business

Auto Added by WPeMatico

Auto Added by WPeMatico

NetEase, China’s second-biggest online games publisher with a growing ecommerce segment, is laying off a significant number of its employees, adding to a list of Chinese tech giants that have shed staff following the Lunar New Year.

A NetEase employee who was recently let go confirmed with TechCrunch that the company had fired a large number of people spanning multiple departments, including ecommerce, education, agriculture (yes, founder and executive officer Ding Lei has a thing for organic farming) and public relations, although downsizing at Yanxuan, its ecommerce brand that sells private-label goods online and offline, had started before the Lunar New Year holiday.

Multiple Chinese media outlets covered the layoff on Wednesday. According to a report from Caijing Magazine, Yanxuan fired 30-40 percent of its staff; the agricultural brand Weiyang got a 50 percent cut; the education unit downsized from 300 to 200 employees; and 40 percent of NetEase’s public relations staff was gone.

A spokesperson from NetEase evaded TechCrunch’s questions about the layoff but said the company is “indeed undergoing a structural optimization to narrow its focus.” The goal, according to the person, is to “boost innovation and organizational efficiency so NetEase can fully play to its own strengths and adapt to market competition in the longer term.”

NetEase CEO Ding Lei pictured picking Longjing tea leaves in Hangzhou. Photo: NetEase Yanxuan via Weibo

Oddly, ecommerce and education appear to be some of NetEase’s brighter spots. The company singled them out alongside music streaming during its latest earnings call as the three sectors that saw “strong profit growth potential” and “will be the focus of [the company’s] next phase of strategic growth.” The staff cuts, then, may represent an urgency to tighten the purse strings for even NetEase’s rosiest businesses.

The shakeup fits into market speculation about company staff cuts to save costs as China copes with a weakening domestic economy. JD.com, a rival to Alibaba, is firing 10 percent of its senior management to cut costs, Caixin reported last week. Ride-hailing giant Didi Chuxing plans to let go 15 percent of its staff this year as part of a reorganization to boost internal efficiency, though it’s adding new members to focus on more promising segments.

Alibaba took an unexpected turn, announcing last week that it will continue to hire new talent in 2019. “We are poised to provide more resources to our platforms to help businesses navigate current environment and create more job opportunities overall,” the firm said in a statement.

2018 was a tough year for China’s games companies of all sorts. The industry took a hit after regulators froze all licensing approvals to go through a reshuffle, dragging down stock prices of big players like Tencent and NetEase. These companies continue to feel the chill even after approvals resumed, as the newly minted regulatory body imposes stricter checks on games, slowing down the application process altogether and delaying companies’ plans to monetize lucrative new titles.

That bleak domestic outlook compelled NetEase to take what Ding dubs a “two-legged” approach to game publishing, with one foot set in China and the other extending abroad. Tencent, too, has been finding new channels for its games through regional partners like Sea’s Garena in Southeast Asia.

NetEase started in 1997 and earned its name by making PC games and providing email services in the early years of the Chinese internet. More recently the company has intended to diversify its business by incubating projects across the board. It has so far enjoyed growth in segments like music streaming and ecommerce (which is reportedly swallowing up Amazon China’s import-led service) while stepping back from others such as comics publishing, an asset it is selling to youth-focused video streaming site Bilibili.

Powered by WPeMatico

Polis founder Kendall Tucker began her professional life as a campaign organizer in local Democratic politics, but — seeing an opportunity in her one-on-one conversations with everyday folks — has built a business taking that shoe leather approach to political campaigns to the business world.

Now the company she founded to test her thesis that Americans would welcome back the return of the door-to-door salesperson three years ago is $2.5 million richer thanks to a new round of financing from Initialized Capital (the fund founded by Garry Tan and Reddit co-founder Alexis Ohanian) and Semil Shah’s Haystack.vc.

The Boston-based company currently straddles the line between political organizing tool and new marketing platform — a situation that even its founder admits is tenuous at the moment.

That tension is only exacerbated by the fact that the company is coming off one of its biggest political campaign seasons. Helping to power the get-out-the-vote initiative for Senatorial candidate Beto O’Rourke in Texas, Polis’ software managed the campaign’s outreach effort to 3 million voters across the state.

