Brex

Auto Added by WPeMatico

Auto Added by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

First, a big thanks to everyone who took part in the Equity survey, we really appreciated your notes and thoughts. The crew is chewing over what you said, and we’ll roll up the best feedback into show tweaks in the future.

Today, though, we’ve got Danny and Natasha and Chris and Alex back again for our regular news dive. This week we had to leave the Vroom IPO filing, Danny’s group project on The Future of Work and a handwashing startup (?) from Natasha to get to the very biggest stories:

And at the end, we got Danny to explain what the flying frack is going on over at Luckin. It’s somewhere between tragedy and farce, we reckon. That’s it for today, more Tuesday after the holiday!

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Starting today, TechCrunch readers can send an Extra Crunch annual membership as a gift to a friend, family member or co-worker. For a limited time we’re offering the gift at a discounted rate of $99/year (plus tax).

The gifting feature can be found here.

Extra Crunch membership is designed for startup teams, entrepreneurs, investors and business school students, and it includes more than 100 exclusive articles per month:

Extra Crunch membership can save you time time with an exclusive newsletter, no banner ads, Rapid Read mode and our List Builder tool. Annual and two-year members can also save money with discounts on events and access to Partner Perks. Our Partner Perks provide discounted access to services from companies like AWS, Brex, DocSend, Crunchbase, Typeform and more.

Gifting is currently supported in the U.S., Canada, U.K. and select countries in Europe. Purchases can be made through Visa, Mastercard and PayPal in all supported countries, but Amex support is limited to the U.S. and Canada.

If there are other features you’d like to see us add to Extra Crunch, please let us know by leaving a comment on this post or emailing me directly at travis@techcrunch.com.

TechCrunch readers can find the Extra Crunch gifting feature here.

Powered by WPeMatico

Brex, a Silicon Valley fintech darling, has lofty plans to battle big banks —and Stripe.

Code-named “Gemini,” Brex today announced a new product designed to replace and improve the functionality of traditional bank accounts. Brex Cash, as it will be known publicly, is a business cash management account integrated with the Brex Card, a corporate card for startups launched in 2018.

Brex tells us they’ve built the core banking infrastructure from scratch, allowing the company to forgo third-party processing fees and provide a much-needed tech infusion to antiquated banking systems. In partnership with Boston’s Radius Bank, Brex Cash will allow customers to send payments quickly and easily with no transaction fees attached. Rather, Brex plans to reward its users for making or receiving payments using Brex Cash with points redeemable for cash back, travel and air miles. Customers will also receive 1.6% yield on deposits.

It’s not a bank, but in practice, it can replace a bank, says Brex co-founder and co-chief executive officer Henrique Dubugras .

“Our idea is that new businesses —the new Y Combinator companies —we hope a big percent of them never open a bank account,” Dubugras tells TechCrunch.

Brex now has many similarities to a bank. What differentiates it is its lack of physical branches — it’s exclusively digital — and it’s insurance. Traditional banks are insured by the Federal Deposit Insurance Corporation (FDIC), which protects up to $250,000 per depositor. Brex Cash users are protected by the Securities Investor Protection Corporation (SIPC), a nonprofit agency overseen by the U.S. Securities and Exchange Commission that protects up to $500,000 and specializes in protecting customers of brokerage firms from the loss of cash and securities.

We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex? -Brex co-CEO Henrique Dubugras

Additionally, Brex invests its customers’ money in a money market mutual fund of U.S. treasury bonds. “If Brex goes out of business, customers’ money will be safe,” the company writes in a press statement. “The only scenario where money could be lost is if the U.S. government defaults.”

Brex Cash user interface

“It’s not that we are inventing this — this model exists with Fidelity,” says Dubugras. “Fidelity isn’t necessarily a bank — we are bringing that concept to businesses to give lower fees, better interest rates, better experiences and more security.”

Brex, a graduate of the winter 2017 Y Combinator cohort, has quickly become a Silicon Valley success story for the ages. The rapid adoption of its startup credit card, which doesn’t require a personal guarantee, and its ability to issue cards instantly and provide higher limits than other options on the market has attracted thousands of customers and venture capitalists. The business, led by a pair of young Brazilian repeat entrepreneurs, including Dubugras and co-CEO Pedro Franceschi, has collected more than $300 million in equity funding, including a $100 million C-2 financing that valued the company at $2.6 billion earlier this year.

