cards

Auto Added by WPeMatico

Auto Added by WPeMatico

At a time when more transactions than ever are happening online, payments behemoth Stripe is announcing three new features to continue expanding its reach.

The company today announced that it will now offer card issuing services directly to businesses to let them in turn make credit cards for customers tailored to specific purposes. Alongside that, it’s going to expand the number of accepted local, large card networks to cut down some of the steps it takes to make transactions in international markets. And finally, it’s launching a “revenue optimization” feature that essentially will use Stripe’s AI algorithms to reassess and approve more flagged transactions that might have otherwise been rejected in the past.

Together the three features underscore how Stripe is continuing to scale up with more services around its core payment processing APIs, a significant step in the wake of last week announcing its biggest fundraise to date: $600 million at a $36 billion valuation.

The rollouts of the new products are specifically coming at a time when Stripe has seen a big boost in usage among some (but not all) of its customers, said John Collison, Stripe’s co-founder and president, in an interview. Instacart, which is providing grocery delivery at a time when many are living under stay-at-home orders, has seen transactions up by 300% in recent weeks. Another newer customer, Zoom, is also seeing business boom. Amazon, Stripe’s behemoth customer that Collison would not discuss in any specific terms except to confirm it’s a close partner, is also seeing extremely heavy usage.

But other Stripe users — for example, many of its sea of small business users — are seeing huge pressures, while still others, faced with no physical business, are just starting to approach e-commerce in earnest for the first time. Stripe’s idea is that the launches today can help it address all of these scenarios.

“What we’re seeing in the COVID-19 world is that the impact is not minor,” said Collison. “Online has always been steadily taking a share from offline, but now many [projected] years of that migration are happening in the space of a few weeks.”

Stripe is among those companies that have been very mum about when they might go public — a state of affairs that only become more set in recent times, given how the IPO market has all but dried up in the midst of a health pandemic and economic slump. That has meant very little transparency about how Stripe is run, whether it’s profitable and how much revenues it makes.

But Stripe did note last week that it had some $2 billion in cash and cash reserves, which at least speaks to a level of financial stability. And another hint of efficiency might be gleaned from today’s product news.

While these three new services don’t necessarily sound like they are connected to each other, what they have underpinning them is that they are all building on top of tech and services that Stripe has previously rolled out. This speaks to how, even as the company now handles some 250 million API requests daily, it’s keeping some lean practices in place in terms of how it invests and maximises engineering and business development resources.

The card issuing service, for example, is built on a card service that Stripe launched last year. Originally aimed at businesses to provide their employees with credit cards — for example to better manage their own work-related expenses, or to make transactions on behalf of the business — now businesses can use the card issuing platform to build out aspects of its customer-facing services.

For example, Stripe noted that the first customer, Zipcar, will now be placing credit cards in each of its vehicles, which drivers can use to fuel up the vehicles (that is, the cards can only be used to buy gas). Another example Collison gave for how these could be implemented would be in a food delivery service, for example for a Postmates delivery person to use the card to pay for the meal that a customer has already paid Postmates to pick up and deliver to them.

Collison noted that while other startups like Marqeta have built big businesses around innovative card issuing services, “this is the first time it’s being issued on a self-serving basis,” meaning companies that want to use these cards can now set this up more quickly as a “programmatic card” experience, akin to self-serve, programmatic ads online.

It seems also to be good news for investors. “Stripe Issuing is a big step forward,” said Alex Rampell, general partner at Andreessen Horowitz, in a statement. “Not just for the millions of businesses running on Stripe, but for credit cards as a fundamental technology. Businesses can now use an API to create and issue cards exactly when and where they need them, and they can do it in a few clicks, not a few months. As investors, we’re excited by all the potential new companies and business models that will emerge as a result.”

Meanwhile, the revenue “optimization” engine that Stripe is rolling out is built on the same machine learning algorithms that it originally built for Radar, its fraud prevention tool that originally launched in 2016 and was extended to larger enterprises in 2018. This makes a lot of sense, since oftentimes the reason transactions get rejected is because of the suspicion of fraud. Why it’s taken four years to extend that to improve how transactions are approved or rejected is not entirely clear, but Stripe estimates that it could enable a further $2.5 billion in transactions annually.

One reason why the revenue optimization may have taken some time to roll out was because while Stripe offers a very seamless, simple API for users, it’s doing a lot of complex work behind the scenes knitting together a lot of very fragmented payment flows between card issuers, banks, businesses, customers and more in order to make transactions possible.

