board member

Auto Added by WPeMatico

Auto Added by WPeMatico

When you enter the health tech industry as a new startup, an advisory board is a crucial foundational step. A board can guide you through industry-specific nuances, help you make important decisions and prove your legitimacy to investors looking for a strong industry background.

An advisory board will be able to give you strategic insights about both your company and the wider healthcare and technology industries.

In my experience of raising capital, the unpredictable financial situation at the beginning of the pandemic meant we nearly lost our $2 million round, but came through with a committed $250,000, which we used to bring in about $500,000 in revenue.

Something that helped this process was building our advisory board and starting small — we didn’t go for all of healthcare but instead focused on two healthcare verticals. This allowed us to prove our concept, build case studies and win contracts with specific teams in our customers’ companies.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future. For this reason, it’s important to identify the main intention behind your board, and exactly who should be on it.

Three to five people is an ideal starting point for an advisory board, depending on the size and stage of your company. In health tech, you need more than just the healthcare perspective — you also need the insight of those who have already grown technology companies, perhaps outside of the industry. Our company’s board is an even split of two healthcare and two technology advisers, and, ideally, you want to find a fifth who is well versed in both industries.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future.

An M.D., a Ph.D. from a respected institution or a thought leader in your relevant field of healthcare is the most important asset to an advisory board. These are the highly decorated physicians who have strong connections and act as a reference for their peers.

They provide instant credibility for your company, help you get into the minds of both patients and healthcare providers, and can outline how various health systems work.

