blockchain

Auto Added by WPeMatico

Auto Added by WPeMatico

As the infrastructure for developing games becomes more advanced, studios have turned to buying best-in-class technology from others instead of building everything from scratch (often with inferior quality).

This shift underpinned Unity’s rise as the most popular game engine. The current focus on games as ever-evolving social hubs that can remain popular for a decade requires investment in “live ops” to keep updating the game with new features and experiences, only adding to a game studio’s responsibilities.

There are big movements in gaming right now to make games cross-platform (not just restricted to mobile or PC or one console), incorporate new types of chat (in-game or outside of it) and to automatically remove bullies and bots among other things. Optimizing games’ virtual economies is only getting more complex as trade of virtual goods becomes increasingly popular.

All this means more opportunity for startups (and large incumbents) that provide new tools and platforms to game developers and gamers. To gauge which opportunities are prime for entrepreneurs, I asked four leading early-stage investors who focus on the gaming sector to share their analysis:

Which areas within gaming infrastructure seem firmly dominated by large incumbents, versus open for new startups to rise up?

I’m always rooting for the startup, but some of the really big and expensive infrastructure challenges seem unlikely to be solved by a startup, especially where the incumbents have a lead in time, money and the personnel they’re throwing at the problem. I’m thinking here, for example, about something like cloud computing, storage solutions, etc.

Powered by WPeMatico

Securitization is a critical function of the modern financial system. Banks “package” individual loans, say a mortgage or an auto loan, into a group with similar characteristics and sell them to other investors. That gets the debt off the originator’s balance sheet so that they can offer more loans, while also offering private investors alternative investment opportunities to buy up.

Despite the scale of the market — the trade association SIFMA’s research shows that the volume for asset-backed securities reached more than $300 billion in 2019 (excluding mortgages) — much of that structuring remains relatively ad hoc, with structuring agents and buyers constantly seeking each other out.

Much in the way that real estate and startup crowdsourcing platforms democratized access to those alternative investments, Cadence wants to expand access to securitized products while increasing the velocity of transactions for originators and lowering prices. Founder and CEO Nelson Chu said that “our job is to bring transparency and efficiency to this market and through all the various things that we do.” The company operates on top of the Ethereum blockchain network.

Founded in 2018 and launched publicly in 2019, the New York City-based capital markets startup has now structured $88 million in notes across 76 offerings and 12 originators according to the company. The firm’s public leaderboard shows that the largest originators were Sellers Funding with more than $23 million and Wall Street Funding with almost $26 million in transaction volume. Chu said that “I think we are the 21st largest structuring agent the United States in 2020 so far,” which is not a bad place to be for a young startup in a massive multi-trillion dollar market.

In addition to that $88 million volume processed on the company’s retail platform, Cadence also structured a $40 million whole business securitization with FAT Brands, the owner of restaurant chains like Fatburger and Yalla Mediterranean. The company notes that the structuring reduced the company’s interest costs by $2 million.

The company has hit a number of milestones over the past two years. It closed a seed round of $4 million in December led by Revel VC, with Revel’s Thomas Falk, Navtej S. Nandra, former President of E*Trade, and portfolio manager Oliver Wriedt joining the company’s board.

In addition, back in 2019, the company said that it also became the first digital asset company to launch a digital asset ticker on Bloomberg Terminal and also the first to join the Bloomberg App Portal. It also secured the first financial debt rating for a digital asset.

The company has a variety of revenue streams from different areas of its platform. It takes transaction fees on each deal, but also derives revenues from hosting data related to the performance of the underlying loans. Given the company’s technology stack, it has better and more verified data about how the underlying assets that back each security are performing, giving all investment holders a much more robust look at the health of their portfolio.

Longer term, Cadence’s goal is to move to a mostly SaaS model for originators and buyers. “We can be very, very beneficial to every single counterparty involved when we become that,” Chu said, adding “we essentially are Switzerland … because our incentives are all aligned.”

I asked about how the company is responding to the COVID-19 situation, and Chu said that as the world saw in the 2008 global financial crisis, “there are pockets of opportunity here that we continue to find, and we allow retail, accredited investors to get access to that.” Chu gave the example of game developers waiting on payments from Apple and Google who need short-term loans to cover costs.

In addition to Revel, other investors in the seed round included Morgan Creek Digital, Nimble Ventures, Argo, Tuesday Capital, Manatt, and Recharge Capital. R&R Venture Partners, a joint VC firm of former Citi chairman Richard D. Parsons and Clinique chairman Ronald S. Lauder, also participated.

Powered by WPeMatico

Xage, a startup that has been taking an unusual path to secure legacy companies like oil and gas and utilities with help from the blockchain, announced a new data protection service today.