“There will always be customers that are skeptical, but I think by starting out with a card, we built a lot of trust,” Dubugras said. “It was us giving them money instead of them giving us money. A few years in … We think we’ve won a lot of credibility. Before, who was going to give their money to a random-ass startup called Brex?”

In the weeks ahead of TechCrunch Disrupt San Francisco, where Dubugras announced Brex Cash on Wednesday, the CEO told TechCrunch that Brex had no immediate fundraising plans and that they were “waiting for the right time” to raise again. As for what’s next, he said the company is discussing the launch of a debit card and plans to add another 100 employees in the next year, bringing the Brex headcount to 400.

The Brex news follows the launch of Stripe Capital, a new offering from payments behemoth Stripe that will make instant loan offers to customers on its platform, and the announcement of the Stripe Corporate Card. Akin to Brex, Stripe will issue a no-fee, no interest rate credit card intended for Stripe customers. Brex and Stripe, two Y Combinator grads, will go head-to-head in a battle for customers, particularly YC grads looking for friendly financial tools.

Immediately following Stripe’s announcements, the business announced a $250 million funding at a $35 billion valuation. Brex may be following a similar playbook, announcing a major product on the heels of a large capital infusion.

Brex Cash represents a new era for the company. Though the product may be costly for Brex, it opens the business up to thousands more potential customers. Now, any startup, regardless of funding, can create a Brex account to store cash, explains Dubugras, and all companies using Brex Cash will be immediately issued a Brex corporate credit card.

“If you’re starting out, if you don’t have funding yet, you can still receive your payments using Brex,” Dubugras said. “That’s a super big deal for us.”

Brex Cash was built under product lead Ritik Malhotra, who joined the team as part of an acquisition of his startup, Elph. Brex poached the company, which was focused on blockchain infrastructure, right out of YC for an undisclosed amount. In retrospect, the deal looks much more like an acqui-hire of Malhotra, who had the digital payments infrastructure acumen necessary to complete this project.

“It’s an easy way to move money, which is the lifeblood of a business,” Malhotra tells TechCrunch of the new product.

Brex Cash is itself not a cash cow for Brex; rather, the startup makes money on purchases made on its corporate card, in which it charges the merchant, not the customer. This model is particularly beneficial when its customers are spending a lot of money, growing quickly and raising capital. In a downturn, however, this model isn’t as attractive.

Brex seems unconcerned with the possibility of an impending recession. Brex writes that even in downturns, entrepreneurs will start companies and attempt to raise money. The Brex Cash product, regardless of the economy, will help Brex better underwrite Brex Cards, as it gives them better access to a customer’s financial health.

In a battle against Stripe, Brex is at a disadvantage. At only two years old, the company may have garnered a lot of credibility in a short time but it doesn’t have the decade of experience building fintech products that Stripe has and, more importantly, it doesn’t have 10 years of customer loyalty.

Powered by WPeMatico

Sex, despite being one of the most fundamental human experiences, is still one of those businesses that some advertisers reject, banks are hesitant to financially support and some investors don’t want to fund.

Given how sex is such a huge part of our lives, it’s no surprise founders are looking to capitalize on the space. But the idea of pleasure versus function, plus the stigma still associated with all-things sex, is at the root of the barriers some startup founders face.

Just last month, Samsung was forced to apologize to sextech startup Lioness after it wrongfully asked the company to take down its booth at an event it was co-hosting. Lioness is a smart vibrator that aims to improve orgasms through biofeedback data.

Sextech companies that relate to the ability to reproduce or, the ability to not reproduce, don’t always face the same problems when it comes to everything from social acceptance to advertising to raising venture funding. It seems to come down to the distinction between pleasure and function, stigma and the patriarchy.

This is where the trajectories for sextech startups can diverge. Some startups have raised hundreds of millions from traditional investors in Silicon Valley while others have struggled to raise any funding at all. As one startup founder tells me, “Sand Hill Road was a big no.”

Powered by WPeMatico

Welcome to this transcribed edition of The Operators. TechCrunch is beginning to publish podcasts from industry experts, with transcriptions available for Extra Crunch members so you can read the conversation wherever you are.

The Operators features insiders from companies like Airbnb, Brex, Docsend, Facebook, Google, Lyft, Carta, Slack, Uber, and WeWork sharing their stories and tips on how to break into fields like marketing and product management. They also share best practices for entrepreneurs on how to hire and manage experts from domains outside their own.

