challenger banks

Auto Added by WPeMatico

Auto Added by WPeMatico

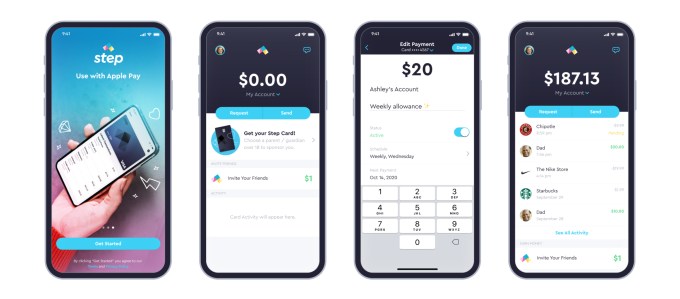

Step, the digital banking service aimed at teens and endorsed by TikTok star Charli D’Amelio, announced this morning the close of a $100 million round of Series C funding after growing to more than 1.5 million users just six months after launch. The new round, led by General Catalyst, comes shortly after Step’s $50 million Series B, announced at the end of last year after the startup hit half a million users in only two months post-launch.

The new round also includes participation from Step’s existing investors, Coatue, Stripe, Charli D’Amelio, The Chainsmokers, Will Smith and Jeffrey Katzenberg, and brings on newcomer Franklin Templeton, signaling a plan to move into investments is on the horizon. It also includes actor and musician Jared Leto. Step is also formally announcing NBA All-Star Stephen Curry as an investor, which had not previously been disclosed, as well as former Square executives Sarah Friar, Jacqueline Reses and Gokul Rajaram.

As a result of the fundraise, Kyle Doherty of General Catalyst is joining Step’s board. To date, Step has raised more than $175 million.

Image Credits: Step

According to CEO CJ MacDonald, Step hasn’t yet spent the money from its Series B, but believes the additional funds can help the startup grow more quickly.

“We’ve signed up more than a million and a half accounts in the first six months. We’re signing up 10,000 accounts-plus a day, and there’s just a lot of things that we want to do to bring this to millions and millions of households to help educate the next generation be smarter with money,” he says. At the time of the Series B, for comparison, Step said it was adding around 7,000 to 10,000 accounts per day.

“Honestly we don’t need the capital,” MacDonald added. “It’s just we think speed to market is really key and we think we can accelerate our growth and invest in infrastructure.”

The company is also planning to hire across operations, engineering, product and design, to double its now 65-person team over the next year.

Step today competes in a crowded market of mobile banking services aimed at a younger demographic, but it’s one of very few that targets teenagers ages 13 to 18. Through Step’s app, teens gain access to an FDIC-insured bank account without fees and a secured Visa card that helps them establish credit before they turn 18. The app also offers Venmo-like functionality for sending money to friends.

Image Credits: Step

Step’s growth so far has benefitted from a combination of factors, including word-of-mouth, use of social media and its popular referral program, which has paid out a few dollars per new sign-up. Step has also leveraged its partnerships with social media influencers like D’Amelio and Josh Richards, as well as celebs like Step investor Justin Timberlake.

The company believes the Curry announcement may also help to raise awareness about the banking app. As a father of three, if Curry talks about introducing Step to his own children, people will take notice.

While the additional funds are focused on driving growth, Step is also thinking about its future as its existing users begin to age up. The company plans to enter into the credit and lending market, as well as introduce investments at some point in the future. The Franklin Templeton investment could be useful here, MacDonald notes.

“Franklin [Templeton is] obviously, one of the largest financial institutions in the world. And, as we start thinking about investments and the journey of the customer, to have a great brand like Franklin Templeton that’s invested in this round — I think it’s just a testament to where they see the world going,” he says.

Step’s fundraise falls on the same day that competitor Current and Greenlight, both which focus on families, also raised new rounds.

Powered by WPeMatico

Monzo founder Tom Blomfield is departing the U.K. challenger bank entirely at the end of the month, staff were informed earlier today.

Blomfield held the role of CEO until May last year when he assumed the newly created title of president and resigned from the Monzo board. However, having been given the time and space to consider his long-term future at the bank he helped create six years ago, and with a refreshed executive team now in place, he says it is time to “hand over the baton”.

