capitalization table

Auto Added by WPeMatico

Auto Added by WPeMatico

There’s an old startup adage that goes: Cash is king. I’m not sure that is true anymore.

In today’s cash rich environment, options are more valuable than cash. Founders have many guides on how to raise money, but not enough has been written about how to protect your startup’s option pool. As a founder, recruiting talent is the most important factor for success. In turn, managing your option pool may be the most effective action you can take to ensure you can recruit and retain talent.

That said, managing your option pool is no easy task. However, with some foresight and planning, it’s possible to take advantage of certain tools at your disposal and avoid common pitfalls.

In this piece, I’ll cover:

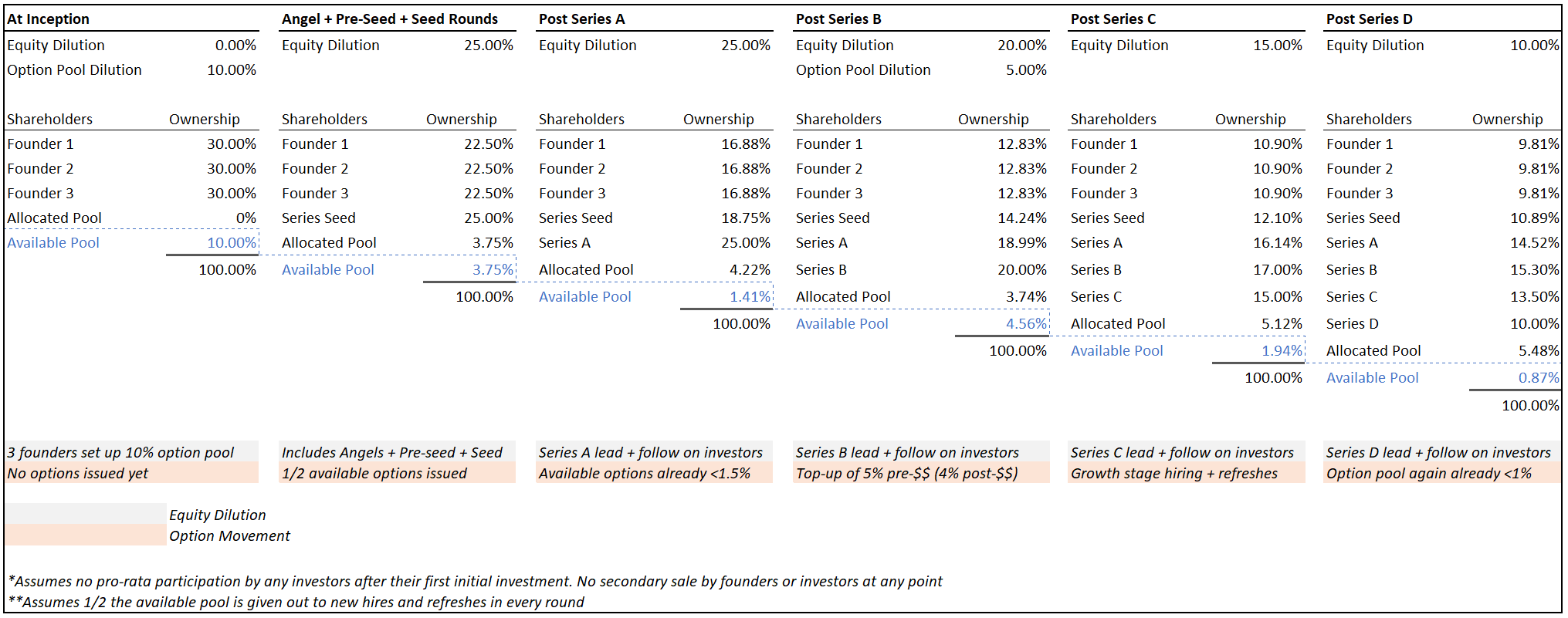

Let’s run through a quick case study that sets the stage before we dive deeper. In this example, there are three equal co-founders who decide to quit their jobs to become startup founders.

Since they know they need to hire talent, the trio gets going with a 10% option pool at inception. They then cobble together enough money across angel, pre-seed and seed rounds (with 25% cumulative dilution across those rounds) to achieve product-market fit (PMF). With PMF in the bag, they raise a Series A, which results in a further 25% dilution.

