business incubators

Auto Added by WPeMatico

Auto Added by WPeMatico

Less than a decade ago IPOs, acquisitions and global expansion by African startups were more possibility than reality. March saw all three from the continent’s tech scene.

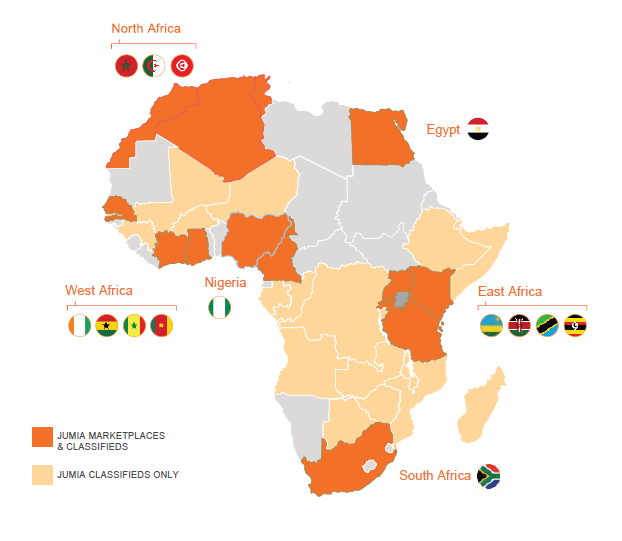

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange, per SEC documents and confirmation from chief executive Sacha Poignonnec.

In an updated filing, (since the March 12 original) Jumia indicated it will offer 13,500,000 ADR shares, for an offering price of $13 to $16 per share to trade under the ticker symbol “JMIA.” The IPO could raise up to $216 million for Jumia.

Since our first story (and reflected in the latest SEC docs), Mastercard Europe agreed upfront to buy $50 million in Jumia ordinary shares.

With a smooth filing process, Jumia will become the first African startup to list on a major global exchange. The company is incorporated in Germany, but maintains its headquarters in Nigeria, and operates exclusively in Africa, with 4,000 employees on the continent.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data. The company has started to generate annual revenues over $100 million, but like many burn-rate startups, has done so while racking up big losses.

There’ll be a lot more to cover, analyze and debate pre and post Jumia’s NYSE bell toll — which could happen in coming weeks or months. For example, can Jumia generate a profit; is it really an African startup; will Jumia become an acquisition target for a big outside name or an acquirer of smaller startups in African e-commerce? Stay tuned for continuing TechCrunch coverage.

On the acquisition front, Lagos-based online lending startup OneFi bought Nigerian payment solutions company Amplify for an undisclosed amount.

OneFi is taking over Amplify’s IP, team and client network of more than 1,000 merchants to which Amplify provides payment processing services, OneFi CEO Chijioke Dozie told TechCrunch.

The purchase of Amplify caps off a busy period for OneFi. Over the last seven months the Nigerian venture secured a $5 million lending facility from Lendable, announced a payment partnership with Visa and became one of the first (known) African startups to receive a global credit rating. OneFi is also dropping the name of its signature product, Paylater, and will simply go by OneFi (for now).

Collectively, these moves represent a pivot for OneFi away from operating primarily as a digital lender, toward becoming an online consumer finance platform.

“We’re not a bank but we’re offering more banking services…Customers are now coming to us not just for loans but for cheaper funds transfer, more convenient bill payment, and to know their credit scores,” said Dozie.

OneFi will add payment options for clients on social media apps, including WhatsApp, this quarter — something in which Amplify already holds a specialization and client base. Through its Visa partnership, OneFi will also offer clients virtual Visa wallets on mobile phones and start providing QR code payment options at supermarkets, on public transit and across other POS points in Nigeria.

On the back of the acquisition, OneFi is in the process of raising a round and will look to expand internationally, considering Senegal, Côte d’Ivoire, DRC, Ghana and Egypt and Europe for Diaspora markets.

On African startups expanding globally, FlexClub — a South African venture that matches investors and drivers to cars for ride-hailing services — announced it will expand in Mexico in a partnership with Uber after closing a $1.2 million seed round led by CRE Venture Capital.

The move comes as Africa’s tech-transit space continues to produce unique mobility solutions shaped around local needs.

FlexClub touts itself as a “gig economy investment platform” that is creating new asset classes in emerging markets, according to chief executive and co-founder Tinashe Ruzane.