In a brief but candid telephone interview, Blomfield also revealed that, as well as being unhappy during the last couple of years as CEO when the company scaled well beyond a “scrappy startup”, the pandemic and subsequent lockdowns exacerbated pressures placed on his own mental well-being. “I’m very happy to talk about what’s gone on with me, because I don’t think people do it enough”, he says.

“I stopped enjoying my role probably about two years ago… as we grew from a scrappy startup that was iterating and building stuff people really love, into a really important U.K. bank. I’m not saying that one is better than the other, just that the things I enjoy in life is working with small groups of passionate people to start and grow stuff from scratch, and create something customers love. And I think that’s a really valuable skill but also taking on a bank that’s three, four, five million customers and turning it into a 10 or 20 million customer bank and getting to profitability and IPOing it, I think those are huge exciting challenges, just honestly not ones that I found that I was interested in or particularly good at”.

In early 2019 after realising he was “doing too much and not enjoying it,” Blomfield began talking to Monzo investor Eileen Burbidge of Passion Capital, and Monzo Chair Gary Hoffman, about changing roles and how he needed more help. Then, he says, “COVID just exacerbated things,” a period when Monzo also had to cut staff, shutter its Las Vegas office and raise bridge funding in a highly publicised down round.

“I think [for] a lot of people in the world — and you and I have spoken about this — going through a pandemic, going through lockdown and the isolation involved in that has an impact on people’s mental health,” says Blomfield. “I don’t think I was any different, so I was really struggling. I had a really, really supportive exec team around me and a really supportive set of investors on board and I was really grateful that when I put my hand up and said, ‘I need help,’ they were super receptive to that”.

Blomfield also comes clean about his role as president, a title that was intended as a way to provide the time and space for him to get well and figure out if he would return longer-term to Monzo or depart entirely. Contrary to rumours, Blomfield says he wasn’t pushed out by investors. Instead, the Monzo board actually put pressure on him to remain as CEO longer than he wanted or perhaps should have (a version of events corroborated by my own sources). “When I took that president role, it was not certain one way or another what would happen,” Blomfield says, apologising in case I felt I was misled when I reported the news.

(The truth is, within weeks of running that news piece, I knew it was far from certain Blomfield would ever return, with multiple sources, including people close to and worried about Blomfield, confiding in me how burned out the Monzo founder was. As weeks turned into months and following additional sourcing, I had enough information to write a follow-up story much earlier but chose to wait until a formal decision was taken.)

TechCrunch’s Steve O’Hear interviewing Monzo’s Tom Blomfield. Image Credits: Startup Grind

Meanwhile, Blomfield describes his resignation as a Monzo employee as “bitter-sweet,” and is keen to praise what the Monzo team has already achieved, including since his much-reduced involvement. “I think the team has done phenomenally well over the last year or so in really difficult circumstances,” he says. In particular, he cites Monzo’s new CEO TS Anil as doing a “phenomenal” job, while describing Sujata Bhatia, who joined as COO last year, as “an absolute machine, a real operator”.

To that end, Monzo now has almost 5 million customers, up from 1.3 million in 2019. Monzo’s total weekly revenue is now 30% higher than pre-pandemic, helped no doubt by over 100,000 paid subscribers across Monzo Plus and Premium in the last five months (sources tell me the company surpassed £2 million in weekly revenue in December for the first time in its history). Albeit at a lower valuation, the challenger bank also raised £125 million from new and existing investors during the pandemic.

Blomfield also says that Anil and Bhatia and other members of the Monzo executive team have specific skills — that he simply doesn’t have — related to scaling and managing a bank approaching 5 million customers. And even if he did, he has learned the hard way that there are aspects of running a large company that not everyone enjoys.

“Going from a CEO where you’re front and centre dealing with all of the different pressures every day to a much lighter role is a huge huge weight off my shoulders and has given me the time and space to recover”, he adds. “I’m now feeling pretty great. I’m enjoying life again”.

As for what’s next for Blomfield, he says he wants to “chill out” for a bit and perhaps take a holiday. He’s also finishing his vaccination training so that he can volunteer to help deliver the U.K.’s national COVID-19 vaccination rollout. A recent tweet by Blomfield about a side project also led to speculation that he has begun a new venture. Not true, says Blomfield, telling me it was a five-day project designed to get back into coding and play with a robotic 2D printer. And while he’s very much left Monzo, he says he’ll continue cheering on the company from the outside.

