BlackRock

Auto Added by WPeMatico

Auto Added by WPeMatico

The two founders of Crusoe Energy think they may have a solution to two of the largest problems facing the planet today — the increasing energy footprint of the tech industry and the greenhouse gas emissions associated with the natural gas industry.

Crusoe, which uses excess natural gas from energy operations to power data centers and cryptocurrency mining operations, has just raised $128 million in new financing from some of the top names in the venture capital industry to build out its operations — and the timing couldn’t be better.

Methane emissions are emerging as a new area of focus for researchers and policymakers focused on reducing greenhouse gas emissions and keeping global warming within the 1.5 degree target set under the Paris Agreement. And those emissions are just what Crusoe Energy is capturing to power its data centers and bitcoin mining operations.

The reason why addressing methane emissions is so critical in the short term is because these greenhouse gases trap more heat than their carbon dioxide counterparts and also dissipate more quickly. So dramatic reductions in methane emissions can do more in the short term to alleviate the global warming pressures that human industry is putting on the environment.

And the biggest source of methane emissions is the oil and gas industry. In the U.S. alone roughly 1.4 billion cubic feet of natural gas is flared daily, said Chase Lochmiller, a co-founder of Crusoe Energy. About two-thirds of that is flared in Texas, with another 500 million cubic feet flared in North Dakota, where Crusoe has focused its operations to date.

For Lochmiller, a former quant trader at some of the top American financial services institutions, and Cully Cavness, a third generation oil and gas scion, the ability to capture natural gas and harness it for computing operations is a natural combination of the two men’s interests in financial engineering and environmental preservation.

NEW TOWN, ND – AUGUST 13: View of three oil wells and flaring of natural gas on The Fort Berthold Indian Reservation near New Town, ND on August 13, 2014. About 100 million dollars’ worth of natural gas burns off per month because a pipeline system isn’t in place yet to capture and safely transport it. The Three Affiliated Tribes on Fort Berthold represent Mandan, Hidatsa and Arikara Nations. It’s also at the epicenter of the fracking and oil boom that has brought oil royalties to a large number of Native Americans living there. (Photo by Linda Davidson / The Washington Post via Getty Images)

The two Denver natives met in prep-school and remained friends. When Lochmiller left for MIT and Cavness headed off to Middlebury they didn’t know that they’d eventually be launching a business together. But through Lochmiller’s exposure to large-scale computing and the financial services industry, and Cavness’ assumption of the family business, they came to the conclusion that there had to be a better way to address the massive waste associated with natural gas.

Conversation around Crusoe Energy began in 2018 when Lochmiller and Cavness went climbing in the Rockies to talk about Lochmiller’s trip to Mt. Everest.

When the two men started building their business, the initial focus was on finding an environmentally friendly way to deal with the energy footprint of bitcoin mining operations. It was this pitch that brought the company to the attention of investors at Polychain, the investment firm started by Olaf Carlson-Wee (and Lochmiller’s former employer), and investors like Bain Capital Ventures and new investor Valor Equity Partners.

(This was also the pitch that Lochmiller made to me to cover the company’s seed round. At the time I was skeptical of the company’s premise and was worried that the business would just be another way to prolong the use of hydrocarbons while propping up a cryptocurrency that had limited actual utility beyond a speculative hedge against governmental collapse. I was wrong on at least one of those assessments.)

“Regarding questions about sustainability, Crusoe has a clear standard of only pursuing projects that are net reducers of emissions. Generally the wells that Crusoe works with are already flaring and would continue to do so in the absence of Crusoe’s solution. The company has turned down numerous projects where they would be a buyer of low-cost gas from a traditional pipeline because they explicitly do not want to be net adders of demand and emissions,” wrote a spokesman for Valor Equity in an email. “In addition, mining is increasingly moving to renewables and Crusoe’s approach to stranded energy can enable better economics for stranded or marginalized renewables, ultimately bringing more renewables into the mix. Mining can provide an interruptible base load demand that can be cut back when grid demand increases, so overall the effect to incentivize the addition of more renewable energy sources to the grid.”

