money into Jammber and raised roughly $400,000 in early seed funding. The $2.3 million that the company raised in its most recent round came from a who’s who of music executives, including former Sony Nashville chief executive Joe Galante; Hootie and the Blowfish manager Clarence Spalding; and Kings of Leon manager Ken Levitan.

These investors know the tension at the heart of the music business better than anyone, Cobb says — which is that the creative act of making music can often be at odds with the mundanity of organizing and running an effective business to ensure that the music getting made is actually heard by an audience that then pays the musician for their work.

“The irony about making a living in a copyright industry like the music industry is you have to be very organized to make money in a timely manner or even get credit for your work,” said Cobb. “Over 40 percent of the money creators are owed is tied up by bad or wrong data because it’s very difficult to be organized while you create. These tools finally change that.”

Jammber’s services are currently in a closed, invite-only beta that will be capped at 10,000 users. There’s a basic set of services that will be available for free, with pricing for “unlimited” access to the toolkit starting at $10 per month. In addition to the applications, the company also has an online platform that integrates with the mobile suite. Pricing for that service starts at $25 per month.

“This is an ecosystem play for us. I’ve been in software for a long time and the realization for me is that it’s not just mobile-first or cloud-first anymore, it’s simplicity-first. Independent artists and record labels generated $5.2 billion in revenues last year and the sector continues to grow — all while largely using paper and spreadsheets for their back office tools,” said Cobb. “This is a massive, underserved market and we believe we’ve figured out how to provide the value they’ve been waiting for.”

Powered by WPeMatico

A Cleveland.com article detailed the lengths the small midwestern city would go to lure Amazon’s in 50,000-person HQ2. In a document obtained by reporter Mark Naymik, we learn that Cleveland was ready to give over $120 million in free services to Amazon including considerably reduced fares on Cleveland-area trains and buses.

The document, available here, focuses on the Northeast Ohio Areawide Coordinating Agency (NOACA)’s ideas regarding the key component in many of Amazon’s decisions – transportation.

Ohio has a budding but often tendentious connection to public transport. Cities like Columbus have no light rail while Cincinnati just installed a rudimentary system. Cleveland, for its part, has a solid if underused system already in place.

That the city would offer discounts is not surprising. Cities were falling over themselves to gain what many would consider – including Amazon itself – a costly incursion on the city chosen. However, given the perceived importance of having Amazon land in a small city – including growth of the startup and tech ecosystems – you can see why Cleveland would want to give away plenty of goodies.

Ultimately the American Midwest is at a crossroads. It could go either way, with small cities growing into vibrant artistic and creative hubs or those same cities falling into further decline. And the odds are stacked against them.

The biggest city, Chicago, is a transport, finance, and logistics hub and draws talent from smaller cities that orbit it. Further, “smart” cities like Pittsburgh and Ann Arbor steal the brightest students who go on to the coasts after graduation. As Richard Florida noted, the cities with a vibrant Creative Class are often the ones that succeed in this often rigged race and many cities just can’t generate any sort of creative ecosystem – cultural or otherwise – that could support a behemoth like Amazon landing in its midst.

What Cleveland did wasn’t wrong. However, it did work hard to keep the information secret, a consideration that could be dangerous. After all, as Maryland Transportation Secretary Pete K. Rahn told reporters: “Our statement for HQ2 is we’ll provide whatever is necessary to Amazon when they need it. For all practical purposes, it’s a blank check.”

Powered by WPeMatico

Some folks I met in Chicago are holding an amazing event at a great place on South Canalport Avenue. This former macaroni factory now builds startups and I’ll be helping judge their pitch-off alongside some Chicago luminaries.

You can RSVP here and sign up for a spot to pitch here. We’ll choose eight startups to pitch there are some great prizes available.

Blue Lacuna is at 2150 South Canalport Avenue in Chicago and the event is on April 19 at 6pm. Grab your tickets early for this cool meet and greet.