Powered by WPeMatico

With nearly half a million customers across Mexico and a network of 30,000 retail locations where representatives can take deposits, the challenger bank albo is already on its way to becoming a dominant player in Mexico’s emerging fintech industry.

And the company has recently raised another $45 million to consolidate its position.

“When your mission is to build the biggest bank in Mexico, you will need a ton of money,” said albo founder Angel Sahagún.

The company received its license to operate as a full depository bank in Mexico, and is slowly working toward being the premier internet-based financial services provider for Mexico’s large and growing middle class, Sahagún said.

“We are targeting a similar target market to Chime,” the albo founder and chief executive said. “We are targeting people who are underbanked and don’t have access to all the financial products in the market.”

Sahagún said the money will be used to expand into lending and insurance products the range of services albo offers. That’s a path that has already produced one multi-billion-dollar business in Nubank, Brazil’s wildly successful fintech company, which planted a flag for a new generation of Latin American startups.

While many challenger banks in the region pursued a strategy targeting upper-class and upper-middle-class consumers, Sahagún said his service had chosen a different path.

The company is trying to bring the middle and low-income Mexican consumers into the banking system by making it easy for them to move from a cash-based world to a digital one. “Where 90% of transactions are cash-based you need a value proposition that fits very well on that cash-based society,” Sahagún said.

It’s why the company set up a network of 30,000 locations, including convenience stores and drug stores, so that it can accept deposits at the places where its customers frequent.

That growth, and the company’s 40% share of the digital banking market in Mexico, according to data from Apptopia cited by the company, is why investors like Valar Ventures, Greyhound Capital, Mountain Nazca and Flourish Ventures were willing to invest as part of the $45 million round.

“albo has proven its ability to drive sustainable growth and is leading the market. This is the team that is going to transform banking in the region and we are proud to be supporting them in that,” said James Fitzgerald of Valar Ventures, in a statement.

Powered by WPeMatico

Amount, a new service that helps traditional banks compete in a digital world, has raised $81 million from none other than Goldman Sachs as it looks to help legacy fintech players compete with their more nimble digital counterparts.

The company, which spun out from the startup lending company Avant in January of this year, has already inked deals with Banco Popular, HSBC, Regions Bank and TD Bank to power their digital banking services and offer products like point-of-sale lending to compete with challenger banks like Chime and lenders like Affirm or Klarna.

“Most banks are looking for resources and infrastructure to accelerate their digital strategy and meet the demands of today’s consumer,” said Jade Mandel, a vice president in Goldman Sachs’ growth equity platform, GS Growth, who will be joining the board of directors at Amount, in a statement. “Amount enables banks to navigate digital transformation through its modular and mobile-first platform for financial products. We’re excited to partner with the team as they take on this compelling market opportunity.”

Complementing those customer-facing services is a deep expertise in fraud prevention on the back-end to help banks provide more loans with less risk than competitors, according to chief executive Adam Hughes.

It’s the combination of these three services that led Goldman to take point on a new $81 million investment in the company, with participation from previous investors August Capital, Invus Opportunities and Hanaco Ventures — giving Amount a post-money valuation of $681 million and bringing the company’s total capital raised in 2020 to a whopping $140 million.

Think of Amount as a white-labeled digital banking service provider for Luddite banks that hadn’t upgraded their services to keep pace with demands of a new generation of customers or the COVID-19 era of digital-first services for everything.

Banks pay a pretty penny for access to Amount’s services. On top of a percentage for any loans that a bank processes through Amount’s services, there’s an up-front implementation fee that typically averages at $1 million.

The hefty price tag is a sign of how concerned banks are about their digital challengers. Hughes said that they’ve seen a big uptick in adoption since the launch of their buy-now-pay-later product designed to compete with the fast growing startups like Affirm and Klarna .

Indeed, by offering banks these services, Amount gives Klarna and Affirm something to worry about. That’s because banks conceivably have a lower cost of capital than the startups and can offer better rates to borrowers. They also have the balance sheet capacity to approve more loans than either of the two upstart lenders.

