cash app

Auto Added by WPeMatico

Auto Added by WPeMatico

This morning Square, a fintech company that serves both individuals and companies, announced that it has purchased a majority stake in Tidal, a music streaming service. The deal, worth some $297 million, will allow artist-partners to keep their ownership in the music company.

Square CEO Jack Dorsey used his other company, Twitter, this morning to explain the deal. Dorsey seemed to expect the transaction to generate skepticism — which it definitely has. In his opening message, he asked a rhetorical question: “Why would a music streaming company and a financial services company join forces?!”

Why indeed. Dorsey’s expectation is that his company can replicate the success of Cash App and other Square products in the world of music. Noting that “new ideas are found at the intersection,” Dorsey argued that the confluence of “music and the economy” is one such point of convergence.

The deal also installs musician and businessperson Jay-Z on Square’s board.

Some early reaction to the deal has proved negative. It’s not hard to riff on the seeming strangeness of Square and Tidal as a pair. And Square has made acquisitions in the past that appeared adjacent and failed to stick. The company bought food-delivery service Caviar in 2014 before selling it to DoorDash in 2019, for example; that Square appears to have made a venture-level return on the transaction is immaterial to the focus argument.

But the bull-case for the Square-Tidal tie-up is easy to make as well. The American fintech just spent a minute fraction of a single percent of its market capitalization on the smaller company, and through its choice to let artists keep their stake, has effectively onboarded a host of ambassadors for its brand.

And Dorsey is not wrong that Square did shake up the commerce game for many offline businesses with its original card reader. Why not take a swing at a part of the economy — music — that has migrated from the physical world to the digital in the past few years, much like small businesses in recent quarters?

Square’s business users, its “seller ecosystem,” as it likes to call it, are increasingly digital. In its most recent quarterly earnings report, “in-person only” usage is falling as a percentage of seller gross payment volume (GPV), while “online only” and “omnichannel” GPV are taking up the slack.

Square has a known win in its consumer-focused Cash App service, which reached 36 million monthly actives in December of 2020, up from 24 million in the same period one year prior. You can imagine tie-ups between the music company and the youth-skewing Cash App audience. And having Jay-Z at the Square boardroom table will hardly make the company less innovative; he may bring fresh perspective.

And then there’s the question of NFTs, or non-fungible tokens, a new form of digital asset that have recently become the cause célèbre of the cryptocurrency community. Given that Square has a growing cryptocurrency business via Cash App, and has invested hundreds of millions of dollars into bitcoin itself. If there is space in the market for Square to bring music-based NFTs to its larger consumer user base is an interesting question. If the answer is yes, Square could now be in a leading position to create that market.

Perhaps the Square-Tidal deal won’t generate the future growth that Square imagines. But the deal is cheap, snagging Jay-Z as a leader is a win and it’s hard to win by only playing corporate defense.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Cash App, the peer-to-peer payments service from Square, is giving select users a way to get short-term loans.

The company said it’s only testing the feature with around 1,000 users for now. But it could become more broadly available — and there are probably plenty of people who could use the money, given the state of the U.S. and global economy, not to mention the current uncertainty about further stimulus plans.

Cash App is starting out by offering loans for any amount between $20 and $200. You’ll be expected to pay the loan back in four weeks, along with a flat fee of 5%. (Multiplied over a year, that turns into a 60% APR — which sounds high, but at least it’s significantly lower than the average payday loan.)

If you don’t pay off the loan after four weeks, you’ll get an additional one-week grace period, then Square and Cash App will start adding 1.25% (non-compounding) interest each week. You also won’t be able to take out an additional loan if you’ve previously defaulted.

“We are always testing new features in Cash App, and recently began testing the ability to borrow money with about 1,000 Cash App customers,” a company spokesperson said in a statement. “We look forward to hearing their feedback and learning from this experiment.”

Square has already been expanding Cash App’s features beyond simple peer-to-peer money transfer with things like the Cash Card (a free debit card), Cash Boost (rewards) and Cash App Investing. And beyond Cash App, Square has been offering loans to small businesses through its Square Capital arm.