Powered by WPeMatico

The American Midwest has a long history of making stuff. During the 20th century, it was the manufacturing center for the nation, and indeed much of the world. It’s still where a surpassing majority of agricultural commodities are grown and processed. But is it also a major producer of technology startups? Maybe not as much as the coasts, but the Midwest’s bustling metropoli and vast expanses of rural land prove to be fertile ground for quite a bit of startup activity.

And that’s what we’re going to take a look at here. In a similar vein to our recent analysis of startup fundraising in the South, we’ll break down the region into its constituent parts, assessing deal and dollar volume trends in the Midwest’s two primary sub-regions, some of its individual states and the most active metropolitan areas in the U.S.’s midsection.

And, to be clear, this is not Crunchbase News’s first foray into the region. We’ve covered the region’s seed-stage interest in AI and hard tech, a few notable rounds and have always included the Midwest in all manner of data-spelunking expeditions. And to this, we’ll add a deep dive into the numbers.

Borders and boundaries are a deep well of disputes. To preempt debate, we use the U.S. Census Bureau’s definition of the Midwest region which, unlike its definition of the South, shouldn’t be too controversial. If you have something against Kansas or Ohio being included in this group, take it up with the Feds.

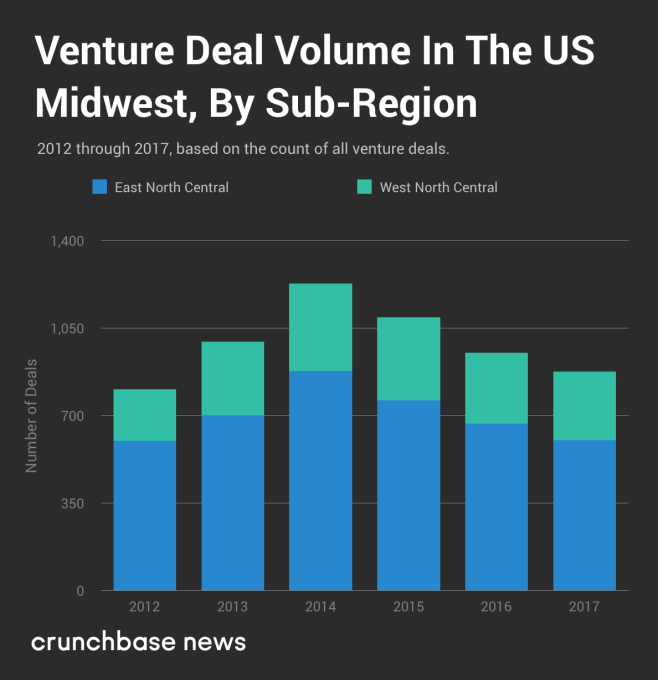

The good folks at the Census Bureau split the Midwest into two distinct — and rather unimaginatively named — sub-regions: the West North Central and East North Central states, which are separated by the Mississippi River. We’ve included the map below.

By splitting the Midwest into two distinct parts, we’ll be able to see where most of the startup and funding activity is concentrated. Spoiler alert: The farther west you go, the startup population (and the population itself) grows more scattered.