“Amount has the wind at its back and the industry is taking notice,” said Nigel Morris, the co-founder of Capital One and an investor in Amount through the firm QED Investors. “The latest round brings Amount’s total capital raised in 2020 to nearly $140 million, which will provide for additional investments in platform research and development while accelerating the company’s go-to-market strategy. QED is thrilled to be a part of Amount’s story and we look forward to the company’s future success as it plays a vital role in the digitization of financial services.”

FT Partners served as advisor to Amount on this transaction.

Powered by WPeMatico

With $90 million in deposits and $18.25 million in new financing, HMBradley is making moves as the Los Angeles-based entrant into the challenger bank competition.

LA is home to a growing community of financial services startups, and HMBradley is quickly taking its place among the leaders with a novel twist on the banking business.

Unlike most banking startups that woo customers with easy credit and savvy online user interfaces, HMBradley is pitching a better savings account.

The company offers up to 3% interest on its savings accounts, much higher than most banks these days, and it’s that pitch that has won over consumers and investors alike, according to the company’s co-founder and chief executive, Zach Bruhnke.

With climbing numbers on the back of limited marketing, Bruhnke said raising the company’s latest round of financing was a breeze.

“They knew after the first call that they wanted to do it,” Brunke said of the negotiations with the venture capital firm Acrew, a venture firm whose previous exposure to fintech companies included backing the challenger bank phenomenon which is Chime . “It was a very different kind of fundraise for us. Our seed round was a terrible, treacherous 16-month fundraise,” Brunke said.

For Acrew’s part, the company actually had to call Chime’s founder to ensure that the company was okay with the venture firm backing another entrant into the banking business. Once the approval was granted, Brunke said the deal was smooth sailing.

Acrew, Chime and HMBradley’s founders see enough daylight between the two business models that investing in one wouldn’t be a conflict of interest with the other. And there’s plenty of space for new entrants in the banking business, Bruhnke said. “It’s a very, very large industry as a whole,” he said.

As the company grows its deposits, Bruhnke said there will be several ways it can leverage its capital. That includes commercial lending on the back end of HMBradley’s deposits and other financial services offerings to grow its base.

For now, it’s been wooing consumers with one-click credit applications and the high interest rates it offers to its various tiers of savers.

“When customers hit that 3% tier they get really excited,” Bruhnke said. “If you’re saving money and you’re not saving to HMBradley then you’re losing money.”

The money that HMBradley raised will be used to continue rolling out its new credit product and hiring staff. It already poached the former director of engineering at Capital One, Ben Coffman, and fintech thought leader Saira Rahman, the company said.

In October, the company said, deposits doubled month-over-month and transaction volume has grown to over $110 million since it launched in April.

Since launching the company’s cash back credit card in July, HMBradley has been able to pitch customers on 3% cash back for its highest tier of savers — giving them the option to earn 3.5% on their deposits.

The deposit and lending capabilities the company offers are possible because of its partnership with the California-based Hatch Bank, the company said.

