california

Auto Added by WPeMatico

Auto Added by WPeMatico

In the United States, a 401(k) plan is an employer-sponsored defined-contribution pension account. However, with legacy institutional investing, most of these have at least some level of fossil fuel involvement, and, let’s face it, very few of us really know. Now a startup plans to change that.

California-based startup Sphere wants to get employees to ask their employers for investment options that are not invested in fossil fuels. To do that it’s offering financial products that make it easier — it says — for employers to offer fossil-free investment options in their 401(k) plans. This could be quite a big movement. Sphere says there are more than $35 trillion in assets in retirement savings in the U.S. as of Q1 2021.

It’s now raised a $2 million funding round led by climate tech-focused VC Pale Blue Dot. Also participating were climate-focused investors including Sundeep Ahuja of Climate Capital. Sphere is also a registered “Public Benefit Corporation,” allowing it to campaign in public about climate change.

Alex Wright-Gladstein, CEO and founder of Sphere said: “We are proud to be partnering with Pale Blue Dot on our mission to reverse climate change by making our money talk. Heidi, Hampus, and Joel have the experience and drive to help us make big changes on the short seven-year time scale that we have to limit warming to 1.5°C.” Wright-Gladstein has also teamed up with sustainable investing veteran Jason Britton of Reflection Asset Management and BITA custom indexes.

Wright-Gladstein said she learned the difficulty of offering fossil-free options in 401(k) plans when running her previous startup, Ayar Labs. She tried to offer a fossil-free option for employees, but found out it took would take three years to get a single fossil-free option in the plan.

Heidi Lindvall, general partner at Pale Blue Dot, said: “We are big believers in Sphere’s unique approach of raising awareness through a social movement while offering a range of low-cost products that address the structural issues in fossil-free 401(k) investing.”

Powered by WPeMatico

Back in December 2020 we covered the launch of a new kind of smartphone app-based search engine, Xayn.

“A search engine?!” I hear you say? Well, yes, because despite the convenience of modern search engines’ ability to tailor their search results to the individual, this user-tracking comes at the expense of privacy. This mass surveillance might be what improves Google’s search engine and Facebook’s ad targeting, to name just two examples, but it’s not very good for our privacy.

Internet users are admittedly able to switch to the U.S.-based DuckDuckGo, or perhaps France’s Qwant, but what they gain in privacy, they often lose in user experience and the relevance of search results, through this lack of tailoring.

What Berlin-based Xayn has come up with is personalized, but a privacy-safe web search on smartphones, which replaces the cloud-based AI employed by Google et al. with the innate AI in-built into modern smartphones. The result is that no data about you is uploaded to Xayn’s servers.

And this approach is not just for “privacy freaks”. Businesses that need search but don’t need Google’s dominant market position are increasingly attracted by this model.

And the evidence comes today with the news that Xayn has now raised almost $12 million in Series A funding led by the Japanese investors Global Brain and KDDI (a Japanese telecommunications operator), with participation from previous backers, including the Earlybird VC in Berlin. Xayn’s total financing now comes to more than $23 million.

It would appear that Xayn’s fusion of a search engine, a discovery feed and a mobile browser has appealed to these Asian market players, particularly because Xayn can be built into OEM devices.

The result of the investment is that Xayn will now also focus on the Asian market, starting with Japan, as well as Europe.

Leif-Nissen Lundbæk, co-founder and CEO of Xayn said: “We proved with Xayn that you can have it all: great results through personalization, privacy by design through advanced technology and a convenient user experience through clean design.”

He added: “In an industry in which selling data and delivering ads en masse are the norm, we choose to lead with privacy instead and put user satisfaction front and center.”

The funding comes as legislation such as the EU’s GDPR or California’s CCPA have both raised public awareness about personal data online.

Since its launch, Xayn says its app has been downloaded around 215,000 times worldwide, and a web version of its app is expected soon.

Over a call, Lundbæk expanded on the KDDI aspect of the fund-raising: “The partnership with KDDI means we will give users access to Xayn for free, while the corporate — such as KDDI — is the actual customer but gives our search engine away for free.”

The core features of Xayn include personalized search results; a personalized feed of the entire internet, which learns from their Tinder-like swipes, without collecting or sharing personal data; and an ad-free experience.

Naoki Kamimeada, partner at Global Brain Corporation said: “The market for private online search is growing, but Xayn is head and shoulders above everyone else because of the way they’re re-thinking how finding information online should be.”

Kazuhiko Chuman, head of KDDI Open Innovation Fund, said: “This European discovery engine uniquely combines efficient AI with a privacy-protecting focus and a smooth user experience. At KDDI, we’re constantly on the lookout for companies that can shape the future with their expertise and technology. That’s why it was a perfect match for us.”