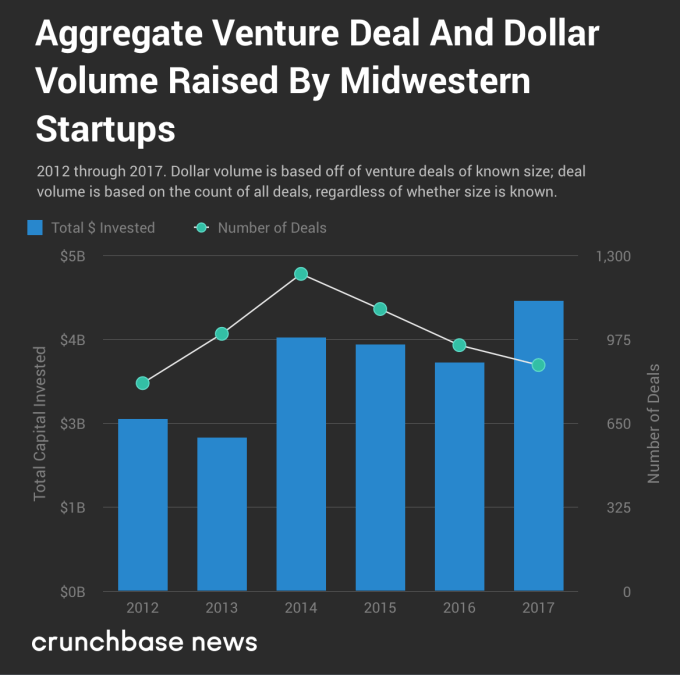

Based only on reported data in Crunchbase, the Midwest appears to be affected by the same phenomenon as the rest of the country. Crunchbase News has previously found that the number of seed and early-stage deals has gone off a cliff in the U.S., resulting in a top-heavy market featuring many large, late-stage deals. And this wouldn’t be a problem if it weren’t for a shortfall in new startups to fill the next cycle of early-stage funding. The “hollowing out” of the Midwestern venture deal pipeline becomes readily apparent when you look at funding data for the past several years, which you can find in the chart below.

To wit, deal volume is down markedly since 2014, as Crunchbase News reported in its Q4 2017 report of startup funding activity in the U.S. and Canada. But somewhat counterintuitively, the amount of money being invested into startups is on the rise in the Midwest and throughout many other parts of the country, reaching fresh multi-year highs in 2017. Almost one full quarter into 2018, the trend appears to continue unabated.

But this chart abstracts away a lot of nuance, so let’s take a closer look at the region and its states.

We’ll start first with deal volume, because that’s a fairly decent indicator of a geographic region’s level of startup activity. Below, we’ve plotted venture deal volume, divided by sub-region.

Again, based on the reported data from Crunchbase, we found that deal counts have been on a downward trend for several years. And though some of this may be attributable to reporting delays, projected deal volume data for the whole of the U.S. and Canada (fourth chart down in the Q4 quarterly report) shows a years’-long downtrend. There’s no reason to believe that startup activity in the Midwest is materially different from the rest of the U.S. and Canada.

But what about the relative “balance of power” between the two sub-regions? At least when it comes to deal volume, has one sub-region waxed while the other waned? To a limited extent, the answer is yes. Between 2012 and 2017, the percentage share of all Midwestern dealflow going to West North Central states like the Dakotas, Minnesota and Missouri has grown from 25.4 percent to 31.2 percent, up by nearly one-fifth in relative terms.

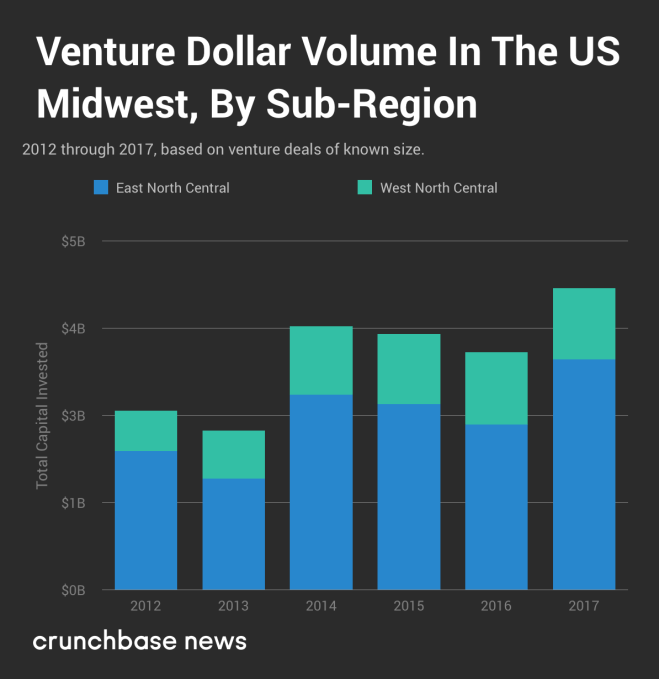

Now let’s check out dollar volume. The chart below displays aggregate reported venture capital dollar volume raised by startups in the Midwest.