Powered by WPeMatico

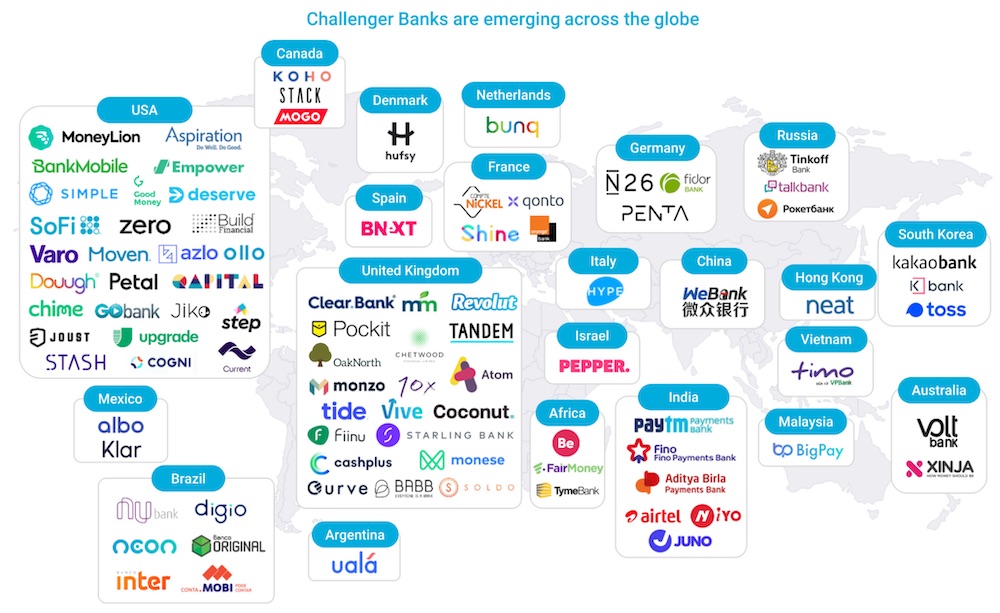

The neobank, or digital bank, phenomenon continues to take the world by storm, with global winners, from Brazil’s Nubank valued at $10 billion and Berlin’s N26 valued at $3.5 billion, to Chime, now valued at $14.5 billion as the most valuable consumer fintech in the United States.

Neobanks have led the charge of the $3.6 billion in venture capital funding for consumer fintech startups this year. And as the coronavirus-fueled acceleration of digital transformation continues, it seems the digital bank is here to stay, with some estimates pointing to neobanks reaching 60 million customers in North America and Europe by the end of 2020, and surpassing 145 million by 2024.

The space is also becoming more crowded, a trend which will only accelerate with fintech eating the world and creating greater infrastructure that enables any company to include a bank account as a product extension.

FT Partners Fintech Industry Research, January 2020

As a result, neobanks are not a monolithic model and not all are created equal. Looking underneath the hood of business models across the globe reveals remarkable operational differences and highlights specific features that are more likely to succeed in the long-term.

Today there are five distinct models that are leading globally:

Interchange-led: Relies on payments revenue, sourced through interchange as the revenue driver. Every time a customer uses the neobank’s card as a payment method they get paid [e.g. Chime / US; Neon (hybrid of 1 & 2) / Brazil].

Credit-led: Leverages a credit-first model, starting off with a credit card or similar offering, and later providing a bank account [e.g. Nubank, Neon (hybrid of 1 & 2) / Brazil].

Powered by WPeMatico

More than five years after starting the company, Monzo co-founder Tom Blomfield is stepping down as CEO of the U.K. challenger bank to take up the newly created role of president.

Current U.S. CEO, TS Anil, will become the new “Monzo UK Bank CEO,” subject to regulatory approval, and for now will hold both U.K. and U.S. roles.

Anil previously held exec roles at Visa, Standard Chartered Bank and Citi, and therefore brings a ton of banking and financial services experience. This includes things like dealing with regulators and overseeing a large corporate structure, two things a scale-up challenger bank like Monzo, with more than 4 million customers and over 1,500 staff, requires.

The thinking behind Blomfield’s move to president is a startup cliché but also likely holds water; he’ll be able to spend more time doing the things he enjoys most (and is arguably best at), such as focusing on the longer-term vision, product and how Monzo can stay close to and best serve customers. Meanwhile, Anil — and, in the future, other country-specific CEOs — can do the day to day, more regulated aspects of running a bank.

In a brief call with Blomfield just moments ago, he told me he had been thinking about a transition into a different role for about 18 months, but it wasn’t until much more recently that a formal decision was taken.

“I went through all the stuff I love about my job, and it was all the stuff I did in the first two or three years,” he said. “And I went through all the stuff that drains me, and it’s all the stuff I’ve done in the last two years, honestly. Things I think TS is awesome at.”

Although it is unlikely that a huge amount will change immediately, Blomfield says he hopes that he’ll be able to spend a “bunch more time doing the stuff I really, really love, which is community, talking to customers, helping develop the product proposition, long-term vision, and talking to journalists, like you Steve, obviously, and try to unwind my involvement a little bit in more formal regulated banking activities.”

Meanwhile, it has been somewhat of a turbulent time for Monzo in recent months, as it, along with many other fintech companies, has attempted to insulate itself from the coronavirus crisis and resulting economic downturn.