In addition to the three co-founders (Leif-Nissen Lundbæk, chief executive officer, Professor Michael Huth, chief research officer, and Felix Hahmann, chief operations officer), Dr Daniel von Heyl will come on board as chief financial officer. Frank Pepermans will take on the role of chief technology officer and Michael Briggs will join as chief growth officer.

Powered by WPeMatico

One of the world’s biggest video game companies is reeling after a state discrimination and sexual harassment suit kicked off a firestorm of controversy within the company. California’s Department of Fair Employment and Housing sued Activision Blizzard last week, alleging that the company fostered a “breeding ground for harassment and discrimination against women.”

Following a combative response to the lawsuit from corporate leadership, a group of employees at Blizzard will stage a walkout, which is planned for Wednesday at 10 a.m. PDT. Most employees at Blizzard continue to work remotely, but walkout participants will gather tomorrow at the gates to the company’s Irvine campus.

“Given last week’s statements from Activision Blizzard, Inc. and their legal counsel regarding the DFEH lawsuit, as well as the subsequent internal statement from Frances Townsend, and the many stories shared by current and former employees of Activision Blizzard since, we believe that our values as employees are not being accurately reflected in the words and actions of our leadership,” the organizers wrote.

In the new statement, they called for supporters to donate to organizations including Black Girls Code, the anti-sexual-violence organization RAINN and Girls Who Code.

Activision Blizzard publishes some of the biggest titles in gaming, including the Call of Duty franchise, World of Warcraft, Starcraft and Overwatch. Blizzard came under Activision’s wing through a 2008 merger and the subsidiary operates out of its own Irvine, California headquarters.

In the suit, the state agency describes a “frat house” atmosphere in which women are not only not afforded the same opportunities as their male counterparts, but are routinely and openly harassed, sometimes by their superiors.

The company pushed back last week in a fiery statement, blaming “unaccountable state bureaucrats that are driving many of the state’s best businesses out of California” for pursuing the lawsuit. Activision Blizzard Executive Vice President Frances Townsend, former Homeland Security adviser to George W. Bush, echoed that aggressive messaging in an internal memo, slamming the lawsuit as a “distorted and untrue picture of our company.”

In an open letter published Monday, the walkout’s organizers condemned Blizzard’s response to the lawsuit’s allegations. “We believe these statements have damaged our ongoing quest for equality inside and outside of our industry,” they wrote. “ … These statements make it clear that our leadership is not putting our values first.”

More than 2,600 employees signed the letter, which demands an end to mandatory arbitration clauses that “protect abusers and limit the ability of victims to seek restitution,” improved representation and opportunities for women and nonbinary employees, salary transparency and a full audit of diversity, equity and inclusion at the company.

On Twitter, streamers, gamers, game devs and former employees expressed support for Wednesday’s walkout under the hashtag #ActiBlizzWalkout, with some calling for a blackout on Activision Blizzard games as a show of solidarity. Others called for streamers to use the walkout time slot to raise awareness about rampant sexual harassment and discrimination in gaming culture at large.

One Blizzard employee shared a photo of the company’s iconic statue depicting an axe-wielding orc, a central feature of its Irvine headquarters. Three plaques displaying corporate values that surround the statue had been covered with paper: “Lead responsibly,” “play nice, play fair,” and “every voice matters.”

Powered by WPeMatico

The need for more affordable housing has never been more urgent as a shortage in the U.S. housing market persists.

Startups attempting to help address the shortage in a variety of ways abound. One such startup, Abodu, has raised $20 million in a Series A funding round led by Norwest Venture Partners. Previous backer Initialized Capital also participated in the financing, along with Redfin CEO Glenn Kelman, former Stockton, California Mayor Michael Tubbs, GGV investor Hans Tung and Paradox Capital’s Kyle Tibbitts.

The California legislature changed laws in 2017 to make it easier to build Accessory Dwelling Units (ADUs). Then on January 1, 2020, the state of California made it dramatically easier to add extra housing units to single-family home sites. Cities and local agencies have to quickly approve or deny ADU projects within 60 days of receiving a permit application. The state also now prevents cities from imposing minimum lot size requirements, maximum ADU dimensions or off-street parking requirements.

Redwood City, California-based Abodu, which builds prefabricated ADUs, was founded in 2018 to serve as a “one-stop shop” for building an ADU, or as some describe it, a home in a backyard.

Image Credits: Co-founders John Geary and Eric McInerney / Abodu

What sets the company apart from others in the space, its execs claim, is that it not only builds and installs the units, it helps homeowners with the painful process of getting permits. Abodu says it pre-approves its structural engineering with California state-level agencies to ensure its units can be built statewide and works with local agencies to pre-approve its foundation systems to ensure projects can proceed on predictable timelines.

It also claims to offer a cheaper and faster process than if one were to build an ADU from start to finish. Specifically, the startup claims that one of its backyard homes can be installed in just 10% of the time it would take for a traditional ADU to be built.