That asset class, for now, is ride-hail vehicles. FlexClub allows investors to go on the site and purchase a car (ultimately managed and serviced by FlexClub). The startup then connects that car to an Uber driver who uses earnings to pay a weekly rental charge.

Those fees generate monthly fixed-rate interest income for the investor. The driver has the option of buying the car after 12 months, with a descending purchase price over time.

FlexClub’s platform manages the investment, rental income and disbursement of funds across all parties. The startup also handles insurance, maintenance and upkeep of the cars.

Ruzane envisions this as a model to finance multiple asset classes in emerging markets — where lending options are fewer for individuals who may not have credit histories.

“Our goal is to make this completely passive… where investors can invest in different kinds of assets on our platform, login to a dash, and see this is how my five cars in South Africa are doing, my vans in Mexico, my motorbikes in Indonesia — with a diversified portfolio around the world,” he explained.

FlexClub will begin work matching investors to cars and Uber drivers in Mexico in April. The startup sees opportunities to move into other mobility classes, such as Africa’s ride-hail motorcycle taxi and three-wheel tuk-tuk market, CEO Tinashe Ruzane told TechCrunch in this feature.

And finally, francophone Africa will see a boost in funds and support for startups. The Dakar Network Angels group launched last month, making its first investment to cleantech venture Coliba — an Ivorian startup that uses a mobile app to coordinate waste recycling

The deal is part of Dakar Network Angels’ mission of convening experts and capital to bridge the resource gap for startups in French-speaking Africa — or 24 of the continent’s 54 countries.

The organization — which goes by DNA for short — will offer seed fund investments of between $25,000 to $100,000 to early-stage ventures with high growth potential. These rounds will come with the entrepreneurial guidance of DNA’s angel network.

Launched in Senegal, the organization’s founder Marieme Diop — a VC investor at Orange Digital Ventures — named the goal of bridging VC disparities between francophone and non-francophone Africa as the primary driver for DNA. She pointed to funding data by Partech, indicating that 76 percent of investment to African startups goes to three English-speaking countries — Nigeria, Kenya and South Africa.

To gain consideration for DNA investment, startups must gain referral by a member. DNA will take a minority stake (less than 10 percent) in ventures that receive seed funds and provide program mentorship until exits, Diop told TechCrunch.

To become an angel, members must commit to investing a minimum of $10,000 a year (for those coming on as individuals), $20,000 (for corporates) and be on hand to support the portfolio startups, according to DNA’s Corporate Membership Charter.

More Africa Related Stories @TechCrunch

African Tech Around The Net

Powered by WPeMatico

Aditya and Aarti Kochhar Kaji didn’t set out to start the snack food business Taali Foods when they were studying for their business degrees at Harvard.

The couple both hail from Mumbai and met at the University of Pennsylvania . They were married before starting at Harvard’s Business School and initially were interested in other areas — Aarti was exploring a career in venture capital and Aditya was looking at the food and beverage industry broadly in his classes at Harvard.

Addicted to snack foods like chips and popcorn to fuel her Harvard study sessions, Aarti started making popped water lily seeds as a snack — a food both she and her husband had grown up eating in India, she said.

The seeds, which are high in anti-oxidants and low in fat, have been a staple of Ayurvedic medicine — thanks to their purported anti-inflammatory properties, and are a staple of Indian snacking traditions. Now, with American consumers on the hunt for healthier snacks, they’re becoming a big business in the U.S. as well.

Y Combinator is very on-trend, with its decision to invest and accelerate Taali as part of its most recent cohort of startups. But in this instance you may call the accelerator a fast follower rather than a progenitor of this trend.

No less auspicious a food tastemaker than Whole Foods named water lily seeds as one of the top 10 new food trends of 2019. With that attention, competitors to Taali abound.

Bohana and AshaPops are just two new snack food companies floating on the popped water lily seed movement. Bohana even managed to nab the attention of PepsiCo’s Nutrition Greenhouse competitive accelerator.

It’s no secret that technology investors are investing more heavily in consumer businesses — everything from snack foods to period products and baby formula — and startups need only point to the success of Amazon as the everything store to show that there’s always money to be made in the category.