Other investors have since piled on, including: Lowercarbon Capital, DRW Ventures, Founders Fund, Coinbase Ventures, KCK Group, Upper90, Winklevoss Capital, Zigg Capital and Tesla co-founder JB Straubel.

The company now operates 40 modular data centers powered by otherwise wasted and flared natural gas throughout North Dakota, Montana, Wyoming and Colorado. Next year that number should expand to 100 units as Crusoe enters new markets such as Texas and New Mexico. Since launching in 2018, Crusoe has emerged as a scalable solution to reduce flaring through energy intensive computing, such as bitcoin mining, graphical rendering, artificial intelligence model training and even protein folding simulations for COVID-19 therapeutic research.

Crusoe boasts 99.9% combustion efficiency for its methane, and is also bringing additional benefits in the form of new networking buildout at its data center and mining sites. Eventually, this networking capacity could lead to increased connectivity for rural communities surrounding the Crusoe sites.

Currently, 80% of the company’s operations are being used for bitcoin mining, but there’s increasing demand for use in data center operations, and some universities, including Lochmiller’s alma mater of MIT, are looking at the company’s offerings for their own computing needs.

“That’s very much in an incubated phase right now,” said Lochmiller. “A private alpha where we have a few test customers… we’ll make that available for public use later this year.”

Crusoe Energy Systems should have the lowest data center operating costs in the world, according to Lochmiller and while the company will spend money to support the infrastructure buildout necessary to get the data to customers, those costs are negligible when compared to energy consumption, Lochmiller said.

The same holds true for bitcoin mining, where the company can offer an alternative to coal-powered mining operations in China and the construction of new renewable capacity that wouldn’t be used to service the grid. As cryptocurrencies look for a way to blunt criticism about the energy usage involved in their creation and distribution, Crusoe becomes an elegant solution.

Institutional and regulatory tailwinds are also propelling the company forward. Recently New Mexico passed new laws limiting flaring and venting to no more than 2% of an operator’s production by April of next year, and North Dakota is pushing for incentives to support on-site flare capture systems while Wyoming signed a law creating incentives for flare gas reduction applied to bitcoin mining. The world’s largest financial services firms are also taking a stand against flare gas with BlackRock calling for an end to routine flaring by 2025.

“Where we view our power consumption, we draw a very clear line in our project evaluation stage where we’re reducing emissions for an oil and gas projects,” Lochmiller said.

Powered by WPeMatico

There’s no denying that 2020 has been the year of the special purpose acquisition company.

Since the beginning of the year, 219 SPACs have raised $73 billion, according to widely reported market research from Goldman Sachs. That’s a 462% jump from 2019 and more than traditional public offerings raised by about $6 billion. By some counts, roughly one quarter of the SPACs that have been announced will target climate-related businesses.

Since the beginning of the year, 219 SPACs have raised $73 billion.

Already, of the 78 deals that have either completed or announced a merger since 2018, just over one-third have been climate-related, as tallied by Climate Tech VC. And these SPACs have outperformed the broader technology market, with the 10 climate tech companies that have completed mergers averaging a 131% return on investment versus the 50% return of the total SPAC market (assuming average offering prices of $10 per share).

Clearly this has been a banner year for companies that are tackling the climate crisis across a number of verticals, but can it last?

There are a few reasons to think that it can — led chiefly by the demand for these kinds of public offerings from institutional investors, including the pension funds, mutual funds and asset managers handling trillions of investment dollars.

“[The] current wave [of SPACs] is because over the past 24 months the institutional investor universe has come fully into believing that climate solutions are going to be a major growth area in the 2020s and beyond, but they weren’t seeing options available to them for investing into,” wrote longtime clean technology investor, Rob Day, in a DM.

“The available publicly traded ‘green’ companies were already getting really bought up, and the private equity options were underwhelming as well (smallish in the case of VC, low returns in the case of large-format projects). Throw in a Robinhood market of retail investors with a lot of enthusiasm for EVs and such, and you have a nice recipe for this to happen.”

