car ownership

Auto Added by WPeMatico

Auto Added by WPeMatico

Just months after raising $28 million, Jerry announced today that it has raised $75 million in a Series C round that values the company at $450 million.

Existing backer Goodwater Capital doubled down on its investment in Jerry, leading the “oversubscribed” round. Bow Capital, Kamerra, Highland Capital Partners and Park West Asset Management also participated in the financing, which brings Jerry’s total raised to $132 million since its 2017 inception. Goodwater Capital also led the startup’s Series B earlier this year. Jerry’s new valuation is about “4x” that of the company at its Series B round, according to co-founder and CEO Art Agrawal.

“What factored into the current valuation is our annual recurring revenue, growing customer base and total addressable market,” he told TechCrunch, declining to be more specific about ARR other than to say it is growing “at a very fast rate.” He also said the company “continues to meet and exceed growth and revenue targets” with its first product, a service for comparing and buying car insurance. At the time of the company’s last raise, Agrawal said Jerry saw its revenue surge by “10x” in 2020 compared to 2019.

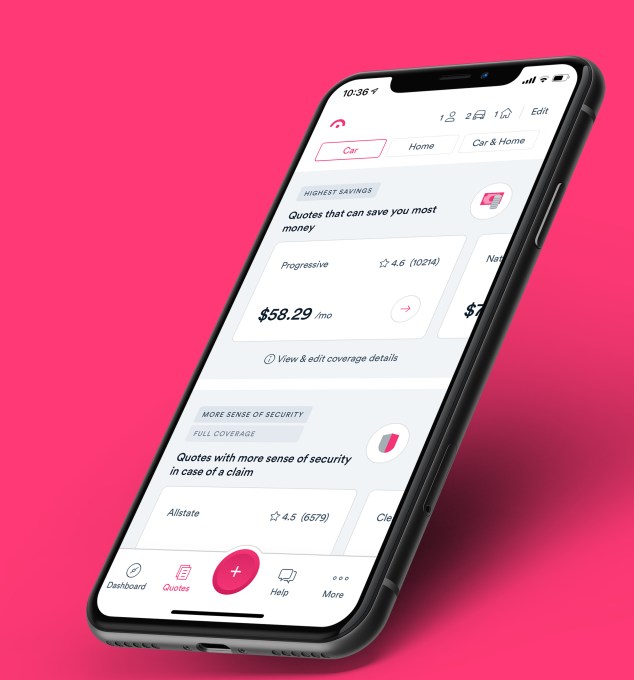

Jerry, which says it has evolved its model to a mobile-first car ownership “super app,” aims to save its customers time and money on car expenses. The Palo Alto-based startup launched its car insurance comparison service using artificial intelligence and machine learning in January 2019. It has quietly since amassed nearly 1 million customers across the United States as a licensed insurance broker.

“Today as a consumer, you have to go to multiple different places to deal with different things,” Agrawal said at the time of the company’s last raise. “Jerry is out to change that.”

The new funding round fuels the launch of the company’s “compare-and-buy” marketplaces in new verticals, including financing, repair, warranties, parking, maintenance and “additional money-saving services.” Although Jerry also offers a similar product for home insurance, its focus is on car ownership.

Image Credits: Jerry

“Access to reliable and affordable transportation is critical to economic empowerment,” said Rafi Syed, Jerry board member and general partner at Bow Capital, which also doubled down on its investment in the company. “Jerry is helping car owners make the most of every dollar they earn. While we see Jerry as an excellent technology investment showcasing the power of data in financial services, it’s also a high-performing investment in terms of the financial inclusion it supports.”

Goodwater Capital Partner Chi-Hua Chien said the firm’s recurring revenue model makes it stand out from lead generation-based car insurance comparison sites.

CEO Agrawal agrees, noting that Jerry’s high-performing annual recurring revenue model has made the company “attractive to investors” in addition to the fact that the startup “straddles” the auto, e-commerce, fintech and insurtech industries.

“We recognized those investment opportunities could drive our business faster and led to raising the round earlier than expected,” he told TechCrunch. “We’re eager to launch new categories to save customers time and money on auto expenses and the new investment shortens our time to market.”

Agrawal also believes Jerry is different from other auto-related marketplaces out there in that it aims to help consumers with various aspects of car ownership (from repair to maintenance to insurance to warranties), rather than just one. The company also believes it is set apart from competitors in that it doesn’t refer a consumer to an insurance carrier’s site so that they still have to do the work of signing up with them separately, for example. Rather, Jerry uses automation to give consumers customized quotes from more than 45 insurance carriers “in 45 seconds.” The consumers can then sign on to the new carrier via Jerry, which can then cancel former policies on their behalf.

Jerry makes recurring revenue from earning a percentage of the premium when a consumer purchases a policy on its site from carriers such as Progressive.

Powered by WPeMatico

Car shoppers now have several new options to avoid long-term debt and commitments. Automakers and startups alike are increasingly offering services that give buyers new opportunities and greater flexibility around owning and using vehicles.

In the first part of this feature, we explored the different startups attempting to change car buying. But not everyone wants to buy a car. After all, a vehicle traditionally loses its value at a dramatic rate.

Some startups are attempting to reinvent car ownership rather than car buying.

My favorite car blog Jalopnik said it best: “Cars Sales Could Be Heading Straight Into the Toilet.” Citing a Bloomberg report, the site explains automakers may have had the worst first half for new-vehicle retail sales since 2013. Car sales are tanking, but people still need cars.

Companies like Fair are offering new types of leases combining a traditional auto financing option with modern conveniences. Even car makers are looking at different ways to move vehicles from dealer lots.

Fair was founded in 2016 by an all-star team made up of automotive, retail and banking executives including Scott Painter, former founder and CEO of TrueCar.

Powered by WPeMatico

This week on Extra Crunch, I am exploring innovations in inclusive housing, looking at how 200+ companies are creating more access and affordability. Yesterday, I focused on startups trying to lower the costs of housing, from property acquisition to management and operations.

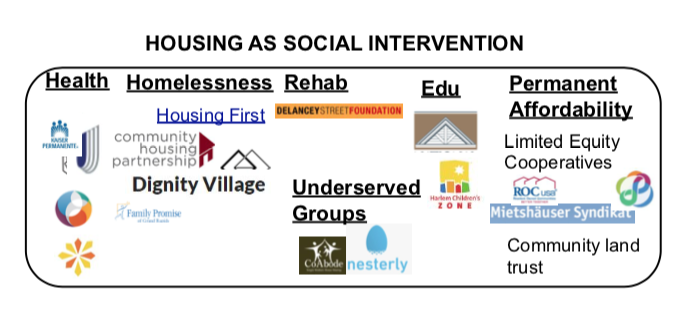

Today, I want to focus on innovations that improve housing inclusion more generally, such as efforts to pair housing with transit, small business creation, and mental rehabilitation. These include social impact-focused interventions, interventions that increase income and mobility, and ecosystem-builders in housing innovation.

Nonprofits and social enterprises lead many of these innovations. Yet because these areas are perceived to be not as lucrative, fewer technologists and other professionals have entered them. New business models and technologies have the opportunity to scale many of these alternative institutions — and create tremendous social value. Social impact is increasingly important to millennials, with brands like Patagonia having created loyal fan bases through purpose-driven leadership.

While each of these sections could be their own market map, this overall market map serves as an initial guide to each of these spaces.

These innovations address:

Powered by WPeMatico