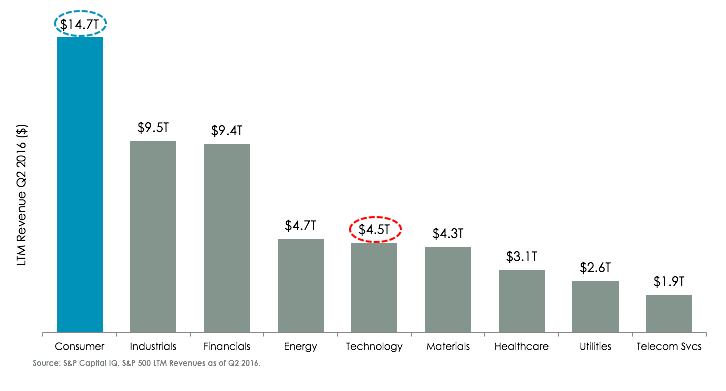

Indeed, at $1.47 trillion, the consumer packaged goods industry dwarfs technology as a share of the nation’s economy.

As Ryan Caldbeck, the head of the consumer-focused investment firm CircleUp noted last year:

The uptick in tech VC dollars going to the CPG market is partly because tech investing is brutally competitive and saturated, and largely because these VCs are awakening to the strong historical returns in CPG, especially with the trend leaning towards small brands stealing market share.

Consumer is a massive market – about 3x the size of tech, as seen below.

Despite the size of the market, the early-stage has historically been underserved by investors due to market inefficiencies like the geographic dispersion of brands and a lack of structured information sources (i.e. there is no Silicon Valley for consumer, and certainly no Crunchbase equivalents – yet).

Strong exits are already possible for consumer brands — and not necessarily from the big-ticket, headline grabbing acquisitions like Dollar Shave Club. Last week This is L. — the condom and period product retailer — sold for roughly $100 million after raising seed funding from investors, including 500 Startups and Y Combinator.

Taali was similarly bootstrapped before it was accepted into Y Combinator. The company is already selling its snacks through Amazon and in retail locations like Fairway in New York and Central Market in Texas. The founders expect to be in stores in California in the next few months.

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

SOSV, a 20-year-old fund with $500 million in assets under management, has been running accelerators for years. Their oldest one, HAX, is the premier hardware accelerator in San Francisco and Shenzhen, and they’ve recently launched a food accelerator in New York and a pair of biology accelerators. Now, however, they’ve just announced DLab, a crypto accelerator that is paired with Cardano to build out distributed apps and solutions.

It is led by Nick Plante, a programmer integral in drafting the JOBS Act and who co-founded Wefunder, a successful crowdfunding platform.

“We can only make this sort of commitment to ecosystems we feel are incredibly compelling; it takes a substantial amount of dedication, education, staffing, and of course the long-term financial commitment to support the space and the companies,” said Plante. “We invest in ecosystems that we identify as ‘macro trends’ like disruptive food, life sciences and synthetic biology, Chinese market entry, IoT and robotics… things that will fundamentally alter the way that we live in the next 100 years.”

“Decentralization is clearly a macro trend, in the macro sense. What’s happening with blockchain and digital ledger technologies has the potential to upend some of the most basic economic incentives that lie beneath the things we do every day; to affect the ways that humans collaborate, identify, trust, govern, and bring new ideas to life… it underlies all of it,” he said.

DLab supplies up to $200,000 in pre-seed funding as well as perks from the SOSV global network of accelerators. They are also offering fellowships in partnership with Cardano to work with projects that would further blockchain research.

“Through last year and the start of this year we kept watching the blockchain ecosystem do some amazing things — along with some criminal things. The surveys and reports about the fraud rates of ICOs and other unpleasantness kept underlining our concerns report after report. The potential for the big economic shifts I mentioned earlier were clearly here but there were so, so many problems; there was a real need for education, for curation, and for proper governance and incentive structures to be put in place,” said Plante.

The group is accepting applications now for a January cohort. The group invests in 150 startups per year, a heady number in these cash-poor times.

Powered by WPeMatico

The American Midwest has a long history of making stuff. During the 20th century, it was the manufacturing center for the nation, and indeed much of the world. It’s still where a surpassing majority of agricultural commodities are grown and processed. But is it also a major producer of technology startups? Maybe not as much as the coasts, but the Midwest’s bustling metropoli and vast expanses of rural land prove to be fertile ground for quite a bit of startup activity.