However, politically focused software and services businesses are risky. Earlier this year the Sean Parker-backed Brigade shut down and there are rumblings that other startups targeting political action may follow suit.

“Essentially, we got really excited about going into the corporate space because online has gotten so nasty,” says Tucker. “And, at the end of the day, digital advertising isn’t as effective as it once was.”

Customer acquisition costs in the digital ad space are rising. For companies like NRG Energy and Inspire Energy (both Polis clients), the cost of acquisitions online can be as much as $300 per person.

Polis helps identify which doors for salespeople to target and works with companies to identify the scripts that are most persuasive for consumers, according to Tucker. The company also monitors for sales success and helps manage the process so customers aren’t getting too many house calls from persistent sales people.

“We do everything through the conversation at the door,” says Tucker. “We do targeting and we do script curation (everything from what script do you use and when do you branch out of scripts) and we have an open API so they can push that out and they run with it through the rest of their marketing.”

Powered by WPeMatico

When considering the structural impact of technology companies on our economy and society, we tend to focus on questions of scale and monopoly.

It’s true that the FAANG companies and more recent winners (Airbnb, Uber) have surfed a combination of network effects, preferential access to capital and classic efficiencies of scale to generate tremendous value for their shareholders — to the detriment of new entrants who attempt to unseat them.

At their high water mark in mid-2018, FAANG alone made up 11 percent of the total market cap of the S&P 500 and 38 percent of the index’s year-to-date gain, representing a doubling in their influence in only five years. The question of regulating technology companies — to the point of instituting anti-trust actions — has even become a rare point of relative concord between Democrats and Republicans in Congress.

But is the narrative of tech companies in the 2010s only a story of economic consolidation and growing inequality? Many of the most successful B2B startups of the last decade are aligned by a theme that paints a different picture. By transforming the nature of the costs required to start a business, these startups are reducing the influence of capital and leveling the playing field for new entrants to share in the surplus generated by the secular shift to a tech-mediated economy.

Source: Getty Images/MIKIEKWOODS

What do AWS, WeWork, Stord, Gusto

But they are alike in the economic purpose they serve for their customers. Each of these services takes a fixed cost — a bank of servers, a lease, a legal retainer — and transforms it into a variable cost. As a refresher, a fixed cost stays constant regardless of output, and variable costs scale with the output of a business.

When my father started his software consulting business in the early 1990s, I remember the giant boxes of AIX servers that arrived at our apartment, and tagging along to office tours in central New Jersey before he decided to run the company out of our spare bedroom. Back then, starting almost any kind of business was hard because of high fixed costs. Without AWS or WeWork, you shelled out upfront for hardware and a lease.

Access to capital, whether in the form of a bank loan, savings or friends and family was a prerequisite for entrepreneurship.

Today, startups make it possible to start and scale almost any kind of business while incurring few fixed costs. Want to found an e-commerce store? Start with a free Shopify account and dropship your inventory. Want to become a freelance designer? Put a shingle up on Fiverr and meet clients at a Breather you rent by the hour.

Whether software or hardware or labor, building a business is way easier when overhead is transformed into a string of flexible microservices that you only pay for as you grow.

Image courtesy of Getty Images

Taken together, startups that turn fixed costs into variable costs make it less capital-intensive to start a business. This decreases the influence of gatekeepers and aggregators of capital — an impact evident in the way entrepreneurs think about starting businesses today.

It’s no coincidence that the rise of B2B startups fitting this theme has coincided with the bootstrap movement, in which tech entrepreneurs with major ambitions demur from raising venture funding because — well, they don’t need the money anymore.

It has also coincided with a renaissance in freelance entrepreneurship: 56.7 million Americans freelanced in 2018. Beyond the economic benefits of working for yourself — the fastest growing segment of freelancers earns more than $75,000 a year — freelancers can access the lifestyle and health benefits of owning their destiny, which aren’t directly captured but play a role in the economic picture. Indeed, 51 percent of freelancers said no amount of money would lure them into a traditional job, and 64 percent reported feeling healthier and happier.