Powered by WPeMatico

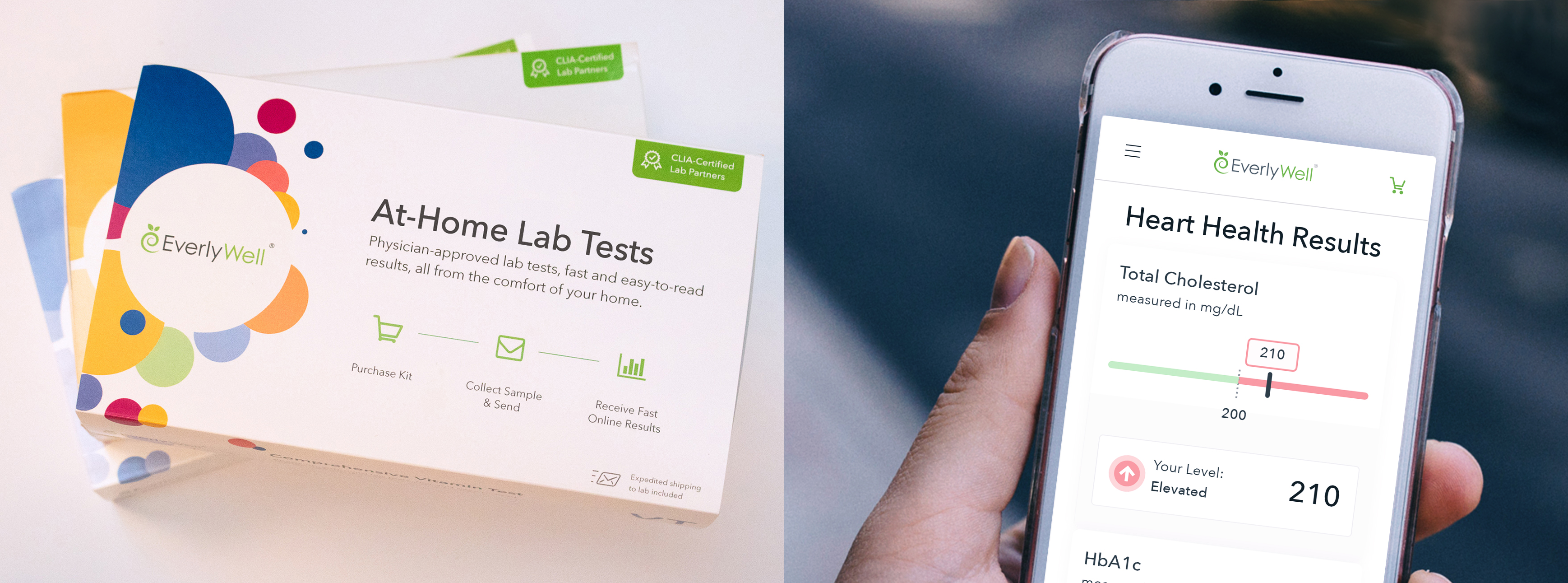

Digital health startup Everlywell has raised a $175 million Series D funding round, following relatively fast on the heels of a $25 million Series C round it closed in February of this year. The Series D included a host of new investors, including BlackRock, The Chernin Group (TCG), Foresite Capital, Greenspring Associates, Morningside Ventures and Portfolio, along with existing investors including Highland Capital Partners, which led the Series C round. The startup has now raised more than $250 million to date.

Everlywell, which launched to the public at TechCrunch Disrupt SF 2016 as a participant in Startup Battlefield, specializes in home healthcare, and specifically on home healthcare tests supported by their digital platform for providing customers with their results and helping them understand the diagnostics, and how to seek the right follow-on care and expert medical advice.

Earlier this year, Everlywell launched an at-home COVID-19 test collection kit — the first of this type of test to receive an emergency authorization from the U.S. Food and Drug Administration (FDA) for its use that allowed cooperation with multiple lab service providers over time. The COVID-19 test kit joins its many other offerings, which include tests for thyroid hormone levels, food and allergen sensitivity, women’s health and fertility, vitamin D deficiency and more. I spoke to Everlywell CEO and founder Julia Cheek about the raise, and she acknowledged that the COVID-19 pandemic was definitely behind the decision to raise such a large amount so quickly again after the close of the Series C, since the company saw a sharp increase in demand coming out of the coronavirus crisis — not only for its COVID-19 test kit, but for at-home digital healthcare options in general.

