bright health

Auto Added by WPeMatico

Auto Added by WPeMatico

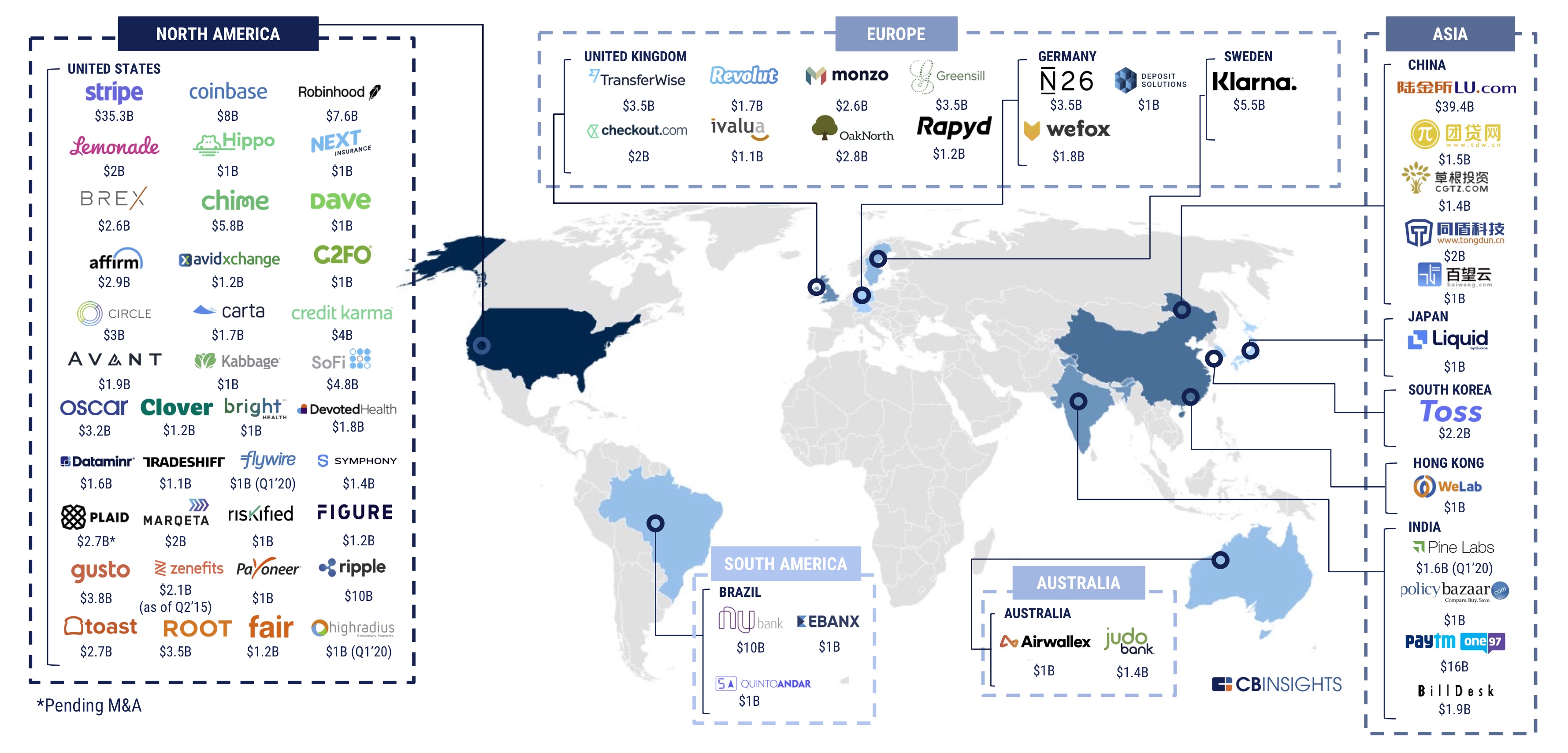

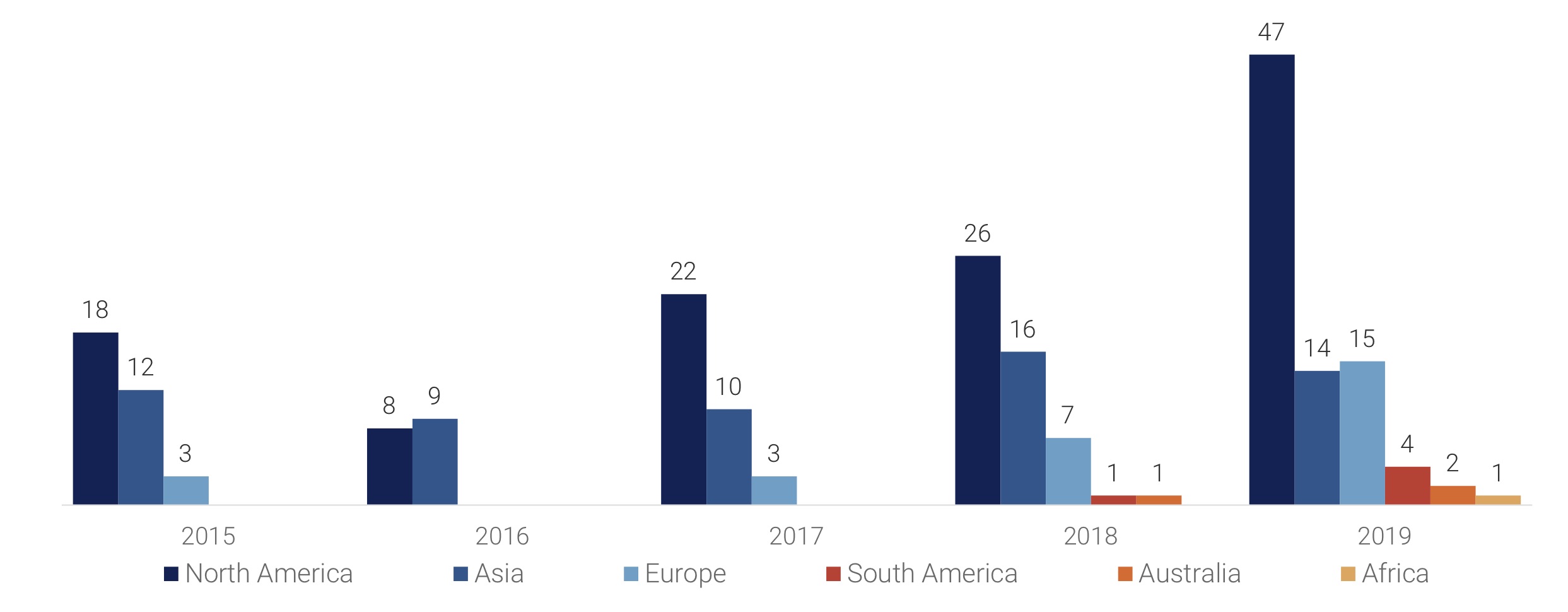

Financial services startups raised less money in 2019 than they did in 2018 as VC firms looked to back late stage firms and focused on developing markets, a new report has revealed.

According to research firm CB Insights’ annual report published this week, fintech startups across the world raised $33.9 billion* in total last year across 1,912 deals*, down from $40.8 billion they picked up by participating in 2,049 deals the year before.

It’s a comprehensive report, which we recommend you read in full here (your email is required to access it), but below are some of the key takeaways.

Early-stage deals dropped to a 12-quarter low as deal share globally shifts to mid- and late-stages (CB Insights)

The fintech market globally today has 67 unicorns as of earlier this month (CB Insights)

2019 saw 83 mega-rounds totaling $17.2B, a record year in every market except Europe

*CB Insights report includes a $666 million financing round of Paytm . It was incorrectly reported by some news outlets and the $666 million raise was part of the $1 billion round the Indian startup had revealed weeks prior. We have adjusted the data accordingly.

Powered by WPeMatico

Despite a number of well-publicized hiccups, venture capitalists are betting another $500 million on health insurance provider Clover Health, TechCrunch has learned.