Powered by WPeMatico

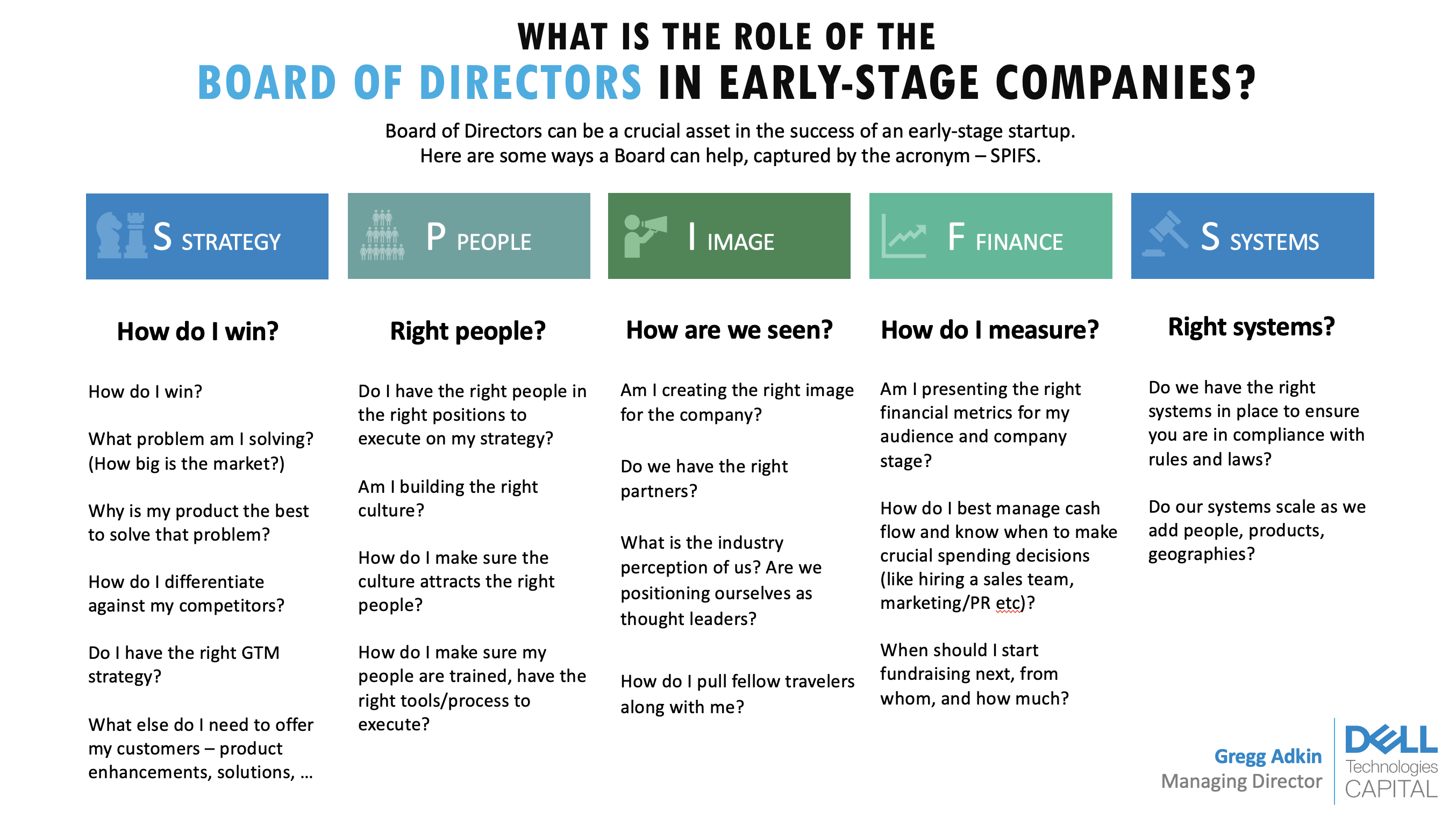

What’s the board’s role in an early-stage startup?

Startup founders frequently ask me about the role of a board of directors. A board can be a crucial asset in an early-stage startup.

Here’s a framework for how it can help drive success at your company: Strategy, People, Image, Finance and Systems for compliance, or “SPIFS.”

The board of directors helps with governance of the company. U.S. law requires that any company have one, though does not require how big it should be. By generic definition, the board of directors consists of elected individuals that represent shareholders. It is the governing body that provides company oversight and helps set business policy and strategy.

On a more practical level and in a startup environment, the board can aid in creating a successful business strategy, putting together the right management team, developing branding, building good financial habits, and avoiding legal and compliance issues. The needs and composition of the board will change depending on the startup’s stage, management and financing history (e.g., if there are preferred shareholders, investors that require a board seat and more).

Investors often ask founders about their board: It says a lot about their character, their judgment and their willingness to be challenged.

Investors often ask founders about their board for two reasons. First, it says a lot about their character, their judgment and their willingness to be challenged. The founder can typically choose who is on their board (through careful selection of investors and advisers) and negotiate a board structure they prefer.

Typically, a healthy board will have a good balance between common shareholders, preferred shareholders and independents. It also helps investors and analysts understand who will ask critical questions and give important advice to the company’s executive management, especially when the going gets tough (it inevitably does!).

After 20 years as a venture capitalist and board member, I boiled down the value of a board into five main pieces under the acronym SPIFS: Strategy, People, Image, Finance and Systems for compliance.

Image Credits: Dell Technologies Capital

Setting business strategy is one of the main ways that the board helps founders, especially if it’s their first time running a business. It is a valuable sounding board for validating that you have taken a sober account of the market and have the right plan to develop your product and acquire customers.

The board should ask these questions when guiding founders through setting strategy:

Powered by WPeMatico

For many companies in the United States, a board of directors is a fact of doing business. While sole proprietorships and LLCs are not obligated to have one, C and S corporations must. The board’s goal is to ensure the best is done for the company and its shareholders. While many entrepreneurs see board meetings as a chore, they can be a powerful tool if used well.

While board meetings usually happen quarterly, it’s good practice to keep the conversation going in between them. Sending a monthly email update to the board offers multiple advantages:

When meeting online, founders should pause often and regularly ask if there are questions — even if moments of silence feel awkward at times — to give directors a better opportunity to speak up.

Board members can also be solicited on an ad-hoc basis — founders should keep in mind that board members are here to help the company. If you have doubts about a project decision or want a second, informed opinion, reach out to a board member. This is especially true of directors who have expertise on a specific topic. A quick five-minute call can be a game changer.

Being a founder can be a lonely experience because it can be difficult to discuss sensitive matters with the team. Board members should sign nondisclosure agreements, allowing entrepreneurs to share confidential information and get a different perspective on things.

Founders should make sure to regularly discuss business goals to ensure they reach their next round of funding. Because the industry landscape or economy evolved or the competition stepped up, investors may reconsider their expectations to further fund the company.