“We obviously have a very successful COVID-19 test,” she said. “But we’ve also seen three-fourths of our test menu just explode at well over 100% year-over-year growth, and several of our tests are at 4x or 5x growth. That is really representative of this shift in consumer health behavior that will continue in a big way in many different verticals that include testing, and making things more convenient, digitally-enabled, and in the home.”

Like other companies built on solving for a shift to more remote and virtual care options, Cheek said that Everlywell had already anticipated this kind of consumer demand — but COVID-19 has dramatically accelerated the pace of change, which is why the startup put together this round, at this size, this quickly (she says they started the process of putting together the Series D in September).

“We’ve been talking about the digital health movement, and the consumer-directed movement probably for a decade now,” she told me. “I do believe that this will be the watershed moment, unfortunately. But hopefully, we will come out on the other side of the pandemic and say, ‘There are some good things that happened broadly for healthcare.’ That is the hope of what we lean into everyday, and fundamentally, why we went out and raised this amount of capital in this tremendous growth year.”

Image Credits: Everlywell

Everlywell has also expanded availability of its products this year, with distribution in more than 10,000 retail locations across Target, Walgreens, CVS and Kroger stores across the U.S. The company also landed a number of new partnerships on the diagnostic lab and insurance payer side, as well as with major employers — a key customer group as employers shoulder the largest share of healthcare spending in the U.S. due to employee benefit plans. Cheek says that despite their commercial and enterprise customer wins, the focus remains squarely on consumer satisfaction, which is what distinguishes their offering.

“Our COVID-19 test is 75% new people buying our product, and it has an NPS [net promoter score] of 75,” she said. “And then it’s the most highly referred product, and also one of our top tests where people buy other tests. Experience matters here — we know that if someone is a promoter of Everlywell, if they rate us a nine or a 10, on NPS, they are five times more likely to purchase again on the platform.”

That’s not new for Everlywell, according to Cheek — customers have always had a high degree of satisfaction with the company’s products. But what is new is the expanded reach, and the realization among many Americans that virtual care and at-home options are available, and are effective.

“What you have is this lightbulb moment for Americans in a new way that care can be delivered where then they definitely don’t want to go back,” she said. “It’s not just for Everlywell. This is all of these verticals, that have really shifted consumer behavior around healthcare in the home, and I think that will be somewhat permanent. That is the main driver here, and is what we’re seeing, and it’s why Everlywell has resonated so well with so many Americans.”

Powered by WPeMatico

Leading on-demand digital freight platform Loadsmart has raised a $90 million Series C funding round, led by funds under management by BlackRock and co-led by Chromo Invest. The funding will be used to continue to build out its platform to offer even more end-to-end logistics services to its freight customers, and the company says that it will be doing that in part through new collaboration with strategic investor TFI International, a leader in the logistics space, which also participated in this round.

In addition to TFI, the round also saw renewed investment from Maersk, a global oceanic shipping leader and one of Loadsmart’s strategic backers since its Series A round. The company says it has increased its revenues by 250% across 2020, while at the same time managing to keep its operating expenses flat. In a press release announcing the news, the company seemed to take indirect shots at competitors, including Uber Freight and Convoy, by noting that it has achieved its growth through “organic” means, rather than “by subsidizing its customers’ freight spend” through aggressive pricing.

Loadsmart offers booking for freight transportation across land, rail and through ports, all from a single online portal. It recently added the ability to ship partial truckloads, and its consistency brought in new strategic investors deeply involved in all aspects of the industry, including port management and overland shipping, which is likely contributing to its growth through ever-deeper industry insight.

Powered by WPeMatico

JumpCloud, the cloud directory service that debuted at TechCrunch Disrupt Battlefield in 2013, announced a $75 million Series E today. The round was led by BlackRock with participation from existing investor General Atlantic.

The company wasn’t willing to discuss the current valuation, but has now raised more than $166 million, according to Crunchbase data.