And that’s what we’re going to take a look at here. In a similar vein to our recent analysis of startup fundraising in the South, we’ll break down the region into its constituent parts, assessing deal and dollar volume trends in the Midwest’s two primary sub-regions, some of its individual states and the most active metropolitan areas in the U.S.’s midsection.

And, to be clear, this is not Crunchbase News’s first foray into the region. We’ve covered the region’s seed-stage interest in AI and hard tech, a few notable rounds and have always included the Midwest in all manner of data-spelunking expeditions. And to this, we’ll add a deep dive into the numbers.

Borders and boundaries are a deep well of disputes. To preempt debate, we use the U.S. Census Bureau’s definition of the Midwest region which, unlike its definition of the South, shouldn’t be too controversial. If you have something against Kansas or Ohio being included in this group, take it up with the Feds.

The good folks at the Census Bureau split the Midwest into two distinct — and rather unimaginatively named — sub-regions: the West North Central and East North Central states, which are separated by the Mississippi River. We’ve included the map below.

By splitting the Midwest into two distinct parts, we’ll be able to see where most of the startup and funding activity is concentrated. Spoiler alert: The farther west you go, the startup population (and the population itself) grows more scattered.

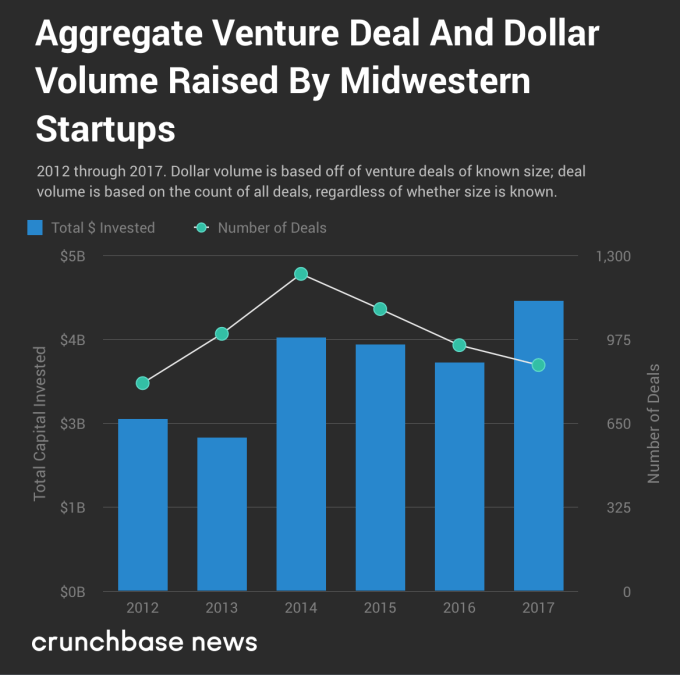

Based only on reported data in Crunchbase, the Midwest appears to be affected by the same phenomenon as the rest of the country. Crunchbase News has previously found that the number of seed and early-stage deals has gone off a cliff in the U.S., resulting in a top-heavy market featuring many large, late-stage deals. And this wouldn’t be a problem if it weren’t for a shortfall in new startups to fill the next cycle of early-stage funding. The “hollowing out” of the Midwestern venture deal pipeline becomes readily apparent when you look at funding data for the past several years, which you can find in the chart below.

To wit, deal volume is down markedly since 2014, as Crunchbase News reported in its Q4 2017 report of startup funding activity in the U.S. and Canada. But somewhat counterintuitively, the amount of money being invested into startups is on the rise in the Midwest and throughout many other parts of the country, reaching fresh multi-year highs in 2017. Almost one full quarter into 2018, the trend appears to continue unabated.

But this chart abstracts away a lot of nuance, so let’s take a closer look at the region and its states.