Abodu has been active in the market, selling and building its ADUs since the fall of 2019. Since then, it has put “dozens and dozens” of units in the ground, and has multiple dozen units in production on top of that, according to CEO and co-founder John Geary. So far, it’s operating in the Bay Area, Los Angeles and Seattle. The company claims it can deliver an ADU in as little as 30 days in San Jose and Los Angeles thanks to the cities’ pre-approval process. In other cities in California and Washington, turnaround is “as little as 12 weeks.” But a standard bespoke project takes 4-5 months from start to finish, according to Geary.

The startup’s three products include a 340-square foot studio; a 500-square foot one bedroom, one bath, and a 610-square foot two bedroom unit. All have kitchens and living space.

Pricing starts at $190,000, but the average project cost across all sizes is around $230,000, Geary said, inclusive of permits and site work.

There are a variety of use cases for ADUs, the most popular of which is to house family and for rental income.

“During the pandemic, multigenerational living has been at an all-time high. There are acute family needs that people are trying to solve for,” Geary said. “In addition, folks are earning extra money by renting them out to members of the community such as teachers or fireman, a single person or younger couple.”

Next, Abodu is eyeing the San Diego market.

Earlier this week, we covered the recent raise of Mighty Buildings, another Bay Area-based startup building ADUs and other housing. The biggest difference between the two companies, according to Geary, is that Mighty Buildings is focused on innovation in construction with its 3D-printed method.

“We decided early on that we didn’t want to reinvent the wheel from the construction standpoint,” Geary said. “Instead, we looked at ‘how can we solve for speed and ease?’ ”

Abodu operates with an asset-light model, and doesn’t own any factories. Instead, it has built a network of factory “partners” across the Western U.S. that builds its units depending on how their capacities look at any given time.

Naturally, the company’s investors are bullish on the company’s business model.

Jeff Crowe, managing partner of Norwest Venture Partners, believes that Abodu’s “beautifully crafted units” are just one of the company’s selling points.

“John, Eric, and their team manage the end-to-end process of permitting, building, and installing on behalf of their customers,” he told TechCrunch. “And with the expedited permitting that Abodu has been granted in over two dozen cities, it has faster time-to-installation than other ADU market participants. The result has been very high levels of customer satisfaction and rapid growth.”

Former Stockton Mayor Tubbs said Abodu is tackling two of California’s most consequential issues: the statewide housing shortage and its impacts on racial and economic segregation in our neighborhoods.

“By making it fast and accessible for normal homeowners to build high-quality backyard housing units, Abodu’s success will mean integrating options for both renters and homeowners in the same neighborhoods, while supporting small landlords and property owners in building equity in their homes,” he wrote via email.

Powered by WPeMatico

AttackIQ, a cybersecurity startup that provides organizations with breach and attack simulation solutions, has raised $44 million in Series C funding as it looks to ramp up its international expansion.

The funding round was led by Atlantic Bridge, Saudi Aramco Energy Ventures (SAEV) and Gaingels, with existing vendors — including Index Ventures, Khosla Ventures, Salesforce Ventures and Telstra Ventures — also participating. The round brings the company’s total funding raised to date to $79 million.

AttackIQ was founded in 2013 and is based out of San Diego, California. It provides an automated validation platform that runs scenarios to detect any gaps in a company’s defenses, enabling organizations to test and measure the effectiveness of their security posture and receive guidance on how to fix what’s broken. Broadly, AttackIQ’s platform helps an organization’s security teams anticipate, prepare and hunt for threats that may impact their business, before hackers get there first.

Its Security Optimization Platform platform, which supports Windows, Linux and macOS across public, private and on-premises cloud environments, is based on the MITRE ATT&CK framework, a curated knowledge base of known adversary threats, tactics and techniques. This is used by a number of cybersecurity companies also building continuous validation services, including FireEye, Palo Alto Networks and Cymulate.

AttackIQ says this latest round of funding, which comes more than two years after its last, arrives at a “dynamic time” for the company. Not only has cybersecurity become more of a priority for organizations as a result of a major uptick in both ransomware and supply-chain attacks, the company also recently accelerated its international expansion efforts through a partnership with technology distributor Westcon.

The startup says it’s planning to use these new funds to further expand internationally through its newfound partnership with Atlantic Bridge, which will also see Kevin Dillon, the company’s co-founder and managing director, join the AttackIQ board of directors.

“AttackIQ has established itself as a category leader with a formidable enterprise customer base that includes four of the Fortune 20,” said Dillon. “We believe deeply in the company’s vision and potential to become the next billion-dollar cybersecurity software company and look forward to helping the company turn early traction in Europe and the Middle East into robust, long-term expansion.”

Brett Galloway, CEO of AttackIQ, said the round “reaffirms the strength” of its platform.