Powered by WPeMatico

Productivity analytics startup Time is Ltd. wants to be the Google Analytics for company time. Or perhaps a sort of “Apple Screen Time” for companies. Whatever the case, the founders reckon that if you can map how time is spent in a company, enormous productivity gains can be unlocked and money better spent.

It’s now raised a $5.6 million late-seed funding round led by Mike Chalfen, of London-based Chalfen Ventures, with participation from Illuminate Financial Management and existing investor Accel. Acequia Capital and former Seal Software chairman Paul Sallaberry are also contributing to the new round, as is former Seal board member Clark Golestani. Furthermore, Ulf Zetterberg, founder and former CEO of contract discovery and analytics company Seal Software, is joining as president and co-founder.

The venture is the latest from serial entrepreneur Jan Rezab, better known for founding SocialBakers, which was acquired last year.

We are all familiar with inefficient meetings, pestering notifications chat, video conferencing tools and the deluge of emails. Time is Ltd. says it plans to address this by acquiring insights and data platforms such as Microsoft 365, Google Workspace, Zoom, Webex, MS Teams, Slack and more. The data and insights gathered would then help managers to understand and take a new approach to measure productivity, engagement and collaboration, the startup says.

The startup says it has now gathered 400 indicators that companies can choose from. For example, a task set by The Wall Street Journal for Time is Ltd. found the average response time for Slack users versus email was 16.3 minutes, comparing to emails which was 72 minutes.

Chalfen commented: “Measuring hybrid and distributed work patterns is critical for every business. Time Is Ltd.’s platform makes such measurement easily available and actionable for so many different types of organizations that I believe it could make work better for every business in the world.”

Rezab said: “The opportunity to analyze these kinds of collaboration and communication data in a privacy-compliant way alongside existing business metrics is the future of understanding the heartbeat of every company — I believe in 10 years time we will be looking at how we could have ignored insights from these platforms.”

Tomas Cupr, founder and Group CEO of Rohlik Group, the European leader of e-grocery, said: “Alongside our traditional BI approaches using performance data, we use Time is Ltd. to help improve the way we collaborate in our teams and improve the way we work both internally and with our vendors — data that Time is Ltd. provides is a must-have for business leaders.”

Powered by WPeMatico

With the increase of digital transacting over the past year, cybercriminals have been having a field day.

In 2020, complaints of suspected internet crime surged by 61%, to 791,790, according to the FBI’s 2020 Internet Crime Report. Those crimes — ranging from personal and corporate data breaches to credit card fraud, phishing and identity theft — cost victims more than $4.2 billion.

For companies like Sift — which aims to predict and prevent fraud online even more quickly than cybercriminals adopt new tactics — that increase in crime also led to an increase in business.

Last year, the San Francisco-based company assessed risk on more than $250 billion in transactions, double from what it did in 2019. The company has over several hundred customers, including Twitter, Airbnb, Twilio, DoorDash, Wayfair and McDonald’s, as well a global data network of 70 billion events per month.

To meet the surge in demand, Sift said today it has raised $50 million in a funding round that values the company at over $1 billion. Insight Partners led the financing, which included participation from Union Square Ventures and Stripes.

While the company would not reveal hard revenue figures, President and CEO Marc Olesen said that business has tripled since he joined the company in June 2018. Sift was founded out of Y Combinator in 2011, and has raised a total of $157 million over its lifetime.

The company’s “Digital Trust & Safety” platform aims to help merchants not only fight all types of internet fraud and abuse, but to also “reduce friction” for legitimate customers. There’s a fine line apparently between looking out for a merchant and upsetting a customer who is legitimately trying to conduct a transaction.

Sift uses machine learning and artificial intelligence to automatically surmise whether an attempted transaction or interaction with a business online is authentic or potentially problematic.

Image Credits: Sift

One of the things the company has discovered is that fraudsters are often not working alone.

“Fraud vectors are no longer siloed. They are highly innovative and often working in concert,” Olesen said. “We’ve uncovered a number of fraud rings.”

Olesen shared a couple of examples of how the company thwarted fraud incidents last year. One recently involved money laundering through donation sites where fraudsters tested stolen debit and credit cards through fake donation sites at guest checkout.

