blockchains

Auto Added by WPeMatico

Auto Added by WPeMatico

I learned about Yat in April, when a friend sent our group chat a link to a story about how the key emoji sold as an “internet identity” for $425,000. “I hate the universe,” she texted.

Sure, the universe would be better if people with a spare $425,000 spent it on mutual aid or something, but minutes later, we were trying to figure out what this whole Yat thing was all about. And few more minutes later, I spent $5 (in U.S. dollars, not crypto) to buy

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

, an emoji string that I think tells a moving story about my caffeine dependency and sensitive stomach. I didn’t think I would be writing about this when I made that choice.

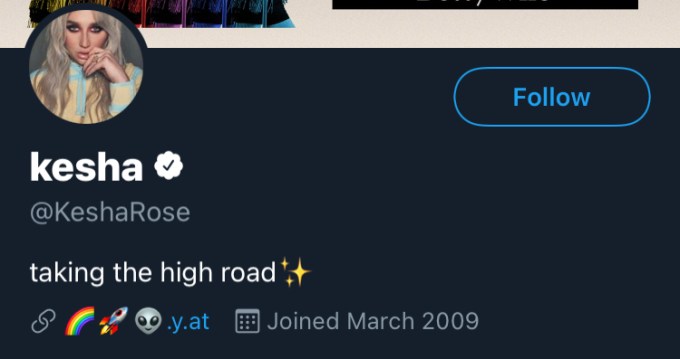

Kesha’s Yat URL on Twitter

On the surface, Yat is a platform that lets you buy a URL with emojis in it — even Kesha (y.at/

), Lil Wayne (y.at/

), Lil Wayne (y.at/ ), and Disclosure (y.at/

), and Disclosure (y.at/ ) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

) are using them in their Twitter bios. Like any URL on the internet, Yats can redirect to another website, or they can function like a more eye-catching Linktree. While users could purchase their own domain name that supports emojis and use it instead of a Yat, many people don’t have the technical expertise or time to do so. Instead, they can make a one-time purchase from Yat, which owns the Y.at domain, and the company will provide you with your own y.at link for you.

This convenience, however, comes at a premium. Yat uses an algorithm to determine your Yat’s “rhythm score,” its metric for determining how to price your emoji combo based on its rarity. Yats with one or two emojis are so expensive that you have to contact the company directly to buy them, but you can easily find a four- or five-emoji identity that’ll only put you out $4.

Beyond that, CEO Naveen Jain — a Y Combinator alumnus, founder of digital marketing company Sparkart and angel investor — thinks that Yat is ultimately an internet privacy product. Jain wants people to be able to use their Yats in any way they’re able to use an online identity now, whether that’s to make payments, send messages, host a website or log in to a platform.

“Objectively, it’s a strange norm. You go on the internet, you register accounts with ad-supported platforms, and your username isn’t universal. You have many accounts, many usernames,” Jain said. “And you don’t control them. If an account wants to shut you down, they shut you down. How many stories are there of people trying to email some social network, and they don’t respond because they don’t have to?”

Image Credits: Yat (opens in a new window)

Yat doesn’t plan to fuel itself with ad money, since users pay for the product when they purchase their Yat, whether they get it for $4 or $400,000.

In the long run, Yat’s CEO says the company plans to use blockchain technology as a way to become self-sovereign. Yats would become assets issued on decentralized, distributed databases. Today, there are several projects working to create a decentralized alternative to the current domain name system (DNS), which is managed by internet regulatory authority ICANN. DNS is how you find things on the internet, but uses a centralized, hierarchical system. A blockchain domain name system would have no central authority, and some believe this could be the foundation of a next-gen web, or “Web 3.0.”

Today, words like “blockchain” and “cryptocurrency” don’t appear on the Yat website. Jain doesn’t think that’s compelling to average consumers — he believes in progressive decentralization, which explains why Yats are currently purchased with dollars, not ethereum.

“Something we think is really funny about the cryptocurrency world is that anyone who’s a part of it spends a lot of time talking about databases,” Jain said. “People don’t care about databases. When’s the last time you went to a website and it said ‘powered by MySQL’?”

Y.at, however, was registered at a traditional internet registrar, not on the blockchain.

