Bitcoin

Auto Added by WPeMatico

Auto Added by WPeMatico

Erik Finman is a twenty-something bitcoin maximalist as famous for his precocity as he is for his $12 bet on the currency a few years ago.

Now, Finman, who built his first company while still in high school, is launching a new startup called CoinBits, which allows users to passively invest in bitcoin.

The idea, according to Finman, is to democratize access to the currency by letting everyday folks invest nominal sums through well-known mechanisms like roundups on transactions made with a credit or debit card or through regular transactions from a customer’s savings or checking account to bitcoin through CoinBits.

Every transaction also helps Finman’s own bitcoin holdings grow, and makes the young entrepreneur a little wealthier himself through his bitcoin holdings.

Users can make one-time investments of $10, $25, $50 or $100 through the web-based platform and can establish a level of risk for their holdings.

Finman’s app collects no commissions on transactions, and 98% of the bitcoin is stored offline — for safety.

“Overall, investing in bitcoin is complicated and can feel almost impossible,” said Finman. “Coinbits allows you to put that spare change in bitcoin. For example, if you spend $1.75 on French fries, that remaining 25 cents is invested automatically.”

Withdrawals are handled by CoinBits, which will give users same-day processing for a 50 cent-fee, and offers an easily downloadable record for accountants to deal with any gains or losses associated with bitcoin.

Given the fractional nature of these investments, and the volatility of bitcoin, it’s hard to know what real value investors can reap from these small transactions, but it’s a less risky way to experiment with building bitcoin holdings than take a huge flyer on the market.

Powered by WPeMatico

Crypto represent a “border-less” asset that anyone can own, but actually getting hold of it isn’t easy for everyone. Amun, a company that wants to make buying crypto as easy as stock, has pulled in $4 million in funding to offer more established channels for crypto ownership.

The startup currently offers punters an ETP (exchange-traded product) on the Swiss Stock Exchange that pulls together five of the most popular crypto assets: Bitcoin, Ethereum, Bitcoin Cash, XRP and Litecoin. HODL — as it is called after “holding” crypto rather than selling it (LOL) — can be purchased just like any stock.

That five-crypto basket is just the start for Amun, which is developing ETPs for other crypto assets individually. The first one is for Bitcoin — ABTC — with others planned to come soon; you’d imagine the usual suspects such as Ethereum and co will follow. Indeed, Amun has licenses to the five crypto assets in HODL as well as EOS.

While the products are ETP and not covered by Collective Investment Schemes Act (CISA), they are protected in custody and by insurance. They are collateralized and backed by an identical amount of crypto assets.

Personally, I’ve been able to buy crypto — just base tokens like Bitcoin and Ethereum rather than company-specific ICO tokens — but it certainly is true that it takes some learning. While, speaking for me and likely many others, exchange-based products aren’t easier to me, it does appeal to more institutionally minded individuals or companies for whom holding an account with an exchange or a crypto wallet isn’t feasible. That’s the target that Amun has in mind, as well as outlier cases, too.

Amun CEO and co-founder Hany Rashwan told TechCrunch that growing up in Egypt, he saw the government ban Bitcoin despite the fact that it offered an alternative to the Egyptian pound, which saw its valuation tank massively in 2016. He believes that products like Amun allow anyone to take part in crypto even when they face local restrictions, as was the case in Egypt and other countries.

“We want to make investing in crypto as easy as buying a stock. Institutional investors around the world are looking for a secure, easy and regulated way of accessing the crypto asset class. Amun’s products do that at a low price in one of the most reputable financial hubs in the world,” Rashwan told TechCrunch.

Investors share his optimism and those who took part in this round include Boost VC founder Adam Draper — son of outspoken pro-Bitcoin VC Tim Draper — Graham Tuckwell, founder of ETFS Capital who built ETF products for gold, and Greg Kidd, co-founder of investment firm Hard Yaka. Four undisclosed family offices also took part.

One reason for their optimism is the fact that Amun is developing technology that could, in theory, be licensed out to allow others to develop their own ETFs.

“We invest a ton of resources in both our product development and underlying tech infrastructure. This allows us to come up with innovative but professional and safe ways of accessing the crypto asset class, as well as do all this on a tech platform that can be used by not just us, but any issuer that wishes to do the same as well,” Rashwan said.

“The world needs a company like Amun to make crypto as easy as buying a stock. Now that they were the first to do that, they can now provide the toolset and be the de facto platform for anyone else looking to take their crypto assets/securities to the public markets,” Draper added.