As well as enabling organizations to review the robustness of their security defenses, the startup also runs the AttackIQ Academy, which provides free entry-level and advanced cybersecurity training. It has accumulated 17,200 registered students to date across 176 countries.

Powered by WPeMatico

Briq, which has developed a fintech platform used by the construction industry, has raised $30 million in a Series B funding round led by Tiger Global Management.

The financing is among the largest Series B fundraises by a construction software startup, according to the company, and brings Briq’s total raised to $43 million since its January 2018 inception. Existing backers Eniac Ventures and Blackhorn Ventures also participated in the round.

Briq CEO and co-founder Bassem Hamdy is a former executive at construction tech giant Procore (which recently went public and has a market cap of $10.4 billion) and Canadian software giant CMiC. Wall Street veteran Ron Goldshmidt is co-founder and COO.

Briq describes its offering as a financial planning and workflow automation platform that “drastically reduces” the time to run critical financial processes, while increasing the accuracy of forecasts and financial plans.

Briq has developed a toolbox of proprietary technology that it says allows it to extract and manipulate financial data without the use of APIs. It also has developed construction-specific data models that allows it to build out projections and create models of how much a project might cost, and how much could conceivably be made. Currently, Briq manages or forecasts about $30 billion in construction volume.

Specifically, Briq has two main offerings: Briq’s Corporate Performance Management (CPM) platform, which models financial outcomes at the project and corporate level, and BriqCash, a construction-specific banking platform for managing invoices and payments.

Put simply, Briq aims to allow contractors “to go from plan to pay” in one platform with the goal of solving the age-old problem of construction projects (very often) going over budget. Its longer-term, ambitious mission is to “manage 80% of the money workflows in construction within 10 years.”

The company’s strategy, so far, seems to be working.

From January 2020 to today, ARR has climbed by 200%, according to Hamdy. Briq currently has about 100 employees, compared to 35 a year ago.

Briq has 150 customers, and serves general and specialty contractors from $10 million to $1 billion in revenue. They include Cafco Construction Management, WestCor Companies and Choate Construction and Harper Construction. The company is currently focused on contractors in North America but does have long-term plans to address larger international markets, Hamdy told TechCrunch.

Hamdy came up with the idea for Santa Barbara, California-based Briq after realizing the vast amount of inefficiencies on the financial side of the construction industry. His goal was to do for construction financials what Procore did to document management, and PlanGrid to construction drawing. He started Briq with his own cash, amassed through secondary sales as Procore climbed the ranks of startups to become a construction industry unicorn.

Briq CEO and co-founder Bassem Hamdy. Image Credits: Briq

“I wanted to figure out how to bring the best of fintech into a construction industry that really guesses every month what the financial outcomes are for projects,” Hamdy told me at the time of the company’s last raise — a $10 million Series A led by Blackhorn Ventures announced in May of 2020. “Getting a handle on financial outcomes is really hard. The vast majority of the time, the forecasted cost to completion is plain wrong. By a lot.”

In fact, according to McKinsey, an astounding 80% of projects run over budget, resulting in significant waste and profit loss.

So at the end of a project, contractors often find themselves having doled out more money and resources than originally planned. This can lead to negative cash flow and profit loss. Briq’s platform aims to help contractors identify outliers, and which projects are more at risk.

Throughout the COVID-19 pandemic, Briq has proven to be “extremely valuable” to contractors, Hamdy said.

“In an industry where margins are so thin, we have given contractors the ability to truly understand where they stand on cash, profit and labor,” he added.

Powered by WPeMatico

As an entrepreneur, you started your business to create value, both in what you deliver to your customers and what you build for yourself. You have a lot going on, but if building personal wealth matters to you, the assets you’re creating deserve your attention.

You can implement numerous advanced planning strategies to minimize capital gains tax, reduce future estate tax and increase asset protection from creditors and lawsuits. Capital gains tax can reduce your gains by up to 35%, and estate taxes can cost up to 50% on assets you leave to your heirs. Careful planning can minimize your exposure and actually save you millions.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle. Different strategies should be used at different times and for different reasons. The following are a few key considerations when determining what, if any, advanced strategies you might consider:

Some additional items to consider include issues related to qualified small business stock (QSBS), gift and estate taxes, state and local income taxes, liquidity, asset protection, and whether you and your family will retain control and manage the assets over time.

Smart founders and early employees should closely examine their equity ownership, even in the early stages of their company’s life cycle.

Here are some advanced equity planning strategies that you can implement at different stages of your company life cycle to reduce tax and optimize wealth for you and your family.

