board of directors

Auto Added by WPeMatico

Auto Added by WPeMatico

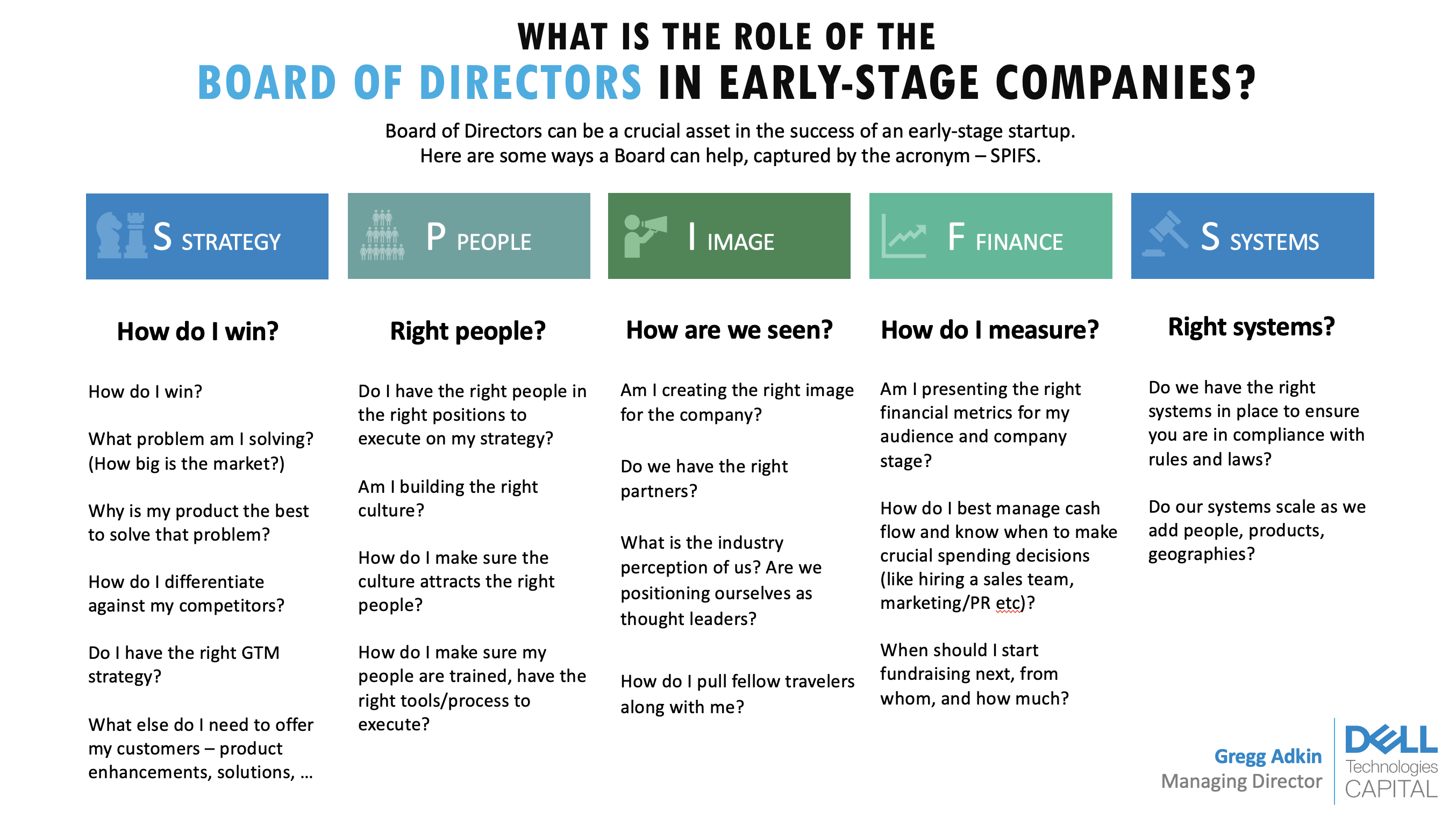

What’s the board’s role in an early-stage startup?

Startup founders frequently ask me about the role of a board of directors. A board can be a crucial asset in an early-stage startup.

Here’s a framework for how it can help drive success at your company: Strategy, People, Image, Finance and Systems for compliance, or “SPIFS.”