The third product announcement speaks to how Stripe is simplifying a bit more of that. Now, it’s able to provide direct links into six big card networks — Visa, Mastercard, American Express, Discover, JCB and China Union Pay, which effectively covers the major card networks in North and Latin America, Southeast Asia and Europe. Previously, Stripe would have had to work with third parties to integrate acceptance of all of these networks in different regions, which would have cut into Stripe’s own margins and also given it less flexibility in terms of how it could handle the transaction data.

Launching the revenue optimization by being able to apply machine learning to the transaction data is one example of where and how it might be able to apply more innovative processes from now on.

While Stripe is mainly focused today on how to serve its wider customer base and to just help business continue to keep running, Collison noted that the COVID-19 pandemic has had a measurable impact on Stripe beyond just boosts in business for some of its customers.

The whole company has been working remotely for weeks, including its development team, making for challenging times in building and rolling out services.

And Stripe, along with others, is also in the early stages of piloting how it will play a role in issuing small business loans as part of the CARES Act, he said.

In addition to that, he noted that there has been an emergence of more medical and telehealth services using Stripe for payments.

Before now, many of those use cases had been blocked by the banks, he said, for reasons of the industries themselves being strictly regulated in terms of what kind of data could get passed across networks and the sensitive nature of the businesses themselves. He said that a lot of that has started to get unblocked in the current climate, and “the growth of telemedicine has been off the charts.”

Powered by WPeMatico

Just ahead of the launch of the Apple Card, a startup that has its own take on modernizing the credit card industry, Zero, is announcing the close of its $20 million Series A. The new round of funding was led by New Enterprise Associates (NEA), and brings Zero’s total raised to date to $35 million, including both equity and debt funding.

Other investors in the round include SignalFire, Eniac Ventures, Nyca Partners and some unnamed school endowments. Zero had previously announced an $8.5 million raise in fall 2017, led by Eniac, and had raised $7 million in venture debt from Silicon Valley Bank.

Zero has a clever idea that targets millennials’ hesitance to sign up for credit cards.

Today, only 33% of millennials have a major credit card, a Bankrate survey found — largely because they’re wary of falling into the vicious debt cycle. Instead, this younger demographic often only carries a debit card. But that also means they’re missing out on credit card benefits — like points, rewards and cash back.

Zero’s idea is to offer a rewards credit card that works like debit.

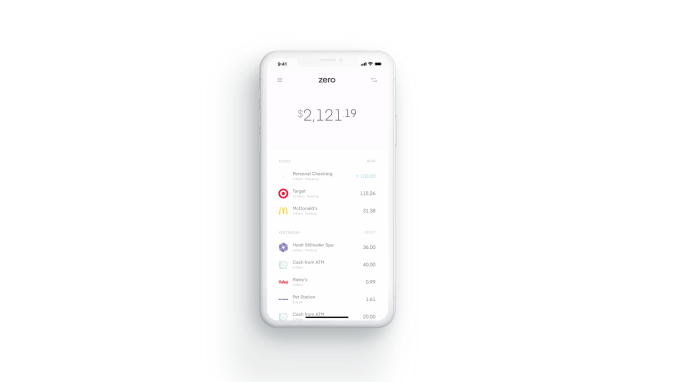

The Zerocard itself is a World Mastercard, so it earns credit card cash back. But unlike a traditional credit card, it’s combined with an FDIC-backed checking account called Zero Checking. That means Zerocard and Zero Checking work together in the app, allowing cardholders to see one net number they can spend from.

That way, they won’t make the mistake of accidentally going over budget, as is often the case with traditional credit cards, which then benefit from charging interest on the unpaid balance.

Zero co-founder and CEO Bryce Galen says he had always liked optimizing his personal finances, but didn’t see the value in overspending to chase rewards.

“People spend 10 to 15% more on average just because they’re putting it on a credit card, and not seeing where they stand all the time,” he says. “Spending 10 to 15% more to chase 1 to 2% in rewards doesn’t make sense.”

Plus, he adds, “half of all credit card points are never even redeemed.”

With Zerocard, the company does away with other credit card annoyances as well.

Zerocard doesn’t charge annual fees like many traditional credit cards do. And Zero Checking doesn’t add any additional ATM fees beyond what the ATM owner charges. It also does away with foreign transaction fees, minimum balance fees and overdraft fees — like many of today’s challenger banks.

Meanwhile, the Zero app is built with an eye toward what makes apps great.

Galen, who led product development for Zynga’s “Words with Friends” has experience in this department, while co-founder and COO Joel Washington previously co-founded car sales marketplace Shift. The executive team, combined, has backgrounds that include time at Affirm, Apple, Capital One, Dropbox, Google, Postmates, Silicon Valley Bank, Upgrade and Wells Fargo.