Changes in the way that IT works have been evolving since the company launched. Back then, most companies used Microsoft Active Directory in a Windows-centric environment. Since then, things have gotten more heterogeneous with multiple operating systems, web applications, the cloud and mobile, and that has required a different way of thinking about directory structures.

JumpCloud co-founder and CEO Rajat Bhargava says that the pandemic has only accelerated the need for his company’s kind of service as more companies move to the cloud. “Obviously now with COVID, all these changes made it much more difficult for IT to connect their users to all the resources that they needed, and to us that’s one of the most critical tasks that an IT organization has is making their team productive,” he said.

He said their idea was to build an “independent cloud directory platform that would connect people to really whatever it is they need and do that in a secure way while giving IT complete control over that access.”

The product, which includes a free tier for 10 users on 10 systems for an unlimited amount of time, has 100,000 users. Of those, Bhargava says that about 3,000 are paying.

The company has 300 employees, with plans to add 200-250 in the next year with a goal of adding 500 in the next couple of years. As he does that, Bhargava, who is South Asian, sees diversity and inclusion as an important component of the hiring process. In fact, the company tries to make sure it always has diverse candidates in the hiring pool.

“Some of the things that we’ve tried to do is make sure that every role has some diversity candidates involved in the hiring process. That’s something that our recruiting team is working on and making sure that we’re having that conversation with every single hire,” he said. He acknowledges that it’s a work in progress, and a problem across the entire tech industry that he and his company continue to try to address.

Since the pandemic, the company, which is based in Colorado, has made the decision to be remote first, and they will be hiring from across the country and across the world as they make these new hires, which could help contribute to a more diverse workforce over time.

With a $75 million investment, and having reached Series E, it’s fair to ask if the company is thinking ahead to an IPO, but Bhargava didn’t want to discuss that. “We just raised this $75 million round. There’s so much work to be done, so we’re just looking forward to that right now,” he said.

Powered by WPeMatico

Companies that have leveraged technology to make the procurement and delivery of food more accessible to more people have been seeing a big surge of business this year, as millions of consumers are encouraged (or outright mandated, due to COVID-19) to socially distance or want to avoid the crowds of physical shopping and eating excursions.

Today, one of the companies that is supplying produce and other items both to consumers and other services that are in turn selling food and groceries to them, is announcing a new round of funding as it gears up to take its next step, an IPO.

GrubMarket, which provides a B2C platform for consumers to order produce and other food and home items for delivery, and a B2B service where it supplies grocery stores, meal-kit companies and other food tech startups with products that they resell, is today announcing that it has raised $60 million in a Series D round of funding.

Sources close to the company confirmed to TechCrunch that GrubMarket — which is profitable, and originally hadn’t planned to raise more than $20 million — has now doubled its valuation compared to its last round — sources tell us it is now between $400 million and $500 million.

The funding is coming from funds and accounts managed by BlackRock, Reimagined Ventures, Trinity Capital Investment, Celtic House Venture Partners, Marubeni Ventures, Sixty Degree Capital and Mojo Partners, alongside previous investors GGV Capital, WI Harper Group, Digital Garage, CentreGold Capital, Scrum Ventures and other unnamed participants. Past investors also included Y Combinator, where GrubMarket was part of the Winter 2015 cohort. For some context, GrubMarket last raised money in April 2019 — $28 million at a $228 million valuation, a source says.

Mike Xu, the founder and CEO, said that the plan remains for the company to go public (he’s talked about it before), but given that it’s not having trouble raising from private markets and is currently growing at 100% over last year, and the IPO market is less certain at the moment, he declined to put an exact timeline on when this might actually happen, although he was clear that this is where his focus is in the near future.

“The only success criteria of my startup career is whether GrubMarket can eventually make $100 billion of annual sales,” he said to me over both email and in a phone conversation. “To achieve this goal, I am willing to stay heads-down and hardworking every day until it is done, and it does not matter whether it will take me 15 years or 50 years.”

I don’t doubt that he means it. I’ll note that we had this call in the middle of the night his time in California, even after I asked multiple times if there wasn’t a more reasonable hour in the daytime for him to talk. (He insisted that he got his best work done at 4:30 a.m., a result of how a lot of the grocery business works.) Xu on the one hand is very gentle with a calm demeanor, but don’t let his quiet manner fool you. He also is focused and relentless in his work ethic.