“This is laying the foundation — there are certain elements of the vision that are certainly more of a social contract than actual implementation at this point in time,” says Jain. “But this is the vision that we’ve set forth, and we’re working continuously towards that goal.”

Still, until Yat becomes more decentralized, it can’t yet give users the complete control it aspires to. At present, the Terms & Conditions give Yat the authority to terminate or suspend users at its discretion, but the company claims it hasn’t yet booted anyone from the system.

“As Yat becomes more decentralized, our terms and conditions won’t be important,” Jain said. “This is the nature of pursuing a progressive decentralization strategy.”

In its “generation zero” phase (an open beta), Yat claims to have sold almost $20 million worth of emoji identities. Now, as the waitlist to get a Yat ends, Yat is posting some rare emoji identities on OpenSea, the NFT marketplace that recently reached a valuation of $1.5 billion.

A still image of a Yat visualizer creation

“For the first time ever, we’re going to be auctioning some Yats on OpenSea, and we’re going to be launching minting of Yats on Ethereum,” Jain said. Before minting Yats as NFTs, users can create a digital art landscape for their Yats through a Visualizer. These features, as well as new emojis in the Yat emoji set, will launch this evening at a virtual event called Yat Horizon.

“Yat Creators will now have more rights,” Jain said about the new ability to mint Yats as NFTs. “We are going to continue to pursue progressive decentralization until we achieve our ultimate goal: making Yat the best self-directed, self-sovereign identity system for all.”

Consumers have a demonstrated interest in retaining greater privacy on the internet — data shows that in iOS 14.5, 96% of users opted out of ad tracking. But the decentralization movement hasn’t yet been able to market its privacy advantages to the mainstream. Yat helps solve this problem because even if you don’t understand what blockchain means, you understand that having a personal string of emojis is pretty fun. But, before you spend $425,000 on a single-emoji username, keep in mind that Yat’s vision will only completely materialize with the advent of Web 3.0, and we don’t yet know when or if that will happen.

Powered by WPeMatico

While retail investors grew more comfortable buying cryptocurrencies like Bitcoin and Ethereum in 2021, the decentralized application world still has a lot of work to do when it comes to onboarding a mainstream user base.