This week’s edition features Airbnb’s Global Product Director of Customer and Community Support Platform Products, Andy Yasutake, and Carta’s Head of Enterprise Relationship Management, Jared Thomas.

Airbnb, one of the most valuable private tech companies in the world, has millions of hosts who trust strangers (guests) to come into their homes and hundreds of millions of guests who trust strangers (hosts) to provide a roof over their head. Carta, a $1 Billion+ company formerly known as eShares, is the leading provider of cap table management and valuation software, with thousands of customers and almost a million individual shareholders as users. Customers and users entrust Carta to manage their investments, a very serious responsibility requiring trust and security.

In this episode, Andy and Jared share with Neil how companies like Airbnb, Carta, and LinkedIn think about customer service, how to get into and succeed in the field and tech generally, and how founders should think about hiring and managing the customer support. With their experiences at two of tech’s trusted companies, Airbnb and Carta, this episode is packed with broad perspectives and deep insights.

Neil Devani and Tim Hsia created The Operators after seeing and hearing too many heady, philosophical podcasts about the future of tech, and not enough attention on the practical day-to-day work that makes it all happen.

Tim is the CEO & Founder of Media Mobilize, a media company and ad network, and a Venture Partner at Digital Garage. Tim is an early-stage investor in Workflow (acquired by Apple), Lime, FabFitFun, Oh My Green, Morning Brew, Girls Night In, The Hustle, Bright Cellars, and others.

Neil is an early-stage investor based in San Francisco with a focus on companies building stuff people need, solutions to very hard problems. Companies he’s invested in include Andela, Clearbit, Kudi, Recursion Pharmaceuticals, Solugen, and Vicarious Surgical.

If you’re interested in starting or accelerating your marketing career, or how to hire and manage this function, you can’t miss this episode!

The Operators brings experts with experience at companies like Airbnb, Brex, Docsend, Facebook, Google, Lyft, Carta, Slack, Uber, WeWork, etc. to share insider tips on how to break into fields like marketing and product management. They also share best practices for entrepreneurs on how to hire and manage experts from domains outside their own.

In Episode 5, we’re talking about customer service. Neil interviews Andy Yasutake, Airbnb’s Global Product Director of Customer and Community Support Platform Products, and Jared Thomas, Carta’s Head of Enterprise Relationship Management.

Neil Devani: Hello and welcome to the Operators, where we talk to entrepreneurs and executives from leading technology companies like Google, Facebook, Airbnb, and Carta about how to break into a new field, how to build a successful career, and how to hire and manage talent beyond your own expertise. We skip over the lofty prognostications from venture capitalists and storytime with founders to dig into the nuts and bolts of how it all works here from the people doing the real day to day work, the people who make it all happen, the people who know what it really takes. The Operators.

Today we are talking to two experts in customer service, one with hundreds of millions of individual paying customers and the other being the industry standard for managing equity investments. I’m your host, Neil Devani, and we’re coming to you today from Digital Garage in downtown San Francisco.

Joining me is Jared Thomas, head of Enterprise Relationship Management at Carta, a $1 billion-plus company after a recent round of financing led by Andreessen Horowitz. Carta, formerly known as eShares, is the leading provider of cap table management and valuation software with thousands of customers and almost a million individual shareholders as users. Customers and users trust Carta to manage their investments, a very serious responsibility requiring trust and security.

Also joining us is Andy Yasutake, the Global Product Director of Customer and Community Support Platform Products at Airbnb, one of the most valuable private tech startups today. Airbnb has millions of hosts who are trusting strangers to come into their homes and hundreds of millions of guests who are trusting someone to provide a roof over their head. The number of cases and types of cases that Andy and his team have to think about and manage boggle the mind. Jared and Andy, thank you for joining us.

Andy Yasutake: Thank you for having us.

Jared Thomas: Thank you so much.

Devani: To start, Andy, can you share your background and how you got to where you are today?

Yasutake: Sure. I’m originally from southern California. I was born and raised in LA. I went to USC for undergrad, University of Southern California, and I actually studied psychology and information systems.

Late-90s, the dot com was going on, I’d always been kind of interested in tech, went into management consulting at interstate consulting that became Accenture, and was in consulting for over 10 years and always worked on large systems of implementation of technology projects around customers. So customer service, sales transformation, anything around CRM, as kind of a foundation, but it was always very technical, but really loved the psychology part of it, the people side.