Existing investor Greenoaks Capital led the round, according to the startup, which confirmed it was closing a new round of capital in the coming weeks. Clover Health has raised a total of $925 million to date, garnering a valuation of $1.2 billion with a $130 million Series D funding in 2017. The company, backed by Alphabet’s venture arm GV, Sequoia Capital, Floodgate, Bracket Capital, First Round Capital and more, declined to disclose its latest valuation.

San Francisco-based Clover Health was founded in 2012 by chief executive officer Vivek Garipalli, the former founder of New Jersey healthcare system CarePoint Health; and Kris Gale, who served as the startup’s chief technology officer until transitioning into an adviser role in December 2017. As part of its latest funding round, the company told TechCrunch it’s promoting Andrew Toy, its chief technology officer since early 2018, to the role of president and CTO. He will also join its board of directors.

Varsha Rao, Airbnb’s former chief operating officer, joined the company in September 2017 as COO.

The tech-enabled health insurer differentiates itself from incumbents by collecting and analyzing health and behavioral data to lower costs and improve medical outcomes for its members. It’s part of a new cohort of heavily funded insurtech startups, including Devoted Health and Bright Health, both of which similarly provide Medicare Advantage plans. Devoted Health, backed by Andreessen Horowitz, raised a $300 million Series B funding round three months ago. Bright Health, for its part, brought in a $200 million Series C in late November at a $950 million valuation. It’s backed by Bessemer Venture Partners, Greycroft, NEA and Redpoint Ventures, among others.