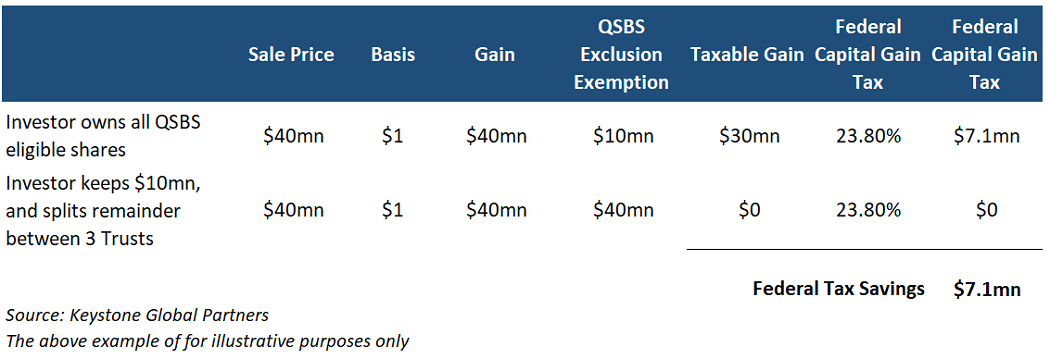

QSBS allows you to exclude tax on $10 million of capital gains (tax of up to 35%) upon an exit/sale. This is a benefit every individual and some trusts have. There is significant opportunity to multiply the QSBS tax exclusion well beyond $10 million.

The founder can gift QSBS eligible stock to an irrevocable nongrantor trust, let’s say for the benefit of a child, so that the trust will qualify for its own $10 million exclusion. The founder owning the shares would be the grantor in this case. Typically, these trusts are set up for children or unborn children. It is important to note that the founder/grantor will have to gift the shares to accomplish this, because gifted shares will retain the QSBS eligibility. If the shares are sold into the trust, the shares lose QSBS status.

Image Credits: Peyton Carr

In addition to the savings on federal taxes, founders may also save on state taxes. State tax can be avoided if the trust is structured properly and set up in a tax-exempt state like Delaware or Nevada. Otherwise, even if the trust is subject to state tax, some states, like New York, conform and follow the federal tax treatment of the QSBS rules, while others, like California, do not. For example, if you are a New York state resident, you will also avoid the 8.82% state tax, which amounts to another $2.6 million in tax savings if applied to the example above.

This brings the total tax savings to almost $10 million, which is material in the context of a $40 million gain. Notably, California does not conform, but California residents can still capture the state tax savings if their trust is structured properly and in a state like Delaware or Nevada.

Currently, each person has a limited lifetime gift tax exemption, and any gifted amount beyond this will generate up to a 40% gift tax that has to be paid. Because of this, there is a trade-off between gifting the shares early while the company valuation is low and using less of your gift tax exemption versus gifting the shares later and using more of the lifetime gift exemption.

The reason to wait is that it takes time, energy and money to set up these trusts, so ideally, you are using your lifetime gift exemption and trust creation costs to capture a benefit that will be realized. However, not every company has a successful exit, so it is sometimes better to wait until there is a certain degree of confidence that the benefit will be realized.

One way for the founder to plan for future generations while minimizing estate taxes and high state taxes is through a parent-seeded trust. This trust is created by the founder’s parents, with the founder as the beneficiary. Then the founder can sell the shares to this trust — it doesn’t involve the use of any lifetime gift exemption and eliminates any gift tax, but it also disqualifies the ability to claim QSBS.

The benefit is that all the future appreciation of the asset is transferred out of the founder’s and the parent’s estate and is not subject to potential estate taxes in the future. The trust can be located in a tax-exempt state such as Delaware or Nevada to also eliminate home state-level taxes. This can translate up to 10% in state-level tax savings. The trustee, an individual selected by the founder, can make distributions to the founder as a beneficiary if desired.

Further, this trust can be used for the benefit of multiple generations. Distributions can be made at the discretion of the trustee, and this skips the estate tax liability as assets are passed from generation to generation.

This strategy enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, specifically without using any lifetime gift exemption or being subject to gift tax. It’s particularly helpful when an individual has used up all their lifetime gift tax exemption. This is a powerful strategy for very large “unicorn” positions to reduce a founder’s future gift/estate tax exposure.

For the GRAT, the founder (grantor) transfers assets into the GRAT and gets back a stream of annuity payments. The IRS 7520 rate, currently very low, is a factor in calculating these annuity payments. If the assets transferred into the trust grow faster than the IRS 7520 rate, there will be an excess remainder amount in GRAT after all the annuity payments are paid back to the founder (grantor).

This remainder amount will be excluded from the founder’s estate and can transfer to beneficiaries or remain in the trust estate tax-free. Over time, this remainder amount can be multiples of the initial contributed value. If you have company stock that you expect will pop in value, it can be very beneficial to transfer those shares into a GRAT and have the pop occur inside the trust.

This way, you can transfer all the upside gift and estate tax-free out of your estate and to your beneficiaries. Additionally, because this trust is structured as a grantor trust, the founder can pay the taxes incurred by the trust, making the strategy even more powerful.