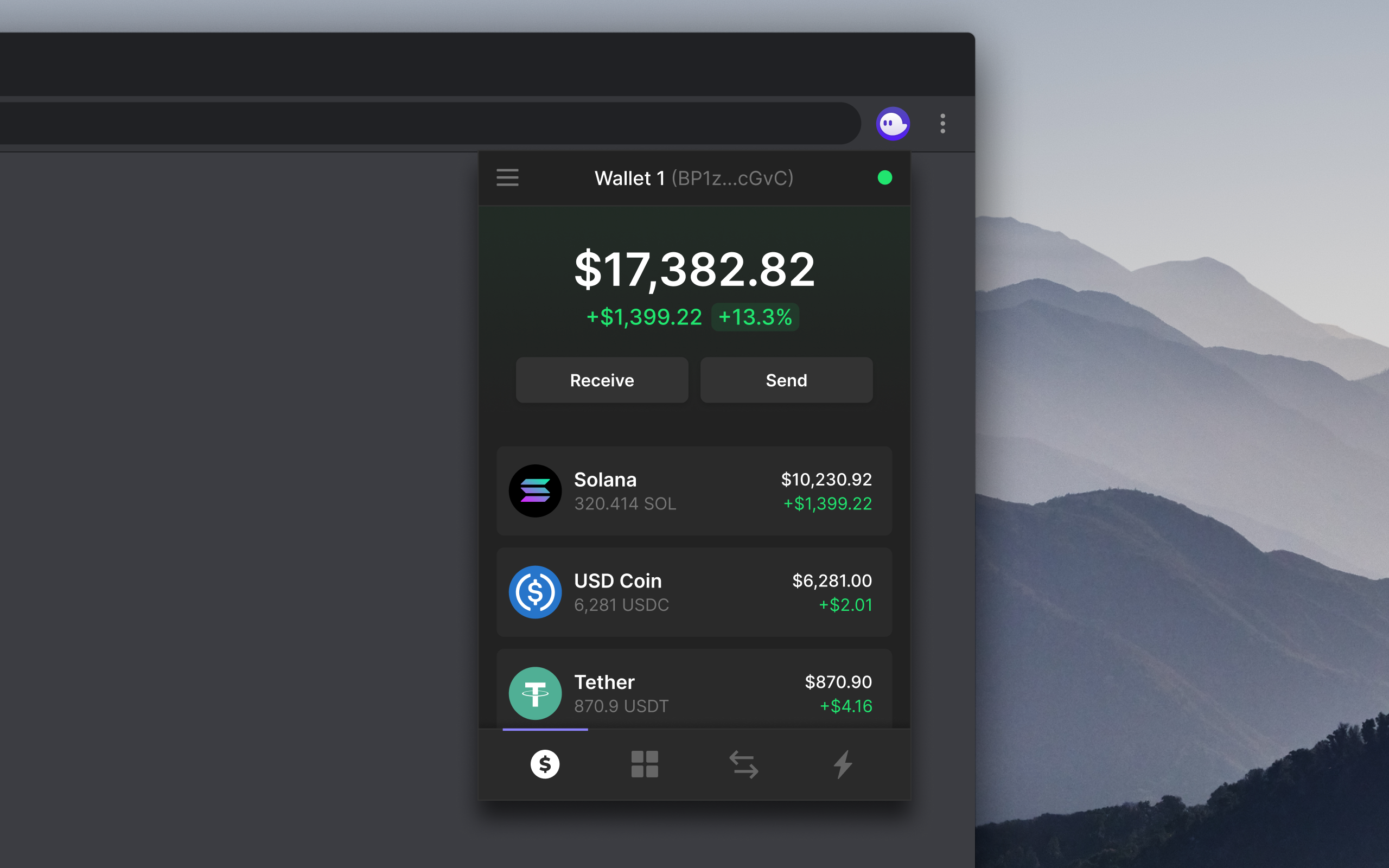

Phantom is part of a new class of crypto startups looking to build infrastructure that streamlines blockchain-based applications and provides a more user-friendly UX for navigating the crypto world, something that can make the entire space more approachable to a non-developer audience. Users can download the Phantom wallet to their browsers to interact with applications, swap tokens and collect NFTs.

The crypto wallet startup has banked a $9 million Series A round led by Andreessen Horowitz (a16z), with Variant Fund, Jump Capital, DeFi Alliance, Solana Foundation and Garry Tan also participating. The round, which closed earlier this summer, comes as some venture capital firms embrace a crypto future even as volatility continues to envelop the broader market. Last month, a16z announced a whopping 2.2 billion crypto fund, the firm’s largest vertical-specific investment vehicle ever.

Image via Phantom

The co-founding team of CEO Brandon Millman, CPO Chris Kalani and CTO Francesco Agosti all come aboard from crypto infrastructure startup 0x.

At the moment, Phantom is best-known among the Solana community, where it has become the go-to wallet for applications on that blockchain. The startup’s ambition is to interface with more and more networks, currently building out compatibility with Ethereum and looking to embrace other blockchains, aiming to be a product built for a “multichain world,” Millman tells TechCrunch.

Alongside building out support for other networks, Phantom wants to build more sophisticated DeFi mechanisms right into their wallet, allowing users to stake cryptocurrencies and swap more tokens inside the wallet.

The startup says they have some 40,000 users of their existing wallet product.

Building out a presence on the popular Ethereum blockchain, which already has a handful of popular wallet providers, will be a challenge, but Phantom’s broadest challenge is helping a new breed of crypto-curious users interface with a network of apps that still have a long way to go when it comes to being mainstream-friendly.

“The entire space is kind of stuck in this ‘built by developers for other developers mode,’ ” Millman says. “This bar has been kind of stuck there, and no one is really stepping up to push the bar up higher.”

Powered by WPeMatico

Augmented reality and non-fungible tokens, need I say more? Yes? Oh, well NFTs have certainly had their moment in 2021, but the question of what they do or what can be done with them has certainly been getting voiced more frequently as the speculative gold rush begins to cool off and people start to think more about how digital goods can evolve in the future.

Anima, a small creative crypto startup built by the founders of photo/video app Ultravisual, which Flipboard acquired back in 2014, is looking to use AR to shift how NFT art and collectibles can be viewed and shared. Their latest venture is an effort to help artists bring their digital creations to a bigger digital stage and help find what the future of NFTs looks like in augmented reality.