The board of directors helps with governance of the company. U.S. law requires that any company have one, though does not require how big it should be. By generic definition, the board of directors consists of elected individuals that represent shareholders. It is the governing body that provides company oversight and helps set business policy and strategy.

On a more practical level and in a startup environment, the board can aid in creating a successful business strategy, putting together the right management team, developing branding, building good financial habits, and avoiding legal and compliance issues. The needs and composition of the board will change depending on the startup’s stage, management and financing history (e.g., if there are preferred shareholders, investors that require a board seat and more).

Investors often ask founders about their board: It says a lot about their character, their judgment and their willingness to be challenged.

Investors often ask founders about their board for two reasons. First, it says a lot about their character, their judgment and their willingness to be challenged. The founder can typically choose who is on their board (through careful selection of investors and advisers) and negotiate a board structure they prefer.

Typically, a healthy board will have a good balance between common shareholders, preferred shareholders and independents. It also helps investors and analysts understand who will ask critical questions and give important advice to the company’s executive management, especially when the going gets tough (it inevitably does!).

After 20 years as a venture capitalist and board member, I boiled down the value of a board into five main pieces under the acronym SPIFS: Strategy, People, Image, Finance and Systems for compliance.

Image Credits: Dell Technologies Capital

Setting business strategy is one of the main ways that the board helps founders, especially if it’s their first time running a business. It is a valuable sounding board for validating that you have taken a sober account of the market and have the right plan to develop your product and acquire customers.

The board should ask these questions when guiding founders through setting strategy:

Powered by WPeMatico

For many companies in the United States, a board of directors is a fact of doing business. While sole proprietorships and LLCs are not obligated to have one, C and S corporations must. The board’s goal is to ensure the best is done for the company and its shareholders. While many entrepreneurs see board meetings as a chore, they can be a powerful tool if used well.

While board meetings usually happen quarterly, it’s good practice to keep the conversation going in between them. Sending a monthly email update to the board offers multiple advantages:

When meeting online, founders should pause often and regularly ask if there are questions — even if moments of silence feel awkward at times — to give directors a better opportunity to speak up.

Board members can also be solicited on an ad-hoc basis — founders should keep in mind that board members are here to help the company. If you have doubts about a project decision or want a second, informed opinion, reach out to a board member. This is especially true of directors who have expertise on a specific topic. A quick five-minute call can be a game changer.

Being a founder can be a lonely experience because it can be difficult to discuss sensitive matters with the team. Board members should sign nondisclosure agreements, allowing entrepreneurs to share confidential information and get a different perspective on things.

Founders should make sure to regularly discuss business goals to ensure they reach their next round of funding. Because the industry landscape or economy evolved or the competition stepped up, investors may reconsider their expectations to further fund the company.

Powered by WPeMatico

The pandemic forced companies around the world to adjust to a “new normal,” which caused many leaders to pivot their business strategies and adopt new technologies to continue operations. In a time of chaos and change, there is no senior leader that can navigate this sort of change better than a CTO.

Not only do CTOs understand the ever-changing tech landscape, they also provide invaluable insights to help organizations go beyond traditional IT conversations and leverage technology to successfully scale businesses.

Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

There are now more reasons than ever to consider adding a CTO to your board. As a CTO myself, I know how important and impactful it can be to have technical-minded leaders on a company’s board of directors. At a time when companies are accelerating their digital transformation, it’s critical to have diverse technical perspectives and people from varying backgrounds, as transformations are a mix of people, process and technology.

Drawing on my experience on Lightbend’s board of directors, here are five hidden benefits of making space at the table for a CTO.

Currently, most boards of directors are composed of former CEOs, CFOs and investors. While such executives bring vast experience, they have very specific expertise, and that frequently does not include technical proficiency. In order for a company to be successful, your board needs to have people with different backgrounds and expertise.

Inviting different perspectives forces companies out of the groupthink mentality and find new, creative solutions to their problems. Diverse perspectives aren’t just about the title –– racial ethnicity and gender diversity are clearly a play here as well.

For a product-led company, having a CTO who has been close to product development and innovation can bring deep insights and understanding to the boardroom. Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

Powered by WPeMatico

Much has been made about the roles and responsibilities of board members these days. This is especially true in the venture-backed startup world where there is an intimate and complex relationship between entrepreneurs and investors. With increasing scrutiny and growing pressure for accountability, the role of a board member has been thrust into the spotlight.