When capital plays a reduced role in new business formation, access to capital plays a smaller role in determining who will succeed. More companies are founded, and the economy becomes more likely to birth new Davids that will unseat the Goliaths. Economics 101: lower barriers to entry create markets that converge on perfect competition instead of oligarchic concentration.

Source: Getty Images/ERHUI1979

Variable costs have their downsides. A startup with a relatively higher proportion of fixed costs — the profile of the classic high-tech software business — can achieve higher profit margins as it scales. Compare Microsoft or Google, which pay high fixed costs in the form of salaries and servers but few costs in delivering their services and achieve operating margins of 25-30 percent, to Costco, which takes in more than $100 billion of annual revenue but earns an operating margin in the single digits.

That’s OK. Neither type of cost is “better” or “worse,” but having the option to decide how to structure costs through a company’s life cycle can meaningfully impact an entrepreneur’s ability to execute a business idea.

Founders investigating startup ideas — and politicians debating the impact of technology — would do well to pay attention to how B2B companies have democratized access to entrepreneurship.

Powered by WPeMatico

Nine years after launching its online magazine, and three years after diversifying into the subscription box business, FabFitFun has raised $80 million in a growth round of funding, led by Kleiner Perkins, with participation from its previous investors Upfront Ventures and NEA.

The Los Angeles-based company has steadily expanded its retail and lifestyle empire through subscription boxes, video… and even an augmented reality app.

Last year the company crossed $200 million in revenue and managed to net more than 1 million subscribers for the service.

In a statement the company said the new financing would be used to expand FabFitFun membership offerings and consolidate its position as a marketing partner and platform for brands.

As a result of the investment, Kleiner Perkins general partners Mood Rowghani and Mary Meeker will join as board member and observer, respectively.

It’s been a long ride for co-founders Daniel and Michael Broukhim and Katie Rosen Kitchens. From a newsletter and blog to the subscription box to the launch of live programming last year.

For brands, the pitch is a new way to find customers and engage with them. The seasonally curated boxes and special exclusive co-branded box opportunities with Los Angeles’ pool of influencers results in hundreds of millions of targeted impressions, according to the company.

“FabFitFun has emerged into an exciting and entirely new distribution channel that brings retail to the platforms where consumers are most engaged,” said Mood Rowghani, a general partner at Kleiner Perkins, in a statement. “The company’s personalized connection with its community allows brands to better understand and interact with consumers – establishing a long-term relationship rather than simply a transaction.”

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

According to a new report from The Wall Street Journal, U.S. federal prosecutors are preparing a criminal indictment against Huawei for stealing trade secrets. The report, which cites sources with knowledge of the indictment, specifically mentions Huawei’s actions surrounding a T-Mobile smartphone testing tool known as “Tappy.” The report notes that the current investigation is far enough along that an indictment may come soon.

This isn’t the first we’ve heard of Tappy. In 2014, T-Mobile sued Huawei for allegedly gaining access to a company lab outside of Seattle and photographing and attempting to steal parts of the robotic smartphone testing device. In May 2017, T-Mobile won $4.8 million against Huawei, only a fraction of the $500 million the U.S. mobile carrier sought. The current federal criminal investigation reportedly arose from that civil suit.

The Chinese phone maker has faced increased scrutiny, escalating to open hostility from U.S. agencies and lawmakers who believe that Huawei poses a security threat due to its close relationship with the Chinese government. The tension escalated considerably last December, when Canada arrested Huawei CFO Meng Wanzhou at the request of the U.S. Meng was charged with fraud for deceptive practices that allowed the Chinese company to avoid U.S. sanctions against Iran.

Huawei, now the world’s number two smartphone maker, trails only Samsung when it comes to mobile device sales, beating Apple for the second slot in late 2018.

Powered by WPeMatico

Sprint today announced it will support Apple’s Business Chat — the new platform that allows businesses and customers to interact over iMessage. According to the carrier, customers can now message a Sprint customer service agent, get info about plans and other services, as well as look up store information in Maps, Safari and with Siri during a chat session.