The startup has put together a small $500K pre-seed round from Coinbase Ventures, Divergence Ventures, Flamingo DAO, Lyle Owerko and Andrew Unger.

“As NFTs move away from being a more speculative market where it’s all about returns on your purchases, I think that’s healthy and it’s good for us specifically because we want to make things that are more approachable,” co-founder Alex Herrity says.

Their broader vision is finding ways for digital objects to interact with the real world, something that’s been a pretty top-of-mind concern for the AR world over the last few years, though augmented reality development has cooled more recently as creators have sunk into a wait-and-see attitude toward new releases from Apple and Facebook. Both the AR and NFT spaces are incredibly early, something Anima’s co-founders were quick to admit, but they think both spaces have matured enough that the gimmicks are out in the open.

“There’s a context shift that happens when you see AR as a vehicle to have a tactile relationship with something that you collected or that you see is a lifestyle accessory versus the common thing now where it’s a little bit more of an experiential gimmick,” co-founder Neil Voss tells TechCrunch.

The team has worked with a couple artists already as they’ve made early experiments in bringing digital art objects into AR and they’re launching a marketplace late next month based on ConsenSys’s Palm platform, where they hope to showcase more of their future partnerships.

Powered by WPeMatico

As decentralized currencies have taken off in recent months, there’s been renewed attention around DAOs, or Decentralized Autonomous Organizations, as a means of bringing together groups of investors who can deploy capital as a unit while voting collectively on those investments. In the spirit of blockchain, they aim to bring greater transparency to investment decision-making.

A number of high-profile DAOs have launched in recent months as the fervor for crypto mania increased. Komorebi Collective, launching today, is a new organization founded by women in the blockchain space that will be making investments exclusively in “exceptional female and nonbinary crypto founders,” founding member Manasi Vora tells TechCrunch.

The group is comprised of a number of core team members largely assembled from the crypto nonprofit she256 and the organization Women in Blockchain, including Vora, Eva Wu, Kristie Huang, Medha Kothari and Kinjal Shah, who will collectively do most of the heavy lifting behind finding and presenting investments to the group. Other hand-selected members who committed a minimum of $5,000 USD will likely have a lighter commitment.

Each investment will be voted on by all the collective’s key signers, some 36 in total, the majority of whom are female.

“DAOs level the hierarchy of a venture fund by ensuring everyone is going to have a seat at the table,” says Shah, who is also an investor at crypto VC firm Blockchain Capital. “We are very careful in approaching the backers that are really mission-aligned.”

Other members of the DAO include firms like Kleiner Perkins, Mechanism Capital, Dragonfly Capital, IDEO CoLab Ventures and Stacks Accelerator alongside a number of individuals and founders who work at firms like Twitter, Coinbase, Skynet Labs, Celo Labs and Gitcoin.

The organization itself is built on the Syndicate Protocol, a project that shares some of Komorebi Collective’s backers.

The group hopes the structure of their organization will be able to take a mission-driven approach that improves diversity in the crypto space while proving the sustainability of the DAO model. Despite an explosion in startup investments in the past year, women-led startups received just 2.3% of venture dollars invested in 2020, a study in HBR found.

“There’s so much more room to grow when it comes to female founders getting funding and I want to be part of the solution,” Shah tells TechCrunch.

Powered by WPeMatico

Microsoft didn’t rush to bring blockchain technology to its Azure cloud computing platform, but over the course of the last year, it started to pick up the pace with the launch of its blockchain development kit and the Azure Blockchain Workbench. Today, ahead of its Build developer conference, it is going a step further by launching Azure Blockchain Services, a fully managed service that allows for the formation, management and governance of consortium blockchain networks.

We’re not talking cryptocurrencies here, though. This is an enterprise service that is meant to help businesses build applications on top of blockchain technology. It is integrated with Azure Active Directory and offers tools for adding new members, setting permissions and monitoring network health and activity.

The first support ledger is J.P. Morgan’s Quorum. “Because it’s built on the popular Ethereum protocol, which has the world’s largest blockchain developer community, Quorum is a natural choice,” Azure CTO Mark Russinovich writes in today’s announcement. “It integrates with a rich set of open-source tools while also supporting confidential transactions—something our enterprise customers require.” To launch this integration, Microsoft partnered closely with J.P. Morgan.