Xage CEO Duncan Greatwood, says that up until this point, the company has concentrated on protecting customers at the machine layer, but today’s announcement involves protecting data as it travels between parties, which is more of a classic blockchain security scenario.

“We are moving beyond the protection of machines with greater focus on the protection of data. And this announcement around Dynamic Data Security that we’re delivering today is really a data protection layer that spans multiple dimensions. So it spans from the physical machine layer right up to business transaction,” Greatwood explained.

He says that what separates his company from competitors is the ability to have that protection up and down the stack. “We can guarantee the authenticity, integrity and the confidentiality of data, as it’s produced at the machine, and we can maintain that all the way to [delivery to the various parties],” he said.

Greatwood says that this solution is designed to help protect data, even in highly complex data sharing scenarios, using the blockchain as the trust mechanism. Imagine a supply chain scenario in which the parties are sharing data, but each participant only needs to see the piece of data they need to complete their part of the transaction and no more. To do this, Xage has the concept of security fabric, which acts as a layer of protection across the platform.

“What Xage is doing is to use this kind of security outsource approach we bring to authenticity, integrity and confidentiality, and then using the fabric to replicate all of that security metadata across the extent of the fabric, which may very well cover multiple locations and multiple participants,” he said.

This approach enables customers to have confidence in the providence and integrity of the data they are seeing. “We’re able to allow all of the participants to define a set of security policies that gives them control of their own data, but it also allows them to share very flexibly with the rest of the participants in the ecosystem, and to have confidence in that data, up to and including the point where they’ll pay each other money, based on the integrity of the data.”

The new solution is available today. It has been in testing with three beta customers, which included an oil and gas customer, a utility and a smart city scenario.

Xage was founded in 2016 and has raised just over $16 million, according to PitchBook data.

Powered by WPeMatico

Coinbase’s mobile wallet app Coinbase Wallet puts you in control of your crypto assets. The app already lets you access decentralized crypto apps (dapps) using a dapp browser. But Coinbase is going one step further, with deep integrations with some of the most popular DeFi projects.

DeFi means “decentralized finance,” and it has been a hot trend in the cryptocurrency space. DeFi projects try to reproduce traditional financial products in the blockchain. For instance, you can lend and borrow money, invest in derivative assets and more.

A popular category of DeFi projects has been lending protocols, such as Compound and dYdX. Those protocols work pretty muck like LendingClub, but on the blockchain. Some users send money to a DeFi lending project to contribute to liquidity pools. Other users borrow money from that pool. Interest rates go up and down depending on supply and demand.

With today’s update, you can contribute to lending protocols much more easily. Coinbase Wallet lets you pick a cryptocurrency, compare interest rates across multiple DeFi protocols, interact with those protocols and view your balances in a unified dashboard, you don’t have to use Coinbase Wallet’s dapp browser.

Interest rates will change over time. At any time, you can check the current interest rate, see how much you’ve earned already and withdraw your crypto assets.

Those protocols rely on collateralized borrowing in order to avoid default payments. It means that borrowers have to lock crypto assets as collateral. You often have to provide a bigger collateral than what you’re trying to borrow with those DeFi protocols — that’s the downside of not relying on credit history and external financial data.

Again, this isn’t a traditional finance product. Your deposits are not insured and there could be some bugs in DeFi protocols. For instance, bZx recently suffered from a “flash loan” attack. But it’s an interesting crypto use case.