Powered by WPeMatico

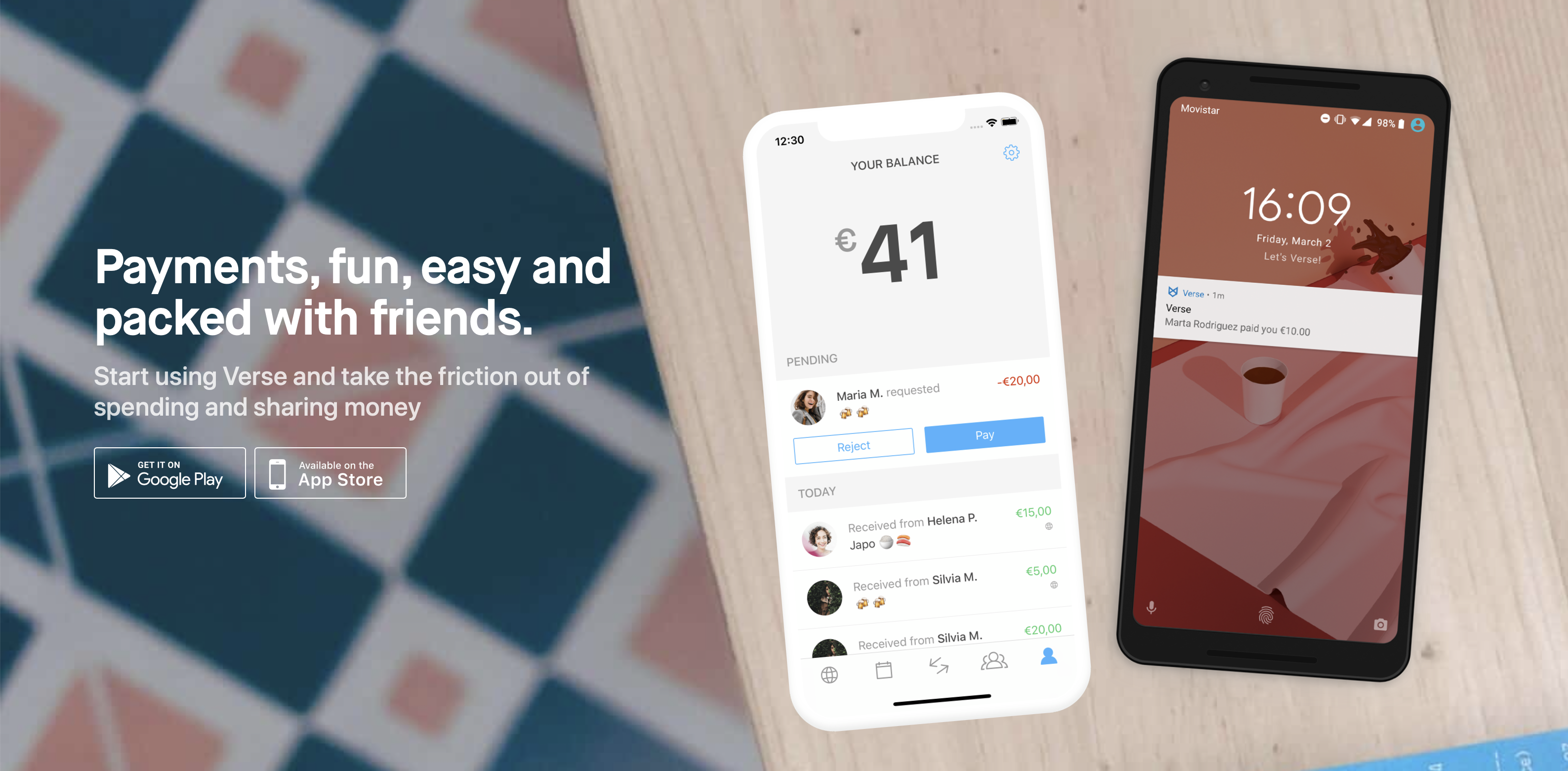

Square acquired Verse, a Spanish peer-to-peer payment app that works across Europe. Terms of the deal are undisclosed. According to Crunchbase, Verse had raised $37.6 million from Spark Capital, eVentures, Greycroft Partners and others.

Square has attracted a ton of users with Cash App, its peer-to-peer payment app that lets you easily send and receive money from your phone. But Cash App has only been available in the U.S. and the U.K.

Acquiring Verse seems like a good fit to expand Square’s presence in Europe. Verse’s team will join the Cash App division within Square.

There are many similarities between Cash App and Verse. Verse’s main feature is that it lets you send and receive money from a mobile app. Users don’t pay any fees and transfers occur in just a few seconds.

Verse users sign up with their phone numbers, which means that you can send money to other users as long as you have their phone numbers in your address book. If you don’t have enough money on your Verse account, the app can charge your debit card directly. And if you want to withdraw money from your Verse account, you can transfer your balance to your bank account.

You can also track group expenses from the app (like Splitwise), create money pots and organize events with a basic ticketing feature.

More recently, Verse launched a Visa debit card in Spain, which lets you spend money on your Verse account directly. You don’t pay any foreign exchange fees and you get two free ATM withdrawals per month. Verse uses Visa’s exchange rate.

While the startup hasn’t shared usage numbers for a while, according to App Annie, it is currently the No. 247 most downloaded app in the App Store in Spain across all categories. Peer-to-peer payment is a fragmented market. For instance, French startup Lydia has 3 million users in France.

“At this point, our main priority is enabling Verse to continue their successful growth in Europe. Verse will continue to operate as an independent business, working out of their offices with no immediate changes to their existing products, customers, or business operations,” Square wrote in the announcement.

The three most important words in this statement are “at this point.” Square doesn’t want to fix what isn’t broken. But I wouldn’t be surprised if Verse slowly evolves to become Cash App in Europe.

Image credits: Square

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Earlier this week, the popular free stock trading service Robinhood suffered downtime over a two-day period. The company, a well-funded unicorn taking on incumbents in its industry, failed to operate properly when the public markets were surging on Monday (bad) and falling on Tuesday (very bad).

Complaints flooded investing forums and social media. Images of Robinhood account screens featuring huge losses from the periods of downtime (or missed upside) weren’t hard to find. For Robinhood, it wasn’t its first misstep, but it was perhaps its worst. Mishandling the rollout of a high-yield savings function? Embarrassing, but hardly a serious wound. Some options oddness? Eh, not the worst.

Going down during surging volatility? Much worse. The company is already in the market with apologies and some give-aways to try to stem the negative news cycle. But what’s notable so far is that, while you might expect to see rival apps and services to Robinhood boom in the wake of its downtime, it instead appears that only select competitors to the popular company are seeing a jump in downloads this week. And given the insane market movements, it’s hard to pin some of their gains on Robinhood instead of, say, what stocks are themselves doing.

I’d expected by today to have some data in hand that painted a starker picture for Robinhood, given that the company’s recent missteps triggered a lot of negative press and user reaction. Let’s peek at what numbers can tell us, and try to figure out if there’s a lesson for consumer fintech and finservies companies while we’re at it.

Powered by WPeMatico