The managed service is only one part of this package, though. Microsoft also today launched an extension to Visual Studio Code to help developers create smart contracts. The extension allows Visual Studio Code users to create and compiled Etherium smart contracts and deploy them other on the public chain or on a consortium network in Azure Blockchain Service. The code is then managed by Azure DevOps.

Building applications for these smart contracts is also going to get easier thanks to integrations with Logic Apps and Flow, Microsoft’s two workflow integration services, as well as Azure Functions for event-driven development.

Microsoft, of course, isn’t the first of the big companies to get into this game. IBM, especially, made a big push for blockchain adoption in recent years and AWS, too, is now getting into the game after mostly ignoring this technology before. Indeed, AWS opened up its own managed blockchain service only two days ago.

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

Chris Hays and Mark Jeffrey wanted to create a way for everyone to be able to tell their loved ones if they were in trouble. Their first product, Guardian Circle, did just that, netting a mention a few years ago. Now the same team is truly decentralizing alerts with a new token called, obviously, Guardium.

The plan is to create an ad hoc network of helpers and first responders. “Guardium and Guardian Circle together open the emergency response grid to vetted citizens, private response and compatible devices for the very first time,” write the founders. “Providing an economic framework on our global distributed emergency response network; Guardium brings first responders to the 4 billion people on the planet without government-sponsored emergency response.”

Because the product already works, the team is taking on the token sale as a new challenge.

“We’re serial entrepreneurs — both of us have been venture-backed in the past by names like SoftBank and Intel, and we’ve been senior execs in companies backed by Sequoia and Elon Musk. Transitioning to the token sale-backed universe has been an interesting study in contrasts,” said Hays. “There are a number of ‘panic button apps’ — but without exception, all of them have forgotten ‘the second half of the problem’ — organizing the response. Getting people who do not know one another into instant communication and location sharing during an emergency — the importance of that cannot be overstated.”

The founders found that their idea wasn’t fundable in the valley. After all, what VC wants to help people when they can invest in Snapchat? Instead, Hays and Jeffrey are aiming bigger.

“We’re rebooting the world’s safety grid,” said Hays. “We’re creating a new global public utility. And we want it to service everyone, everywhere on earth. Although it is a very big vision, and it is a capitalist, multibillion dollar ecosystem that we’re chasing — it’s still a very different vision, and not the one venture capitalists are looking for.”

The token works to create a flash mob of help. Guard tokens pay first responders and dispatchers and “cities, campuses, and resorts stake $GUARD to access Alerts created within their geofenced borders,” allowing local folks to help immediately. They’ve sold half of their hard cap of $10 million thus far.

While tokens are always an iffy investment, this team has produced product and, more important, it’s clear they’ll never raise venture. A token, no matter how it’s used in the future, seems like a solid solution.

Powered by WPeMatico

Minds, a decentralized social network, has raised $6 million in Series A funding from Medici Ventures, Overstock.com’s venture arm. Overstock CEO Patrick Byrne will join the Minds Board of Directors.

What is a decentralized social network? The creators, who originally crowdfunded their product, see it as an anti-surveillance, anti-censorship, and anti-“big tech” platform that ensures that no one party controls your online presence. And Minds is already seeing solid movement.

“In June 2018, Minds saw an enormous uptick in new Vietnamese of hundreds of thousands users as a direct response to new laws in the country implementing an invasive ‘cybersecurity’ law which included uninhibited access to user data on social networks like Facebook and Google (who are complying so far) and the ability to censor user content,” said Minds founder Bill Ottman.

“There has been increasing excitement in recent years over the power of blockchain technology to liberate individuals and organizations,” said Byrne. “Minds’ work employing blockchain technology as a social media application is the next great innovation toward the mainstream use of this world-changing technology.”

Interestingly, Minds is a model for the future of hybrid investing, a process of raising some cash via token and raising further cash via VC. This model ensures a level of independence from investors but also allows expertise and experience to presumably flow into the company.

Ottman, for his part, just wants to build something revolutionary.