One thing to note is that the grantor must survive the GRAT’s term for the strategy to work. If the grantor dies before the end of the term, the strategy unravels and some or all the assets remain in his estate as if the strategy never existed.

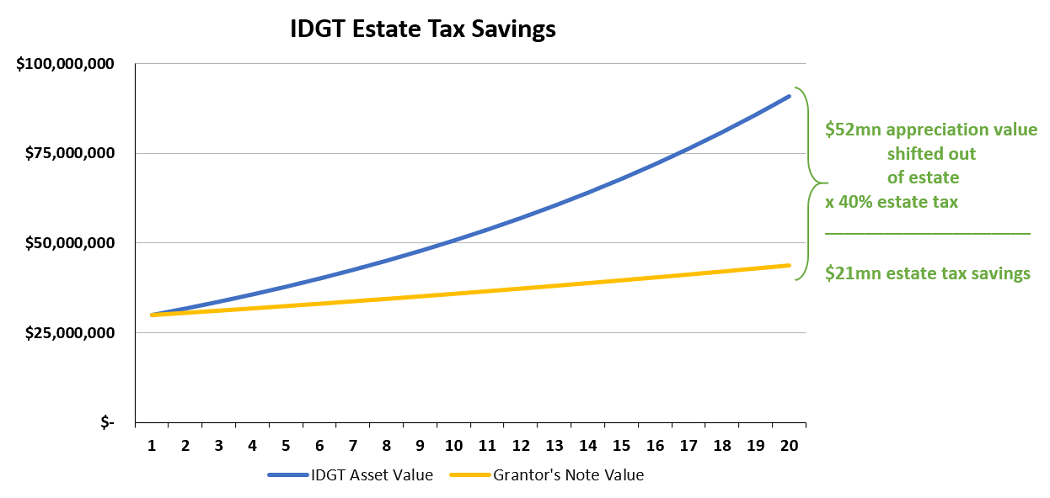

This is similar to the GRAT in that it also enables the founder to minimize their estate tax exposure by transferring wealth outside of their estate, but has some key differences. The grantor must “seed” the trust by gifting 10% of the asset value intended to be transferred, so this approach requires the use of some lifetime gift exemption or gift tax.

The remaining 90% of the value to be transferred is sold to the trust in exchange for a promissory note. This sale is not taxable for income tax or QSBS purposes. The main benefits are that instead of receiving annuity payments back, which requires larger payments, the grantor transfers assets into the trust and can receive an interest-only note. The payments received are far lower because it is interest-only (rather than an annuity).

Image Credits: Peyton Carr

Another key distinction is that the IDGT strategy has more flexibility than the GRAT and can be generation-skipping.

If the goal is to avoid generation-skipping transfer tax (GSTT), the IDGT is superior to the GRAT, because assets are measured for GSTT purposes when they are contributed to the trust prior to appreciation rather than being measured at the end of the term for a GRAT after the assets have appreciated.

Depending on a founder’s situation and goals, we may use some combination of the above strategies or others altogether. Many of these strategies are most effective when planning in advance; waiting until after the fact will limit the benefits you can extract.

When considering strategies for protecting wealth and minimizing taxes as it relates to your company stock, there’s a lot to take into account — the above is only a summary. We recommend you seek proper counsel and choose wealth transfer and tax savings strategies based on your unique situation and individual appetite for complexity.

Powered by WPeMatico

As the oldest of 12 children, Bunim Laskin spent much of his teen years looking for ways to help keep his siblings entertained. Noticing that a neighbor’s pool was often empty, Laskin reached out to ask if his family could use her pool. To make it worth her while, he suggested that they could help cover her expenses for maintaining the pool.

Soon after, five other families had made the same arrangement with her and the pool owner had six families covering 25% of her expenses. This meant that the neighbor was actually making money off her pool. The arrangement sparked a business idea in Laskin’s mind. At the age of 20, he founded Swimply, a marketplace for homeowners to rent out their underutilized pools to local swimmers, with Asher Weinberger.

The Cedarhurst, New York-based company launched a beta in 2018, starting with four pools in the New Jersey area.

“We used Google Earth to find houses, and then knocked on 80 doors with a pool,” CEO Laskin recalls. “We got to 100 pools organically. Word of mouth really helped us grow.” The site was pretty bare bones, he admits, with potential customers only able to view photos of the pools and connect with the pool owner by phone.

That year, Swimply did around 400 reservations and raised $1.2 million from friends and family.

In 2019, Swimply launched what he describes as a “proper” website and app with an automated platform. It grew “four to five times” that year, again mostly organically. In an episode that aired in March 2020, the company appeared on Shark Tank but went home without a deal.

Then the COVID-19 pandemic hit. Swimply, Laskin said, pivoted right into the pandemic.

“We were the perfect solution for people when the world was falling on its head,” he said. The company restructured its offering to ensure that pool owners did not have to interact with guests. “It was the perfect, contact-free, self-serve experience to hang out and be with people you quarantined with.”