I was fortunate to begin my service as a board member early in my career. For the past 20 years, I’ve had the privilege to serve on boards of companies of many shapes and sizes, ranging from startups to publicly traded companies and everything in between. As I reflect on those experiences, I first have to express my deep gratitude to all the CEOs, management teams and boards that I have had the fortune to work with. I’ve certainly grown enormously through each one of those experiences.

My biggest observation is that these varied companies need very different board members. The nature of the business and the stage of the company define “value-added” as a director. That said, I have found that a board member can create value in a way that transcends the specifics of each company and its leaders. I write this post to try to abstract the essence of this very privileged role and share my experiences with a broader ecosystem. I also hope this can serve as a guide to entrepreneurs who are selecting investors and constructing boards.

In that context, it is important to realize the peculiar nature of board directors. Our role, as such, is to help the company create greater shareholder value. Some might define that as being the “CEO’s boss.” Without a doubt, that is an oversimplification, or perhaps a misconception, of a board member’s duties. We are not the CEO’s boss. The role of the collective board is to be an advisor to the CEO and the management team, which, in some corner cases, is called upon to encourage changes in that management team. But, the relationship between a board and the company’s leadership is much more subtle in nature and is worthy of deeper inspection.

In venture communities, we often oscillate between two extreme views of the role of a board member. One view is that a board is there to be “chief cheerleaders.” That view posits that a board member is there to support the CEO and the founders of a company, to “add value” in the context of tips and advice, introductions, recruiting efforts, marketing, PR and general cheering. In extreme cases, that has even led to the abdication of voting rights and governance to the founders and CEO. While this view is tempting in an era where founders and CEOs are the decision-makers for which VCs they elect as investors in their company, it’s also a very short-sighted view of the role. There is no doubt that a director should be helpful and, as a company leader, it might feel great to have an investor “at your service.” But, is an entrepreneur simply purchasing a brand and adding a helper or are they genuinely deriving shareholder value by having a blind supporter on the board?

The opposite extreme is the view that a board member should instruct the CEO and the management team on how to run the company and ultimately be the “judge and jury” of the management team’s performance. This relationship is also fraught with risk. CEOs, founders and management teams are far more versed in the business that they are operating than any investor. They know the internal details, the nuances of the business, the products, the market and the competitive dynamics. By and large, they are far better equipped to run the business than any board member could be.

I have personally found that the healthiest relationship between a board director and the CEO is one that is peer-like. The board member’s function in that context is one where, as a good friend would, they are supportive but candid and transparent about their view on the state of the company, its challenges and its opportunities. In doing so, the dialog that occurs will be one which is genuine in nurturing the company rather than a cat-and-mouse game or a love-fest.

One of the analogies I often use for the role of a board is that of being a “mirror” to the management team. Entrepreneurs, by their nature, live on a roller-coaster ride that is matching their startup’s journey. Their perception of the business is often an amplification of the current state of the business. The highs are often more optimistic than the business might really deserve and the lows are often much lower than they should be. The board should reflect a snapshot of the reality of the business. All businesses, both the most successful and the somewhat troubled, involve a lot of sausage-making. There are aspects that are not working well that shouldn’t be brushed aside or ignored, but should be focal points of improvement. Conversely, when things aren’t going well, entrepreneurs can often be too critical of their own business.

By placing things in the context of other experiences, the board member should aid the entrepreneurs in “normalizing” the state of the company. Sometimes, reminding the leadership teams that they are neither the masters of the universe nor a losing locker room makes all the difference. All too often, boards have tendencies of “jumping on the pile” and accentuating the entrepreneur’s perception of the business for better or worse — which ultimately provides little value.

Command of the context is one of the most important values boards can provide. While entrepreneurs have the deepest knowledge of their own business, they do not have the benefit of having seen many other companies that are like them. Especially in the startup universe where there are so many common patterns that recur regularly, the ability to provide the comparative context is very valuable. These recurring patterns exist in almost every aspect of a business. Whether it’s in strategy, go-to-market, executive hiring and firing, market adoption versus monetization, and many other attributes, there are lessons that a new business can learn, both positively or negatively, from others who have walked in their shoes earlier on. Not all of those lessons apply. Each business is a snowflake — unique in its own way. But, for the leadership of a company, being able to compare and contrast the situations with those that have come before can be of enormous value in shaping the right business decisions.