And so I was always on multiple consulting projects and one of the consulting projects with actually here in the Bay Area. I eventually moved up here 10 years ago and joined eBay, and at eBay I was the director of product for the customer services organization as well. And was there for five years.

I left for Linkedin, so another rocket ship that was growing and was the senior director of technology solutions and operations where I had all the kind of business enabling functions as well as the technology, and now have been at Airbnb for about four months. So I’m back to kind of my, my biggest passion around products and in the customer support and community experience and customer service world.

Powered by WPeMatico

Silicon Valley has many dreams. One dream — the Hollywood version anyway — is for a down-and-out founder to begin tinkering and coding in their proverbial garage, eventually building a product that is loved by humans the world over and becoming a startup billionaire in the process.

The more prosaic and common version of that Valley dream though is to join an early-stage company right before its growth kicks into high gear. Sure, those early employees might only have a smidgen of equity, but that equity could be worth a whole heck of a lot if they join the right startup.

Every startup has a window of opportunity, a timeframe in which early employees can join while the stock option strike prices are low and the equity grants are high. Join before the big uptick in valuation, and suddenly what might have been an otherwise nice couple of hundred K dollars in the coming years becomes actually, well, in the Bay Area, a reasonably-sized domicile.

Yet, that opportune window seems to be shrinking in size, making it harder for potential startup employees to nail the timing necessary to garner their own best financial return.

For every Roblox, which as we profiled in-depth this week, took almost two decades to reach its current apotheosis, there is a Brex, which seems to reach unicorn status in no time at all. And such stories — while certainly anecdotal — seem to be more commonplace than ever.

Part of the reason for that fast early valuation growth is that Silicon Valley has simply learned how to grow even faster, even earlier. As venture capitalist Reid Hoffman and Chris Yeh discuss in their book Blitzscaling, there are now frameworks and tried-and-true techniques to not just grow a startup, but to grow it at a dizzying rate. Through better marketing channels, growth strategies, and product development, we have indeed made progress at cutting at least some of the time to better valuations.

That rapid transformation from nothing to everything though gives very little time for early employees to discover a startup through the grapevine when the financial conditions are still interesting.

Half a decade ago, I wrote about the plight of early employees in an article I entitled “The Problem with Founders.” I wrote then that:

The secret of Silicon Valley is that the benefits of working at a startup accrues almost entirely to the founders, and that’s why people repeat the advice to just go start a business. There is a reason it is hard to hire in Silicon Valley today, and it isn’t just that there are a lot of startups. It’s because engineers and other creators are realizing that the cards are stacked against them unless they are the ones in charge.

My reasoning then was simple: early employees take on pretty much just as much risk as their founders do, but for a fraction of the equity. Now, with startups jumping to unicorn status in sometimes as short as a handful of months, that risk-reward ratio seems to be even more off-kilter for those early employees.

And it doesn’t just have to be a Brex -scale transformation either. The rapid increase in the size and valuation of series A rounds of financing the past three years means that engineers and salespeople who might have an employee number in the low double digits are suddenly seeing their options struck at a couple of hundred million in valuation. Exits, meanwhile, aren’t suddenly getting richer to compensate.

I started to notice this pattern over the past few weeks in the course of several conversations with software engineering friends of mine who had gotten excited about very early-stage companies — say, just a handful of employees — but who walked away from their offer letters due to already sky-high company valuations.

Now, there is an argument to be made that joining these sorts of companies is precisely where the best opportunities lie. Sure, the valuations are already high, but these are startups with the financial resources and the backing that might allow them to compete effectively. So maybe the equity is smaller and more expensive, but ultimately, if the startup is more likely to be successful, the expected value function might actually be favorable.

Maybe. Yet it is also hard to see how these startups, which despite their rich valuations have barely laid any foundation for success, are a safer bet than a similarly-valued startup with years of experience under its belt and a growth strategy based upon dependable results. Even worse, early employees are perhaps taking even more financial risk, since the preference stack of the venture capital could mean that smaller exits are particularly unfavorable to them.

Plus, the shrinking opportunity window for leading startups means that the difference in financial outcome between two early employees — what could be millions of dollars upon an exit — could have been decided based on who joined the week before the other. That doesn’t seem fair or right, but is increasingly widespread in our industry.