The support from Sprint comes after two other launches on the platform this week.

TD Ameritrade said it will allow customers to fund their brokerage accounts using Apple Pay on Apple Business Chat. And Gubagoo said it will connect car dealerships with customers through Business Chat for viewing inventory, plus scheduling test drives and service appointments.

Apple has been steadily growing its list of supported Business Chat partners, and today has a number of big brands on its platform, which is still in beta. These include names like 1-800-Contacts, DISH, Overstock.com, Quicken Loans, Kimpton Hotels, West Elm, Burberry, Vodafone, Wells Fargo, Credit Suisse, Jos A. Bank, Men’s Warehouse, The Home Depot, Hilton, Four Seasons, American Express, Harry & David and several others.

The platform also supports integrations with customer service platforms LivePerson, Salesforce, Nuance, Genesys, InTheChat, Zendesk, Quiq, Cisco, Kipsu, Lithium, eGain, [24]7.ai, ContactAtOnce, Dimelo, Brand Embassy, ASAPP, IMImobile and MessengerPeople, according to Apple’s website.

Business Chat was officially introduced at WWDC 2017, and is Apple’s entry into the business messaging and chatbot space.

Before its arrival, customers would generally reach out to businesses through social media sites like Facebook (e.g. Pages and Messenger, WhatsApp and Instagram) and Twitter. But Apple’s product gets the businesses even closer to the customer, as their chats can live alongside those from family and friends. Plus, they don’t have to share their data with a third party.

For consumers, reaching a business through iMessage is also a bit easier at times.

A company’s Business Chat profile is highlighted across Apple’s iOS platform in areas like Safari, Maps and Spotlight, and via Siri. This makes it more seamless to move from one Apple app to an iMessage chat, compared with having to seek out the business’s social media profile.

It’s also less painful than having to dial a customer service phone number, in many cases — as Sprint today pointed out.

“More consumers are embracing quick and easy self-service and digital assistance versus calling customer service through an 800 line,” said Rob Roy, Sprint chief digital officer, in a statement about the launch. “Apple Business Chat is an amazing tool for our customers that makes communicating with Sprint fast, easy and stress-free.”

Business Chat has come at a time when the “phone” part of our smartphones is turning into just another “app” — and increasingly, a spammy and bothersome one thanks to spam calls. Apple’s solution makes it easier for customers and businesses to move away from phone lines, while Google is leveraging AI to handle spammers — and even place calls for customers through its Google Duplex technology.

Powered by WPeMatico

Many founders believe in the myth that the first steps of starting a business are the hardest: Attracting the first investment, the first hires, proving the technology, launching the first product and landing the first customer. Although those critical first steps are difficult, they are certainly not the most difficult on the arduous path of building an iconic company. As early and late-stage funding becomes more abundant, founders and their early VC backers need to get smarter about how to position their companies for a looming valley of death in-between. As we’ll learn below, it’s only going to get much, much harder before it gets easier.