“By making small donations to themselves, they laundered that money and at the same tested the validity of the stolen cards so they could use it on another site with significantly higher purchases,” he said.

In another case, the company uncovered fraudsters using Telegram, a social media site, to make services available, such as food delivery, with stolen credentials.

The data that Sift has accumulated since its inception helps the company “act as the central nervous system for fraud teams.” Sift says that its models become more intelligent with every customer that it integrates.

Insight Partners Managing Director Jeff Lieberman, who is a Sift board member, said his firm initially invested in Sift in 2016 because even at that time, it was clear that online fraud was “rapidly growing.” It was growing not just in dollar amounts, he said, but in the number of methods cybercriminals used to steal from consumers and businesses.

“Sift has a novel approach to fighting fraud that combines massive data sets with machine learning, and it has a track record of proving its value for hundreds of online businesses,” he wrote via email.

When Olesen and the Sift team started the recent process of fundraising, Insight actually approached them before they started talking to outside investors “because both the product and business fundamentals are so strong, and the growth opportunity is massive,” Lieberman added.

“With more businesses heavily investing in online channels, nearly every one of them needs a solution that can intelligently weed out fraud while ensuring a seamless experience for the 99% of transactions or actions that are legitimate,” he wrote.

The company plans to use its new capital primarily to expand its product portfolio and to scale its product, engineering and sales teams.

Sift also recently tapped Eu-Gene Sung — who has worked in financial leadership roles at Integral Ad Science, BSE Global and McCann — to serve as its CFO.

As to whether or not that meant an IPO is in Sift’s future, Olesen said that Sung’s experience of taking companies through a growth phase such as what Sift is experiencing would be valuable. The company is also for the first time looking to potentially do some M&A.

“When we think about expanding our portfolio, it’s really a buy/build partner approach,” Olesen said.

Powered by WPeMatico

It all started with an email from a customer: “Do you know why Bain Capital Ventures is reaching out to me about Clockwise?”

That email would mark the beginning of a journey toward closing $18 million in new funding that will dramatically accelerate my company, Clockwise . It would require getting to know a partner in lockdown, long nights assembling a pitch deck and many bleary-eyed Zoom calls with some of the best VCs in the world.

Here’s how Ajay Agarwal from Bain Capital Ventures and I established trust online, how I made high-stakes decisions in extreme economic uncertainty and how we were able to turn the pandemic’s constraints into opportunities.

Let’s start at the beginning.

Clockwise was founded in late fall of 2016. We realized that, as personal as time is, our schedules inside modern work environments are intertwined by a network of calendar events and attendees. People schedule meetings without considering the preferences of colleagues by simply hunting for any available “white space” (read: time to do real work). The net effect is that our most valuable resource, time, is easy to take and almost impossible to protect.

More than two years later, in June of 2019, we launched Clockwise to the public. After years of experimentation and refinement, we delivered to the world an intelligent calendar assistant that frees up your time so you can focus on what matters. Workers soon confirmed our hunch that they’re hungry for a tool that gives them more productive hours in their day. Our rapid user growth carried throughout 2019.

By January of 2020, we were on fire. Since January 1, our user base has grown by more than 90%, expanding at a clip of well over 5% week-over-week. As people sought remote tools during shelter-in-place, our rate of growth accelerated even further.

Our growth, incredible team, top-tier existing investors (Accel and Greylock) and strong cash position meant we didn’t need to raise additional capital until the fall of 2020. While COVID-19 certainly sent shock waves through the community, I was in regular communication with a few highly engaged investors who still seemed eager to invest in the future of productivity. I felt cautiously confident more capital could wait.

But, you know, best-laid plans.

Powered by WPeMatico

The novel coronavirus has been devastating for many people, families and communities — and the consequences are still being calculated. The tech world has seen wave after wave of layoffs, sometimes multiple waves at one company only weeks apart. Some startups have lost nearly all their revenue, and depending on their cash reserves, have little hope of recovering.

For VCs, the last two months have been an exercise in triage.

Partners have gone through their entire investment portfolios to identify the winners, what’s salvageable and what (at least in their minds) has no hope of resuscitation. If you are in the first two groups, it’s back to whatever normal looks like in the midst of a global pandemic and a deep economic recession.