As with most macroeconomic structural changes, there’s not much for anyone to do. Founders aren’t going to take lower valuations or less money just to make the lives of their early employees a bit more rosy, and certainly venture capitalists aren’t going to lowball their offers in a hyper-competitive investment environment. Indeed, the very excitement of a sudden unicorn may be the best attraction for candidates to hear a startup’s pitch and ultimately join.

But when it comes to that Silicon Valley dream of a nice house from a decent return on exit, it’s getting narrower and less widely-distributed. Blitzscaling is making a lot of people a lot of wealth, but early employees? Not so much.

Powered by WPeMatico

William Hockey, co-founder, chief technology officer and president of the fast-growing fintech business Plaid, will step down next week, TechCrunch has learned.

The former Bain associate (pictured above left) co-founded the startup in 2012 alongside chief executive officer Zach Perret. Today, the San Francisco-based company employs 300 with additional offices in Salt Lake City and New York.

Plaid has confirmed the news, stating that Hockey will remain on the company’s board of directors.

“This conclusion was neither a rash nor a recent decision,” Hockey writes in a blog post shared with TechCrunch. “Over the past couple of years, I have known that there would come a point at which I would choose to move to a purely strategic and advisorial role.”

Most companies should be constantly running running at least one exec search. Post-product/market fit, the limiting factor to scale generally derives from some version of not having enough great leaders.

— Zachary Perret (@zachperret) June 18, 2019

Plaid builds infrastructure that allows consumers to interact with their bank account on the web, powering a number of third-party applications, like Venmo, Robinhood, Coinbase, Acorns and LendingClub. It rose to prominence recently, closing a $250 million Series C investment at a $2.65 billion valuation late last year. The deal was led by famed venture capitalist and author of the Internet Trends report Mary Meeker, who’s joined the startup’s board of directors.

In total, Plaid has secured $310 million in venture capital funding from Andreessen Horowitz, Index Ventures, Norwest Venture Partners, Coatue Management, Goldman Sachs, NEA, Spark Capital and others.

Plaid has integrated with 15,000 banks in the U.S. and Canada and says 25% of people living in those countries with bank accounts have linked with Plaid through at least one of the hundreds of apps that leverage Plaid’s application program interfaces (APIs) — an increase from 13% last year. Last month, the company launched its fintech platform in the U.K.

“As we’ve done in the U.S., Plaid will become the foundation for that growth by providing access to a financial network that allows developers to deliver the experience users expect from their financial apps,” the company wrote in a blog post.

TechCrunch participated in a panel discussion with Hockey and Brex CEO Henrique Dubugras last month, in which Hockey gave no indication of impending plans to leave the business. In fact, taking off just as Plaid amps up its global expansion efforts and accelerates growth is strange timing for a founder to depart.

Oftentimes, when a startup co-founder steps down from the C-suite, it’s to make room for a more experienced executive to lead the company through periods of fast growth. Recently, for example, Lime announced its co-founder Toby Sun would transition out of the CEO role to focus on company culture and R&D. Brad Bao, a Lime co-founder and longtime Tencent executive, assumed chief responsibilities.

Other times, it comes amid turmoil. Mike Cagney’s departure from SoFi, of course, is an example of this. One month after reports of a sexual harassment and wrongful termination lawsuit against the online lending business surfaced, SoFi announced Cagney would step down.

In Hockey’s case, the move was planned and calculated, he said. Plaid chief operating officer Eric Sager, who joined earlier this year, Perret and other executives will take over engineering and product reports, among Hockey’s other responsibilities.

“In tech, it has historically been taboo to talk about founders or executives transitioning to different roles inside companies,” Hockey writes. “Leadership transitions need to become a bedrock of any company that desires to endure across decades.”

Powered by WPeMatico

Brex, the fintech business that’s taken the startup world by storm with its sought after corporate card tailored for entrepreneurs, is raising millions in Series D funding less than a year after it launched, TechCrunch has learned.

Bloomberg reports Brex is raising at a $2 billion valuation, though sources tell TechCrunch the company is still in negotiations with both new and existing investors. Brex didn’t immediately respond to requests for comment.