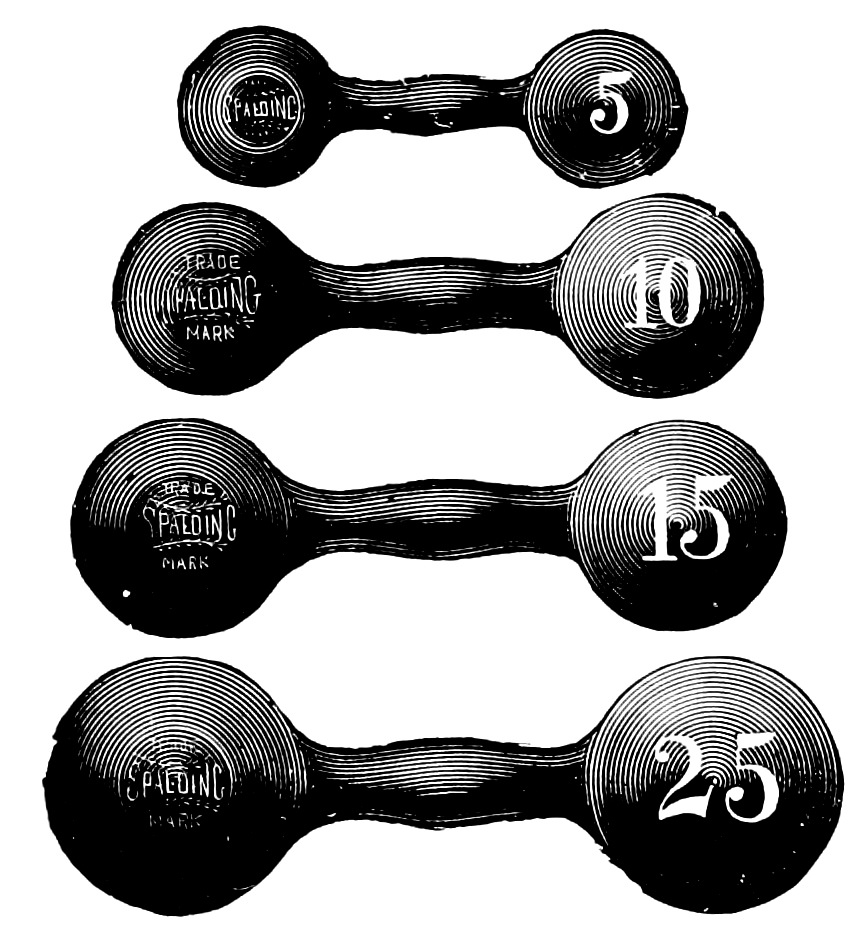

Money will have the look, and heft, of dumbbells as the economic cycle turns. Expect an abundance of small, seed checks at one end, an abundance of massive checks for clear, breakout companies at the other, and a dearth of capital for expanding companies with early proof points and market traction. Read more on how to best prepare for this inevitable future. (Image courtesy Flickr/CircaSassy)

There will be an abundance of capital at the two ends of the startup spectrum. At one end, hundreds of seed and micro VCs, each armed with dozens of $250,000-$1 million checks to write every year, are on the prowl for visionary founders with pedigrees and resumes. At the other end, behemoths like SoftBank, sovereigns, as well “early-stage” firms raising larger funds are seeking breakout companies ready for checks that are in the mid-tens to hundreds of millions. There will be a dearth of capital to grow companies from a kernel of a business, to becoming the clear market-defining leader. In fact, we’re already seeing deal volume decreasing significantly as dollars increase, likely evidence of larger checks going into fewer companies.

Even as the overall number of deals decrease below 2012 levels, the overall dollars invested into startups continue to soar. The 200+ “seed-stage” funds formed since 2012 will continue to chase nascent companies. Meanwhile, the increasing number of mega-funds will seek breakout companies into which to make $100 million+ investments. Companies with early traction seeking ~$20 million to grow will be abundant and have difficulty accessing capital.

Founders should no longer assume that their all-star seed and Series A syndicates will guarantee a successful follow-on financing. Progress on recruiting and product development, though necessary, are no longer sufficient for B-rounds and beyond. Founders should be mindful that investors that specialize in leading $20-50 million rounds will have a plethora of well-funded, well-mentored, well-staffed startups with slick presentations, big visions and some early market traction from which to choose.

Today, there is far more capital chasing fewer quality companies. Fewer breakout companies and fear of missing out is making it easy to raise growth rounds with revenue growth, which may not be scalable or even reflective of an attractive business. This is creating false realities and prompting founders to raise big rounds at high prices — which is fine when there is an over-abundance of capital, but can cripple them when capital later becomes scarce. For example, not long ago, cleantech companies, armed with very preliminary sales, raised massive financings from VCs eager to back winners toward scaling into what they characterized as infinite demand. The reality is that the capital required to meet target economics was far greater and demand far smaller. As the private markets turned, access to cash became difficult and most faltered or were acquired for pennies on the dollar.

There is a likely future where capital grows scarce, and investors take a harder look at the underpinnings of revenue, growth and (dis)economies of scale.

What should startup leadership teams emphasize in an inevitable future where the $30 million rounds will be orders of magnitude harder than their $5 million rounds?

