Bunq

Auto Added by WPeMatico

Auto Added by WPeMatico

Amsterdam-based challenger bank Bunq is updating its service with a handful of new features. In addition to Dutch, German and French bank account numbers, existing and new users in Spain can now get a Spanish IBAN.

European IBANs are supposed to work across Europe. Your employer or internet provider can’t force you to get a local IBAN. And yet, that’s rarely the case. When you move to another European country, chances are the first thing you do is that you open a local bank account.

While European fintech companies have teamed up to create a lobbying effort called “Accept my IBAN”, some challenger banks, such as Bunq, are adding the ability to get local bank account numbers as an intermediary fix. Bunq users can also choose to associate IBANs from multiple European countries with their account. You have to pay a one-time fee of €9.99 every time you add a new local IBAN.

Bunq is also drawing inspiration from Revolut, Wise, Vivid Money and others as you’ll soon be able to receive, convert and hold other currencies. For instance, if you’re going to a non-Euro country for an internship, you will be able to receive your salary on your Bunq account. Bunq is starting with USD accounts with plans to add more currencies down the road.

Other new features include the ability to receive reminders the day before a direct debit occurs, a subscription view that lets you view current subscriptions and when they’re set to expire, an improved search feature and the ability to automatically accept direct debits and payment requests from your friends — make sure you set up a limit before enabling that feature.

Bunq recently announced plans to raise $228 million (€193 million) at a $1.9 billion valuation (€1.6 billion). The investment round hasn’t been approved by the Netherlands’ banking regulator just yet. Bunq is currently operating in 29 European markets.

Powered by WPeMatico

Amsterdam-based challenger bank Bunq has been self-funded by its founder and CEO Ali Niknam for several years. But the company has decided to raise some external capital, leading to the largest Series A round for a European fintech company.

The startup is raising $228 million (€193 million) in a round led by Pollen Street Capital. Bunq founder Ali Niknam is also participating in the round — he’s investing $29.5 million (€25 million) while Pollen Street Capital is financing the rest of the round.

As part of the deal, Bunq is also acquiring Capitalflow Group, an Irish lending company that was previously owned by … Pollen Street Capital.

Founded in 2012, Ali Niknam has already invested quite a bit of money into his own company. He poured $116.6 million (€98.7 million) of his own capital into Bunq — that doesn’t even take into account today’s funding round.

But it has paid off as the company expects to break even on a monthly basis in 2021. The company passed €1 billion in user deposits earlier this year. So why is the company raising external funding after turning down VC firms for so many years?

“Everything has a right time. In the beginning of Bunq, it was important to get a laser user focus in the company. Having to also focus on fundraises and the needs of investors distracts. Bunq now is mature enough to start scaling up significantly, so more capital is welcome,” Niknam said.

In particular, the company expects to acquire smaller companies to fuel its growth strategy. Challenger banks have also represented a highly competitive market over the past years in Europe. It’s clear that there will be some consolidation at some point.

Bunq offers bank accounts and debit cards that you can control from a mobile app. It works particularly well if your friends and family are also using Bunq as you can instantly send money, share a bunq.me payment link with other people, split payments and more.

In particular, if you’re going on a weekend trip, you can start an activity with your friends. It creates a shared pot that lets you share expenses with everyone. If you live with roommates, you can also create subaccounts to pay for bills from that account.

The company offers different plans that range from €2.99 per month to €17.99 per month — there’s also a free travel card with a limited feature set. By choosing a subscription-based business model, the startup has a clear path to profitability as most users are paid users.

Powered by WPeMatico

Challenger bank Bunq is adding a new feature that lets you donate to charities directly from the app. In addition to that, Bunq is also in the process of redesigning its app. The company is launching a public beta test to get feedback from its users.

Other fintech startups, such as Revolut and Lydia, have launched donation features in the past. But in those cases, startups have selected a handful of charities.

Bunq has chosen a different approach, as you can create your own donation campaigns in the app. As long your local charity has an IBAN number, you can add it to Bunq’s donation feature. You can even add a local business in case you want to help them stay in business.

You can then invite other people to donate to your charities. You can also track the total amount of your donations, as well as the total donations from the entire Bunq user base.

The company has also been working on the third major version of the app. In order to test it before the public release, Bunq is launching a public beta program. The first build will roll out in the coming weeks.

In order to simplify navigation, Bunq has tried to remove clutter by focusing on one main button on each page. The app will be divided in four main tabs.

The first tab, called “Me,” will feature all your personal information — personal bank accounts, savings goals, etc. On the second tab, called “Us,” you can see information about Bunq, such as total investments and total donations. The third tab features your profile information.

Finally, the fourth tab is a dedicated camera button. It lets you scan invoices and receipts, which could be particularly useful for business customers. I’m not sure a lot of people use that feature, but things could still change before the final release.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

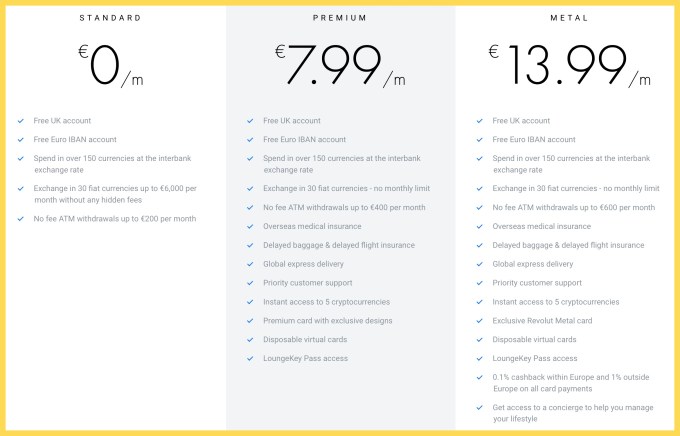

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Fintech startup Bunq is launching a metal card called the Green Card. While some banks offer a cashback program with premium cards, Bunq is offering a special kind of “cashback”. For every €100 spent, Bunq plants a tree. The company has partnered with Eden Reforestation Projects to finance reforestation around the globe.