But what if you suddenly get a call informing you that your investor — perhaps your biggest champion to date — is going to cut the rope and write you off entirely?

That’s what we are going to talk about today.

Before we go anywhere, be thankful if you even know how your investors are judging your startup. Most, unfortunately, will couch the terms they use (“we will be engaging less” or perhaps “we are unlikely to do our pro rata going forward”) rather than just saying directly, “we are writing you off; don’t call us — we’ll call you.” That’s polite and face-saving for all parties, but the lack of transparency can make decisions down the road much harder. It’s better to know where you stand, even if the news is hard.

The first step to approaching this situation is to get your bearings. Much like during a fundraise process, it’s not uncommon for different investors on your cap table to reach different conclusions about your startup’s potential. One investor may write you off, while another has you marked at a more neutral valuation or even positively. This can absolutely be frustrating, and given the emotion of this situation, it can be hard to rationally accept that an investor who once believed in you no longer does so.

Powered by WPeMatico

Spotify did it. Slack did it. Many other late-stage private technology companies are reported to be seriously considering it. Should yours?

If you are a board member of a late-stage, venture-backed company or part of its management team, you likely have heard of the term “direct listing.” Or you may have attended one or all of the slew of recent conferences being hosted by big-name investment banks and others, including tech investor guru Bill Gurley, who recently debated the pros and cons of choosing a direct listing over a traditional IPO.

Before you decide what’s right for your company, here are a few things you need to know about direct listings.

For people not familiar with the term, a direct listing is an alternative way for a private company to “go public,” but without selling its shares directly to the public and without the traditional underwriting assistance of investment bankers.

In a traditional IPO, a company raises money and creates a public market for its shares by selling newly created stock to investors. In some instances, a select number of pre-IPO investors, usually very large stockholders or management, may also sell a portion of their holdings in the IPO. In an IPO, the company engages investment bankers to help promote, price and sell the stock to investors. The investment bankers are paid a commission for their work that is based on the size of the IPO—usually seven percent for a traditional technology company IPO.

In a direct listing, a company does not sell stock directly to investors and does not receive any new capital. Instead, it facilitates the re-sale of shares held by company insiders such as employees, executives and pre-IPO investors. Investors in a direct listing buy shares directly from these company insiders.

Does this mean that a company doing a direct listing doesn’t need investment banks? Not quite. Companies still engage investment banks to assist with a direct listing and those banks still get paid quite well (to the tune of $35 million in Spotify and $22 million in Slack).

However, the investment banks play a very different role in a direct listing. Unlike a traditional IPO, in a direct listing, investment banks are prohibited under current law from organizing or attending investor meetings and they do not sell stock to investors. Instead, they act purely in an advisory capacity helping a company to position its story to investors, draft its IPO disclosures, educate a company’s insiders on process and strategize on investor outreach and liquidity.

The concept of a direct listing is actually not a new one. Companies in a variety of industries have used similar structures for years. However, the structure has only recently received a lot of investor and media attention because high-profile technology companies have started to use it to go public. But why have technology companies only recently started to consider direct listings?

The rise of massive pre-IPO fundraising rounds

With an abundance of investor capital, especially from institutional investors that historically hadn’t invested in private technology companies, massive pre-IPO fundraising rounds have become the norm. Slack raised over $400 million in August 2018—just over a year prior to its direct listing. Because of this widespread availability of capital, some technology companies are now able to raise sufficient capital before their actual IPO to either become profitable or put them on a path to profitability.

Criticism of current IPO process

There has been increasing negative sentiment, especially amongst well-known venture capitalists, about certain aspects of the traditional IPO process—namely IPO lock-up agreements and the pricing and allocation process.

IPO lock-up agreements. In a traditional IPO, investment bankers require pre-IPO investors, employees and the company to sign a “lock-up agreement” restricting them from selling or distributing shares for a specified period of time following the IPO—usually 180 days. The bankers put these agreements in place in order to stabilize the stock immediately after the IPO. While the merits of a lock-up agreement can certainly be debated, by the time VCs (and other insiders) are allowed to sell following an IPO, oftentimes the stock price has fallen significantly from its highs (sometimes to below the IPO price) or the post lock-up flood of selling can have an immediate negative impact on the trading price.