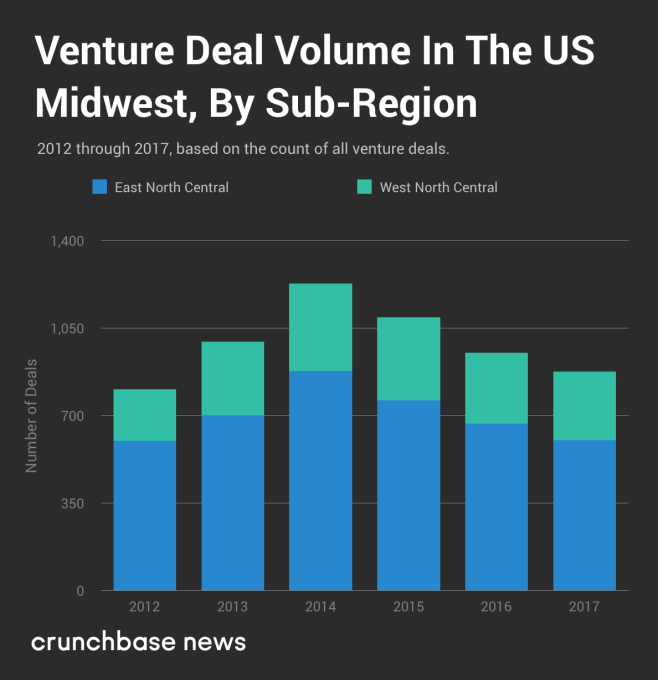

We’ll start first with deal volume, because that’s a fairly decent indicator of a geographic region’s level of startup activity. Below, we’ve plotted venture deal volume, divided by sub-region.

Again, based on the reported data from Crunchbase, we found that deal counts have been on a downward trend for several years. And though some of this may be attributable to reporting delays, projected deal volume data for the whole of the U.S. and Canada (fourth chart down in the Q4 quarterly report) shows a years’-long downtrend. There’s no reason to believe that startup activity in the Midwest is materially different from the rest of the U.S. and Canada.

But what about the relative “balance of power” between the two sub-regions? At least when it comes to deal volume, has one sub-region waxed while the other waned? To a limited extent, the answer is yes. Between 2012 and 2017, the percentage share of all Midwestern dealflow going to West North Central states like the Dakotas, Minnesota and Missouri has grown from 25.4 percent to 31.2 percent, up by nearly one-fifth in relative terms.

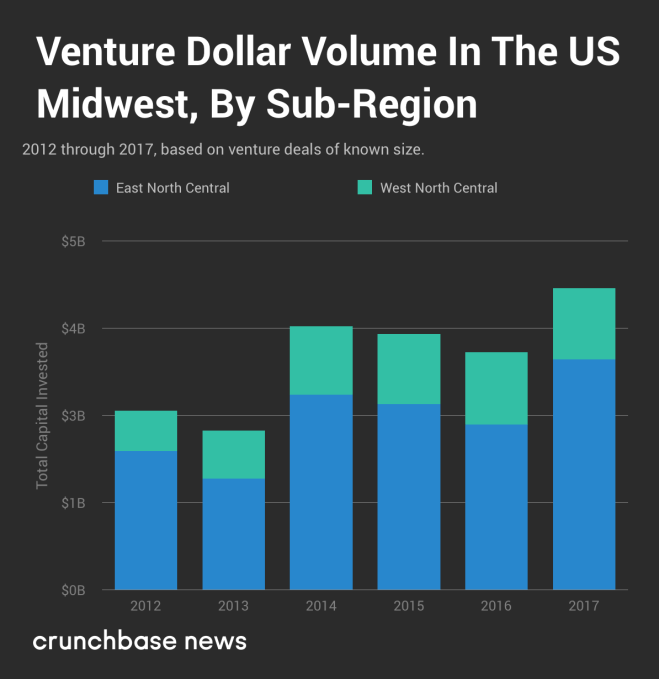

Now let’s check out dollar volume. The chart below displays aggregate reported venture capital dollar volume raised by startups in the Midwest.

As far as the amount of money Midwestern startups have raised over time, the trendline is generally up and to the right. But that’s not the only way this differs from the deal volume data we looked at earlier. For dollar volume, there appears to be no appreciable change in the “balance of power” between the two sub-regions since 2012. Depending on the year, East North Central states like Illinois, Michigan and Ohio raked in between 70 and 78 percent of total dollar volume, but that variance doesn’t appear in an orderly trend.