Powered by WPeMatico

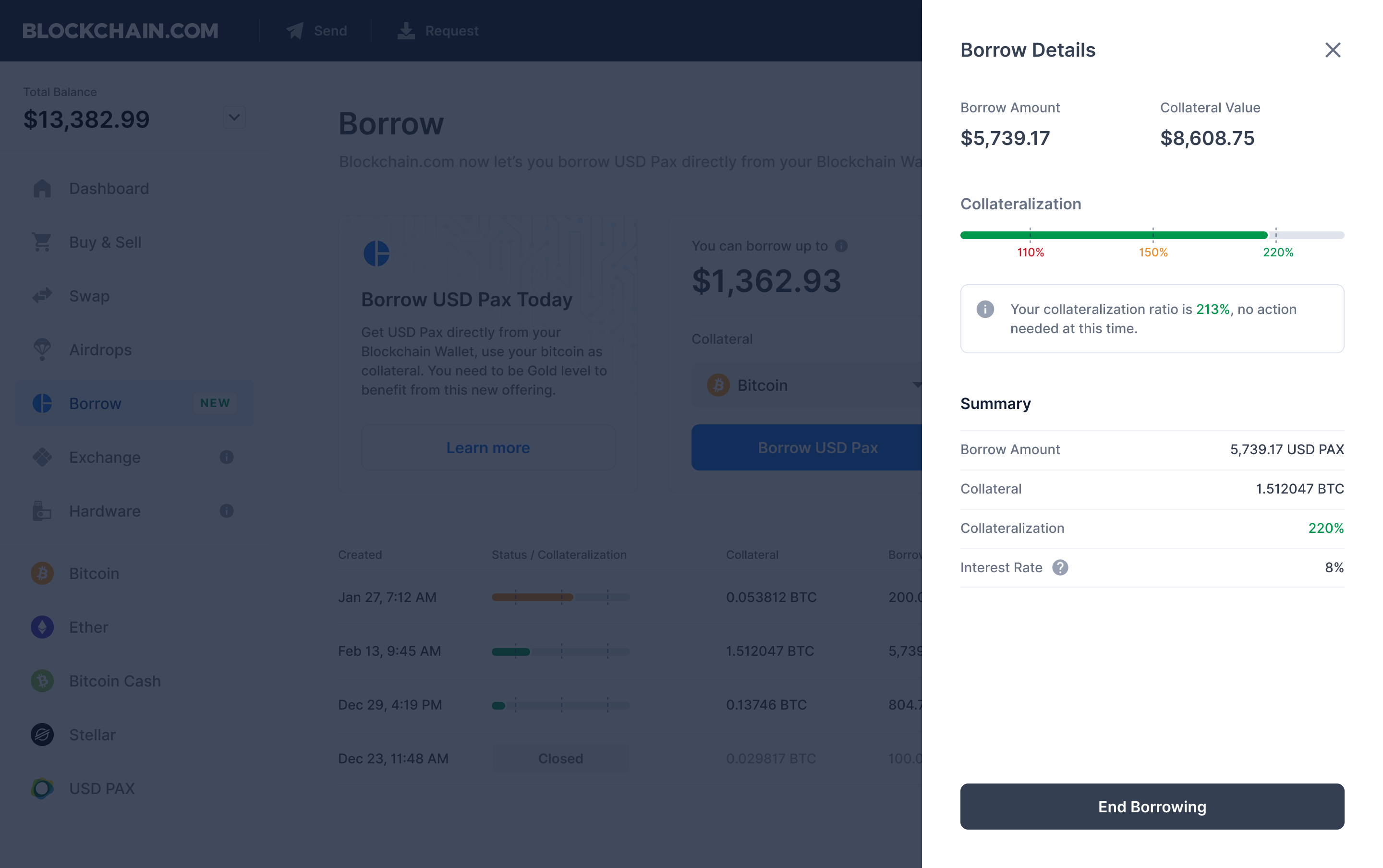

lets you borrow USD PAX against collateral")

What do you do when you’re rich in cryptocurrencies but you don’t want to sell your positions? The company named Blockchain thinks it has found a solution. It lets you borrow money against cryptocurrencies held in your Blockchain wallet.

As soon as you lock cryptocurrencies in your wallet, you receive USD PAX, a stablecoin that is pegged against USD. You can then convert, send and do whatever you want with your stablecoins. You can pay back your loan whenever you want.

The minimum loan size is $1,000 and Blockchain requires a collateralization ratio of 200%. It means that if you want to borrow $5,000, you need to put down the equivalent of $10,000 in cryptocurrencies as collateral.

Blockchain charges interest on loans. Your interest rate may vary but the company tries to be transparent about it before you accept the loan. By default, Blockchain uses your collateral to collect interest. Be careful with the value of your cryptocurrencies, as your collateral could end up losing a ton of value even though you still owe USD.

Behind the scene, Blockchain is running a lending desk for institutional investors. The company launched this feature back in August. Blockchain thinks that it has built a strong liquidity pool that it can leverage with retail investors.

Users in the U.S., Canada and the U.K. are not eligible to the feature for now. Blockchain only accepts collateral in BTC for now.

Powered by WPeMatico

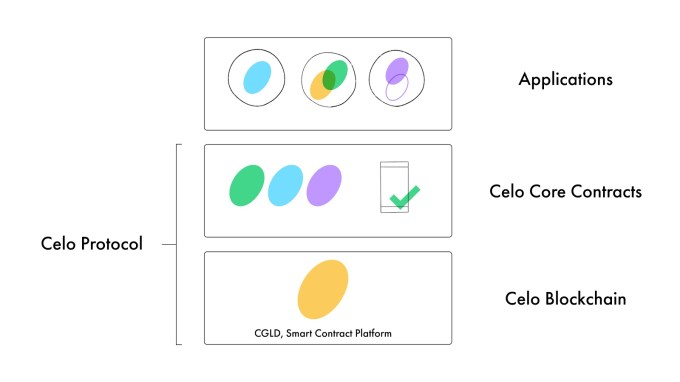

Some Libra Association members like Andreessen Horowitz and Coinbase Ventures are double-dipping, backing a competing cryptocurrency developer platform. Launching today with over 50 partners, non-profit The Celo Foundation’s ‘Alliance For Prosperity’ offers a way for developers to build decentralized mobile apps that are based on Celo’s blockchain platform and USD stablecoin.