When people talk today about buying food, alongside traditional grocery stores and other physical food markets, they increasingly talk about grocery delivery companies, restaurant delivery platforms, meal kit services and more that make or provide food to people by way of apps. GrubMarket has built itself as a profitable but quiet giant that underpins the fuel that helps companies in all of these categories by becoming one of the critical companies building bridges between food producers and those that interact with customers.

Its opportunity comes in the form of disruption and a gap in the market. Food production is not unlike shipping and other older, non-tech industries, with a lot of transactions couched in legacy processes: GrubMarket has built software that connects the different segments of the food supply chain in a faster and more efficient way, and then provides the logistics to help it run.

To be sure, it’s an area that would have evolved regardless of the world health situation, but the rise and growth of the coronavirus has definitely “helped” GrubMarket not just by creating more demand for delivered food, but by providing a way for those in the food supply chain to interact with less contact and more tech-fueled efficiency.

Sales of WholesaleWare, as the platform is called, Xu said, have seen more than 800% growth over the last year, now managing “several hundreds of millions of dollars of food wholesale activities” annually.

Underpinning its tech is the sheer size of the operation: economies of scale in action. The company is active in the San Francisco Bay Area, Los Angeles, San Diego, Seattle, Texas, Michigan, Boston and New York (and many places in between) and says that it currently operates some 21 warehouses nationwide. Xu describes GrubMarket as a “major food provider” in the Bay Area and the rest of California, with (as one example) more than 5 million pounds of frozen meat in its east San Francisco Bay warehouse.

Its customers include more than 500 grocery stores, 8,000 restaurants and 2,000 corporate offices, with familiar names like Whole Foods, Kroger, Albertson, Safeway, Sprouts Farmers Market, Raley’s Market, 99 Ranch Market, Blue Apron, Hello Fresh, Fresh Direct, Imperfect Foods, Misfit Market, Sun Basket and GoodEggs all on the list, with GrubMarket supplying them items that they resell directly, or use in creating their own products (like meal kits).

While much of GrubMarket’s growth has been — like a lot of its produce — organic, its profitability has helped it also grow inorganically. It has made some 15 acquisitions in the last two years, including Boston Organics and EJ Food Distributor this year.

It’s not to say that GrubMarket has not had growing pains. The company, Xu said, was like many others in the food delivery business — “overwhelmed” at the start of the pandemic in March and April of this year. “We had to limit our daily delivery volume in some regions, and put new customers on waiting lists.” Even so, the B2C business grew between 300% and 500% depending on the market. Xu said things calmed down by May and even as some B2B customers never came back after cities were locked down, as a category, B2B has largely recovered, he said.

Interestingly, the startup itself has taken a very proactive approach in order to limit its own workers’ and customers’ exposure to COVID-19, doing as much testing as it could — tests have been, as we all know, in very short supply — as well as a lot of social distancing and cleaning operations.

“There have been no mandates about masks, but we supplied them extensively,” he said.

So far it seems to have worked. Xu said the company has only found “a couple of employees” that were positive this year. In one case in April, a case was found not through a test (which it didn’t have, this happened in Michigan) but through a routine check and finding an employee showing symptoms, and its response was swift: the facilities were locked down for two weeks and sanitized, despite this happening in one of the busiest months in the history of the company (and the food supply sector overall).

That’s notable leadership at a time when it feels like a lot of leaders have failed us, which only helps to bolster the company’s strong growth.

Powered by WPeMatico

Puppet, the Portland, Oregon-based infrastructure automation company, announced a $40 million debt round today from BlackRock Investments.

CEO Yvonne Wassenaar says the company sees this debt round as part of a longer-term relationship with BlackRock . “What’s interesting, and I think part of the reason why we decided to go with BlackRock, is that typically when you look at how they invest this is the first step of a much longer-term relationship that we will have with them over time that has different elements that we can tap into as the company scales,” Wassenaar told TechCrunch.