The CDC then came out to say that it was safe to swim because chlorine could help kill the virus, and that proved to be a big boon to its business.

“On one end, it was a way for people to have a normal day and on the other, it helped give owners a way to earn an income, at a time when many people were being affected financially,” Laskin told TechCrunch.

Business took off in 2020 with revenue growing 4,000% and now Swimply is announcing a $10 million Series A round. Norwest Venture Partners led the financing, which also included participation from Trust Ventures and a number of angel investors such as Poshmark founder and CEO Manish Chandra; Rob Chesnut, former general counsel and chief ethics officer at Airbnb; Ancestry.com CEO Deborah Liu and Michael Curtis.

Swimply is now operating in a total of 125 U.S. markets, two markets in Canada and five markets in Australia. It plans to use its new capital in part to expand into new markets and toward product development.

Image Credits: Swimply

The way it works is pretty straightforward. Swimply simply connects homeowners that have underutilized backyard spaces and pools with those seeking a way to gather, cool off or exercise, for example. People or families can rent pools by the hour, ranging in price from $15 to $60 per hour (at an average of $45/hour) depending on the amenities. New markets that Swimply has recently expanded to include Portland, Oregon; Raleigh, North Carolina and the California cities of Oakland, San Luis Obispo and Los Gatos.

“The shifting mindset from younger generations about ownership is a huge contributor to increased growth of the Swimply marketplace,” said co-founder Weinberger, who serves as Swimply’s COO. “Swimming is the third most popular activity for adults and number one for children, and yet no other company has tackled the aquatic space to make swimming more affordable and accessible…until now.”

While the company declined to provide hard revenue figures, Laskin said Swimply was seeing “seven digits a month in revenue” and 15,000 to 20,000 reservations a month. Families represent the most popular reservation.

“People can book and pay through our platform, and only 20% of hosts ever meet their guests,” Laskin said. “We’re enabling a new kind of consumer behavior with what we’re doing.”

The company is planning to use its new capital to also rebuild much of its tech infrastructure and boost its customer support team to be more “readily available.”

It is also now offering a complimentary up to $1 million worth of insurance per booking for liability as well as $10,000 for property damage.

Swimply has a little over 20 employees, up 10 times from two people in December of 2020. It plans to double that number over the next few months.

The company’s model has proven quite lucrative for some owners, according to Laskin.

“Last year, there were some owners who earned $10,000 a month. One owner in Denver earned $50,000 last year and he had signed up toward the end of the summer. He should make over $100,000 this year,” Lasken projects.

Its only criteria is that owners offer a clean pool. Eighty-five percent of hosts offer restrooms as well. If they don’t, they are limited to one-hour reservations with a max of five guests. Swimply has also partnered with local pool companies, and if they pay one of its owners a visit and certify that pool, that owner gets a badge on the site “so guests get an additional level of security,” Laskin said.

Ed Yip of Norwest Venture Partners admits that when he first heard of the concept of Swimply, he “didn’t know what to make of it.”

But the more he heard about it, the more excited he got.

“This is the Holy Grail for a consumer investor. We’re not changing consumer behavior, but rather [we] productize the experience and make it safer and easier on both sides,” Yip told TechCrunch.

What also gets the investor excited is the potential for Swimply beyond just swimming pools in the future.

“We’re seeing a ton of demand from hosts wanting to list hot tubs and tennis courts, for example,” Yip said. “So this can turn into a marketplace for shared outdoor resources and that’s a huge market opportunity that adds value on both sides.”

Indeed, the concept of monetizing underutilized space is a growing concept. Earlier this year, we reported on Neighbor, which operates a self-storage marketplace, raising $53 million in a Series B round of funding. Neighbor’s unique model aims to repurpose under-utilized or vacant space — whether it be a person’s basement or the empty floor of an office building — and turn it into storage.

Powered by WPeMatico

Smartphones will be included in the scope of a planned “security by design” U.K. law aimed at beefing up the security of consumer devices, the government said today.

It made the announcement in its response to a consultation on legislative plans aimed at tackling some of the most lax security practices long-associated with the Internet of Things (IoT).

The government introduced a security code of practice for IoT device manufacturers back in 2018 — but the forthcoming legislation is intended to build on that with a set of legally binding requirements.

A draft law was aired by ministers in 2019 — with the government focused on IoT devices, such as webcams and baby monitors, which have often been associated with the most egregious device security practices.

Its plan now is for virtually all smart devices to be covered by legally binding security requirements, with the government pointing to research from consumer group “Which?” that found that a third of people kept their last phone for four years, while some brands only offer security updates for just over two years.

The forthcoming legislation will require smartphone and device makers like Apple and Samsung to inform customers of the duration of time for which a device will receive software updates at the point of sale.