The open-source Celo platform is still in testing with plans to officially launch its mainnet in April. The non-profit founded in 2017 has raised $36.4 million, including its Series A where Andreessen Horowitz’s a16z Crypto bought $15 million worth of Celo Gold tokens.

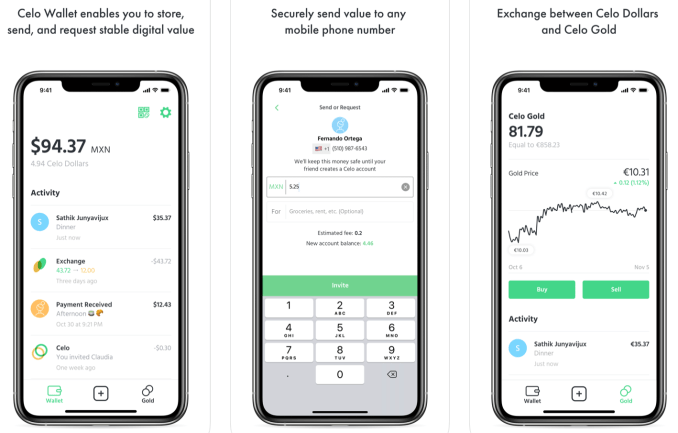

The biggest differentiator of Celo’s network versus other blockchains is that payments in the Celo Dollar stablecoin can be sent to people’s phone numbers rather than complicated addresses. The goal is to make delivering utility via blockchain easier by building a flexible network of applications that doesn’t scare regulators like Libra has.

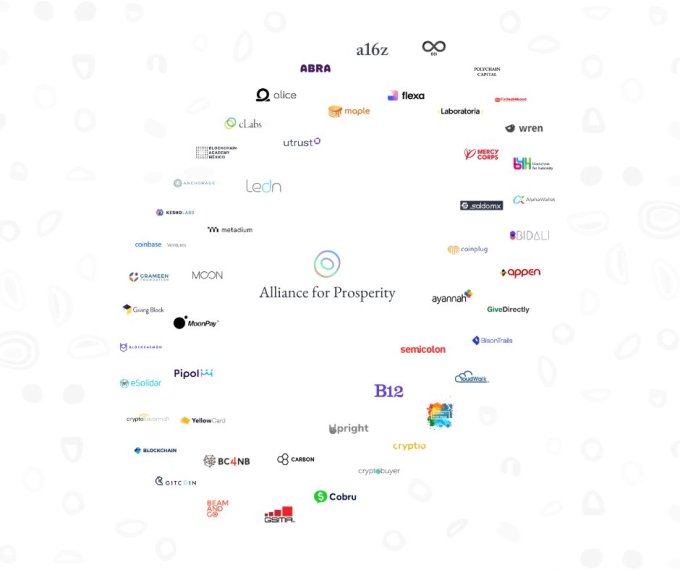

The Alliance For Prosperity includes Andreessen Horowitz (which funded Celo), Coinbase (Ventures), Bison Trails, Anchorage, and Mercy Corps — all of which are also Libra Association members. That could potentially create a conflict of interest regarding which cryptocurrency and developer platform they promote to their portfolio companies, integrate into their products, or focus on for delivering financial services to the needy.

Other high-profile Alliance partners include Carbon, GiveDirectly, Grameen Foundation, Maple, and Polychain. Partners have made a somewhat vague commitment to “backing development efforts of the project, building infrastructure, implementing desired use cases on the platform, integrating Celo assets in their projects, or collaborating on education campaigns in their communities to further advance the use of blockchain technology” according to Chuck Kimble, Celo’s cLabs head of business development and head of the Alliance. Anyone can apply to join the open network, and there’s no minimum financial investment like Libra’s $10 million prerequisite.

Celo isn’t trying to replace the dollar with its own synthetic currency, and its reserve is backed with other cryptocurrencies rather than fiat cash. That might make it more acceptable to regulators who were worried that Libra’s token and fiat currency bundle-backed reserve could impact the global financial system. The first of the decentralized apps on the platform, the Celo Wallet, is already available for iOS and Android.

Like many blockchain projects, there are some lofty intentions for social impact with Celo. Use cases include “powering mobile and online work, enabling faster and affordable remittances, reducing the operational complexities of delivering humanitarian aid, facilitating payments, and enabling microlending” says Kimble. The real driver of this potential is Celo’s promise of much lower transaction fees than traditional middlemen charge.

When asked what the biggest threats to Celo’s success are, he told me “Banking infrastructure improving faster than we expect” and “Mobile adoption or LTE data not expanding on their current trajectory.” He did not mention the developer fatigue, regulatory scrutiny, technical complexity, or slow adoption of blockchain utilities that have plagued other crypto for good projects.