In terms of the arrangement, rather than BlackRock taking a stake in the company, Puppet will pay back the money. “We’ve borrowed a sum of money that we will pay back over time. BlackRock does have a board observer seat, and that’s really because they’re very interested in working with us on how we grow and accelerate the business,” Wassenaar said.

Puppet has been in the process of rebuilding its executive team, with Wassenaar coming on board about 18 months ago. Last year she brought in industry veterans Erik Frieberg and Paul Heywood as CMO and CRO, respectively. This year she brought in former Cloud Foundry Foundation director Abby Kearns to be CTO.

All of these moves are with an eye to a future IPO, says Wassenaar. “We’re looking at how do we progress ultimately, ideally on a path to an IPO, and what is it going to take for Puppet to go through that journey,” she said.

She points out that in some ways, the pandemic has forced companies to look more closely at automation solutions like the ones that Puppet provides. “What’s really interesting is […] that the pandemic in many ways has put wind in our sails in terms of the need for corporations to automate and think about how they leverage and extend from a technology perspective going forward,” she said.

As Puppet continues to grow, she says that diversity is a core organizational value, and that while the company has made progress from a gender perspective (as illustrated by the presence of her and Kearns in the C Suite), they still are working at being more racially diverse.

“Where I believe we have a lot more work and there’s a lot more focus right now is further complementing that [gender diversity] from a racial perspective. And it’s an area that I have personally taken on, and I’m committed to making changes in the company as we go forward to support more racial diversity as well,” she said.

Previously the company had raised almost $150 million, with the most recent round being a $42 million Series F in 2018, according to Crunchbase data. The company previously took $22 million in debt financing in 2016, prior to Wassenaar coming on board.

Powered by WPeMatico

Qumulo, a Seattle storage startup helping companies store vast amounts of data, announced a $125 million Series E investment today on a $1.2 billion valuation.

BlackRock led the round with help from Highland Capital Partners, Madrona Venture Group, Kleiner Perkins and new investor Amity Ventures. The company reports it has now raised $351 million.

CEO Bill Richter says the valuation is more than 2x its most recent round, a $93 million Series D in 2018. While the valuation puts his company in the unicorn club, he says that it’s more important than simple bragging rights. “It puts us in the category of raising at a billion-plus dollar level during a very complicated environment in the world. Actually, that’s probably the more meaningful news,” he told TechCrunch.

It typically hasn’t been easy raising money during the pandemic, but Richter reports the company started getting inbound interest in March just before things started shutting down nationally. What’s more, as the company’s quarter closed at the end of April, they had grown almost 100% year over year, and beaten their pre-COVID revenue estimate. He says they saw that as a signal to take additional investment.

“When you’re putting up nearly 100% year over year growth in an environment like this, I think it really draws a lot of attention in a positive way,” he said. And that attention came in the form of a huge round that closed this week.

What’s driving that growth is that the amount of unstructured data, which plays to the company’s storage strength, is accelerating during the pandemic as companies move more of their activities online. He says that when you combine that with a shift to the public cloud, he believes that Qumulo is well positioned.

Today the company has 400 customers and more than 300 employees, with plans to add another 100 before year’s end. As he adds those employees, he says that part of the company’s core principles includes building a diverse workforce. “We took the time as an organization to write out a detailed set of hiring practices that are designed to root out bias in the process,” he said.

One of the keys to that is looking at a broad set of candidates, not just the ones you’ve known from previous jobs. “The reason for that is that when you force people to go through hiring practices, you open up the position to a broader, more diverse set of candidates and you stop the cycle of continuously creating what I call ‘club memberships’, where if you were a member of the club before you’re a member in the future,” he says.

The company has been around since 2012 and spent the first couple of years conducting market research before building its first product. In 2014 it released a storage appliance, but over time it has shifted more toward hybrid solutions.

Powered by WPeMatico

American automotive technology startup Rivian has raised $1.3 billion in new funding, the company announced today. The new investment is the fourth round of capital announced by the company in 2019 alone, following prior announcements of $700 million led by Amazon, $500 million from Ford (which includes a collaboration on electric vehicle technology) and $350 million from Cox Automotive.