It is also incredibly important for boards to encourage long-term thinking. Most management teams think their job is to deliver the short-term quarter-by-quarter gains to appease the board. To some extent, yes, but it’s actually the board’s job to encourage and allow the company to think long-term. For company leaders, it is particularly more tricky because their own business is right there, staring them in the face. A “value-added” board should help in thinking about the longer-term implications of a company’s decisions. Not so much in just the burning issue of the moment, but in the relative impact of that decision on the company’s long-term prospects. The journey of a board member often spans many years, sometimes more than a decade. It’s important to have that in mind when dispensing advice.

My friend Peter Fenton at Benchmark is extremely effective at this. Peter will almost always leave the ultimate decisions to the CEO he’s working with, but he has a way of using compelling examples from the many successful companies he has been involved with as anecdotes to help steer the CEOs to the right decisions. The success stories have a powerful sway on the thinking of CEOs and they are rich in context because they demonstrate actual case studies rather than hypotheticals.

Especially for a young business, the ability to tap into a board’s network can be of massive value. Networks exist in almost every context to help recruit the right people, to construct impactful business development relationships, to provide strategic advice or deliver customers or investors. The list of valuable networks is endless. A board member should come equipped with those networks and generously and tirelessly provide entrepreneurs with access to them. Surely, not all of these networks are equally useful but, if accessed correctly, some can have transformational effects on a company’s prospects. Board members should be able to tap into these networks at the right time (careful not to over-expose startups to networks that are premature, or useless in the moment). And, these networks should be fresh and relevant.

One of the beauties of rich networks is that they often provide access to the person that is best suited to give the best advice to the entrepreneur. Many VCs are “jacks-of-all-trades.” The best advice on specific topics should come from a true expert. The director’s job is to make sure that advice is available at the right time. With a good board, the right person is always one call away.

The master of the universe of networks is Reid Hoffman. I serve on Aurora’s board with him and no one wields a network quite like Reid. His ability to bring just the right person into the dialog at just the right moment is amazing. For the founder of LinkedIn, that’s no surprise, really. He is truly as good as they come.

Feedback during board meetings is actually a fraction of the ways in which board members should provide value. In fact, a board member that surfaces only at the board meetings is shirking their duties. The meetings themselves are valuable because they represent an opportunity to bring together the collective thinking and contrast views, but not to regurgitate “state of the business” information that should be disseminated and absorbed outside of that venue. It’s also the case that many of the most significant conversations between a board member and a CEO occur in private, where conversations can have continuity and consistency achievable only in the context of a 1:1.

The most effective board members have multiple conversations with their CEO and executive team in between board meetings. This allows them to be current and relevant to the company rather than getting caught up in the usual business platitudes that are commonplace in board meetings. (If I had a nickel for every time I heard the phrase “companies are bought and not sold” in a board meeting…).

The best at this was Coach — the great Bill Campbell . When he and I served on Opsware’s board, I would visit Marc and Ben from time to time in their offices. Without fail, Bill would always be there. He took context to a new level. What all that context gave Bill was an incisive ability to understand what the real issues were and how they should be addressed. He truly became a coach to the CEO.

Startups are real time. Issues surface every day and every moment. Leaders seek “micro-advice” in the moment, all the time. A board member should have the availability to respond to entrepreneurs when needed. Sometimes that means calls at 10 pm. At other times, that means five or 10 text messages in a day. Sometimes these “micro-advice” moments are extremely impactful: how to deal with a particular customer, how to close a candidate, whether or not to fire someone. At other times, they are not pivotal. However, they often provide the CEO with the ammunition to make a tough decision, or simply the ability to offer a moment of empathy. A director’s ability to be available in those key moments is incredibly valuable and irreplaceable. Providing that level of availability can sometimes be a challenge for board members — after all, we all have action-filled busy days. But, the board member who is able to find the time earns the right to become the proverbial “first call” for the entrepreneur. Such “micro-advice” also provides the board members with the ability to be relevant at all times to the leadership team of a company. The moments when CEOs need another perspective don’t show up neatly five times per year at pre-scheduled times.

Particularly with VC-rich boards, I have found that all-too-often we enjoy hearing ourselves talk perhaps a bit too much. Sometimes, the quantity of airtime is confused with value. A board member should recognize that their counterpart can only absorb a finite amount of insight at any given time. My rule of thumb is a board member can, at most, provide two or three key insights at a board meeting. More than that, and it’s overkill.