Leadership teams put lots of emphasis on revenue. Unfortunately, revenue that’s not representative of the big vision is probably worse than no revenue at all. Companies are initially seeded with the expectation that the founding team can build and sell something. What needs to be proven is the hypothesis that the company can a) build a special product that b) is inexpensive to convince customers to pay for, and c) that those customers represent a massive market. It should be proven that it is unattractive for customers to switch to the inevitable copycats. It should be clear that over time, customers will pay more for additional features, and the cost of acquiring new customers will go down. Simply selling a product to customers that don’t represent that model is worse than not selling anything at all.

Early founding teams are cognitively diverse individuals that can convince early investors that they can overcome the incredible odds of building a company that until now, shouldn’t have existed. They build a unique product, leveraging unique tools satisfying an unmet need. The early teams need to demonstrate the big vision, and that they can recruit the people that can make that vision a reality. Unfortunately, more founders struggle when it comes to recruiting people that have real experience reducing a technology to practice, executing on a product that customers want and charting the path to expand their market with improving unit economics. There are always exceptions of people that do the above for the first time at startups; however, most of today’s iconic startups knew what kind of talent they needed to execute and succeeded in bringing them on board. Who’s on your team?

The attractive SaaS valuation multiples behoove all founders to apply its metrics to their businesses even if they aren’t really SaaS businesses. Sophisticated later-stage investors see right past that and dismiss numbers associated with metrics that are not representative. Semiconductors are about winning dedicated sockets in growing markets. Design tools are about winning and upselling seats in an industry that’s going to be hooked on those tools. Develop a clear understanding of how your business will be measured. Don’t inundate your investor with numbers; present a concise hypothesis for your unfair advantage in a growing market with your current traction being evidence to back it.

“Pouring fuel on the fire” is a misleading metaphor that leads some into believing that capital can grow any business. That’s just as true as watering a plant with a fire hose or putting TNT in your Corolla’s gas tank: most business models and markets simply are not native to the much-sought-after venture growth profile. In fact, most later-stage startups that fail after raising large amounts of capital fail for this reason. Most markets are conducive to businesses with DIS-economies of scale, implying dwindling margins with scale, which is why many businesses are small, serving local, fragmented markets that technology alone cannot consolidate. How do your unit economics improve over time? What are the efficiencies generated by economies of scale? Is there a real network effect that drives these economies?

Image courtesy Getty Images

I expect today’s resourceful founders to seek partners, whether it’s employees, advisors or investors, to help them answer these questions. Together, these cognitively diverse teams will work together to accelerate past any metaphoric valley and build the iconic companies taking humanity to its fantastic future.

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

Video won’t start rolling on Meg Whitman and Jeffrey Katzenberg’s new bite-sized streaming service with the billion-dollar backing until the end of 2019, but talent keeps signing up to come along for their ride into the future of serialization.

The latest marquee director to sign on the dotted line with Quibi is Catherine Hardwicke, who will be helming a story around the creation of an artificial intelligence with the working title “How They Made Her,” according to an announcement from Katzenberg onstage at the Variety Innovate summit.

Hardwicke, who directed “Thirteen,” “Lords of Dogtown” and, most famously, “Twilight,” is joining Antoine Fuqua, Guillermo del Toro, Sam Raimi and Lena Waithe in an attempt to answer the question of whether Whitman and Katzenberg’s gamble on premium (up to $6 million per episode) short-form storytelling is a quixotic quest or a quintessential viewing experience for a new generation of media consumers.

Katzenberg also revealed in a LinkedIn post that Quibi would be working on a basketball-related series with Steph Curry’s production company. He wrote:

I announced a new docu-series by Whistle called “Benedict Men” coming exclusively to Quibi. “Benedict Men” will be executive produced by Stephen Curry’s Unanimous Media and will give viewers an inside look at one of the most unique high school basketball teams in America at St. Benedict’s Prep in Newark, New Jersey.

St. Benedict’s Prep is an all-boys secondary school founded on the core belief ‘What Hurts My Brother Hurts Me,’ and aims to foster a legacy of strong character, community, leadership, and faith. As one of the top athletic high schools with a storied basketball program and the highest graduation rate in New Jersey, the series will follow the brotherhood of young men who seek to balance life in complicated surroundings.