Here’s the full list of members working towards these goals:

Abra, Alice, AlphaWallet, Anchorage, Appen, Ayannah, Andreessen Horowitz, B12, BC4NB (Blockchain for the Next Billion), BeamAndGo, Bidali, Bison Trails, Blockchain Academy Mexico, Blockchain.com, Blockchain for Humanity (b4h), Blockchain for Social Impact (BSIC), Blockdaemon, Carbon, cLabs, CloudWalk Inc, Cobru, Coinbase, Coinplug, Cryptio, Cryptobuyer, CryptoSavannah, eSolidar, Fintech4Good, Flexa, Gitcoin, GiveDirectly, Grameen Foundation, GSMA, KeshoLabs, Laboratoria, Ledn, Maple, Mercy Corps, Metadium, Moon, MoonPay, Pipol, Pngme, Polychain, Project Wren, SaldoMX, Semicolon Africa, The Giving Block, Utrust, Upright, Yellow Card, and 88i. [Update: Ledger joined this morning.]

“Many of these organizations have on-the-ground operations that will begin to get Celo into the hands of those who have been underserved by the current global financial system” Andreessen Horowitz general partner Katie Haun told me. “Our hope is that this partnership will start unlocking the potential of internet money”. To spur adoption, the Alliance will distribute ‘Prosperity Gifts’ in the form of financial grants to developers proposing Celo products that would benefit society.

There are also some peculiar characteristics of Celo’s system. People exchange other cryptocurrencies for Celo Gold, then exchange that for Celo Dollars they can spend. The reserve is backed with other cryptocurrencies like bitcoin and ethereum rather that fiat, and isn’t fully collateralized. That could make it vulnerable to a Celo bank run or crash in price of those currencies. Celo also lets arbitrageurs pocket the difference if Celo Gold and Celo Dollars get out of sync.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

While it might not be a danger to the world financial system like Libra, it could be a danger to itself. At least on the anti-money laundering front, cLabs — the team that’s kicking off development of the Celo platform — has hired former Capital One head of enterprise risk management Jai Ramaswamy. Plus, the Celo founders come well pedigreed, including Marek Olszewski and Rene Reinsberg who spun out machine learning startup Locu from MIT and sold it to GoDaddy, as well as EigenTrust inventor and former MIT Media Lab professor Sep Kamvar.

So far, 130 teams have expressed interest in building on the Celo platform. For reference, Libra said 1,500 organizations had said they wanted to work on that project four months after its reveal. Celo Camp and Blockchain for Social Impact Incubator will also be fostering projects for the blockchain.

Celo could make banking cheaper and more accessible while power new fintech innovation. But for any of that to happen, it will need to get enough developers building truly useful products, make the blockchain and currency exchange simple enough for mainstream audiences in developing nations, and grow adoption to meaningful levels few cryptocurrency projects have yet achieved. The Alliance For Prosperity will have to throw their weight into this project, not just their names, if it’s going to succeed.

