bnpl

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s a two-Exchange Tuesday, everyone. First up, we’re talking fintech valuations. Next up, we’re digging into Atlanta.

Last week’s news that PayPal intends to buy Japanese startup Paidy marked the second major acquisition of a buy now, pay later (BNPL) company this year. PayPal’s news followed an even larger deal by Square for the Australian BNPL company Afterpay.

The multibillion-dollar exits provided hard market proof that what BNPL startups are building has value beyond simple operating results; major fintech platforms are willing to shell out large sums for their revenues and possible strategic value.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Because both deals happened in 2021, they provide two data points for the value of BNPL companies operating at scale. And because both Square and PayPal provided some information to their investors concerning their transactions, we have a little bit of comparative work to do.

Let’s do a little math and figure out how much PayPal and Square investors are paying for transaction volume across both platforms. Then, we’ll peek at what Affirm is worth along similar lines. We’ll wrap with a look at Klarna’s numbers to see if there’s anything we can dig up there.

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Square’s Afterpay deal is worth some $29 billion, a huge sum. It isn’t hard to see why the U.S. consumer- and business-focused fintech is willing to write so large a check — Afterpay does volume.

Powered by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

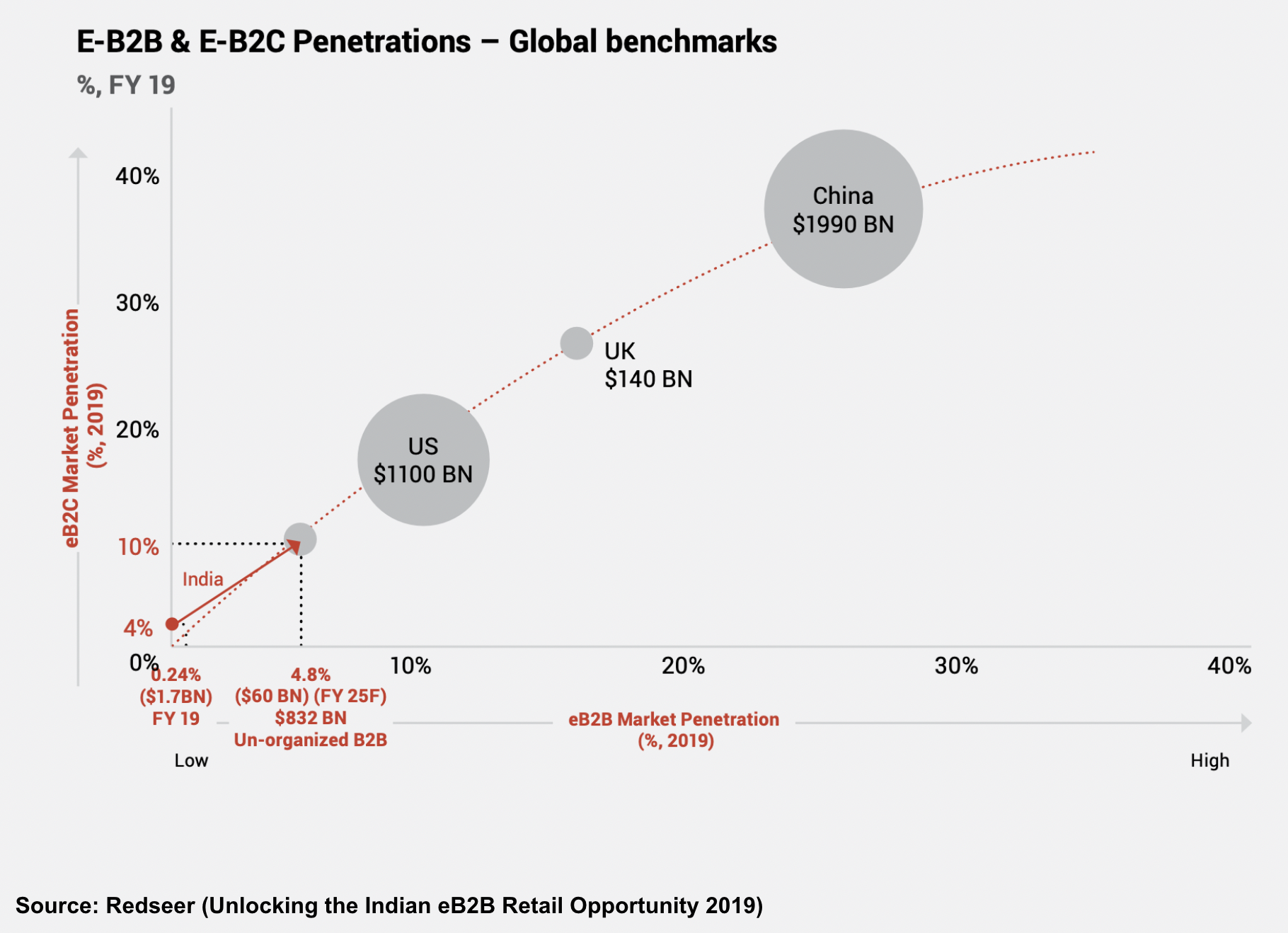

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

On Sunday Square announced it was gobbling up Afterpay in a deal worth $29 billion at the time of announcement. Alex followed up yesterday with more details on why the deal made sense for Square and Afterpay over here, but we wanted to ask some notable VCs what it means for the startup market.