Founded in 2012, Clover Health is years older than its aforementioned counterparts. The business, though supported by top-tier investors and plenty of capital, has struggled in the past to shrink its losses. In 2015, Clover Health posted a net loss of $4.9 million only to increase it 7x the following year to $34.6 million, according to financial documents obtained by Axios. At the time, Clover Health had 20,600 Medicare Advantage members, earning it $184 million in taxpayer revenue. According to reporting from CNBC, the company had initially planned to double its membership base each year but was only able to expand from 20,000 in 2016 to 27,000 in September 2017.

Clover Health currently has 40,000 members in Georgia, New Jersey, Arizona, Pennsylvania, South Carolina, Tennessee and Texas. The business earns roughly $10,000 in revenue per member from the Centers for Medicare and Medicaid Services, or currently about $400 million in annual revenue. As a Medicare Advantage plan, Clover Health makes a majority of its cash from the government.

“Clover’s continuously improving economic fundamentals have allowed us to build sustainably, thoughtfully enter new markets and increase our overall membership by 35 percent during the last 12 months, compared with nationwide growth of 8 percent for Medicare Advantage overall,” the company said in a statement provided to TechCrunch. “This has made Clover one of the fastest growing insurers in [Medicare Advantage] over the past three years. That said, there is much more to accomplish, which is why I am so excited about entering this next phase in our company’s history.”

Powered by WPeMatico

A flurry of digital-first insurers are betting they can surpass industry incumbents with a little help from technology and a lot of help from venture capitalists.

The latest to land a massive check is Bright Health, a Minneapolis-headquartered provider of affordable individual, family and Medicare Advantage healthcare plans in Alabama, Arizona, Colorado, New York City, Ohio and Tennessee. The company, founded by the former chief executive officer of UnitedHealthcare Bob Sheehy; Kyle Rolfing, the former CEO of UnitedHealth-acquired Definity Health; and Tom Valdivia, another former Definity Health executive, has brought in a $200 million Series C.

The funding values Bright Health at $950 million, according to PitchBook — more than double the $400 million valuation it garnered with its $160 million Series B in June 2017. Sheehy, Bright Health’s CEO, declined to comment on the valuation. New investors Declaration Partners and Meritech Capital participated in the round, with backing from Bessemer Venture Partners, Greycroft, NEA, Redpoint Ventures and others. Bright Health has raised a total of $440 million since early 2016.

VCs have deployed significantly more capital to the insurance technology (insurtech) space in recent years. Startups in the industry, long-known for a serious dearth of innovation, have raked in nearly $3 billion in private capital this year. U.S.-based insurtech startups have raised $2 billion in 2018, a record year for the sector and more than double last year’s total.

Deal count, meanwhile, is swelling. In 2016, there were 72 deals conducted in the space, followed by 86 in 2017 and 94 so far this year, again, according to PitchBook’s data.

Oscar Health, the health insurance provider led by Josh Kushner, is responsible for about 25 percent of the capital invested in U.S. insurtech startups this year. The company has raised a total of $540 million across two notable deals in 2018. The first saw Oscar pulling in $165 million at a $3 billion valuation and the second, announced in August, had Alphabet investing a whopping $375 million. Devoted Health, a Waltham, Mass.-based Medicare Advantage startup, followed up with a massive round of its own. The company nabbed $300 million and announced that it would begin enrolling members to its Medicare Advantage plan in eight Florida counties. Devoted is led by Todd Park, the co-founder of Athenahealth and Castlight Health.

Bright Health co-founders Bob Sheehy, CEO; Tom Valdivia, chief medical officer; and Kyle Rolfing, president

VC’s interest in insurtech isn’t limited to healthcare.

Hippo, which sells home insurance plans at lower premiums, officially launched in 2017 and has brought in $109 million to date. Earlier this month the company announced a $70 million Series C funding round led by Felicis Ventures and Lennar Corporation. Lemonade, which is similarly an insurer focused on homeowners, raised $120 million in a SoftBank-led round late last year. And Root Insurance, an app-based car insurance company founded in 2015, itself raised a $100 million Series D led by Tiger Global Management in August. The financing valued the company at $1 billion.

Together, these companies have raised well over $1 billion this year alone. Why? Because building a health insurance platform is incredibly cash-intensive and particularly difficult given the breadth of incumbents like Aetna or UnitedHealth. Sheehy, considering his 20-year tenure at UnitedHealthcare, may be especially well-positioned to disrupt the industry.

The opportunity here for investors and startups alike is huge; the health insurance market alone is forecasted to be worth more than $1 trillion by 2023. Companies that can leverage technology to create consumer-friendly, efficient and, most importantly, reasonably priced insurance options stand to win big.

As for Bright Health, the company plans to use its $200 million infusion to rapidly expand into new markets, planning to triple its geographic footprint in 2019.

“Bright Health has continued to execute at a fast pace towards our goal of disrupting the old health care model that places insurers at odds with providers,” Sheehy said in a statement. “[Its] current high re-enrollment rate shows that consumers are ready for this improved healthcare experience – especially when it is priced competitively.”

Powered by WPeMatico