Still, just giving people access doesn’t guarantee returns — that’s on the crypto market itself.

Last year was a dud across the board in terms of pricing, as Bitcoin, for example, plummeted from a record high of nearly $20,000 at the end of 2017 to $3,930-ish at the time of writing. Plenty in the industry are optimistic that will change as genuine value comes out of blockchain technology.

HODL itself debuted at $15.64 last November; today it is at $12.83

Note: The author owns a small amount of cryptocurrency. Enough to gain an understanding, not enough to change a life.

Powered by WPeMatico

Until now, the Exodus 1 has, fittingly, only been available for purchase with cryptocurrency. Starting today, however, interested parties will be able to pick HTC’s blockchain phone up through more traditional means, including USD, which prices the handset at a not unreasonable $699.

One assumes, of course, if you’ve got enough of an interested in purchasing a blockchain phone that they’ve already got a bit of Bitcoin, Ether or Litecoin lying about. This move, however, is very clearly about helping growing the product beyond its initial soft launch. When the device was released last year, HTC was pretty clearly expecting to sell it in limited quantities to users who could essentially help beta test the product in the wild.

HTC Decentralized Chief Officer Phil Chen calls the product the company’s 1.0 solution. In fact, it’s planning to create a formal bounty program to discover and patch potential exploits.

But HTC has long held that a device like this will play an important role in the future of a company struggling to find its way as it feels the burn of a stagnating mobile industry. As project head and Chen told me on stage at a TechCrunch event in Shenzhen last year that HTC is “as committed as they are to the Vive. I don’t think it’s number one of the priority list, but I would say it’s number three or four.”

When I spoke to Chen again this month, just ahead of today’s Mobile World Congress announcement, he told me that HTC currently has 25 engineers committed to the project. It’s perhaps not a huge number in the grand scheme of a company the size of HTC, but it’s a sizable chunk of manpower, considering the fact that the product is mostly built using existing HTC hardware. The company has also brought in outside help like blockchain security expert Christopher Allen to make sure things are as secure as possible.

And indeed, I’ve been carrying an Exodus One around for about a week now, and it feels like a pretty standard HTC handset, both in terms of hardware and Android software, right down to the inclusion the size-squeezing Edge Sense.

Powered by WPeMatico

It was the Lehman Brothers of blockchain. 850,000 Bitcoin disappeared when cryptocurrency exchange Mt. Gox imploded in 2014 after a series of hacks. The incident cemented the industry’s reputation as frighteningly insecure. Now a controversial crypto celebrity named Brock Pierce is trying to get the Mt. Gox flameout’s 24,000 victims their money back and build a new company from the ashes.

Pierce spoke to TechCrunch for the first interview about Gox Rising — his plan to reboot the Mt. Gox brand and challenge Coinbase and Binance for the title of top cryptocurrency exchange. He claims there’s around $630 million and 150,000 Bitcoin waiting in the Mt. Gox bankruptcy trust, and Pierce wants to solve the legal and technical barriers to getting those assets distributed back to their rightful owners.

The consensus from several blockchain startup CEOs I spoke with was that the plot is “crazy”, but that it also has the potential to right one of the biggest wrongs marring the history of Bitcoin.

But the story starts with Magic: The Gathering. Mt. Gox launched in 2006 as a place for players of the fantasy card game to trade monsters and spells before cryptocurrency came of age. The Magic: The Gathering Online eXchange wasn’t designed to safeguard huge quantities of Bitcoin from legions of hackers, but founder Jed McCaleb pivoted the site in 2010. Seeking to focus on other projects, he gave 88 percent of the company to French software engineer Mark Karpeles, and kept 12 percent. By 2013, the Tokyo-based Mt. Gox had become the world’s leading cryptocurrency exchange, handling 70 percent of all Bitcoin trades. But security breaches, technology problems, and regulations were already plaguing the service.

Then everything fell apart. In February 2014, Mt. Gox halted withdrawls due to what it called a bug in Bitcoin, trapping assets in user accounts. Mt. Gox discovered that it had lost over 700,000 Bitcoins due to theft over the past few years. By the end of the month, it had suspended all trading and filed for bankruptcy protection, which would contribute to a 36 percent decline in Bitcoin’s price. It admitted that 100,000 of its own Bitcoin atop 750,000 owned by customers had been stolen.