“The rise of an open source, encrypted and decentralized social network is crucial to combat the big-tech monopolies that have abused and ignored users for years. With systemic data breaches, shadow-banning and censorship, people over the world are demanding a digital revolution. User-safety, fair economies, and global freedom of expression depend on it – we are all in this battle together,” said Ottman.

Powered by WPeMatico

Many doubted The Civil Media Company‘s ambitious plan to sell $8 million worth of its cryptocurrency, called CVL.

The skeptics, as it turns out, were right. Civil’s initial coin offering, meant to fund the company’s effort to create a new economy for journalism using the blockchain, failed to attract sufficient interest. The company announced today that it would provide refunds to all CVL token buyers by October 29.

Civil’s goal was to sell 34 million CVL tokens for between $8 million and $24 million. The sale began on September 18 and concluded yesterday. Ultimately, 1,012 buyers purchased $1,435,491 worth of CVL tokens. A spokesperson for Civil told TechCrunch an additional 1,738 buyers successfully registered for the sale, but never completed their transaction.

Civil isn’t giving up. The company says “a new, much simpler token sale is in the works,” details of which will be shared soon. Once those new tokens are distributed, Civil will launch three new features: a blockchain-publishing plugin for WordPress, a community governance application called The Civil Registry and a developer tool for non-blockchain developers to build apps on Civil.

ConsenSys, a blockchain venture studio that invested $5 million in Civil last fall, has agreed to purchase $3.5 million worth of those new tokens. The purchase is not an equity; all capital from the token sale is committed to the Civil Foundation, an independent nonprofit initially funded by Civil that funds grants to the newsrooms in Civil’s network.

In a blog post today, Civil chief executive officer Matthew Iles wrote that the token sale failure was a disappointment but not a shock. Days prior, he’d authored a separate post where he admitted things weren’t looking good.

“This isn’t how we saw this going,” Iles wrote. “The numbers will show clearly enough that we are not where we wanted to be at this point in the sale when we started out. But one thing we want to say at the top is that until the clock strikes midnight on Monday, we are still working nonstop on the goal of making our soft cap of $8 million.”

A recent Wall Street Journal report claimed Civil had reached out to The New York Times, The Washington Post, Dow Jones and Axios, among others, but failed to incite interest in its token.

Separate from its token sale, Civil has inked strategic partnerships with media companies like the Associated Press and Forbes, both of which confirmed to TechCrunch today that the failed token sale doesn’t impact their partnerships with Civil.

Forbes became the first major media brand to test Civil’s technology when it announced earlier this month that it would experiment with publishing content to the Civil platform. As for the AP, it granted the newsrooms in Civil’s network licenses to its content.

Civil, of course, isn’t the only blockchain startup targeting journalism. Nwzer, Userfeeds, Factmata and Po.et, which was founded by Jarrod Dicker, a former vice president at The Washington Post, are all trying their hand at bringing the new technology to the content industry.

Which, if any, will actually find success in the complicated space, is the question.

Powered by WPeMatico

SpankChain, a cryptocurrency aimed at decentralized sex cams, has announced that a hacker stole about $38,000 from their payment channel thanks to a broken smart contract. They wrote:

At 6pm PST Saturday, an unknown attacker drained 165.38 ETH (~$38,000) from our payment channel smart contract which also resulted in $4,000 worth of BOOTY on the contract becoming immobilized. Of the stolen/immobilized ETH/BOOTY, 34.99 ETH (~$8,000) and 1271.88 BOOTY belongs to users (~$9,300 total), and the rest belonged to SpankChain.

Our immediate priority has been to provide complete reimbursements to all users who lost funds. We are preparing an ETH airdrop to cover all $9,300 worth of ETH and BOOTY that belonged to users. Funds will be sent directly to users’ SpankPay accounts, and will be available as soon as we reboot Spank.Live.

The hacker used a ‘reentrancy’ bug in which the user calls the same transfer multiple times, draining a little Ethereum each time. The bug is the same one that previously affected the DAO.

The company pointed out that a security audit on their smart contract would have cost $50,000, a bit more than the amount lost. “As we move forward and grow, we will be stepping up our security practices, and making sure to get multiple internal audits for any smart contract code we publish, as well as at least one professional external audit,” they wrote.

I’ve reached out to the company for clarification but in short it seems the spanker has become the spankee.

Powered by WPeMatico