For context, the Square deal follows a ton of money and interest flowing into the BNPL market. Just this year, VCs have invested in companies like Alma ($59.4 million, January 2021), Scalapay ($48 million, January 2021), Wisetack ($19 million, February 2021), Zilch ($80 million, April 2021) and Dividio ($30 million, June 2021).

Most of the investors we reached out to were generally bullish on the Square and Afterpay integration, but they were less excited about opportunities for other consumer BNPL businesses to emerge.

Then there’s Klarna, which raised $639 million at a post-money valuation of $45.6 billion in June, after raising $1 billion in March at a post-money valuation of $31 billion.

There’s also interest from some major public companies. After a slow start, PayPal is aggressively pushing BNPL services with merchants that offer it as a payment option. And there are reports that Apple is building its own BNPL offering through Apple Pay.

We reached out to Commerce Ventures founder and GP Dan Rosen, Better Tomorrow Ventures founding partner Jake Gibson, Fika Ventures partner TX Zhuo, and Matthew Harris of Bain Capital Ventures to see what they thought of the deal, as well as what it might mean for the opportunity for other BNPL companies and startups.

The main takeaways? “Buy now, pay later” may be effective at driving retail conversion, but scale matters and long-term margins look slim for BNPL startups.

Now, let’s hear from the venture community.

Why is the BNPL market so hot?

Powered by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week had the whole crew aboard to record: Grace and Chris making us sound good, Danny to provide levity, Natasha to actually recall facts and Alex to divert us from staying on topic. It’s teamwork, people — and our transitions are proof of it.

And it’s good that we had everyone around the virtual table, as there was quite a lot to get through:

Thanks for hanging out this week, Equity is back on Tuesday with our usual weekly kickoff, thanks to the American holiday on Monday. Chat then, unless you want to follow us on Twitter and get a first-look at all of Chris’ meme work.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday morning at 7:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

This morning Wisetack, a startup that provides buy-now-pay-later services to in-person business transactions, announced that is has closed a total of $19 million across two rounds, a seed investment and a Series A.

Greylock led both rounds, with the seed round clocking in at $4 million and the Series A at $15 million. Bain Capital Ventures also took part in the company’s fundraising.

Notably both rounds were closed in 2019, making these amongst the more aged rounds that we’ve heard of in recent quarters. However, as much venture reporting was delayed last year due to the pandemic and political unsettlement, I am still willing to cover the occasional antique deal.

Wisetack caught our eye not only due to its fundraising activity, but also thanks the buy-now-pay-later (BNPL) space becoming all the more interesting in the wake of Affirm’s direct listing. Affirm is perhaps the best-known service of its type, making its liquidity moment — and post-IPO performance — impactful for its broader business category.

But while Affirm wants to offer point-of-sale BNPL services to online merchants, Wisetack is taking a different approach. It focuses on the in-person business world, helping finance consumer transactions involving things like home improvement and car repair; the sort of big transactions that your average family might not have the cash to cover but also doesn’t want to put on a credit card.

Wisetack partners with vertical SaaS players in different areas. Say, plumbing. This allows users of those vertical SaaS applications — the plumbers, sticking to the same example — to offer Wisetack’s BNPL service to their customers.

It’s well known that vertical SaaS has wide application. A favorite recent example is SingleOps, which provides software for the so-called “green industry,” the world of lawns and landscaping. There’s SaaS for all sorts of IRL work, which could mean that Wisetack has a good number of software providers to sell into.

The model appears to be working, at least thus far. Wisetack shared with TechCrunch that its loan volume rose 20x between January of 2020 and January of 2021. As the company generates revenues from merchants (loan processing costs), and consumer interest, it’s likely that its revenue scales with loan volume. If the relationship is even closer to direct, Wisetack grew quite a lot last year.

The startup also said that the number of businesses using Wisetack grew 25-fold last year to a number in the “thousands.”

Wisetack fits neatly into a number of recent trends. The first is its work with vertical SaaS, a notable slice of the software market. The second is that Wisetack is another example of an API-led business, offering its service as a tech-powered add-on to other bits of code. And, third, that Wisetack had the same lead investor twice in sequential rounds. This sort of doubling-down from the venture community has become common in recent quarters as the signaling risk of having the lead twice in a row has been zeroed out by general investor enthusiasm for more equity in what appear to be winning startups.

Finally, the Wisetack round is interesting as it is nearly a sort of vertical BNPL, or at least a vertically focused BNPL. The company was reticent to share notes on how it comes to credit decisions, but we presume that all BNPL players that do focus on a particular niche or segment.

Powered by WPeMatico