Mt. Gox is now undergoing bankruptcy rehabilitation in Japan overseen by court-appointed trustee and veteran bankruptcy lawyer Nobuaki Kobayashi to establish a process for compensating the 24,000 victims who filed claims. There’s now 137,892 Bitcoin, 162,106 Bitcoin Cash, and some other forked coins in Mt. Gox’s holdings, along with $630 million from the sale of 25 percent of the Bitcoin Kobayashi handled at a precient price point above where it is today. But five years later, creditors still haven’t been paid back.

Brock Pierce, the eccentric crypto celebrity

Pierce had actually tried to acquire Mt. Gox in 2013. The child actor known from The Mighty Ducks had gone on to work with a talent management company called Digital Entertainment Network. But accusations of sex crime led Pierce and some team members to flee the US to Spain until they were extradited back. Pierce wasn’t charged and paid roughly $21,000 to settle civil suits, but his cohorts were convicted of child molestation and child pornography.

The situation still haunts Pierce’s reputation and makes some in the industry apprehensive to be associated with him. But he managed to break into the virtual currency business, setting up World Of Warcraft gold mining farms in China. He claims to have eventually run the world’s largest exchanges for WOW Gold and Second Life Linden Dollars.

Soon Pierce was becoming a central figure in the blockchain scene. He co-founded Blockchain Capital, and eventually the EOS Alliance as well as a “crypto utopia” in Puerto Rico called Sol. His eccentric, Burning Man-influenced fashion made him easy to spot at the industry’s many conferences.

As Bitcoin and Mt. Gox rose in late 2012, Pierce tried to buy it, but “my biggest investor was Goldman Sachs. Goldman was not a fan of me buying the biggest Bitcoin exchange” due to the regulatory issues, Pierce tells me. But he also suspected the exchange was built on a shaky technical foundation that led him to stop pursuing the deal. “I thought there was a big risk factor in the Mt. Gox back-end. That was may intuition and I’m glad I was because my intuition was dead right.”

After Mt. Gox imploded, Pierce claims his investment group Sunlot Holdings successfully bought founder McCaleb’s 12 percent stake for 1 Bitcoin, though McCaleb says he didn’t receive the Bitcoin and it’s not clear if the deal went through. Pierce also claims he had a binding deal with Karpeles to buy the other 88 percent of Mt. Gox, but that Karpeles tried to pull out of the deal that remains in legal limbo.

The Sunlot has since been trying to handle the bankruptcy proceedings, but that arrangement was derailed by a lawsuit from CoinLab. That company had partnered with Mt. Gox to run its North American operations but claimed it never received the necessary assets, and sued Mt. Gox for $75 million, though Mt. Gox countersued saying CoinLab wasn’t legally certified to run the exchange in the US and that it hadn’t returned $5.3 million in customer deposits. For a detailed account the tangle of lawsuits, check out Reuters’ deep-dive into the Mt. Gox fiasco.

CoinLab co-founder Peter Vessenes

This week, CoinLab co-founder Peter Vessenes increased the claim and is now seeking $16 billion. Pierce alleges “this is a frivolous lawsuit. He’s claiming if [the partnership with Mt. Gox] hadn’t been cancelled, CoinLab would have been Coinbase and is suing for all the value. He believes Coinbase is worth $16 billion so he should be paid $16 billion. He embezzled money from Mt. Gox, he committed a crime, and he’s trying to extort the creditors. He’s holding up the entire process hoping he’ll get a payday.” Later, Pierce reiterated that “Coinlab is the villain trying to take all the money and see creditors get nothing.” Industry sources I spoke to agreed with that characterization

Mt. Gox customers worried that they might only receive the cash equivalent of their Bitcoin according to the currency’s $486 value when Gox closed in 2014. That’s despite the rise in Bitcoin’s value rising to around 7X that today, and as high as 40X at the currency’s peak. Luckily, in June 2018 a Japanese District Court halted bankruptcy proceedings and sent Mt. Gox into civil rehabilitation which means the company’s assets would be distributed to its creditors (the users) instead of liquidated. It also declared that users would be paid back their lost Bitcoin rather than the old cash value.