Furthermore, those perspectives should be conveyed in a meaningful and concise way. And, perhaps most importantly, they need to be delivered in a way that the message is heard. Entrepreneurs are very different in the way they “hear.” Some are entirely open to different perspectives, others prefer being asked intelligent questions that they can pursue. Well-thought-out questions often have the most powerful effect on shaping an executive’s thinking.

Ultimately, no one likes to be told what to do. CEOs need to “own” the issues and deal with them operationally, and every day. Ownership is much easier when the idea comes from the CEO. So, the concept of delivering a message well is often to let the CEOs come to their own conclusions rather than spelling out what they should be doing. This is often more true with experienced operational leaders. All they need is a cue. The rest they can figure out themselves.

My best mentor in this dimension is Andy Rachleff . Andy invited me to join Equinix’s board many years ago. I also served on Opsware’s board with him. Now the tables have turned and he’s the CEO at Wealthfront while I am his board director. He will frequently remind me that if a board member gives one good strategic insight per board meeting, that’s a big win. If you offer two in one meeting, you get the “star award for board members.” That is a powerful reminder that less is often more.

The more I serve on boards, the more I appreciate the responsibilities and demands that come from being a board director. In the modern era of venture capital, we are tempted to distill board service as a “right” or a byproduct of investing or, worse, simply a “badge of honor.” Nothing could be further from the truth. Board membership is a privilege and a nuanced responsibility that can have a transformational impact on businesses. Sometimes investors, independents and entrepreneurs forget this. Entrepreneurs should expect a great deal from their boards — not as blind supporters but as true copilots. Likewise, board members should not view board membership as a list of icons on their LinkedIn profile, but as a subtle yet massively impactful role they play in the creation of great businesses. When these relationships function properly, the two parties become true partners in the entrepreneurial journey.

Powered by WPeMatico

According to a new WSJ report, certain members of WeWork’s seven-person board, which includes cofounder and CEO Adam Neumann, are planning to pressure Neumann to step down and instead become We’s non-executive chairman. The move, says the outlet, “would allow him to stay stay at the company he built into one of the country’s most valuable startups, but inject fresh leadership to pursue an IPO that would bring We the cash it needs to keep up its torrid growth.”

The WSJ and Bloomberg are reporting that it is SoftBank specifically that wants Neumann to step down. Neither WeWork nor SoftBank is commenting publicly.

It’s a fascinating development, the kind we saw when Uber’s board successfully forced cofounder and longtime CEO Travis Kalanick to abandon his role as CEO. Still, we’d caution against drawing too close a comparison. While the venture firm Benchmark, which spearheaded Kalanick’s ouster, stood to lose billions of dollars if Kalanick dragged down Uber and continued to push off an IPO, Benchmark was not in a do-or-die situation because of its Uber investment.

SoftBank appears to be in more dire straights, making this standoff a particularly meaningful one.

Let’s back up a minute first, though, and consider who is involved and which way this could potentially go. A few days ago, Business Insider put together a useful cheat sheet about WeWork’s board members that may hint at their allegiance.

1.) Ronald Fisher — who is vice chairman at SoftBank Group after founding SoftBank Capital, a U.S. venture arm of SoftBank — joined SoftBank’s board last year. He oversees 114 class A shares, each of which carries one vote. Obviously, he’s going to side with SoftBank.

2.) Lewis Frankfort — the chairman of a fitness studio chain called Flywheel Sports — has been a board member of WeWork for roughly five years, and BI says WeWork once loaned him $6.3 million, which he repaid with interest earlier this year. We have to think he’d stick with Neumann out of loyalty. At the same time, he doesn’t wield much power unless he has the right to block significant actions at the company (some shareholders get these blocking rights; some don’t.) What he know: he controls 2 million shares, and 750,000 of them are Class B shares that carry 10 votes each.

3.) Benchmark, which first backed WeWork in 2012, is represented on the board by Bruce Dunlevie, the founding partner of the venture firm. Benchmark owns 32.6 million Class A shares, and could go either way, seemingly. On the one hand, Benchmark doesn’t want to establish a reputation for pushing out founders after the Kalanick debacle, and if it supports SoftBank over Neumann, it risks this exact thing happening. On the other hand, Benchmark might not want to battle with SoftBank if it thinks it has staying power or it’s concerned (suddenly) that it allowed Neumann to amass too much control.