It will also ban manufacturers from using universal default passwords (such as “password” or “admin”), which are often preset in a device’s factory settings and easily guessable — making them meaningless in security terms.

California already passed legislation banning such passwords in 2018 with the law coming into force last year.

Under the incoming U.K. law, manufacturers will additionally be required to provide a public point of contact to make it simpler for anyone to report a vulnerability.

The government said it will introduce legislation as soon as parliamentary time allows.

Commenting in a statement, digital infrastructure minister Matt Warman added: “Our phones and smart devices can be a gold mine for hackers looking to steal data, yet a great number still run older software with holes in their security systems.

“We are changing the law to ensure shoppers know how long products are supported with vital security updates before they buy and are making devices harder to break into by banning easily guessable default passwords.

“The reforms, backed by tech associations around the world, will torpedo the efforts of online criminals and boost our mission to build back safer from the pandemic.”

A DCMS spokesman confirmed that laptops, PCs and tablets with no cellular connection will not be covered by the law, nor will secondhand products. Although he added that the intention is for the scope to be adaptive, to ensure the law can keep pace with new threats that may emerge around devices.

Powered by WPeMatico

The coming wave of electric vehicles will require more than thousands of charging stations. In addition to being installed, they also need to work — and today, that isn’t happening.

If a station doesn’t send out an error or a driver doesn’t report it, network providers might never know there’s even a problem. Kameale C. Terry, who co-founded ChargerHelp!, an on-demand repair app for electric vehicle charging stations, has seen these issues firsthand.

One customer assumed that poor usage rates at a particular station was due to a lack of EVs in the area, Terry recalled in a recent interview. That wasn’t the problem.

“There was an abandoned vehicle parked there and the station was surrounded by mud,” said Terry who is CEO and co-founded the company with Evette Ellis.

Demand for ChargerHelp’s service has attracted customers and investors. The company said it has raised $2.75 million from investors Trucks VC, Kapor Capital, JFF, Energy Impact Partners and The Fund. This round values the startup, which was founded in January 2020, at $11 million post-money.

The funds will be used to build out its platform, hire beyond its 27-person workforce and expand its service area. ChargerHelp works directly with the charging manufacturers and network providers.

“Today when a station goes down there’s really no troubleshooting guidance,” said Terry, noting that it takes getting someone out into the field to run diagnostics on the station to understand the specific problem. After an onsite visit, a technician then typically shares data with the customer, and then steps are taken to order the correct and specific part — a practice that often doesn’t happen today.

While ChargerHelp is couched as an on-demand repair app, it is also acts as a preventative maintenance service for its customers.

The idea for ChargerHelp came from Terry’s experience working at EV Connect, where she held a number of roles, including head of customer experience and director of programs. During her time there, she worked with 12 manufacturers, which gave her knowledge into inner workings and common problems with the chargers.

It was here that she spotted a gap in the EV charging market.

“When the stations went down we really couldn’t get anyone on site because most of the issues were communication issues, vandalism, firmware updates or swapping out a part — all things that were not electrical,” Terry said.

And yet, the general practice was to use electrical contractors to fix issues at the charging stations. Terry said it could take as long as 30 days to get an electrical contractor on site to repair these non-electrical problems.

Terry often took matters in her own hands if issues arose with stations located in Los Angeles, where she is based.

“If there was a part that needed to be swapped out, I would just go do it myself,” Terry said, adding she didn’t have a background in software or repairs. “I thought, if I can figure this stuff out, then anyone can.”

In January 2020, Terry quit her job and started ChargerHelp. The newly minted founder joined the Los Angeles Cleantech Incubator, where she developed a curriculum to teach people how to repair EV chargers. It was here that she met Ellis, a career coach at LACI who also worked at the Long Beach Job Corp Center. Ellis is now the chief workforce officer at ChargerHelp.

Since then, Terry and Ellis were accepted into Elemental Excelerator’s startup incubator, raised about $400,000 in grant money, launched a pilot program with Tellus Power focused on preventative maintenance and landed contracts with EV charging networks and manufacturers such as EV Connect, ABB and SparkCharge. Terry said they have also hired their core team of seven employees and trained their first tranche of technicians.

Image Credits: ChargerHelp

ChargerHelp takes a workforce-development approach to finding employees. The company only hires in cohorts, or groups, of employees.

The company received more than 1,600 applications in its first recruitment round for electric vehicle service technicians, according to Terry. Of those, 20 were picked to go through training and 18 were ultimately hired to service contracts across six states, including California, Oregon, Washington, New York and Texas. Everyone picked to go through training is paid a stipend and earn two safety licenses.

The startup will begin its second recruitment round in April. All workers are full-time with a guaranteed wage of $30 an hour and are being given shares in the startup, Terry said. The company is working directly with workforce development centers in the areas where ChargerHelp needs technicians.

Powered by WPeMatico