Kleiner Perkins is leading the round via former general partner Mood Rowghani, who left the storied venture capital fund last year to form Bond alongside Mary Meeker and Noah Knauf. As we’ve previously reported, the Bond crew is still in the process of deploying capital from Kleiner’s billion-dollar Digital Growth Fund III, the pool of capital they were responsible for before leaving the firm.

Bond, which recently closed on $1.25 billion for its debut effort and made its first investment, is not participating in the round for Brex, sources confirm to TechCrunch. Bond declined to comment.

Brex, a graduate of Y Combinator’s winter 2017 cohort, has raised $182 million in VC funding, reaching a valuation of $1.1 billion in October 2018 three months after launching its corporate card for startups and less than a year after completing YC’s accelerator program.

Most recently, Brex attracted a $125 million Series C investment led by Greenoaks Capital, DST Global and IVP. The startup is also backed by PayPal founders Peter Thiel and Max Levchin, and VC firms such as Ribbit Capital, Oneway Ventures and Mindset Ventures, according to PitchBook.

The company’s pace of growth is unheard of, even in Silicon Valley where inflated valuations and outsized rounds are the norm. Why? Brex has tapped into a market dominated by legacy players in dire need of technological innovation and, of course, startup founders always need access to credit. That, coupled with the fact that it’s capitalized on YC’s network of hundreds of startup founders — i.e. Brex customers — has accelerated its path to a multi-billion-dollar price tag.

Brex doesn’t require any kind of personal guarantee or security deposit from its customers, allowing founders near-instant access to credit. More importantly, it gives entrepreneurs a credit limit that’s as much as 10 times higher than what they would receive elsewhere.

Investors may also be enticed by the fact the company doesn’t use third-party legacy technology, boasting a software platform that is built from scratch. On top of that, Brex simplifies a lot of the frustrating parts of the corporate expense process by providing companies with a consolidated look at their spending.

“We have a very similar effect of what Stripe had in the beginning, but much faster because Silicon Valley companies are very good at spending money but making money is harder,” Brex co-founder and chief executive officer Henrique Dubugras told me late last year.

Stripe, for context, was founded in 2010. Not until 2014 did the company raise its unicorn round, landing a valuation of $1.75 billion with an $80 million financing. Today, Stripe has raised a total of roughly $1 billion at a valuation north of $20 billion.

Dubugras and Brex co-founder Pedro Franceschi, 23-year-old entrepreneurs, relocated from Brazil to Stanford in the fall of 2016 to attend the university. They dropped out upon getting accepted into YC, which they applied to with a big dreams for a virtual reality startup called Beyond. Beyond quickly became Brex, a name in which Dubugras recently told TechCrunch was chosen because it was one of few four-letter word domains available.

Brex’s funding history

March 2017: Brex graduates Y Combinator

April 2017: $6.5M Series A | $25M valuation

April 2018: $50M Series B | $220M valuation

October 2018: $125M Series C | $1.1B valuation

May 2019: undisclosed Series D | ~$2B valuation

In April, Brex secured a $100 million debt financing from Barclays Investment Bank. At the time, Dubugras told TechCrunch the business would not seek out venture investment in the near future, though he did comment that the debt capital would allow for a significant premium when Brex did indeed decide to raise capital again.

In 2019, Brex has taken steps several steps toward maturation.Recently, it launched a rewards program for customers and closed its first notable acquisition of a blockchain startup called Elph. Shortly after, Brex released its second product, a credit card made specifically for ecommerce companies.

Its upcoming infusion of capital will likely be used to develop payment services tailored to Fortune 500 business, which Dubugras has said is part of Brex’s long term plan to disrupt the entire financial technology space.