Last month, I reported that Monzo was shuttering its customer support office in Las Vegas, seeing 165 customer support staff in the U.S. lose their jobs. And just a few weeks earlier, we reported that the bank was furloughing up to 295 staff under the U.K.’s Coronavirus Job Retention Scheme. In addition, the senior management team and the board has volunteered to take a 25% cut in salary, and co-founder and CEO Tom Blomfield has decided not to take a salary for the next 12 months.

Like other banks and fintechs, the coronavirus crisis has resulted in Monzo seeing customer card spend reduce at home and (of course) abroad, meaning it is generating significantly less revenue from interchange fees. The bank has also postponed the launch of premium paid-for consumer accounts, one of only a handful of known planned revenue streams, alongside lending, of course.

And just last week, it was reported that Monzo is closing in on £70-80 million in top up funding, to help extend its coronavirus crisis runaway. However, as new and some existing investors play hardball, the company has reportedly had to accept a 40% reduction in its previously £2 billion valuation as part of its last funding round last June, with a new valuation of £1.25 billion.

With that said, it’s not all been bad news. Monzo recently launched business accounts, many of which are revenue generating, with both free and paid tiers. It also recruited Sujata Bhatia, a former American Express executive in Europe, as its new COO.

And, hopefully, in his new role as president, Blomfield will sound re-energised next time I call him.

Powered by WPeMatico

The world of consumer banking has seen a massive shift in the last ten years. Gone are the days where you could open an account, take out a loan, or discuss changing the terms of your banking only by visiting a physical branch. Now, you can do all this and more with a few quick taps on your phone screen — a shift that has accelerated with customers expecting and demanding even faster and more responsive banking services.

As one mark of that switch, today a startup called Thought Machine, which has built cloud-based technology that powers this new generation of services on behalf of both old and new banks, is announcing some significant funding — $83 million — a Series B that the company plans to use to continue investing in its platform and growing its customer base.

To date, Thought Machine’s customers are primarily in Europe and Asia — they include large, legacy outfits like Standard Chartered, Lloyds Banking Group, and Sweden’s SEB through to “challenger” (AKA neo-) banks like Atom Bank. Some of this financing will go towards boosting the startup’s activities in the US, including opening an office in the country later this year and moving ahead with commercial deals.

The funding is being led by Draper Esprit, with participation also from existing investors Lloyds Banking Group, IQ Capital, Backed and Playfair.

Thought Machine, which started in 2014 and now employs 300, is not disclosing its valuation but Paul Taylor, the CEO and founder, noted that the market cap is currently “increasing healthily.” In its last round, according to PitchBook estimates, the company was valued at around $143 million, which, at this stage of funding, puts this latest round potentially in the range of between $220 million and $320 million.

Thought Machine is not yet profitable, mainly because it is in growth mode, said Taylor. Of note, the startup has been through one major bankruptcy restructuring, although it appears that this was mainly for organisational purposes: all assets, employees and customers from one business controlled by Taylor were acquired by another.

Thought Machine’s primary product and technology is called Vault, a platform that contains a range of banking services: checking accounts, savings accounts, loans, credit cards and mortgages. Thought Machine does not sell directly to consumers, but sells by way of a B2B2C model.

The services are provisioned by way of smart contracts, which allows Thought Machine and its banking customers to personalise, vary and segment the terms for each bank — and potentially for each customer of the bank.

It’s a little odd to think that there is an active market for banking services that are not built and owned by the banks themselves. After all, aren’t these the core of what banks are supposed to do?

But one way to think about it is in the context of eating out. Restaurants’ kitchens will often make in-house what they sell and serve. But in some cases, when it makes sense, even the best places will buy in (and subsequently sell) food that was crafted elsewhere. For example, a restaurant will re-sell cheese or charcuterie, and the wine is likely to come from somewhere else, too.

The same is the case for banks, whose “Crown Jewels” are in fact not the mechanics of their banking services, but their customer service, their customer lists, and their deposits. Better banking services (which may not have been built “in-house”) are key to growing these other three.

“There are all sorts of banks, and they are all trying to find niches,” said Taylor. Indeed, the startup is not the only one chasing that business. Others include Mambu, Temenos and Italy’s Edera.