4.) Harvard Business School professor Frances Frei was brought in roughly a minute ago to add a much-need sprinkling of gender diversity to WeWork’s all-male board. Frei’s name first came to be more broadly recognized when she was hired to help address Uber’s battered culture, so presumably she has ties to Benchmark. We’d guess she’ll side with Dunlevie, meaning that we have no idea whose side she will take.

5.) Steven Langman, the cofounder of private equity firm Rhône Group, has ties that go back a ways with Neumann, and he has benefited richly from the association. According to an April story in the WSJ, Langman met Neumann through a shared rabbi in its earlier days and joined the board in 2012. He also invested in the company (he owns 2.28 million shares, according to a bond filing). Langman is on both the company’s compensation committee and its succession committee. He also runs a real-estate investment vehicle in partnership with We that buys and develops buildings to then lease back to the co-working company, despite that it raises conflict-of-interest questions. We’d guess he’s on Team Neumann.

6.) John Zhao is the chairman and CEO of Hony Capital, which partnered with SoftBank and WeWork to create a standalone entity called WeWork China back in 2017, and Hony has subsequently poured more capital into that subsidiary. We’re not sure how close Zhao is to SoftBank, but if SoftBank brought Hony into WeWork, we’re guessing he will back the Japanese conglomerate on this one. Hony doesn’t own 5 percent or more of WeWork’s parent company so its share holdings aren’t listed publicly.

Neumann, it’s very worth noting, is himself is far more powerful than any of these six individuals. Even after the company recently revised Neumann’s supervoting rights, which gave him 20 times the voting power of ordinary shareholders and now give him 10, he could fire the entire board if he so chooses, notes the WSJ.

Naturally, that wouldn’t be a good look for Neumann, who is already battling growing public perception that, among other negatives for a public company CEO, he smokes a whole lot of pot and that he may be delusional. (A WSJ piece last week reported that Neumann likes to smoke marijuana with friends and while airborne. It also said that Neumann has confided to different people his interest in becoming Israel’s prime minister and president of the world.)

All that said, SoftBank is also fast-losing credibility. While its CEO, Masayoshi Son, has been long revered as a visionary, a growing number of sources we’ve spoken to question the viability of his entire Vision Fund operation. They see WeWork’s ever-soaring valuation on the private market, from $20 billion to, more recently, $47 billion — which was almost single-handedly SoftBank’s doing — as just one in a costly string of poor calls.

Indeed, despite the roughly $10 billion that SoftBank has sunk into WeWork, the financial loss it would take if WeWork falls apart would pale in comparison to the reputational hit Son would suffer, and you can bet there will be ripple effects.

Our suspicion: given the Vision Fund’s impact on the startup industry over the last few years, there’s a lot more riding on what happens with WeWork than meets the eye. Stay tuned.

Powered by WPeMatico

Slack had added Edith Cooper, who most recently served as the global head of human capital management at Goldman Sachs, to its board of directors. As Slack prepares “for accelerated growth at scale,” Slack CEO Stewart Butterfield wrote in a blog post today, Cooper marks Slack’s second independent board member.

Slack had added Edith Cooper, who most recently served as the global head of human capital management at Goldman Sachs, to its board of directors. As Slack prepares “for accelerated growth at scale,” Slack CEO Stewart Butterfield wrote in a blog post today, Cooper marks Slack’s second independent board member.

“She has an unrivaled depth of experience in the hardest… Read More

Powered by WPeMatico

Every company has a board of directors — but few founders and entrepreneurs give the matter of board composition much thought. We’d like to offer some advice to founders and CEOs seeking to learn more about their boards, as well as to people who have been invited to sit on a board. Read More

Every company has a board of directors — but few founders and entrepreneurs give the matter of board composition much thought. We’d like to offer some advice to founders and CEOs seeking to learn more about their boards, as well as to people who have been invited to sit on a board. Read More

Powered by WPeMatico

They say once you’ve had frostbite, you never forget the cold. A founder who has suffered a bad board, or board member, never forgets that, either. I took my company public at age 33 with a board of four: me, someone I trusted and two people who taught me the meaning of the word acrimony. I have been obsessed ever since with helping my founders pick the right board members and avoid… Read More

They say once you’ve had frostbite, you never forget the cold. A founder who has suffered a bad board, or board member, never forgets that, either. I took my company public at age 33 with a board of four: me, someone I trusted and two people who taught me the meaning of the word acrimony. I have been obsessed ever since with helping my founders pick the right board members and avoid… Read More

Powered by WPeMatico