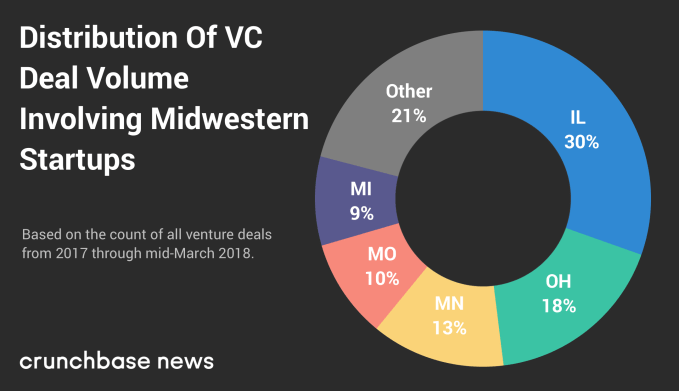

We started first at the regional level, then compared smaller groupings of states. Now, let’s see how deal and dollar volume is distributed on a state-by-state level. Doing so will point to the states that lead the region in venture-backed startup activity. Below, you’ll find a chart of how deal volume is split between the top five Midwestern states.

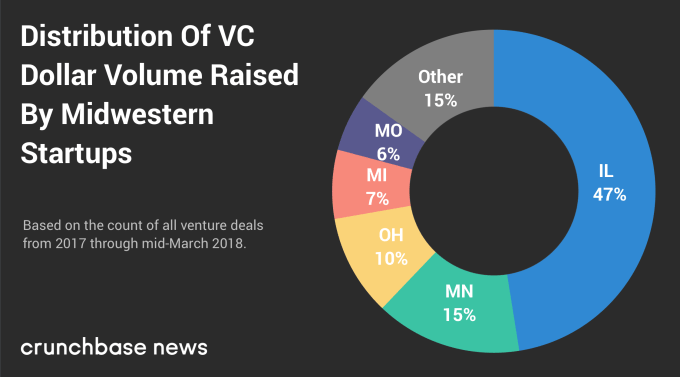

And here is how dollar volume is distributed.

As we saw with our analysis of the South, the top five Midwestern states for deal volume are the same five top-ranked states for dollar volume. But there is some notable variation in how these states rank among each other and the amount of deal and dollar volume they account for.

Considering that Illinois is home to Chicago and a number of downstate universities with deep tech startup roots, the fact that it places first for both metrics shouldn’t come as much of a surprise.

What might be more of a head-scratcher is Minnesota, which ranks third in deal volume but second in dollar volume. Why does it switch places with Ohio? The answer could lie in the industrial mix which, in the case of Minnesota, includes a disproportionately high number of medical device and other life sciences companies, which typically take a lot of capital to get off the ground.

Longtime readers of Crunchbase News may remember a ranking of Midwestern startup cities we wrote back in August 2017. However, here we’re just focusing on deal and dollar volume over the past 15 months, since the start of 2017.

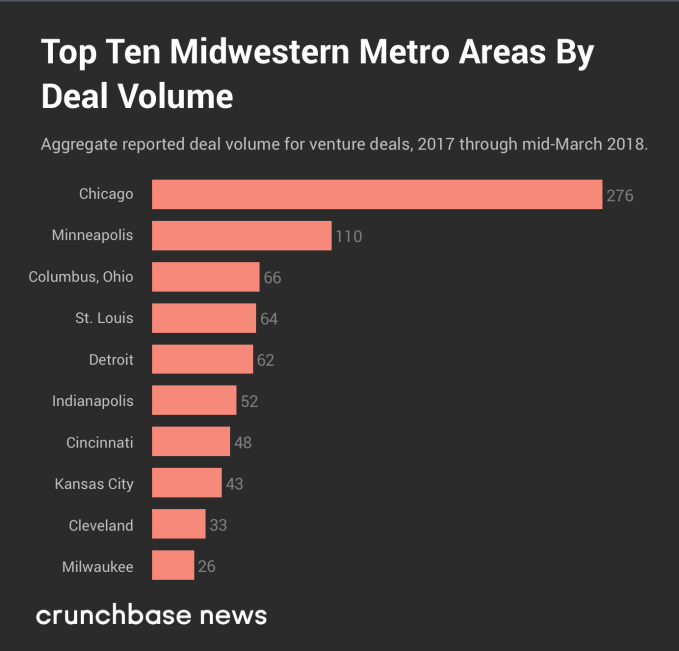

Let’s start first with the top 10 Midwestern cities as measured by number of startup funding rounds.