Now Pierce and Sunlot are attempting another rescue of Mt. Gox’s $1.2 billion assets. He wants to track down the remaining cryptocurrency that’s missing, have it all fairly valued, and then distribute the maximum amount to the robbed users with Mt. Gox equity shareholders including himself receiving nothing. That’s a much better deal for creditors than if Mt. Gox paid out the undervalued sum, and then shareholders like Pierce got to keep the Bitcoins or proceeds of their sale at today’s true value. “I‘ve been very blessed in my life I did commit to giving my first billion away” Pierce notes, joking that this plan could account for the first $700 million he plans to ‘donate’.

“Like Game Of Thrones, the last season of Mt. Gox hasn’t been written” Pierce tells me, speaking in terms HBO’s Silicon Valley would be quick to parody. “What kind of ending do we want to make for it? I’m a Joseph Campbell fan so I’m obviously going to go with a hero’s journey, with a rise and a fall, and then a rise from the ashes like a phoenix.”

But to make this happen, Sunlot needs at least half of those Mt. Gox users seeking compensation, or roughly 12,000 that represent the majority of assets, to sign up to join a creditors committee. That’s where GoxRising.com comes in. The plan is to have users join the committee there so they can present a united voice to Kobayashi about how they want Mt. Gox’s assets distributed. “I think that would allow the process to move faster than it would otherise. Things are on track to be resolved in the next three to five years. If [a majority of creditors sign on] this could be resolved in maybe 1 year.

Beyond providing whatever the Mt. Gox estate pays out, Pierce wants to create a Gox Coin that gives original Mt Gox creditors a stake in the new company. He plans to have all of Mt. Gox’s equity wiped out, including his own. Then he’ll arrange to finance and tokenize an independent foundation governed by the creditors that will seek to recover additional lost Mt. Gox assets and then distribute them pro rata to the Gox Coin holders. There are plenty of unanswered questions about the regulatory status of a Gox Coin and what holders would be entitled to, Pierce admits.

Meanwhile, Pierce is bidding to buy the intangibles of Mt. Gox, aka the brand and domain. He wants to then relaunch it as a Gox or Mt. Gox exchange that doesn’t provide custody itself for higher security.

“We want to offer [creditors] more than the bankruptcy trustee can do on its own” Pierce tells me. He concedes that the venture isn’t purely altruistic. “If the exchange is very successful I stand to benefit sometime down the road.” Still, he stands by his plan, even if the revived Mt. Gox never rises to legitimately challenge Binance, Coinbase, and other leading exchanges. Pierce concludes, “Whether we’re successful or not, I want to see the creditors made whole.” Those creditors will have to decide for themselves who to trust.

Powered by WPeMatico

Taiwanese technology giant Foxconn International is backing Carbon Relay, a Boston-based startup emerging from stealth today that’s harnessing the algorithms used by companies like Facebook and Google for artificial intelligence to curb greenhouse gas emissions in the technology industry’s own backyard — the data center.

Already, the computing demands of the technology industry are responsible for 3 percent of total energy consumption — and the addition of new technologies like Bitcoin to the mix could add another half a percent to that figure within the next few years, according to Carbon Relay’s chief executive, Matt Provo.

That’s $25 billion in spending on energy per year across the industry, Provo says.

A former Apple employee, Provo went to Harvard Business School because he knew he wanted to be an entrepreneur and start his own business — and he wanted that business to solve a meaningful problem, he said.

Variability and dynamic nature of the data center relating to thermodynamics and the makeup of a facility or building is interesting for AI because humans can’t keep up.

“We knew what we wanted to focus on,” said Provo of himself and his two co-founders. “All three of us have an environmental sciences background as well… We were fired up about building something that was true AI that has positive value… the risk associated [with climate change] is going to hit in our lifetime, we were very inspired to build a company whose technology would have an impact on that.”

Carbon Relay’s mission and founding team, including Thibaut Perol and John Platt (two Harvard graduates with doctorates in applied mathematics) was able to attract some big backers.

The company has raised $6 million from industry giants like Foxconn and Boston-based angel investors, including Dr. James Cash — a director on the boards of Walmart, Microsoft, GE and State Street; Black Duck Software founder, Douglas Levin; Karim Lakhani, a director on the Mozilla Corporation board; and Paul Deninger, a director on the board of the building operations management company, Resideo (formerly Honeywell).

Provo and his team didn’t just raise the money to tackle data centers — and Foxconn’s involvement hints at the company’s broader goals. “My vision is that commercial HVAC systems or any machinery that operates in a business would not ship without our intelligence inside of it,” says Provo.

What’s more compelling is that the company’s technology works without exposing the underlying business to significant security risks, Provo says.