In a direct listing, there is no lock-up agreement, which allows for equal access to the offering to all of the company’s pre-IPO investors, including rank-and-file employees and smaller pre-IPO stockholders.

IPO pricing and allocation: In a traditional IPO, shares are often allocated directly by a company (with the assistance of its underwriters) to a small number of large, institutional investors. Traditional IPOs are often underpriced by design to provide large institutional investors the benefit of an immediate 10-15% “pop” in the stock price. Over the last few years, some of these “pops” have become more pronounced. For example, Beyond Meat’s stock soared from $25 to $73 on its first day of trading, a 163% gain. This has fueled a concern, particularly shared amongst the VC community, that investment banks improperly price and allocate shares in an IPO in order to benefit these institutional investors, which are also clients of the same investment banks that are underwriting the IPO. While the merits of this concern can also be debated, in instances where there is a large price discrepancy between the trading price of the stock following the IPO and the price of the IPO, there is often a sense that companies have left money on the table and that pre-IPO investors have suffered unnecessary dilution. If the IPO had been priced “correctly,” the company would have had to sell fewer shares to raise the same amount of proceeds.

Because a company is not selling stock in a direct listing, the trading price after listing is purely market driven and is not “set” by the company and its investment bankers. Moreover, since no new shares are issued in a direct listing, insiders do not suffer any dilution.

The Spotify effect

Before Spotify’s direct listing, technology companies hadn’t used the direct listing structure to go public. Spotify was, in many ways, the perfect test case for a direct listing. It was well known, didn’t need any additional capital and was cash flow positive. In addition, prior to its direct listing, Spotify had entered into a debt instrument that penalized the company so long as it remained private. As a result, it just needed to go public. After clearing some regulatory hurdles, Spotify successfully executed its direct listing in April 2018. After Spotify’s direct listing, Slack (relatively) quickly followed suit. Slack’s direct listing was notable because it represented the first traditional Silicon Valley-based VC-backed company to use the structure. It was also an enterprise software company, albeit one with a consumer cult following.

While a direct listing offers many benefits, the structure does not make sense for every company. Below is a list of key benefits and drawbacks:

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I noted some challenges plaguing mental health tech startups. Before that, I wrote about Zoom and Superhuman’s PR disasters.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Anyway, onto the subject on everyone’s mind this week: SoftBank’s second Vision Fund.

Well into the evening on Thursday, SoftBank announced a target of $108 billion for the Vision Fund 2. Yes, you read that correctly, $108 billion. SoftBank indeed plans to raise even more capital for its sophomore vehicle than it did for the record-breaking debut vision fund of $98 billion, which was majority-backed by the government funds of Saudi Arabia and Abu Dhabi, as well as Apple, Foxconn and several other limited partners.

Its upcoming fund, to which SoftBank itself has committed $38 billion, has attracted investment from the National Investment Corporation of National Bank of Kazakhstan, Apple, Foxconn, Goldman Sachs, Microsoft and more. Microsoft, a new LP for SoftBank, reportedly hopped on board with the Japanese telecom giant as part of a grand scheme to convince the massive fund’s portfolio companies to transition to Microsoft Azure, the company’s cloud platform that competes with Amazon Web Services . Here’s more on that and some analysis from TechCrunch editor Jonathan Shieber.

News of the second Vision Fund comes as somewhat of a surprise. We’d heard SoftBank was having some trouble landing commitments for the effort. Why? Well, because SoftBank’s investments have included a wide-range of upstarts, including some uncertain bets. Brandless, a company into which SoftBank injected a lot of money, has struggled in recent months, for example. Wag is said to be going downhill fast. And WeWork, backed with billions from SoftBank, still has a lot to prove.

Here’s everything else we know about The Vision Fund 2:

On to other news…

WeWork is planning a September listing

The company made headlines again this week after word slipped it was accelerating its IPO plans and targeting a September listing. We don’t know much about its IPO plans yet as we are still waiting on the co-working business to unveil its S-1 filing. Whether WeWork can match or exceed its current private market valuation of $47 billion is unlikely. I expect it will pull an Uber and struggle, for quite some time, to earn a market cap larger than what VCs imagined it was worth months earlier.