The easiest way to ensure you don’t run out of options too quickly is simply to start with a bigger pool.

After hiring a few C-suite executives, they are now running low on options. So at the Series B, the company does a 5% option pool top-up pre-money — in addition to giving up 20% in equity related to the new cash injection. When the Series C and D rounds come by with dilutions of 15% and 10%, the company has hit its stride and has an imminent IPO in the works. Success!

For simplicity, I will assume a few things that don’t normally happen but will make illustrating the math here a bit easier:

Obviously, every situation is unique and your mileage may vary. But this is a close enough proxy to what happens to a lot of startups in practice. Here is what the available option pool will look like over time across rounds:

Image Credits: Allen Miller

Note how quickly the pool thins out — especially early on. In the beginning, 10% sounds like a lot, but it’s hard to make the first few hires when you have nothing to show the world and no cash to pay salaries. In addition, early rounds don’t just dilute your equity as a founder, they dilute everyone’s — including your option pool (both allocated and unallocated). By the time the company raises its Series B, the available pool is already less than 1.5%.

Powered by WPeMatico

On Tuesday, the Open Cap Table Coalition announced its launch through an inaugural Medium post. The goal of this project is to standardize startup capitalization table data as well as make it far more accessible, transparent and portable.

For those unfamiliar with a cap table, it’s a list of who owns your company’s securities, which includes your company shares, options and more. A clear and simple cap table should quickly indicate who owns what and how much of it they own. For a variety of reasons (sometimes inexperience or bad advice) too many equity holders often find companies’ capitalization information to be opaque and not easily accessible.

This is particularly important for the small percentage of startups that survive in the long term, as growth makes for far more complicated cap tables.

A critical part of good startup hygiene is to always have a clean and updated cap table. Since there is no set format and cap tables are generally not out in the open, they are often siloed rather than collaborative.

Cap tables are near and dear to me as someone who has advised hundreds of startups over the past two decades as the founder of an accelerator, a venture partner and a senior adviser at a government-funded startup launchpad. I have been on the shareholder side of the equation as well and can assure you that pretty much nothing destroys trust between shareholders and startups quicker than poor communication, especially around issues such as the current status of the cap table.

A critical part of good startup hygiene is to always have a clean and updated cap table.

I really like the idea of a cap table being an open corporate record, because the value proposition to the companies is clear. From the time a startup creates a cap table, it’s prone to inaccuracy, friction and mistakes. What this means in practice is that startups may spend money on cap-table-related issues that they should be spending on other things. From a legal process perspective, the law firm that is brought in to help with these issues has to deal with tedious back-end work, so the legal time isn’t high value for either the startup or the law firm.

The value proposition for equity holders is equally clear. All equity holders have a general and legal interest in a company’s capitalization information. They have the right to this information, which they may need for a variety of reasons (including, if things ever get really bad, an aggrieved shareholder action). So making this information clear and easily accessible is a service to equity holders and can also encourage more investment, especially from less experienced investors.

When I imagine what this project could become in the next couple of years, I think back to late 2013, when Y Combinator announced the SAFE (simple agreement for future equity). I think the SAFE is a good analogy here, as no one knew what it was and people wondered if this was a nice-to-have rather than a must-have for startups. But the end result was a dramatic improvement in the early-stage capital-raising process.

While the coalition’s founders include Morgan Stanley’s Shareworks, LTSE Software and Carta, it’s also heavy on Big Law, with Cooley, Goodwin Procter, Wilson Sonsini Goodrich & Rosati, Orrick, Gunderson Dettmer, Latham & Watkins, and Fenwick & West rounding out the group of 10 founding members.

So what’s the real motivation of seven law firms, which together saw revenue of over $10 billion in 2020 to collaborate on an open cap table product for startups? Deal flow.

Big Law has been trying for a couple of decades to build relationships with startups at the stage where it makes no sense for a startup to be dealing with a massive and expensive law firm. Their efforts to build startup programs have often fallen short and received mixed reviews. They have also been far too heavy on the self-serve and too light on the “we’re going to give you our regular Big Law level of services at a small fraction of the costs just in case you make it big and can one day pay our regular fees.” So these firms are trying to separate themselves from the rest of the Big Law pack by building this entrepreneur-friendly tech.