As far as the amount of money Midwestern startups have raised over time, the trendline is generally up and to the right. But that’s not the only way this differs from the deal volume data we looked at earlier. For dollar volume, there appears to be no appreciable change in the “balance of power” between the two sub-regions since 2012. Depending on the year, East North Central states like Illinois, Michigan and Ohio raked in between 70 and 78 percent of total dollar volume, but that variance doesn’t appear in an orderly trend.

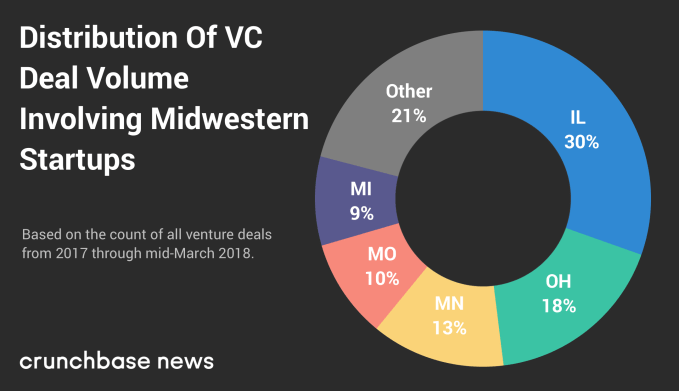

We started first at the regional level, then compared smaller groupings of states. Now, let’s see how deal and dollar volume is distributed on a state-by-state level. Doing so will point to the states that lead the region in venture-backed startup activity. Below, you’ll find a chart of how deal volume is split between the top five Midwestern states.

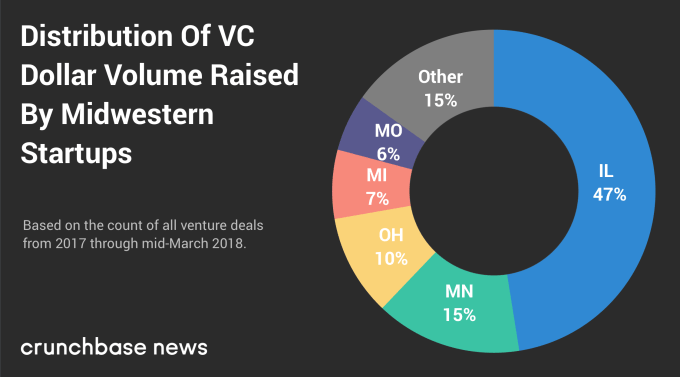

And here is how dollar volume is distributed.

As we saw with our analysis of the South, the top five Midwestern states for deal volume are the same five top-ranked states for dollar volume. But there is some notable variation in how these states rank among each other and the amount of deal and dollar volume they account for.

Considering that Illinois is home to Chicago and a number of downstate universities with deep tech startup roots, the fact that it places first for both metrics shouldn’t come as much of a surprise.

What might be more of a head-scratcher is Minnesota, which ranks third in deal volume but second in dollar volume. Why does it switch places with Ohio? The answer could lie in the industrial mix which, in the case of Minnesota, includes a disproportionately high number of medical device and other life sciences companies, which typically take a lot of capital to get off the ground.

Longtime readers of Crunchbase News may remember a ranking of Midwestern startup cities we wrote back in August 2017. However, here we’re just focusing on deal and dollar volume over the past 15 months, since the start of 2017.