The consumer financial app made headlines twice this week. The first time because it raised a whopping $323 million at a $7.6 billion valuation. That is a whole lot of money for a business that just raised a similarly sized monster round one year ago. In fact, it left us wondering, why the hell is Robinhood worth $7.6 billion? Then, in a major security faux pas, the company revealed it has been storing user passwords in plaintext. So, go change your Robinhood password and don’t trust any business to value your security. Sigh.

Another day, another huge fintech round

While we’re on the subject on fintech, TechCrunch editor Danny Crichton noted this week the rise of mega-rounds in the fintech space. This week, it was personalized banking app MoneyLion, which raised $100 million at a near unicorn valuation. Last week, it was N26, which raised another $170 million on top of its $300 million round earlier this year. Brex raised another $100 million last month on top of its $125 million Series C from late last year. Meanwhile, companies like payments platform Stripe, savings and investment platform Raisin, traveler lender Uplift, mortgage backers Blend and Better and savings depositor Acorns have also raised massive new rounds this year. Naturally, VC investment in fintech is poised to reach record levels this year, according to PitchBook.

Arianna Huffington, the CEO of Thrive Global, stepped down from Uber’s board of directors this week, a team she had been apart of since 2016. She addressed the news in a tweet, explaining that there were no disagreements between her and the company, rather, she was busy and had other things to focus on. Fair. Benchmark’s Matt Cohler also stepped down from the board this week, which leads us to believe the ride-hailing giant’s advisors are in a period of transition. If you remember, Uber’s first employee and longtime board member Ryan Graves stepped down from the board in May, just after the company’s IPO.

Today I told my fellow @Uber board members that given @Thrive‘s growth, I will no longer be able to give my board duties the attention they deserve, so I will be stepping down. I look forward to watching Uber go from strength to strength! Here is the email I sent to the board: pic.twitter.com/sck0CPLwAV

— Arianna Huffington (@ariannahuff) July 24, 2019

Unity, now valued at $6B, raising up to $525M

Bird is raising a Sequoia-led Series D at $2.5B valuation

SMB payroll startup Gusto raises $200M Series D

Elon Musk’s Boring Company snags $120M

a16z values camping business HipCamp at $127M

An inside look at the startup behind Ashton Kutcher’s weird tweets

Dataplor raises $2M to digitize small businesses in Latin America

While we’re on the subject of amazing TechCrunch #content, it’s probably time for a reminder for all of you to sign up for Extra Crunch. For a low price, you can learn more about the startups and venture capital ecosystem through exclusive deep dives, Q&As, newsletters, resources and recommendations and fundamental startup how-to guides. Here are some of my current favorite EC posts:

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Equity co-host Alex Wilhelm, TechCrunch editor Danny Crichton and I unpack Robinhood’s valuation and argue about scooter startups. Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast and Spotify.

That’s all, folks.

Powered by WPeMatico

Zoom, a relatively under-the-radar tech unicorn, has defied expectations with its initial public offering. The video conferencing business priced its IPO above its planned range on Wednesday, confirming plans to sell shares of its Nasdaq stock, titled “ZM,” at $36 apiece, CNBC reports.

The company initially planned to price its shares at between $28 and $32 per share, but following big demand for a piece of a profitable tech business, Zoom increased expectations, announcing plans to sell shares at between $33 and $35 apiece.

The offering gives Zoom an initial market cap of roughly $9 billion, or nine times that of its most recent private market valuation.

Zoom plans to sell 9,911,434 shares of Class A common stock in the listing, to bring in about $350 million in new capital.

If you haven’t had the chance to dive into Zoom’s IPO prospectus, here’s a quick run-down of its financials:

Zoom is backed by Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent); Digital Mobile Venture, a fund affiliated with former Zoom board member Samuel Chen (8.5 percent); and Bucantini Enterprises Limited (5.9 percent), a fund owned by Chinese billionaire Li Ka-shing.

Zoom will debut on the Nasdaq the same day Pinterest will go public on the NYSE. Pinterest, for its part, has priced its shares above its planned range, per The Wall Street Journal.

Powered by WPeMatico