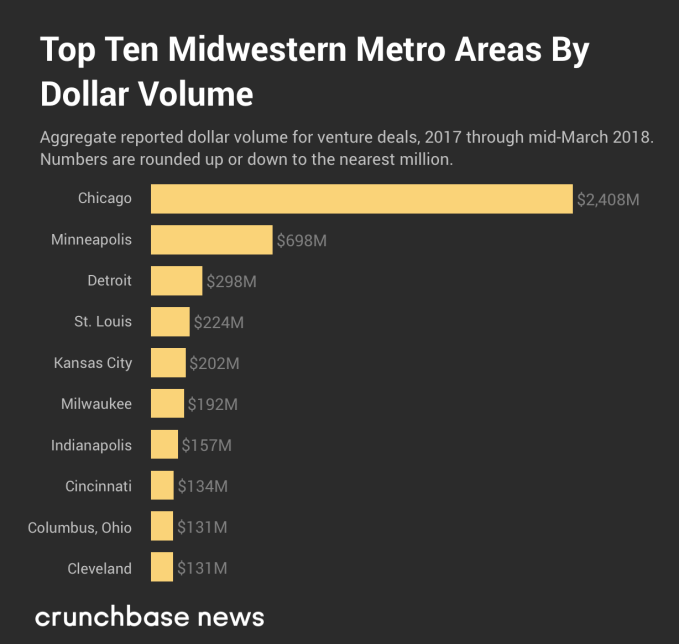

And in the chart below, you can see the top cities, as ranked by venture dollar volume, from the same period of time.

In both rankings, four of the top five cities are the same, but the odd one out appears to be Columbus, Ohio. Although there were a fairly large number of rounds raised by startups in that metro area, most of the rounds were fairly small by national standards. And one of the main reasons why Kansas City, Missouri jumped so much in the dollar volume rankings was a $100 million Series F round raised by C2FO.

But, again, as far as the Midwest goes, everything pales in comparison to Chicago alone.

For many, the Midwest is in a kind of Goldilocks zone. The East and West coasts seem to hold more or less equal sway over the culture and economy and most of its cities are neither too big nor too small. The only extreme it seems to occupy is its winter weather.

Powered by WPeMatico

It seems like startup news is full of overnight success stories and sudden failures, like the scooter rental company that went from zero to a $300 million valuation in months or the blood-testing unicorn that went from billions to nearly naught.

But what about those other companies that mature more gradually? Is there such a thing as slow and successful in startup-land?

To contemplate that question, Crunchbase News set out to assemble a data set of top late-blooming startups. We looked at companies that were founded in or before 2010 that raised large amounts of capital after 2015, and we also looked at companies founded a least five years ago that raised large early-stage funds in the last year. (For more details on the rules we used to select the companies, check “Data Methods” at the end of the post.)

The exercise was a counterpoint to a data set we did a couple of weeks ago, looking at characteristics of the fastest growing startups by capital raised. For that list, we found plenty of similarities between members, including a preponderance of companies in a few hot sectors, many famous founders and a lot of cancer drug developers.

For the late bloomers, however, patterns were harder to pinpoint. The breakdown wasn’t too different from venture-backed companies overall. Slower-growing companies could come from major venture hubs as well as cities with smaller startup ecosystems. They could be in biotech, medical devices, mobile gaming or even meditation.

What we did find, however, was an interesting and inspiring collection of stories for those of us who’ve been toiling away at something for a long time, with hopes still of striking it big.

Even youthful startups have been known to make a major pivot or two. So it’s not surprising to see a lot of pivots among late bloomers that have had more time to tinker with their business models.

One that fits this mold is Headspace, provider of a popular meditation app. The company, founded in 2010 by a British-born Buddhist monk with a degree in circus arts, started as a meditation-focused events startup. But it turned out people wanted to build on their learning on their own time, so Headspace put together some online lessons. Today, Santa Monica-based Headspace has millions of users and has raised $75 million in venture funding.

For late bloomers, the pivot can mean going from a model with limited scalability to one that can attract a much wider audience. That’s the case with Headspace, which would have been limited in its events business to those who could physically show up. Its online model, with instant, global reach, turns the business into something venture investors can line up behind.

They say if you wait long enough, everything comes back in style. That mantra usually works as an excuse for hoarding ’80s clothes in the attic. But it also can apply to entrepreneurial companies, which may have launched years before their industry evolved into something venture investors were competing to back.