In the case of the legacy banks that work with the startup, the idea is that these behemoths can migrate into the next generation of consumer banking services and banking infrastructure by cherry-picking services from the VaultOS platform.

“Banks have not kept up and are marooned on their own tech, and as each year goes by, it comes more problematic,” noted Taylor.

In the case of neobanks, Thought Machine’s pitch is that it has already built the rails to run a banking service, so a startup — “new challengers like Monzo and Revolut that are creating quite a lot of disruption in the market” (and are growing very quickly as a result) — can integrate into these to get off the ground more quickly and handle scaling with less complexity (and lower costs).

Taylor was new to fintech when he founded Thought Machine, but he has a notable track record in the world of tech that you could argue played a big role in his subsequent foray into banking.

Formerly an academic specialising in linguistics and engineering, his first startup, Rhetorical Systems, commercialised some of his early speech-to-text research and was later sold to Nuance in 2004.

His second entrepreneurial effort, Phonetic Arts, was another speech startup, aimed at tech that could be used in gaming interactions. In 2010, Google approached the startup to see if it wanted to work on a new speech-to-text service it was building. It ended up acquiring Phonetic Arts, and Taylor took on the role of building and launching Google Now, with that voice tech eventually making its way to Google Maps, accessibility services, the Google Assistant and other places where you speech-based interaction makes an appearance in Google products.

While he was working for years in the field, the step changes that really accelerated voice recognition and speech technology, Taylor said, were the rapid increases in computing power and data networks that “took us over the edge” in terms of what a machine could do, specifically in the cloud.

And those are the same forces, in fact, that led to consumers being able to run our banking services from smartphone apps, and for us to want and expect more personalised services overall. Taylor’s move into building and offering a platform-based service to address the need for multiple third-party banking services follows from that, and also is the natural heir to the platform model you could argue Google and other tech companies have perfected over the years.

Draper Esprit has to date built up a strong portfolio of fintech startups that includes Revolut, N26, TransferWise and Freetrade. Thought Machine’s platform approach is an obvious complement to that list. (Taylor did not disclose if any of those companies are already customers of Thought Machine’s, but if they are not, this investment could be a good way of building inroads.)

“We are delighted to be partnering with Thought Machine in this phase of their growth,” said Vinoth Jayakumar, Investment Director, Draper Esprit, in a statement. “Our investments in Revolut and N26 demonstrate how banking is undergoing a once in a generation transformation in the technology it uses and the benefit it confers to the customers of the bank. We continue to invest in our thesis of the technology layer that forms the backbone of banking. Thought Machine stands out by way of the strength of its engineering capability, and is unique in being the only company in the banking technology space that has developed a platform capable of hosting and migrating international Tier 1 banks. This allows innovative banks to expand beyond digital retail propositions to being able to run every function and type of financial transaction in the cloud.”

“We first backed Thought Machine at seed stage in 2016 and have seen it grow from a startup to a 300-person strong global scale-up with a global customer base and potential to become one of the most valuable European fintech companies,” said Max Bautin, Founding Partner of IQ Capital, in a statement. “I am delighted to continue to support Paul and the team on this journey, with an additional £15 million investment from our £100 million Growth Fund, aimed at our venture portfolio outperformers.”

Powered by WPeMatico

Penta, the Berlin-based business banking challenger that also now operates in Italy, has partnered with BBVA-backed card reader company SumUp in a bid to attract more offline businesses.

Up until recently, Penta had been targeting digital businesses, such as startups and e-commerce SMEs, but has since re-positioned itself for wider business banking appeal.

By partnering with a POS provider offering easy card reader-enabled payments, the German challenger bank wants to extend that offline (such as restaurants, craftsman, healthcare and architects).

Specifically, Penta says businesses can order a SumUp Card Reader via Penta, and in doing so will save money on the initial SumUp setup fee and be able to seamlessly integrate SumUp-powered payments with their Penta account.

They’ll also get access to the existing Penta features, such as being able to open a business banking account entirely digitally, issue multiple payment cards, grant limits and permissions per card for staff, facilitate expense management and integrate with popular accounting tools.

In the future, the SumUp integration is planned to go deeper. This will include the ability to use SumUp payments data to forecast future sales and feed into a business’s credit worthiness when they seek a loan.