Powered by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

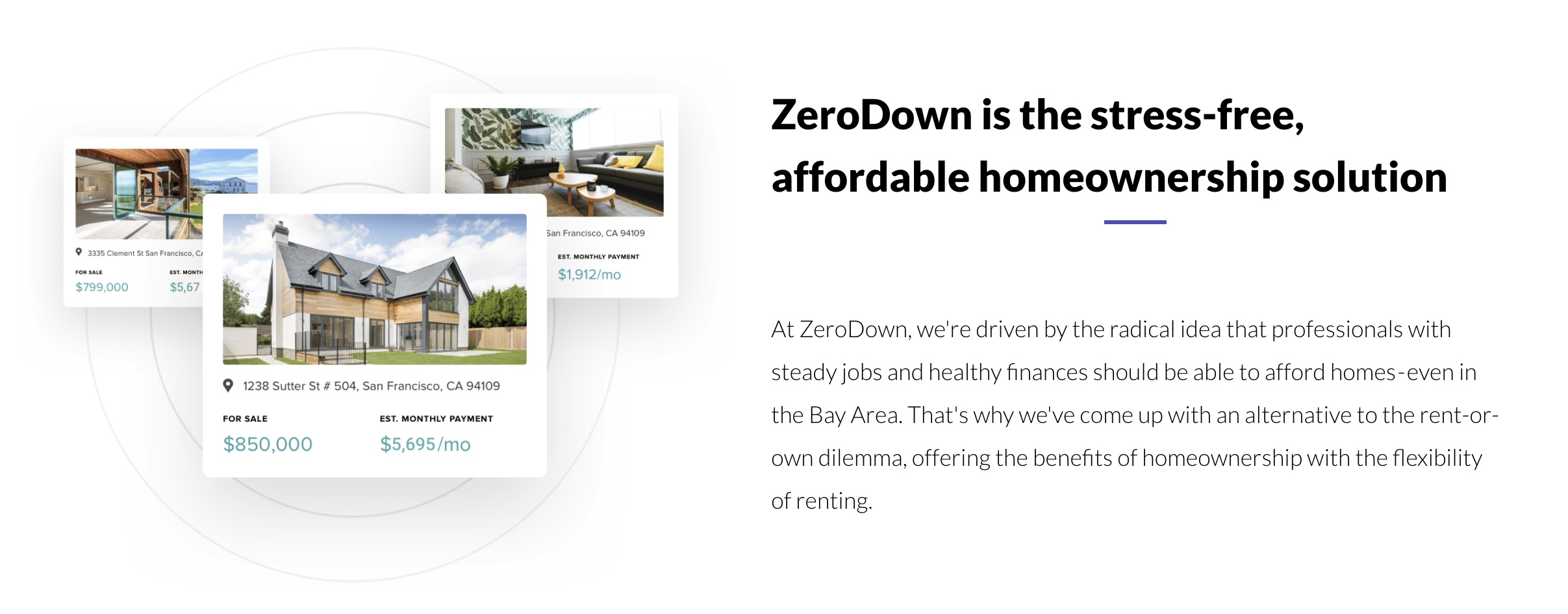

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico

Startups supporting startups are blazing a new trail with support from venture capitalists.

Co-working spaces like The Wing and The Riveter raked in funding rounds this year, as did Brex, the provider of a corporate card built specifically for startups. Now Carta, which helps companies manage their cap tables, valuations, portfolio investments and equity plans, has announced an $80 million Series D at a valuation of $800 million. The company, formerly known as eShares, raised the capital from lead investors Meritech and Tribe Capital, with support from existing investors.

The round brings Carta’s total funding to $147.8 million. Its existing investors include Spark Capital, Menlo Ventures, Union Square Ventures and Social Capital, though the latter didn’t participate in the Series D funding. Tribe Capital, however, is a new venture capital firm launched by Arjun Sethi, who previously led Social Capital’s investment in Carta, Jonathan Hsu and Ted Maidenberg, a trio of former Social Capital partners who exited the VC firm amid its transition from a traditional VC fund to a technology holding company. Tribe is said to be in the process of raising its own $200 million debut fund.

Founded in 2012 by Henry Ward (pictured), the Palo Alto-based company plans to use the latest investment to develop their transfer agent and equity administration products and services to better support startups transitioning into public companies. It also will launch additional products for investors to collect data from their portfolio companies and to manage their back office.

“We’ve come this far by changing how ownership management works for private companies—popularizing electronic securities and cap table software, combined with audit-ready 409As,” Ward wrote in an announcement. “But our ambitions go far beyond supporting privately-held, venture-backed companies.”

Carta, which counts Robinhood, Slack, Wealthfront, Squarespace, Coinbase and more as customers, currently manages $500 billion in equity. This year, Carta expanded its headcount from 310 employees to 450 employees, launched board management and portfolio insights products and completed a study in partnership with #Angels that highlighted the major equity gap female startup employees are victim to.

The study, released in September, revealed that women own just 9 percent of founder and employee startup equity, despite making up 35 percent of startup equity-holding employees. On top of that, women account for 13 percent of startup founders, but just 6 percent of founder equity — or $0.39 on the dollar.

Powered by WPeMatico