Take Vacasa, the vacation rental management provider. The company has been around since 2009, but it began raising VC just a couple of years ago amid a broad expansion of its staff and property portfolio. The Portland-based company has raised more than $140 million to date, all of it after 2016, and most in a $103 million October round led by technology growth investor Riverwood Capital.

CloudCraze, which was acquired by Salesforce earlier this week, also took a long time to take venture funding. The Chicago-based provider of business-to-business e-commerce software launched in 2009, but closed its first VC round in 2015, according to Crunchbase records. Prior to the acquisition, the company raised about $30 million, with most of that coming in just a year ago.

Meanwhile, some late bloomers have always been fashionable, just not necessarily as VC-funded companies. Untuckit, a clothing retailer that specializes in button-down shirts that look good untucked, had been building up its business since 2011, but closed its first venture round, a Series A led by VC firm Kleiner Perkins, last June.

So yes, there is still capital available for those who wait. However, the truth of the matter is most companies that raise substantial sums of venture capital secure their initial seed rounds within a couple years of founding. Companies that chug along for five-plus years without a round and then scale up are comparatively rare.

That said, our data set, which looks at venture and seed funding, does not come close to capturing the full ecosystem of slow-growing startups. For one, many successful bootstrapped companies could raise venture funding but choose not to. And those who do eventually decide to take investment may look at other sources, like private equity, bank financing or even an IPO.

Additionally, the landscape is full of slow-growing startups that do make it, just not in a venture home run exit kind of way. Many stay local, thriving in the places they know best.

On the flip side, companies that wait a long time to take VC funding have also produced some really big exits.

Take Atlassian, the provider of workplace collaboration tools. Founded in 2002, the Australian company waited eight years to take its first VC financing, despite plentiful offers. It went public two years ago, and currently has a market valuation of nearly $14 billion.

The moral: Those who take it slow can still finish ahead.

Data methods

We primarily looked at companies founded in 2010 or earlier in the U.S. and Canada that raised a seed, Series A or Series B round sometime after the beginning of last year, and included some that first raised rounds in 2015 or later and went on to substantial fundraises. We also looked at companies founded in 2012 or earlier that raised a seed or Series A round after the beginning of last year and have raised $30 million or more to date. The list was culled further from there.

Powered by WPeMatico

In the world of mobile apps, numbers come in two sizes: big and bigger. More than one billion people use Facebook’s mobile app every day. But what about the financial side of the mobile business; specifically, venture investment and returns? By looking at the numbers behind two different ends of the startup life cycle, a reasonable understanding of the mobile market today can be had. Read More

In the world of mobile apps, numbers come in two sizes: big and bigger. More than one billion people use Facebook’s mobile app every day. But what about the financial side of the mobile business; specifically, venture investment and returns? By looking at the numbers behind two different ends of the startup life cycle, a reasonable understanding of the mobile market today can be had. Read More

Powered by WPeMatico

With a shortage of machine learning developers bearing down on the industry, startups and big tech companies alike are moving to democratize the tools necessary to commercialize artificial intelligence. The latest startup, Petuum, is announcing a $93 million Series B this morning from Softbank and Advantech Capital.

With a shortage of machine learning developers bearing down on the industry, startups and big tech companies alike are moving to democratize the tools necessary to commercialize artificial intelligence. The latest startup, Petuum, is announcing a $93 million Series B this morning from Softbank and Advantech Capital.

Founded last year by Dr. Eric Xing, a Carnegie Mellon machine learning… Read More

Powered by WPeMatico

Alchemist Accelerator, known for its specialty in working with enterprise startups, held its 16th demo day at Microsoft’s offices in Mountain View, California. 18 startups pitched ideas ranging from more traditional marketplaces to frontier aerospace technology. Addressing the packed auditorium before the pitches began, Ravi Belani, managing partner at Alchemist, reasserted his core… Read More

Alchemist Accelerator, known for its specialty in working with enterprise startups, held its 16th demo day at Microsoft’s offices in Mountain View, California. 18 startups pitched ideas ranging from more traditional marketplaces to frontier aerospace technology. Addressing the packed auditorium before the pitches began, Ravi Belani, managing partner at Alchemist, reasserted his core… Read More

Powered by WPeMatico

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.

First names, foods and animals have been quite popular lately with founders choosing startup names. Meanwhile, other naming styles are getting more fashionable. We take a look at what’s hot now and what might be in vogue next.