“One request that we’ve had since day one has been for our customers to easily and quickly accept card payments, so we are very proud to be able to offer this with our newest partner SumUp,” says Penta CEO Marko Wenthin in a statement.

Adds James Henry, head of Sales and Partnerships at SumUp: “By cooperating with Penta, we will enable even more small and medium-sized companies to digitize their business and make the payment experience as convenient as possible for their customers. Penta, with its growing customer base of companies, is the ideal partner for us to reach the broad mid-market.”

Powered by WPeMatico

The new era of tech-enabled banks is coming, even in regulation-heavy Japan. Kyash, a fintech company with visions on becoming Japan’s first challenger bank, said today it has raised $14 million to continue its expansion.

To be clear, Kyash isn’t a bank. Yet. But it is currently applying for a host of licenses in Japan that could allow it to offer banking-style features, including checking accounts, ATM withdrawals and money remittance. Right now, it is a payment app that offers a connected Visa card in the style of Monzo, N26, Revolut (which has a Japan license) and others of that ilk.

The startup was founded in 2015 by Shinichi Takatori, a former banker and management consultant who saw the potential to merge tech and finance.

“I really noticed that information and communication has become ubiquitous but money itself hasn’t changed for a long time,” Takatori told TechCrunch in an interview.

The company took some time — two years — before it released a consumer product, but it quickly tied up with Visa to offer a prepaid debit card that connects to the Kyash app. That provides benefits like instant payment notifications, clear balance and lower fees for overseas spending, while costs are borne by merchants rather than users. They might seem elementary today, but they are still not standard among Japan’s traditional banks, Takatori explained.

The company declined to share its user numbers, but Takatori said this new round of funding — Kyash’s Series B — is a validation of the progress it has made.

The $14 million investment is co-led by Goodwater Capital, a U.S. investor that has backed fintech startups like Monzo, Stash and Toss in Korea, and Mitsubishi UFJ Capital, the investment arm of Japan’s largest bank.

Mitsubishi’s involvement means that Kyash counts Japan’s three largest banks as investors, with SMBC and Mizuho having previously put money into the company. Others that took part in this Series B include Toppan Printing, JAFCO and Shinsei Corporate Investment Limited.

So many banks on the cap table might seem like a strange thing for a disruptor — let alone the banks, which tend to behave territorially — but Takatori believes that there’s the potential for cooperation, not to mention that it will help the startup with its licensing efforts. Already, he revealed, Mitsubishi plans to integrate its card with the Kyash app to provide its customers with the best of both worlds.

“We’re not here to win over existing banks, but instead inform [them of] how money should work in next decade,” explained Takatori. “So why not collaborate in some way.”

Kyash has a tie-up with Visa that allows it to offer its customers a connected debit card and also provide issuing services to other fintech startups

There’s also the fact that, even with a license, Kyash and others are unlikely to be able to offer full banking services. That means they will have to serve as complementary offerings to the industry, which would likely mean that cooperation is good — essential — for both sides.

But, beyond the consumer play, a notable piece of Kyash’s business that has investors excited is its B2B payment business.

The company developed its own payment processing system to reduce costs, which is one reason it took time to launch. Thanks to a tie-up with Visa, it offers both issuing and processing of prepaid Visa cards to fintech companies in Japan that want to go down the payment route.

That’s increasingly popular, given the government push to make the country a “cashless society” ahead of the 2020 Olympic Games next year. It also could appeal to crypto companies in Japan, which offers the world’s most robust licensing, that want to follow the example of the Coinbase card in Europe or startups like Crypto.com and TenX, which offer similar prepaid cards.

Takatori said Kyash is “in discussions” with crypto companies, but that it has not made a decision on how to proceed yet. The company is also eyeing potential overseas expansions, although that is some way down the line.

“We have open eyes for globalization, it’s just a matter of when,” he told TechCrunch. “We still have a far way to go [in Japan, but] maybe after the Olympics.”

More pressingly, he sees the company looking to raise a “pretty quick” Series C round to give it acceleration into next year. That’s likely to go to more expansion and user acquisition as the licenses the startup has applied for are unlikely to be granted this year.

Powered by WPeMatico