In some ways, the big adventure backed by Katzenberg, the former chairman of Walt Disney Studios and founder of WndrCo, and every major Hollywood studio — including Disney, 21st Century Fox, Entertainment One, NBCUniversal, Sony Pictures Entertainment and Alibaba Goldman Sachs — is the latest in an everything old is new again refrain.

If blogs reinvented printed media, and podcasts and music streaming reinvented radio, why can’t Quibi reinvent serialized storytelling.

Again and again, Whitman and Katzenberg returned to an analogy from the early days of the cable revolution. “We’re not short form, we’re Quibi,” said Whitman, echoing the tagline that HBO made famous in its early advertising blitzes. That Whitman and Katzenberg’s project to take what HBO did for premium television and apply that to mobile media is ambitious. Now industry-watchers will have to wait until 2019 at the earliest to see if it’s also successful.

In the interview onstage at a Variety event on artificial intelligence in media, Katzenberg cited Dan Brown’s “The Da Vinci Code” as something of an inspiration — noting that the book had more than 100 chapters for its 500 pages of text. But Katzenberg could have gone back even further to the days of Dickens and his serialized entertainments.

And right now for the entertainment business it really is the best of times and the worst of times. Traditional Hollywood studios are seeing new players like Netflix, Amazon, Apple and others all trying to drink their milkshake. And, for the most part, these studios and their new telecom owners are woefully ill-equipped to fight these big technology platforms at their own game.

Taking the long view of entertainment history, Katzenberg is hoping to win networks with not just a new skin for the old ceremony of watching entertainment but with a throwback to old style deal-making. The term serialization here takes on greater meaning.

Quibi is offering its production partners a sweetheart deal. After seven years the production company behind the Quibi shows will own their intellectual property, and after two years those producers will be able to repackage the Quibi content back into long-form series and pitch them for distribution to other platforms. Not only that, but Quibi is fronting the money for over 100 percent of the production.

Katzenberg said that it “will create the most powerful syndicated marketplace” Hollywood has seen in decades. It’s a sort of anti-Netflix model where Katzenberg and Whitman view Quibi as a platform where creators and talent will want to come. “We are betting on the success of the platform — and by the way, it worked brilliantly in the ’60s and ’70s and ’80s.” Katzenberg said. “Hundreds of TV shows were tremendous successes and [like the networks then] we don’t want to compete with our suppliers.”

In addition to the business model innovations (or throwbacks, depending on how one looks at it), Quibi is being built from the ground up with a technology stack that will leverage new technologies like 5G broadband, and big data and analytics, according to Whitman.

Indeed, launching the first platform built without an existing stable of content means that Quibi is preparing 5,000 unique pieces of content to go up when it pulls the curtains back on its service in late 2019 or early 2020, Whitman said.

And the company is looking to big telecommunications companies like Verizon (my corporate overlord’s corporate overlord) and AT&T as partners to help it get to market. Since those networks need something to do with all the 5G capacity they’re building out, high-quality streaming content that’s replete with meta-tags to monitor and manage how an audience is spending their time is a compelling proposition.

“We want to work to have video that looks good on mobile [and] ramp up content in terms of quantity and quality,” Whitman said. That quality extends to things like the user interface, search features and analytics.

“We have to have a different search and find metaphor,” Whitman said. “It takes eight minutes to find what you’re looking for on Netflix… We will be able to instrument this with data on what people are watching and using that in our recommendation engine.”

Questions remain about the service’s viability. Like what role will the telcos actually play in distribution and development? Can Quibi avoid the Hulu problem where the various investors are able to overcome their own entrenched interests to work for the viability of the platform? And do consumers even want a premium experience on mobile given the new kinds of stars that are made through the immediacy and accessibility that technology platforms like YouTube, Instagram and Snap offer?

“Where the fish are today is a phenomenal environment,” Katzenberg said of the current short-form content market. “But it is an ocean. We need to find a place where there are these premium services.”

Powered by WPeMatico