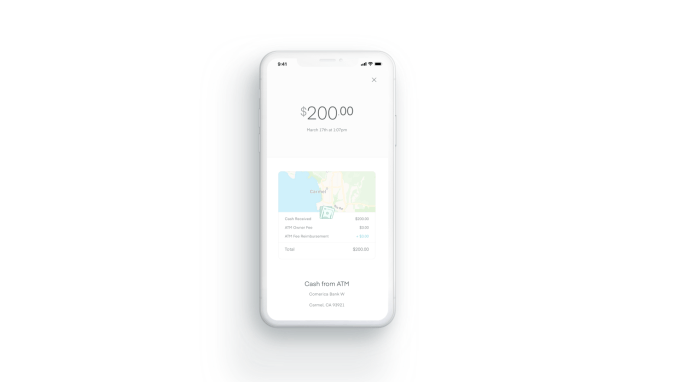

Overall, Zero’s design feels clean and simple, compared to the cluttered and dated apps from traditional banks. It has smart features, too, like a detailed transaction view that shows the vendor’s logo and location on a map to make it easier to recognize purchases.

“Zero creates an innovative debit-style experience, with an elegant design, and truly compelling rewards. It’s a fabulous banking experience,” said Hans Morris, managing partner of Nyca Partners and former president of Visa, Inc., in a statement. “Few people understand how complex it is to launch either a credit card or a checking account program, and I believe Zero is the first U.S. startup to launch both,” he said.

Zero launched in November 2018, but only to a small number of customers. Though officially open for business, it was functioning more like a public beta — though it didn’t call it that at the time. Meanwhile, its waitlist continued to grow.

Today, there are still 204,000 people waiting to be allowed in — something that Galen says is now going to happen.

“We haven’t launched to everyone on the waitlist yet, but we expect to within the next few weeks,” he says.

Another interesting twist on traditional credit cards is Zero’s path to card upgrades: it encourages but also rewards customers for telling their friends. By doing so, customers gain access to better-looking cards and higher cash-back percentages.

Zero customers start with a “Quartz” card offering 1% back on purchases. When a friend they refer joins, they receive a higher-level card called “Graphite” that offers 1.5% back. Two friends earns you the “Magnesium” card with 2% back and four friends gets you the “Carbon” card with 3% back. The Carbon card is also solid metal, capitalizing on the millennial trend of wanting their cards to look cool. And metal cards are in particular demand.

To receive the full cash-back rates, customers have to pay their balances in full by the due date, Zero says.

The company has partnered with Salt Lake City-based WebBank to issue the card, and deposits are held at Memphis-based Evolve Bank & Trust, an FDIC member. Zero makes money primarily on interchange and interest on deposits.

While some users may leave balances on the card that generate interest, Zero isn’t focused on that aspect of the business for revenue generation.

“Most companies in fintech today are launching undifferentiated debit cards as a feature or extension to their product for an additional engagement and monetization stream,” says Rick Yang, partner at NEA, as to why he invested.

“Zero is completely focused on their card programs and building a differentiated solution that actually provides a value proposition that resonates with consumers. We’ve also been fascinated by the growth of debit outpacing credit, and we think that our solution gives consumers the best of both worlds,” he adds.

Zero is currently iOS-only, but is working on an Android version that is expected to be ready in August.

Powered by WPeMatico

A company called Wildcard is today launching a browser for the mobile age, designed specifically with the support of the newer “card” format in mind. Cards are a new design trend which emerged within mobile applications as a way to better showcase content, including rich media like photos and video, on devices’ small screens. Wildcard is also announcing it has raised… Read More

A company called Wildcard is today launching a browser for the mobile age, designed specifically with the support of the newer “card” format in mind. Cards are a new design trend which emerged within mobile applications as a way to better showcase content, including rich media like photos and video, on devices’ small screens. Wildcard is also announcing it has raised… Read More

Powered by WPeMatico

Moonfrye, the family oriented startup best known as the company co-founded by former child star Soleil Moon Frye (aka TV’s “Punky Brewster”) has officially launched its second product, P.S. XO. Now available on the iPhone and iPad, the P.S. XO app allows consumers to take care of party planning activities directly from their mobile phone or tablet, including things like… Read More

Moonfrye, the family oriented startup best known as the company co-founded by former child star Soleil Moon Frye (aka TV’s “Punky Brewster”) has officially launched its second product, P.S. XO. Now available on the iPhone and iPad, the P.S. XO app allows consumers to take care of party planning activities directly from their mobile phone or tablet, including things like… Read More

Powered by WPeMatico