Manufacturing a metal card isn’t particularly environmentally friendly. That’s why the Green Card expires after six years instead of four years. It is also made of recyclable material (even though I’m not sure it’s that easy to recycle a metal card with a chip, a magnetic stripe and an NFC antenna after it expires).

Other than that, the Green Card works more or less like the Travel Card. While Bunq offers traditional bank accounts, you can order a Travel Card or a Green Card and keep your existing bank account.

The Green Card is a Mastercard without any foreign exchange fee. The company uses the standard Mastercard exchange rate but doesn’t add any markup fee.

While the Green Card is a credit card, it doesn’t work like normal credit cards. You don’t get a direct debit on your bank account once a month to cover your credit line. Instead, you have to open the Bunq app and top up your Bunq account — topping up your account with another card may incur some fees, more details here. If you don’t have enough money on your account, the transaction gets rejected like a debit card.

The Travel Card costs €9.99 to order the card. There’s no monthly fee after that. The Green Card costs €99 per year. Bunq charges €0.99 per ATM withdrawal but you get 10 free withdrawals with the Green Card.

The company is selling a limited edition today with “Founders Edition” engraved in the top right corner but the first batch is nearly sold out:

Powered by WPeMatico

European challenger bank Bunq is announcing a handful of updates today. You now get a better overview of your account with more insights on how you spend money. If you’re going on vacation with someone else, you can now choose to automatically add transactions to a Slice Group. There are also improvements to VAT management for business users.

Slice Groups are shared accounts for owners of the Bunq Travel Card. You can create a group with multiple Bunq users and then add expenses to the group. You can’t add money to a Slice Group directly. It is essentially a group accounting feature that lets you keep track of who paid for what, who has a positive balance and who has a negative balance.

While you could easily add Bunq transactions to a group, you still had to manually add them every time there are some new transactions. You can now turn on AutoSlice, a feature that lets you temporarily add all card transactions to a Slice Group.

In other news, Bunq wants to give you more information about your spending habits. It starts with a new feature called Bunq Insights. As the name suggests, your payments are now automatically categorized so that you can see a breakdown of what you do with your money.

When you travel, Bunq now gives you information about your travel destination, such as the exchange rate as well as tips and tricks for that country. Bunq users can add recommendations for other Bunq users.

And if you’re always wondering if you’re spending too much money after getting paid, Bunq now tries to predict how much money you’ll have left at the end of the month. The company analyzes your past transactions to predict how much you’re going to spend over the coming weeks.

Finally, Bunq is updating AutoVAT for business users who have to deal with VAT in Europe. In addition to setting aside VAT you’ll have to pay back, the app now counts how much VAT you’ve paid so far so that you know how much you can reclaim. By combining these two figures, you get the exact VAT amount for your taxes.

Powered by WPeMatico

Fintech startup Bunq is announcing a handful of new features today, such as a way to track group expenses without creating a joint account, a web app and better Siri integration.

If you usually track vacation expenses and group expenses from your phone, chances are you’ve been using two different products — a mobile app like Splitwise to track group expenses with your friends, and a peer-to-peer payment app to settle up balances.

Bunq is essentially bundling these two features with Slice Groups for owners of the Bunq Travel Card. Given that the Bunq app already lists all your transactions, adding transactions to a group is easier than with your average group payment tracking app.

After adding other people to your Slice Group, each person can add expenses to the group. You get a list of your most recent Bunq transactions and you can add them to a group. You also can add manual transactions in case you paid for something using cash, for instance.

This is just a group accounting feature. When you add a transaction to a Slice Group, your money remains in your account. But you can see who has a positive balance and who has a negative balance.

When you settle up a group, people who owe money get a push notification. They can then tap on the notification and send money from their Bunq account to your friends’ Bunq accounts.

This feature will work particularly well for groups of people who all use the Bunq Travel Card. But it doesn’t fundamentally change how you manage your money with groups.

Bunq now has two tiers of users. Free users get a travel card with an account that they can top up. Paid users get a full-fledged bank account with banking information.

Multiple paid users can already create joint accounts with their roommates or partner. You can then associate your Bunq card with a joint account and spend money from that joint account directly.

So if you have a Bunq Travel Card, Slice Groups are for you. If you have a Bunq bank account, joint accounts are for you.

Revolut doesn’t try to reinvent the wheel, either, as you can only split individual card transactions with other users. It could take a while to settle all transactions after a long vacation. Revolut also lets you create Group Vaults. Those are sub-accounts to put some money aside and invite other people to contribute. But only the admin can withdraw and spend money from those vaults.

N26 has promised Shared Spaces so that you can create sub-accounts and share them with other people. But the feature isn’t live yet.

Lydia’s take on group expenses works more like Bunq’s joint accounts. You can create sub-accounts and share those accounts with other people. Everyone can then top up that account and attach a payment method, such as a payment card or a virtual card in Apple Pay or Google Pay. You also can move expenses from one sub-account to another. When you’re back from vacation, you can associate your card with your personal Lydia account again.

In addition to Slice Groups, Bunq is launching a web interface to access your bank account. It works a bit like WhatsApp’s web app. You scan a QR code with your phone and you can then control the mobile app from a desktop web browser.

Bunq should also work better with Siri. You can now send money using your voice or change card settings. Finally, the startup has also made improvements to its business accounts with a few new features. For instance, you can now automatically put money aside to pay back VAT later down the road.

Powered by WPeMatico