“In the end all we’re doing are sending these floats… these values. These values are mathematical directions for the actions that need to be taken,” he says.

Carbon Relay is already profitable, generating $4 million in revenue last year and on track for another year of steady growth, according to Provo.

Carbon Relay offers two products: Optimize and Predict, that gather information from existing HVAC devices and then control those systems continuously and automatically with continuous decision making.

“Each data center is unique and enormously complex, requiring its own approach to managing energy use over time,” said Cash, who’s serving as the company’s chairman. “The Carbon Relay team is comprised of people who are passionate about creating a solution that will adapt to the needs of every large data center, creating a tangible and rapid impact on the way these organizations do business.”

Powered by WPeMatico

The Intercontinental Exchange’s (ICE) cryptocurrency project Bakkt celebrated New Year’s Eve with the announcement of a $182.5 million equity round from a slew of notable institutional investors. ICE, the operator of several global exchanges, including the New York Stock Exchange, established Bakkt to build a trading platform that enables consumers and institutions to buy, sell, store and spend digital assets.

This is Bakkt’s first institutional funding round; it was not a token sale. Participating in the round are Horizons Ventures, Microsoft’s venture capital arm (M12), Pantera Capital, Naspers’ fintech arm (PayU), Protocol Ventures, Boston Consulting Group, CMT Digital, Eagle Seven, Galaxy Digital, Goldfinch Partners and more.

Bakkt is currently seeking regulatory approval to launch a one-day physically delivered Bitcoin futures contract along with physical warehousing. The startup initially planned for a November 2018 launch, but confirmed this morning an earlier CoinDesk report that it was delaying the launch to “early 2019” as it awaits permission from the Commodity Futures Trading Commission. Along with the funding, crypto news blog The Block Crypto also reports Bakkt has hired Balaji Devarasetty, a former vice president at Vantiv, as its head technology.

ICE’s crypto project was first announced in August and is led by chief executive officer Kelly Loeffler, ICE’s long-time chief communications and marketing officer. Bakkt quickly inked partnerships with Microsoft, which provides cloud infrastructure to the service, and Starbucks, to develop “practical, trusted and regulated applications for consumers to convert their digital assets into U.S. dollars for use at Starbucks,” Starbucks vice president of payments Maria Smith said in a statement at the time.

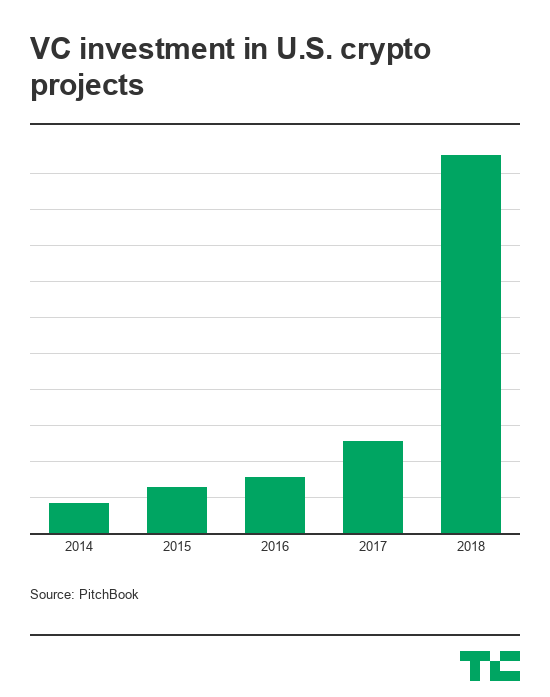

Many Bitcoin startups floundered in 2018, despite record amounts of venture capital invested in the industry. This was as a result of failed initial coin offerings, an inability to scale following periods of rapid growth and the falling price of Bitcoin. Still, VCs remained bullish on Bitcoin and blockchain technology in 2018, funneling a total of $2.2 billion in U.S.-based crypto projects — a nearly 4x increase year-over-year. Around the globe, investment hit a high of $4.6 billion — a more than 4x increase from last year, according to PitchBook.

“Notably, 2018 was the most active year for crypto in its brief ten-year history,” Loeffler wrote. “This was evidenced by rising investment in distributed ledger technology and digital assets, as well as by blockchain network metrics such as daily bitcoin transaction value and active addresses. Yet, these milestones tend to be overshadowed by the more narrow focus on bitcoin’s price, which has been seen by some, as a proxy for the potential of the technology.”