Powered by WPeMatico

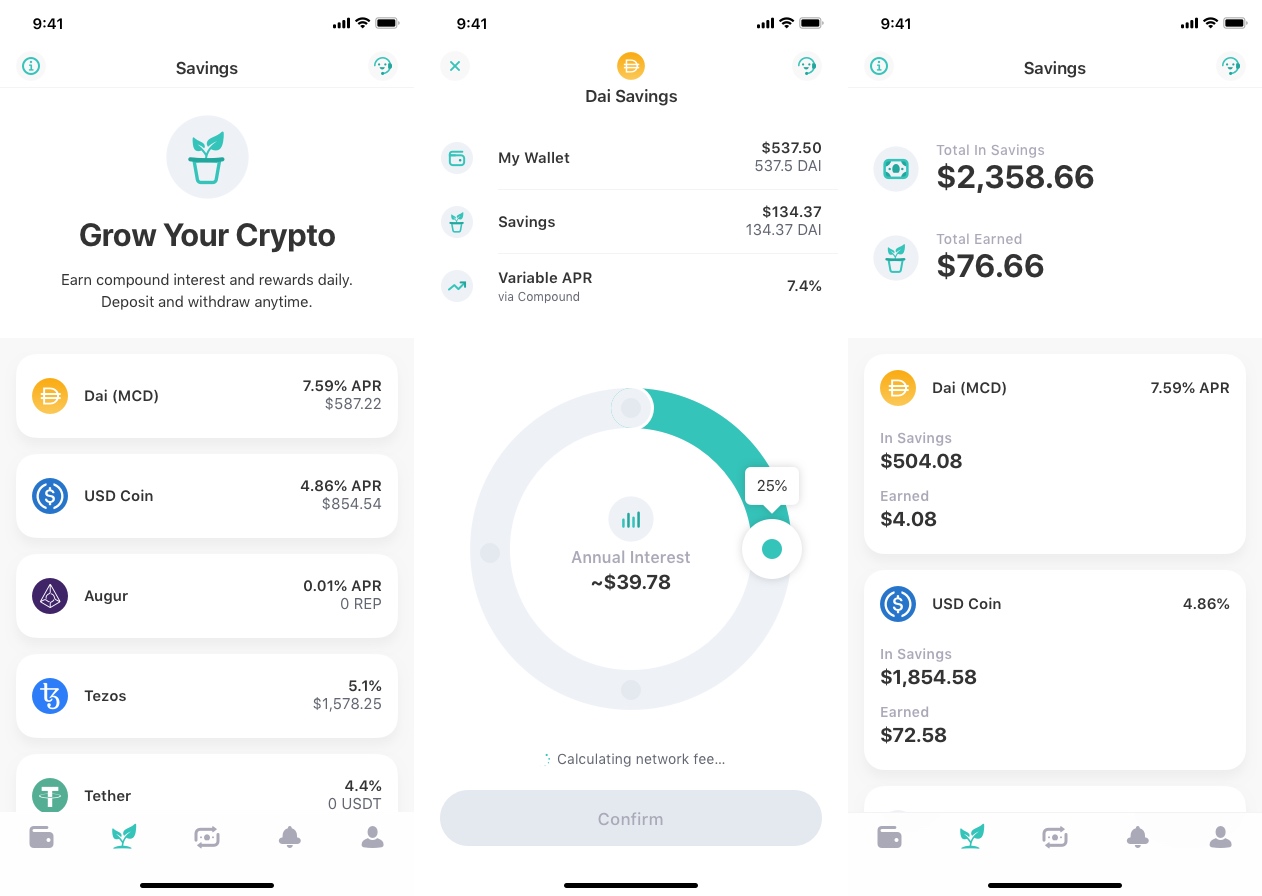

ZenGo is expanding beyond the basic features of a cryptocurrency wallet — letting you hold, send and receive crypto assets. You can now set aside some of your crypto assets to earn interests. In other words, ZenGo now also acts like a savings account.

The company has partnered with two DeFi projects for the new feature. DeFi means “decentralized finance”, and it has been a hot trend in the cryptocurrency space. DeFi projects are the blockchain equivalent of traditional financial products. For instance, you can lend and borrow money, invest in derivative assets and more.

If you want to learn more about DeFi, here’s an article I wrote on the subject:

But let’s come back to ZenGo. When you have crypto assets in your ZenGo wallet, you can now open the savings tab, pick an asset, such as Dai, and select what percentage of your holdings you want to set aside.

After that, all you have to do is wait. You get an overview of your savings “accounts” at any time. This way, you can see your total earned interests. Interests are automatically reinvested over time. You can move your money from those DeFi projects back to your wallet whenever you want.

Behind the scene, ZenGo uses the Compound protocol, a lending DeFi project. It works a bit like LendingClub, but on the blockchain. Some users send money to Compound to contribute to liquidity pools. Other users borrow money from that pool.

Interest rates go up and down depending on supply and demand. That’s why you currently earn more interests when you inject DAI or USD Coin in Compound. But that could change over time.

ZenGo also uses Figment in order to stake Tezos. This time, it isn’t a lending marketplace. When you lock some money in a staking project, it means that you support the operations of a particular blockchain. Few blockchains support staking as they need to be based on proof-of-stake.

For the end user, it looks like a savings account whether you’re relying on Compound or Figment. There are other wallet apps that let you access DeFi projects, such as Coinbase Wallet and Argent. But ZenGo thinks they’re still too complicated for regular users.

Powered by WPeMatico

The world of consumer banking has seen a massive shift in the last ten years. Gone are the days where you could open an account, take out a loan, or discuss changing the terms of your banking only by visiting a physical branch. Now, you can do all this and more with a few quick taps on your phone screen — a shift that has accelerated with customers expecting and demanding even faster and more responsive banking services.

As one mark of that switch, today a startup called Thought Machine, which has built cloud-based technology that powers this new generation of services on behalf of both old and new banks, is announcing some significant funding — $83 million — a Series B that the company plans to use to continue investing in its platform and growing its customer base.

To date, Thought Machine’s customers are primarily in Europe and Asia — they include large, legacy outfits like Standard Chartered, Lloyds Banking Group, and Sweden’s SEB through to “challenger” (AKA neo-) banks like Atom Bank. Some of this financing will go towards boosting the startup’s activities in the US, including opening an office in the country later this year and moving ahead with commercial deals.

The funding is being led by Draper Esprit, with participation also from existing investors Lloyds Banking Group, IQ Capital, Backed and Playfair.