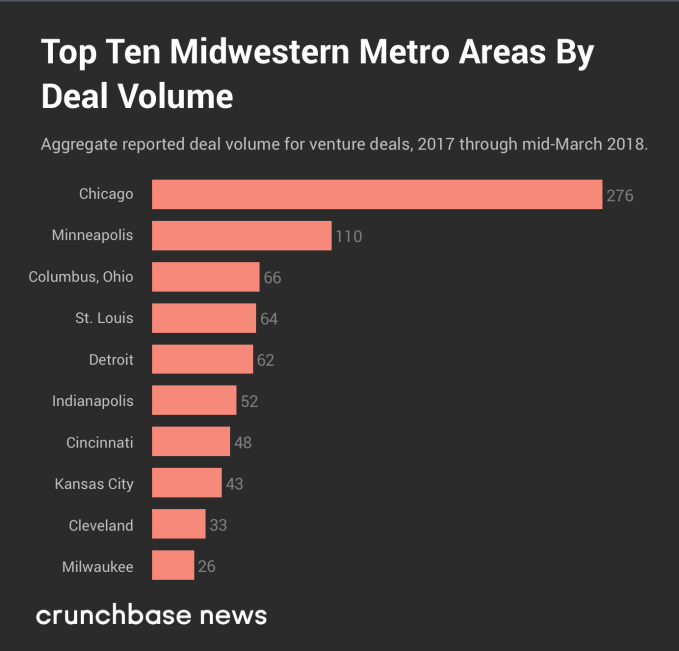

Let’s start first with the top 10 Midwestern cities as measured by number of startup funding rounds.

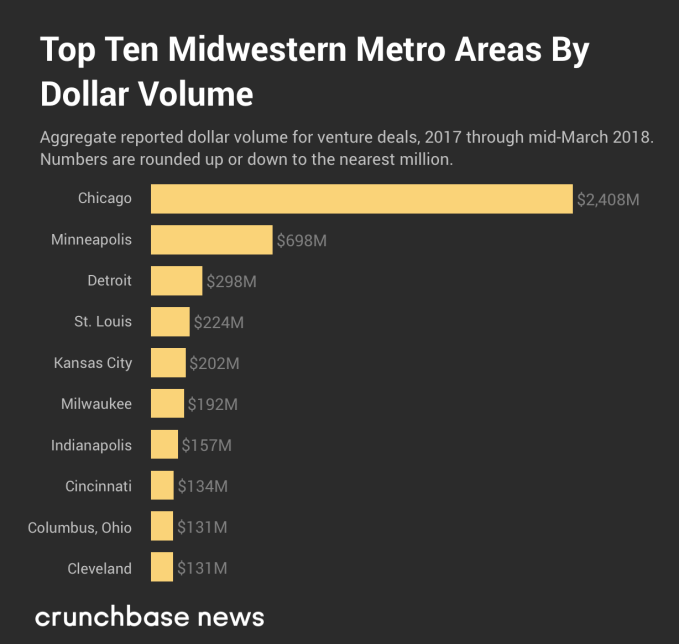

And in the chart below, you can see the top cities, as ranked by venture dollar volume, from the same period of time.

In both rankings, four of the top five cities are the same, but the odd one out appears to be Columbus, Ohio. Although there were a fairly large number of rounds raised by startups in that metro area, most of the rounds were fairly small by national standards. And one of the main reasons why Kansas City, Missouri jumped so much in the dollar volume rankings was a $100 million Series F round raised by C2FO.

But, again, as far as the Midwest goes, everything pales in comparison to Chicago alone.

For many, the Midwest is in a kind of Goldilocks zone. The East and West coasts seem to hold more or less equal sway over the culture and economy and most of its cities are neither too big nor too small. The only extreme it seems to occupy is its winter weather.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

See you tonight! We’ll be meeting at 7pm in the MakeOffices space in the Loop. There will be some free beers and chicken sandwiches. We’ll hold a pitchoff at 8pm and close up at 9pm and perhaps we can go carousing afterwards. The pitch-off will be very cool. I’ve already picked nine contestants and we have two VC judges. First place winners of the pitch off will get a table… Read More

See you tonight! We’ll be meeting at 7pm in the MakeOffices space in the Loop. There will be some free beers and chicken sandwiches. We’ll hold a pitchoff at 8pm and close up at 9pm and perhaps we can go carousing afterwards. The pitch-off will be very cool. I’ve already picked nine contestants and we have two VC judges. First place winners of the pitch off will get a table… Read More

Powered by WPeMatico