That’s a lot of money, but Rivian’s not your typical startup, as it’s aiming to bring fully electric vehicles to market, including the R1T pickup truck and the R1S sport utility vehicle. Both of those are consumer cars, which the company aims to bring to market starting at the end of next year — and Rivian is also working with Amazon on all-electric delivery vans, of which the commerce giant has ordered 100,000, with a target of starting deliveries of the first of those in 2021.

Rivian’s new monster round includes participation from Amazon and Ford Motor Company, along with funds advised by T. Rowe Price Associates and BlackRock, the company said in a release. It’s not adding any new board seats attached to this funding, and it’s not sharing any further details on the specific funds involved in the investment at this time.

The company, founded in 2009, has R&D facilities in a number of cities globally, and also has a 2.6-million-square-foot manufacturing facility in Normal, Ill. It debuted its pickup and SUV at the LA Auto Show last November, and the vehicles will launch with higher-end trim levels first, including up to 410 miles of range on a single charge. Base prices for the R1T pickup start at $69,000 before any tax credits are applied, while the R1S SUV starts at $72,500; Rivian has been taking pre-order reservations, available with a $1,000 deposit.

For a company that in many ways has seemed to appear out of nowhere, Rivian’s capitalization and partnerships make it one of the better existing contenders to take on Tesla, especially in the truck and SUV categories, where Tesla has less presence, with only the high-end Model X actually available to purchase so far.

Powered by WPeMatico

In a wide-ranging conversation at TechCrunch Disrupt San Francisco last week, Postmates co-founder and chief executive officer Bastian Lehmann made light of the company’s lack of IPO documents.

The San Francisco-based on-demand delivery business was expected to publicly file its IPO prospectus in September in preparation for a fall exit, sources familiar with the matter told TechCrunch this summer. September, however, has come and gone and we’re still waiting on Postmates to release the critical document.

“The reality is that we will IPO when we believe we find the right time for the business and the right time for the markets,” Lehmann told TechCrunch. “And if you look at the markets right now, I believe they are a little choppy. They are a little choppy when it comes to growth companies specifically … We are hopeful that we find a good window to get out there.”

Lehmann made reference to Uber and other companies to recently float, citing market conditions as an IPO deterrent. Uber, Lyft, Slack and other fast-growing unicorns have struggled since entering the public markets earlier this year despite sky-high private market valuations. WeWork, a money-losing endeavor, recently decided to delay its IPO after demand from Wall Street devalued the business by the billions. Whether Postmates will complete its debut by the end of the year is unclear.

Postmates confidentially filed with the U.S. Securities and Exchange Commission for an IPO in February. Shortly after, Postmates held M&A talks with DoorDash, another food delivery unicorn, according to people familiar with the matter, but failed to come to mutually favorable terms. DoorDash has previously declined to comment on these reports. On stage last week, Lehmann declined to confirm the reports.

“I don’t think it does any good to speculate on M&A,” he said. “I think you have four well-funded players here in the U.S. in this space. I think everyone is well aware of the strengths and the weaknesses of each other and you know at some point down the line, if we take Europe for example, you will see consolidation in the market. People have conversations all the time but I wouldn’t read too much into it.”

Postmates operates its on-demand delivery platform, powered by a network of local gig economy workers, in more than 3,500 cities across all 50 states. The company does not yet operate in any international markets aside from Mexico City, however, Lehmann’s comments suggest the business could be plotting a foray into Europe, where Deliveroo, Just Eat and others dominate the market.

Postmates has raised about $900 million to date, including a $225 million round announced last month that valued the company at $2.4 billion. DoorDash, on the other hand, reached a $12.6 billion valuation in May with a $600 million Series G and has raised more than double that of Postmates. When asked why DoorDash, a similar and competing business, needed that much more capital, Lehmann joked “Maybe [DoorDash CEO Tony Xu] needs a jet, I don’t know.”

Postmates, founded in 2011 by Lehmann, is backed by Spark Capital, Founders Fund, Uncork Capital, Slow Ventures, Tiger Global, Blackrock and others. In our interview with Lehmann, the long-time CEO discussed the ‘choppy’ public markets, competitors, the company’s autonomous robotics delivery efforts and more.

Powered by WPeMatico