Thought Machine, which started in 2014 and now employs 300, is not disclosing its valuation but Paul Taylor, the CEO and founder, noted that the market cap is currently “increasing healthily.” In its last round, according to PitchBook estimates, the company was valued at around $143 million, which, at this stage of funding, puts this latest round potentially in the range of between $220 million and $320 million.

Thought Machine is not yet profitable, mainly because it is in growth mode, said Taylor. Of note, the startup has been through one major bankruptcy restructuring, although it appears that this was mainly for organisational purposes: all assets, employees and customers from one business controlled by Taylor were acquired by another.

Thought Machine’s primary product and technology is called Vault, a platform that contains a range of banking services: checking accounts, savings accounts, loans, credit cards and mortgages. Thought Machine does not sell directly to consumers, but sells by way of a B2B2C model.

The services are provisioned by way of smart contracts, which allows Thought Machine and its banking customers to personalise, vary and segment the terms for each bank — and potentially for each customer of the bank.

It’s a little odd to think that there is an active market for banking services that are not built and owned by the banks themselves. After all, aren’t these the core of what banks are supposed to do?

But one way to think about it is in the context of eating out. Restaurants’ kitchens will often make in-house what they sell and serve. But in some cases, when it makes sense, even the best places will buy in (and subsequently sell) food that was crafted elsewhere. For example, a restaurant will re-sell cheese or charcuterie, and the wine is likely to come from somewhere else, too.

The same is the case for banks, whose “Crown Jewels” are in fact not the mechanics of their banking services, but their customer service, their customer lists, and their deposits. Better banking services (which may not have been built “in-house”) are key to growing these other three.

“There are all sorts of banks, and they are all trying to find niches,” said Taylor. Indeed, the startup is not the only one chasing that business. Others include Mambu, Temenos and Italy’s Edera.

In the case of the legacy banks that work with the startup, the idea is that these behemoths can migrate into the next generation of consumer banking services and banking infrastructure by cherry-picking services from the VaultOS platform.

“Banks have not kept up and are marooned on their own tech, and as each year goes by, it comes more problematic,” noted Taylor.

In the case of neobanks, Thought Machine’s pitch is that it has already built the rails to run a banking service, so a startup — “new challengers like Monzo and Revolut that are creating quite a lot of disruption in the market” (and are growing very quickly as a result) — can integrate into these to get off the ground more quickly and handle scaling with less complexity (and lower costs).

Taylor was new to fintech when he founded Thought Machine, but he has a notable track record in the world of tech that you could argue played a big role in his subsequent foray into banking.

Formerly an academic specialising in linguistics and engineering, his first startup, Rhetorical Systems, commercialised some of his early speech-to-text research and was later sold to Nuance in 2004.

His second entrepreneurial effort, Phonetic Arts, was another speech startup, aimed at tech that could be used in gaming interactions. In 2010, Google approached the startup to see if it wanted to work on a new speech-to-text service it was building. It ended up acquiring Phonetic Arts, and Taylor took on the role of building and launching Google Now, with that voice tech eventually making its way to Google Maps, accessibility services, the Google Assistant and other places where you speech-based interaction makes an appearance in Google products.

While he was working for years in the field, the step changes that really accelerated voice recognition and speech technology, Taylor said, were the rapid increases in computing power and data networks that “took us over the edge” in terms of what a machine could do, specifically in the cloud.

And those are the same forces, in fact, that led to consumers being able to run our banking services from smartphone apps, and for us to want and expect more personalised services overall. Taylor’s move into building and offering a platform-based service to address the need for multiple third-party banking services follows from that, and also is the natural heir to the platform model you could argue Google and other tech companies have perfected over the years.

Draper Esprit has to date built up a strong portfolio of fintech startups that includes Revolut, N26, TransferWise and Freetrade. Thought Machine’s platform approach is an obvious complement to that list. (Taylor did not disclose if any of those companies are already customers of Thought Machine’s, but if they are not, this investment could be a good way of building inroads.)

“We are delighted to be partnering with Thought Machine in this phase of their growth,” said Vinoth Jayakumar, Investment Director, Draper Esprit, in a statement. “Our investments in Revolut and N26 demonstrate how banking is undergoing a once in a generation transformation in the technology it uses and the benefit it confers to the customers of the bank. We continue to invest in our thesis of the technology layer that forms the backbone of banking. Thought Machine stands out by way of the strength of its engineering capability, and is unique in being the only company in the banking technology space that has developed a platform capable of hosting and migrating international Tier 1 banks. This allows innovative banks to expand beyond digital retail propositions to being able to run every function and type of financial transaction in the cloud.”