The coalition has already produced its initial version of the open cap table. The real question is whether this is going to be a big deal, as the SAFE was, or whether it’s going to be a vanity solution in search of a real problem. My best guess is that if this coalition gets all the relationships right, doesn’t get greedy and understands that there is a social good component at play here, this could be, reasonably quickly, as impactful as the SAFE was.

Powered by WPeMatico

Founders start a company because they have an idea they want to bring to market. As their company gains traction and matures, the way in which they manage their business needs to evolve to enable strategic decisions for growth.

Developing and properly managing a capitalization table (cap table) is one such necessary business evolution. In this context, capitalization is the sum and itemization of all those who hold equity in the company or the right to receive equity in the future. Tracking these items through a central means helps illustrate the ownership stakes in the business and what securities the company has outstanding.

For a first-time founder, it can be overwhelming to develop a cap table and make all related decisions. However, with the right resources and adoption of best practices, founders can better manage, maintain and leverage their cap table to provide actionable business intelligence and management.

In many ways, the cap table is akin to the balance sheet in the sense that it represents the company’s position as of a certain point in time. The balance sheet shows the company’s assets and liabilities. The cap table shows the company’s ownership and accompanying economic and voting rights. The cap table includes factors such as shareholder information, ownership position, rights to purchase additional equity in the future, vesting schedules, voting percentages and purchase price. It takes all of the material information related to capitalization and summarizes it into a digestible format to help founders make executive-level decisions for soliciting stockholder approvals, issuing grants to new hires, raising additional rounds of financing, calculating liquidation waterfalls for a liquidity event, etc.

When it comes to how much founders need to own the cap table, think about it this way: Not every CFO needs to build out the financial statements. However, every CFO needs to have a high degree of confidence that their financial statements are accurate — with systems in place to ensure accuracy so they can spend their time using the financial statements to make strategic decisions. The same is true for founders’ involvement with their cap tables. Most companies rely on competent legal counsel to maintain their cap table and provide their executive team with actionable information in a digestible format.

Here are six best practices that help founders improve and maintain an effective cap table management process.

There are many different elements and formats of a cap table. Viewed as a spreadsheet, table or chart, the cap table can look different for every company at every stage of its growth. While the cap table tends to be simple in the beginning stages of the company, it will naturally evolve and become much more complicated as the company matures.

At a basic level, the cap table should list the equity stakes in a company, including common stock, preferred stock and stock options, and outline all of the ownership details for these securities. Other elements include transaction history and legal restrictions, such as sales, transfers, exercises of options, transfer restrictions and the conversion of debt to equity, among others.

The cap table should show the company’s overall capital structure at a glance, as well as detailed ownership information for each class and series of stock outstanding (see an example at the end of this article). Most importantly, it should always be accurate and up to date.

At its core, the cap table should be designed to help solve business issues for you. If you’re not using it to make decisions as an executive team, then it’s not serving a core purpose. The cap table is also critical to your legal team, so certain aspects may be primarily for their use, but if the company’s management doesn’t find the cap table helpful, that is a problem.

Creating good habits early on will serve you well as the business grows.

A good example of this is its role in the hiring process. Equity is a key consideration in talent recruitment and retention packages. Without an accurate cap table, you’ll find yourself in situations where you have to routinely ask yourself how many shares you can offer to a new hire, which can unnecessarily slow down the hiring process.

However, if you can use the cap table as a way to gain alignment on such matters, you can begin to use it to solve actual business problems. Rather than argue about which equity package to grant a new employee, your HR team can provide routine feedback on standardized equity packages to help improve or maintain competitive compensation.

When it comes to understanding how detailed your cap table needs to be, compare it once again to the financial statements. In the early days of the business, financial statements don’t necessarily feel as valuable as they do in later stages of growth. They aren’t as critical to the business — yet — because it’s not hard to recreate it whenever you need information to make a decision.

However, as the business matures and grows, it becomes more difficult to recreate the financial statement on an ad hoc basis, and virtually impossible to hold the information accurately in your mind. The same holds true with the cap table: In the beginning, you might be able to rattle it off the top of your head or have it documented simply in Excel, but as you grow, the information becomes more complex and you need better, automated systems in place. As with financial statements, creating good habits early on will serve you well as the business grows.