Today, the price of Bitcoin is hovering around $3,700 one year after a historic run valued the cryptocurrency at roughly $20,000. The crash caused many to dismiss Bitcoin and its underlying technology, while others remained committed to the tech and its potential for complete financial disruption. A project like Bakkt, created in-house at a respected financial institution with support from noteworthy businesses, is a logical bet for crypto and traditional private investors alike.

“The path to developing new markets is rarely linear: progress tends to modulate between innovation, dismissal, reinvention, and, finally, acceptance,” Loeffler added. “Each step, whether part of discovery or adversity, ultimately strengthens the product. Twenty years ago, it was controversial to suggest that commodities or bonds could trade electronically on a screen, and many steps were required for that evolution to play out.”

Powered by WPeMatico

I’ve been thinking hard about the concept of sponsored content — you can find some of it on TechCrunch if you look hard enough, and it appears almost everywhere else. It’s an important consideration, because as an online journalist I’ve heard everything from “How much did Apple pay you to post this?” to “How much can I pay you to post something to TechCrunch?”

And I’m sick of it.

Journalists afflict the comfortable and comfort the afflicted. Marketers comfort the comfortable. The only person who wins in that struggle is the guy with the biggest wallet to buy as much coverage as possible. Crypto, for all its faults, promises to change that.

Now I’d like to introduce something else I built (and I never do this on TC so I think it’s pretty important and interesting). It’s called HypeHop and it’s an experiment in sponsored video. Most sponsored video appears in front of your YouTube selections like a cold sore — you know it’s there, it’s unwanted and you know it will take a while for it to go away. For example, this deeply applicable ad appeared as my son was watching Nerf videos, for example, proving that algorithms aren’t always the smartest.

Enough.

In the current system marketers pay media platforms for their audience. The marketer gets eyeballs, the media platform gets money and the user gets bupkus. I wanted to try to change that.

With a few friends I made something called HypeHop. It basically pays you for watching videos. At this point it’s a proof-of-concept that accepts uploaded videos, a small payment for hosting, and then watches the viewer to ensure they are watching the video. “Watching the viewer?,” you ask? Sure. We’re being surveilled every day. Isn’t it time we were paid for it?

Viewers currently get about 40 cents in BTC per view. I created a demo video with my son here to show off how it worked and preseeded some videos with BTC to test. Thus far it’s been an interesting experiment.

I’d love to talk to like-minded folks about expanding this technology. I could, for example, see this as a tool to make sponsored posts more interesting to readers — who doesn’t want a few pennies for reading marketing dross — and a way to monetize many marketing tools for readers, producers and marketers. Ultimately this is a win-win-win in a win-win-lose world and it’s vitally important we look at it as a way forward in our fight against fake news and faker marketing.

Powered by WPeMatico

Bitcoin turned 10 years old, a milestone for a technology that few have used and even fewer understand. Ultimately, the blockchain it wrought could be the biggest change to banking, finance and politics ever — or it could be a dud. The jury is still out, but let’s take a walk down memory lane and see just how the product grew from White Paper to world beater.

Powered by WPeMatico

Watching the current price madness is scary. Bitcoin is falling and rising in $500 increments with regularity and Ethereum and its attendant ICOs are in a seeming freefall with a few “dead cat bounces” to keep things lively. What this signals is not that crypto is dead, however. It signals that the early, elated period of trading whose milestones including the launch of Coinbase and the growth of a vibrant (if often shady) professional ecosystem is over.

Crypto still runs on hype. Gemini announcing a stablecoin, the World Economic Forum saying something hopeful, someone else saying something less hopeful – all of these things and more are helping define the current market. However, something else is happening behind the scenes that is far more important.

As I’ve written before, the socialization and general acceptance of entrepreneurs and entrepreneurial pursuits is a very recent thing. In the old days – circa 2000 – building your own business was considered somehow sordid. Chancers who gave it a go were considered get-rich-quick schemers and worth of little more than derision.

As the dot-com market exploded, however, building your own business wasn’t so wacky. But to do it required the imprimaturs and resources of major corporations – Microsoft, Sun, HP, Sybase, etc. – or a connection to academia – Google, Netscape, Yahoo, etc. You didn’t just quit school, buy a laptop, and start Snapchat.