“We first backed Thought Machine at seed stage in 2016 and have seen it grow from a startup to a 300-person strong global scale-up with a global customer base and potential to become one of the most valuable European fintech companies,” said Max Bautin, Founding Partner of IQ Capital, in a statement. “I am delighted to continue to support Paul and the team on this journey, with an additional £15 million investment from our £100 million Growth Fund, aimed at our venture portfolio outperformers.”

Powered by WPeMatico

TechCrunch has learned that $28 million-funded crypto startup Tagomi will be the newest member of the Libra Association that governs the Facebook-backed Libra stablecoin. A formal announcement is slated for Friday or next week.

Tagomi offers a platform that helps large traders and funds easily access cryptocurrency markets. The news comes days after Libra added Shopify, a reversal of dwindling membership after major partners like Visa, PayPal and Stripe dropped out late last year.

We’ve reached out to the Libra Association and have been promised a response by Facebook’s communications team.

Joining Libra means Tagomi will be expected to contribute at least $10 million toward developing the cryptocurrency, with that investment eligible to reap dividends from interest earned on money kept in the Libra Reserve. Tagomi will also operate a node that validates transactions coming through the Libra blockchain.

Tagomi was founded by Jennifer Campbell, a former investor at Union Square Ventures, which is also a Libra Association Member. The company has 25 employees across five offices. Tagomi will be the 22nd member of the Libra Association, according to information from the startup’s press representative, who was apparently supposed to hold this news until later. “Tagomi is joining the Libra Foundation and Jennifer will be the newest member,” they emailed TechCrunch. We’ll update this story following our interview with Campbell tomorrow.

Campbell and Tagomi will offer technical and policy support to Libra in an effort to make the cryptocurrency more safe and compliant with international law. That will be critical for the Libra Association to get the green light from regulators for a launch in 2020 like it originally planned. Lawmakers in the U.S. and EU have slammed Libra in hearings and the press over its potential to facilitate money laundering, harm privacy and destabilize the global financial system.

The full membership of the Libra Association is now:

Current Members:

Facebook’s Calibra, Tagomi, Shopify, PayU, Farfetch, Lyft, Spotify, Uber, Illiad SA, Anchorage, Bison Trails, Coinbase, Xapo, Andreessen Horowitz, Union Square Ventures, Breakthrough Initiatives, Ribbit Capital, Thrive Capital, Creative Destruction Lab, Kiva, Mercy Corps, Women’s World Banking.

Former Members:

Vodafone, Visa, Mastercard, Stripe, PayPal, Mercado Pago, Bookings Holdings, eBay.

Powered by WPeMatico

As the number of IoT devices proliferate, and machines conduct transactions with machines without humans involved, it becomes increasingly necessary to have a permissionless system that facilitates this kind of communication in a secure way.

Enter the IOTA Foundation, a Berlin-based open-source distributed ledger technology (DLT) project, which has hooked up with the Eclipse Foundation to bring IOTA DLT to the enterprise via the Tangle EE project. For starters, this involves forming a working group.

The distributed ledger idea first emerged as a way to distribute digital currency on the blockchain. Since then, there have been multiple ideas, both open source and commercial, to bring this concept to the enterprise to provide a secure, immutable and frictionless way to share data.

One such open-source project is IOTA, which saw an issue with DLT as it was being implemented by other entities. “IOTA is the first distributed ledger technology that went beyond blockchain with a completely new architecture that resolves the bottleneck problems of blockchain that has prevented real-world adoption,” Dominik Schiener, co-founder of IOTA Foundation, told TechCrunch.

The broad vision is to provide a way for machines and devices to communicate securely. “We provide a protocol layer that enables both humans and machines to bulk transact value without fees, as well as ensure data integrity, which is, of course, increasingly important in the age of Internet of Things, where hundreds of billions of devices are being connected over the next decades,” Schiener said.

Tangle EE is the part of the project aimed at enterprise users — EE stands for Enterprise Edition — that can take this technology and enable larger organizations to build applications on top of the project. For starters the foundation is working with the Eclipse Foundation to bring corporate entities on board who can help better define the requirements of the large business user.

Dell Technologies and STMicroelectronics are the first major companies joining the project, but the hope is that through discussion and dialogue, Tangle EE will begin to gain traction. “The main reason why we created Tangle EE was because of the discussions that we’ve had with corporations. They really understood that we need to have a working group around IOTA to discuss the application layer, to discuss what kind of solutions we can develop broadly across industries, but also really start having more serious discussions about the protocol,” Schiener said.

Much like the Linux Foundation, the Eclipse Foundation will provide a governance framework for the project. “The Eclipse Foundation will provide a vendor-neutral governance framework for open collaboration, with IOTA’s scalable, feeless and permissionless DLT as a base,” Mike Milinkovich, executive director of the Eclipse Foundation, explained in a statement.

If it gains traction, more companies will join in the coming months and years, and begin building out Tangle EE, while developing applications based on the protocol.

Powered by WPeMatico