Using cap management software provides better capabilities and version control than spreadsheets to manage this process. Free software, such as captable.io and Carta are great starting places for early-stage founders. Carta also provides additional features to manage your more complex cap table. Because the cap table’s ultimate purpose is to enable the executive and legal teams to make informed decisions, safeguards on administrative access and version control are critical features to consider when choosing which tool or application to use.

As you model new rounds of financing and analyze the impact on stakeholders, cap table management becomes a significantly valuable activity. This is where your legal team or outside counsel becomes even more advantageous to you as a founder. Delegating cap table management to your lawyer can further help you stay on top of critical changes and minimize errors, while enabling you to focus more on building and scaling the business. Creating and maintaining an accurate cap table requires an ability to read, understand and translate legal documents into numbers and formulas. It is best to rely on the expertise of your legal team for this to ensure the most accurate business decisions are made.

Your cap table should be well-managed, well-understood and up-to-date.

We frequently see founding teams make seemingly small mistakes, such as adding an individual’s name to the cap table before an equity grant has legally been made. This may lead one to believe that more stock is outstanding than is technically the case and can create errors when calculating the number of shares to be granted to subsequent stockholders — or miss making the grant altogether, which can have unfortunate tax consequences for the stockholder and potential liability for the company. Order of operations is critical to legal workflows and it’s best to leave the day to day cap table maintenance to your legal team.

When it comes to how much cap table information you should disclose to your investors, there isn’t a right or wrong answer. Commonly, providing investors with a summary cap table is a fairly standard practice. That allows investors to calculate their ownership position for their internal tracking and audit purposes. More often than not, investors don’t receive an itemized list of every shareholder or investor in the company. While preferences differ on this point, many of our clients prefer that any company-related discussions are directed to the executive team so they can address and control messaging. Of course, in many instances investors will know which of their peers have also invested, but sharing detailed equity positions, contact information and individual employees’ equity stakes is less common.

In Carta, investors generally have portfolio views with visibility into all of their companies. They might send you a request for access to your cap table so they can add you to their portfolio. In this scenario, the summary cap table is the most common approach people default to for the investors. If an investor feels strongly about receiving detailed cap table viewing privileges, they can make their case to the company, which may consider the request on an individual basis.

Major investors will typically have specific, private contractual rights to get regular financial statements and cap table updates. They might even have a representative who is a board observer or board member, in which case, they will have access to the information they want, as agreed to in the equity financing paperwork.

Understanding the appropriate levels of information about your cap table to share with employees is another top consideration for founders. The key to this is determining the balance that you, as a founder, feel comfortable with in terms of employer transparency.

Some founders choose to be transparent about their cap tables and others opt not to disclose much and provide equity information on a need-to-know basis. The important part here is determining how you can best use the cap table to help your employees understand what they need to know.

For example, employees with equity want to understand what their payout is if the company sells. Regular communication or resources that provide employees with access to their holdings and options is a great approach to help motivate employees and improve talent retention, but can have unintended consequences.

For example, most companies will have their common stock valued after each round of financing. Some founders will want to share this number with the team so that people can understand that their stock is appreciating. That is very exciting and motivating — so long as everything is going well. However, if the stock’s appreciation is not meeting the team’s expectation (whether reasonable or not), then providing that information can significantly decrease morale. For this reason, the vast majority of companies choose not to disclose this information to the broader team.

Your cap table should be well-managed, well-understood and up-to-date. Fortunately, the management process doesn’t need to become just another headache: With the proper considerations, communication, resources and ownership, you can put the correct processes and legal team in place efficiently, and effectively manage your cap table so it continues to help you scale your business — rather than slow it down.

This table represents a simple cap table showing a hypothetical breakdown of seed preferred stock, Series A preferred stock, common stock and the available option pool.

All content presented herein is for informational purposes only. Nothing should be construed as legal advice. Transmission and receipt of this information is not intended to create, and does not constitute, an attorney-client relationship with Atrium LLP. There is no expectation of attorney-client privilege or confidentiality of anything you may communicate to us in this forum. Do not act upon any information presented without seeking professional counsel.

Powered by WPeMatico