It took a full decade of steady change to make the revolutionary thought that school wasn’t so great and that money was available for all good ideas to take hold. And take hold it did. We owe the success of TechCrunch and Disrupt to that idea and I’ve always said that TC was career pornography for the cubicle dweller, a guilty pleasure for folks who knew there was something better out there and, with the right prodding, they knew they could achieve it.

So in looking at the crypto markets currently we must look at the dot-com markets circa 1999. Massive infrastructure changes, some brought about by Y2K, had computerized nearly every industry. GenXers born in the late 70s and early 80s were in the marketplace of ideas with an understanding of the Internet the oldsters at the helm of media, research, and banking didn’t have. It was a massive wealth transfer from the middle managers who pushed paper since 1950 to the dot-com CEOs who pushed bits with native ease.

Fast forward to today and we see much of the same thing. Blockchain natives boast about having been interest in bitcoin since 2014. Oldsters at banks realize they should get in on things sooner than later and price manipulation is rampant simply because it is easy. The projects we see now are the Kozmo.com of the blockchain era, pie-in-the-sky dream projects that are sucking up millions in funding and will produce little in real terms. But for every hundred Kozmos there is one Amazon .

And that’s what you have to look for.

Will nearly every ICO launched in the last few years fail? Yes. Does it matter?

Not much.

The market is currently eating its young. Early investors made (and probably lost) millions on early ICOs but the resulting noise has created an environment where the best and brightest technical minds are faced with not only creating a technical product but also maintaining a monetary system. There is no need for a smart founder to have to worry about token price but here we are. Most technical CEOs step aside or call for outside help after their IPO, a fact that points to the complexity of managing shareholder expectations. But what happens when your shareholders are 16-year-olds with a lot of Ethereum in a Discord channel? What happens when little Malta becomes the de facto launching spot for token sales and you’re based in Nebraska? What happens when the SEC, FINRA, and Attorneys General from here to Beijing start investigating your hobby?

Basically your hobby stops becoming a hobby. Crypto and blockchain has weaponized nerds in an unprecedented way. In the past if you were a Linux developer or knew a few things about hardware you could build a business and make a little money. Now you can build an empire and make a lot of money.

Crypto is falling because the people in it for the short term are leaving. Long term players – the Amazons of the space – have yet to be identified. Ultimately we are going to face a compression in the ICO and, for a while, it’s going to be a lot harder to build an ICO. But give it a few years – once the various financial authorities get around to reading the Satoshi white paper – and you’ll see a sea change. Coverage will change. Services will change. And the way you raise money will change.

VC used to be about a team and a dream. Now it’s about a team, $1 million in monthly revenue, and a dream. The risk takers are gone. The dentists from Omaha who once visited accelerator demo days and wrote $25,000 checks for new apps are too shy to leave their offices. The flashy VCs from Sand Hill have to keep Uber and Airbnb’s plates spinning until they can cash out. VC is dead for the small entrepreneur.

Which is why the ICO is so important and this is why the ICO is such a mess right now. Because everybody sees the value but nobody – not the SEC, not the investors, not the founders – can understand how to do it right. There is no SAFE note for crypto. There are no serious accelerators. And all of the big names in crypto are either goldbugs, weirdos, or Redditors. No one has tamed the Wild West.

They will.

And when they do expect a whole new crop of Amazons, Ubers, and Oracles. Because the technology changes quickly when there’s money, talent, and a way to marry the two in which everyone wins.

Powered by WPeMatico

In a delightful bit of irony BitBay, a Central European exchange, has shut down operations in Poland even as it received an invitation by the Polish government to participate in a national blockchain working group. The news, which appeared in a Tweet, states that the group will assess regulations for cryptocurrencies, blockchain, and ICOs.

“Our exchange has received an invitation from the PFSA to participate in the Blockchain Working Group.  As we have recently said, we do not want to abandon crypto activity in the Polish community,” wrote BitBay.

As we have recently said, we do not want to abandon crypto activity in the Polish community,” wrote BitBay.

Nasza giełda otrzymała zaproszenie z KNF do udziału w pracach Grupy roboczej ds. Blockchain.

— BitBay (@BitBayPolska) May 30, 2018

Poland has had an odd relationship with Bitcoin. First, some of the central banks funded a YouTube propaganda video that showed a person losing plenty of cash in crypto. Further, the community is fighting back but releasing counter-propaganda to the central bank’s policies.

After being shut out by Polish banks, BitBay moved its headquarters to Malta and stopped serving Polish customers.

Photo by freestocks.org on Unsplash

Powered by WPeMatico